Can the IRS Garnish Wages? Find Out How to Protect Your Paycheck

The IRS Wage Garnishment Authority: What You Need To Know

Can the IRS garnish wages? Sadly, the answer is yes. The IRS possesses broad authority to collect unpaid taxes. This includes the power to garnish wages, meaning they can legally compel your employer to withhold a portion of your earnings and send it directly to them to settle your tax debt.

Unlike other creditors, the IRS doesn't require a court order to garnish your wages. This power provides the IRS a significant advantage when collecting outstanding tax liabilities. However, there are specific procedures the IRS must follow.

Understanding these procedures is essential to protecting your paycheck. You might find this helpful: How to Stop IRS Wage Garnishment.

Understanding The IRS Garnishment Process

The IRS doesn't immediately start garnishing wages. There's a series of notices and opportunities to address the debt beforehand. The process typically begins with several notices regarding your outstanding tax liability.

This is followed by a critical notice: the Notice of Intent to Levy. This notice indicates the IRS's intention to seize assets, including your wages, to satisfy the debt. It’s not just a warning; it’s a serious step in the process.

The Notice of Intent to Levy grants you a 30-day window to respond. This period represents your best chance to avoid wage garnishment.

During this time, you can explore options such as full payment, setting up an installment agreement, or filing an appeal.

Failing to act within the 30-day timeframe can lead to the IRS issuing a levy notice to your employer. This action initiates the garnishment process. While they don't need a court order, the IRS must adhere to specific procedures.

Before garnishing wages, the IRS sends several notices. This includes a Notice of Intent to Levy and a Notice of Your Right to a Hearing, often called a Final Notice.

This generally provides the taxpayer 30 days to respond by paying the debt, setting up an installment agreement, or filing an appeal.

If there's no response within that timeframe, the IRS can begin garnishment. The IRS can garnish a substantial portion of an individual's income.

However, federal law typically limits garnishment to a maximum percentage of disposable earnings.

In general, agencies are limited to garnishing up to 15% of disposable earnings. Exceptions may apply based on individual circumstances.

Learn more about the details of the process here: Understanding Wage Garnishment by the IRS.

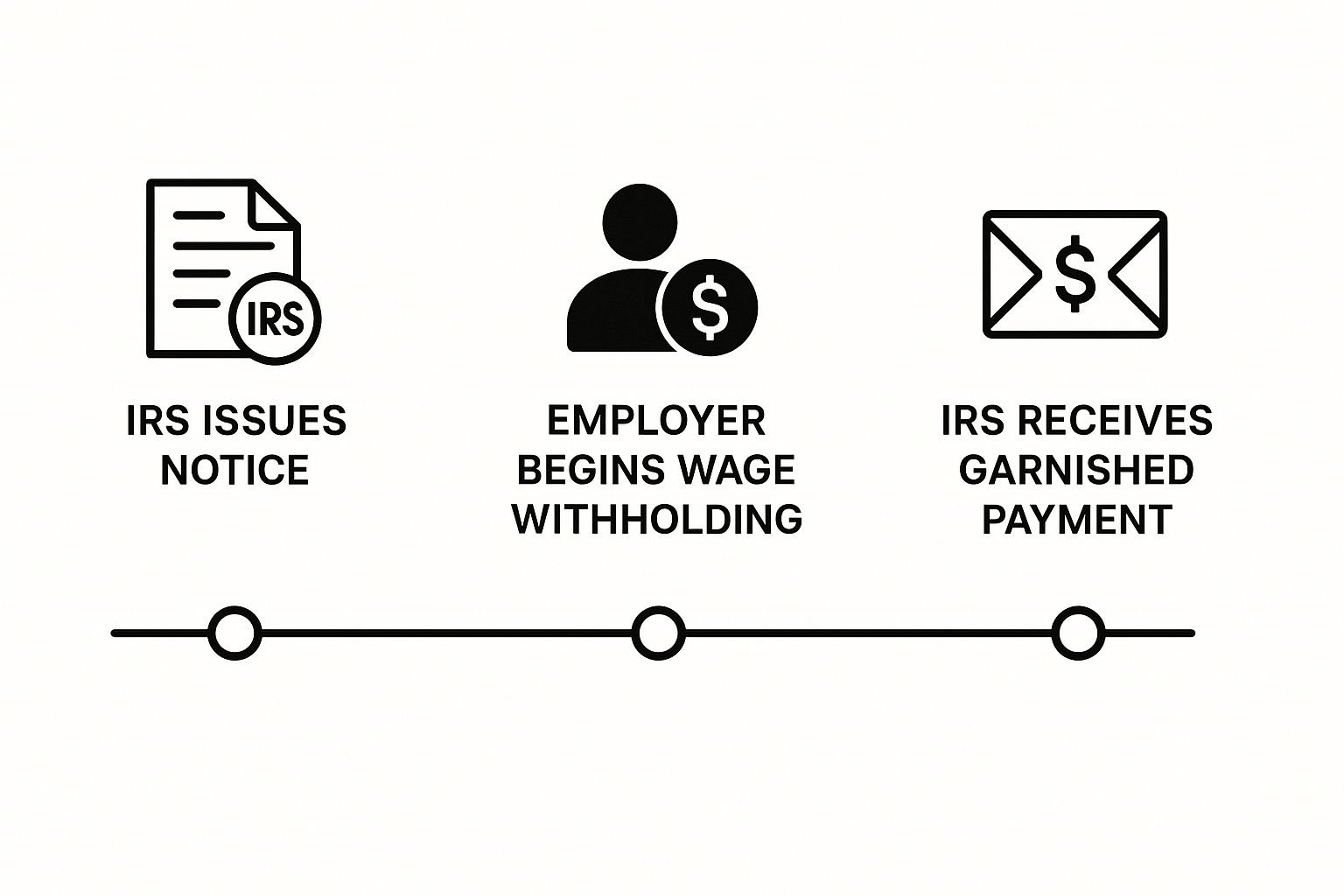

This infographic illustrates the timeline of IRS wage garnishment, from the first notice to the IRS receiving payment. The process involves several steps, providing multiple chances to act before your wages are affected.

To prevent future garnishments, consider tools to help manage your finances and legal paperwork efficiently. For instance, explore options such as legal document automation software.

Calculating Your Paycheck Protection: What the IRS Can Take

Facing the possibility of IRS wage garnishment can be incredibly stressful. One of the most common questions is, "How much of my paycheck can they actually take?" This section breaks down the IRS's calculations, offering clarity on how much of your earnings you can protect.

Decoding "Disposable Income"

The IRS can't simply garnish any amount they please. Calculations revolve around disposable income. This isn't your entire paycheck. Disposable income is the amount remaining after legally required deductions.

These include taxes (federal, state, and local), Social Security, and Medicare. Think of it as the money you have available for spending or saving.

Understanding Exemptions and the CCPA

The IRS must also follow federal law. U.S. wage garnishment laws aim to protect employees while still allowing debt collection. The Consumer Credit Protection Act (CCPA) sets limits on garnishment.

For example, with bi-weekly disposable earnings at or above $580, the CCPA allows garnishment of up to 25%, or $145.00. The IRS also follows specific exemption rules based on the standard deduction, protecting a portion of your income. This protection ensures you have enough to cover essential living expenses.

Calculating Your Specific Case

Let's use an example. Your bi-weekly gross pay is $1,200. After $300 in deductions, your disposable income is $900.

While 25% of this is $225, CCPA limitations might cap the garnishment lower, depending on how your disposable income compares to the federal minimum wage. This highlights the importance of understanding your specific situation.

Standard Deduction: Your Safety Net

The standard deduction plays a vital role in protecting your paycheck. This deduction lowers your taxable income, increasing your disposable income—the portion shielded from garnishment. A higher standard deduction safeguards more of your earnings.

Navigating Your Payroll and Finances

Communicating with your payroll department is essential. Ensure they understand the garnishment limits and correctly calculate your disposable income to prevent over-garnishment.

Creating a detailed budget during this time can also help manage your finances effectively despite the reduced income.

Understanding disposable income, exemptions, and the CCPA allows you to accurately assess your financial standing during wage garnishment. It empowers you to take control, plan effectively, and safeguard your financial well-being.

The Human Side of Garnishment: Who's Most Vulnerable

Beyond the legalities of IRS wage garnishment, it's essential to understand who is most affected. This isn't just a legal procedure; it significantly impacts real people's lives. Looking at the demographics reveals some surprising trends about those most often subject to tax levies.

The Age of Vulnerability

Surprisingly, middle-aged workers between 35 and 44 experience the highest rates of wage garnishment. This is often a time of significant financial strain, juggling growing career demands and increasing family responsibilities.

Mortgages, childcare, and education expenses all contribute to this precarious balancing act. This makes them particularly vulnerable when unexpected financial burdens, like tax debt, occur.

Industry Insights: Manufacturing vs. Service

The industry someone works in also plays a role. Data reveals that manufacturing workers face notably higher garnishment rates than those in the service industry.

This suggests that blue-collar jobs might come with increased financial pressures, making these workers more likely to fall behind on their tax obligations.

Wage garnishment, including actions by the IRS, impacts a substantial portion of the workforce. Approximately 7.6% of employees experience wage garnishment annually.

Garnishment rates are higher among employees of manufacturing companies than service companies. They are highest among the 35-44 age group, reaching 10.5%. Learn more about wage garnishment statistics.

The Gender Gap in Garnishment

While overall garnishment rates are similar for men and women, the reasons for these garnishments often differ. Men are more frequently garnished for child support, highlighting the gendered division of family responsibilities.

Other debt types contribute to similar overall rates for both genders, however, demonstrating that financial vulnerability affects everyone.

Protecting Your Pension

The implications of wage garnishment go beyond immediate financial hardship. It's important to consider long-term financial security, too.

You might be interested in: Can Pensions Be Garnished? Protection Strategies for Retirement.

Protecting your future income is just as critical as managing your current finances, especially when dealing with complex situations like tax debt.

Understanding the human impact of garnishment offers valuable context. Recognizing these vulnerabilities underscores the importance of proactive financial planning and addressing potential tax liabilities early.

Your Action Plan: Responding to IRS Garnishment Threats

Receiving an IRS notice about potential wage garnishment can be a stressful experience. Understanding the process and acting quickly, however, can make a real difference. This section provides a clear action plan, offering practical guidance to help you navigate this difficult situation.

Verifying the Debt and Understanding Your Rights

The first step after receiving an IRS notice is to verify its accuracy. Mistakes can happen. Check your IRS online account or request a tax transcript to confirm the debt amount. This ensures you're addressing the correct liability.

Also, it's important to understand your rights. The IRS must follow specific procedures, including sending multiple notices, before garnishing wages. Knowing these procedures helps you anticipate next steps and prepare accordingly.

Taking Action Before Garnishment Begins

The Notice of Intent to Levy is your main opportunity to prevent wage garnishment. This notice gives you a 30-day window to respond. During this time, you have several options.

Full Payment: If possible, paying the debt in full eliminates the threat entirely.

Installment Agreement: If full payment isn't feasible, an installment agreement allows you to pay the debt over time.

Offer in Compromise (OIC): An OIC allows you to settle for less than the full amount owed, but it requires demonstrating financial hardship.

Currently Not Collectible (CNC): If you can't pay anything due to severe hardship, CNC status may be an option. This temporarily pauses collection efforts, but interest and penalties continue to accrue. Learn more in our article about Ultimate Guide to IRS Back Taxes & Payment Plan Strategies.

The following table summarizes these options:

Response Options to IRS Garnishment Notices

| Response Option | When to Use | Deadline to File | Potential Outcome |

|---|---|---|---|

| Full Payment | Anytime | None | Eliminates the tax debt and stops all collection activity |

| Installment Agreement | Before or after garnishment begins | Varies | Allows payment of the tax debt in monthly installments |

| Offer in Compromise (OIC) | Before or after garnishment begins | Varies | Settles the tax debt for less than the full amount owed |

| Currently Not Collectible (CNC) | Before garnishment begins, if experiencing hardship | Varies | Temporarily suspends collection activities but interest and penalties continue |

This table outlines the different ways you can respond to an IRS notice. Choosing the right option depends on your individual financial situation.

Responding to an Active Garnishment

If your wages are already being garnished, your focus should be on stopping the levy. Contact the IRS immediately to explore resolution options. Options like installment agreements or an OIC are still available.

With an active garnishment, demonstrating your commitment to resolving the debt becomes even more important. Providing complete financial documentation can strengthen your case.

Requesting a Collection Due Process Hearing

If you disagree with the IRS's actions, you can request a Collection Due Process (CDP) hearing. This hearing, handled by the Independent Office of Appeals, allows you to challenge the levy.

You must file Form 12153, Request for a Collection Due Process or Equivalent Hearing, within 30 days of the CDP notice. This hearing provides a formal way to present your case and potentially change or release the garnishment.

Communicating Effectively

Throughout this process, maintain open communication with the IRS and your employer. Keep records of all correspondence.

Provide your employer with clear documentation regarding the garnishment, ensuring they understand the legal limits and correctly calculate your disposable income. This proactive communication helps avoid misunderstandings and potential problems.

Taking quick and decisive action after receiving an IRS notice is crucial for protecting your paycheck and financial well-being.

Breaking Free: How to Release an Existing Garnishment

If the IRS has already started garnishing your wages, getting your full paycheck back becomes a top priority. This section outlines effective strategies to stop these garnishments as quickly as possible. We'll focus on practical solutions that work in the real world.

Understanding Your Options for Relief

Several options exist to release an IRS wage garnishment. Each has its pros and cons, so understanding these is key to choosing the right strategy for you.

Payment Plans: A payment plan, also known as an installment agreement, lets you pay your tax debt in monthly installments. This stops the garnishment once the agreement is in place. However, interest and penalties still add up on the remaining balance.

Offer in Compromise (OIC): An OIC lets you settle your tax debt for less than the full amount. This is a valuable option, but approval hinges on showing true financial hardship. If accepted, an OIC completely releases the garnishment and settles the debt.

IRS Offer in Compromise: A Complete Guide to Tax Debt Settlement

Currently Not Collectible (CNC) Status: If your finances are in dire straits, you might qualify for CNC status. This temporarily stops collection efforts, including wage garnishment. While it offers immediate relief, remember that interest and penalties still accrue, and the IRS will review your finances periodically.

Navigating the IRS and Strengthening Your Case

Successfully releasing a garnishment takes more than just picking an option; it requires good communication and organized documentation. Dealing with the IRS can be frustrating.

Tips for dealing with irate customers can be surprisingly helpful when communicating with the IRS. Clear documentation strengthens your case.

Provide the IRS with complete financial records, including income statements, expense reports, and asset documentation. This helps them accurately assess your finances.

Mistakes to Avoid and Insider Perspectives

Common errors can hurt your efforts to release a garnishment. Avoid incomplete applications, inconsistent information, or slow responses to IRS requests. Honesty and accuracy about your finances are crucial.

Tax professionals often recommend a clear budget showing your actual income and expenses, highlighting any special circumstances adding to your financial hardship. This complete picture can greatly improve your chances of a successful resolution.

Confirming Release and Stopping Withholding

Once the IRS approves your chosen relief option, get written confirmation of the garnishment release. This proof tells your employer to stop withholding wages. Contact your payroll department quickly, giving them the official IRS documentation.

This ensures your full paycheck is restored ASAP. Following these steps carefully ensures your wages are no longer withheld and puts you on the road to financial recovery.

Never Again: Building Your Tax Garnishment Defense System

Facing an IRS wage garnishment can be a stressful experience. But what if you could proactively protect yourself from this happening? This section will guide you in creating a personalized tax strategy that fits seamlessly into your life.

Early Warning Systems: Spotting Trouble Before It Escalates

Think of a financial dashboard with alerts that warn you of potential tax problems before they escalate into collections. That’s the potential of a proactive tax defense system. One essential strategy is accurate withholding.

Many people rely on their employer's default withholding calculations. However, adjusting your W-4 form to reflect your unique financial situation can ensure the correct amount is withheld throughout the year. This avoids unexpected underpayment issues when it's time to file.

Additionally, establishing a designated tax savings account serves as a financial cushion. Regularly contributing even small sums can create a safety net for unanticipated tax obligations.

Calendar Systems That Actually Work

Missed tax deadlines can lead to penalties and interest, drawing unwanted attention from the IRS. Successful taxpayers frequently use calendar systems or reminder apps like Google Calendar to monitor crucial dates.

This could include reminders for estimated tax payments, extension deadlines, and the final filing deadline. Some even establish an annual "tax day" to organize documents and assess their tax situation in advance.

Before we delve into more strategies, let's look at a helpful checklist. This table provides actionable steps to avoid wage garnishment by the IRS.

IRS Wage Garnishment Prevention Checklist

| Prevention Action | When to Complete | Difficulty Level | Impact on Risk Reduction |

|---|---|---|---|

| Adjust Withholding | Annually or after major life changes | Easy | High |

| Set Up Tax Savings Account | Immediately | Easy | Medium |

| Create Tax Deadline Calendar System | Immediately | Easy | High |

| Establish Relationship with Tax Professional | Immediately | Easy | High |

| Build Emergency Tax Fund | Ongoing | Medium | High |

By implementing these straightforward steps, you’re proactively building a defense against future tax problems. Each action, while simple, contributes significantly to reducing your risk of garnishment.

Rebuilding and Long-Term Tax Compliance

Even if you’ve faced garnishment before, recovery is possible. Addressing any credit damage is a key part of this process.

While the garnishment itself doesn't directly appear on your credit report, the underlying tax lien that caused it can negatively affect your credit score.

Fully paying off the tax debt is the most effective method to remove the lien and begin rebuilding your credit.

Developing healthy financial habits is also vital for long-term tax compliance. This includes regular budgeting, tracking expenses, and seeking professional financial guidance when needed.

Creating an emergency fund specifically for potential tax liabilities can provide financial peace of mind.

The Power of Professional Relationships

Forming a relationship with a qualified tax professional before problems occur is invaluable. They can offer personalized advice, guide you through complex tax regulations, and represent you if issues emerge. Consider it like having a trusted advisor in the complex field of tax compliance.

By implementing these strategies, you’re not merely reacting to tax issues—you’re proactively preventing them. You’re creating a strong defense system that protects your earnings and empowers your financial future.

Are you ready to take control of your taxes and avoid future garnishments? Contact Attorney Stephen A. Weisberg today for a free tax debt analysis. We can assist you in developing a personalized strategy to protect your paycheck and secure your long-term financial well-being.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: sweisberg@wtaxattorney.com

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034