Automated Collection System IRS Guide: What You Need to Know

The IRS Automated Collection System (ACS) is the IRS’s massive, computer-driven engine for collecting overdue taxes. It's not a person, but an automated process that churns out notices, handles phone calls, and can even start seizing assets like bank accounts.

Think of it as the IRS's automated first line of defense, designed to handle millions of tax debt cases with efficiency.

What Is The IRS Automated Collection System

Let's face it, the IRS is enormous. It simply doesn't have the manpower to send a Revenue Officer to knock on every single taxpayer's door for an overdue bill.

That's where the Automated Collection System comes in. It's a vast network of call centers and computer systems built to manage the initial stages of collection automatically.

When you have a tax bill you haven't paid, your account gets flagged and dropped into the ACS queue. From that point on, the system follows a predictable, pre-programmed script of actions designed to get a response.

How The ACS Really Works

So, what does this system actually do? The ACS is more than just a glorified mail machine; it has a few core jobs that define the early collection experience. Understanding them helps take the mystery out of those intimidating IRS letters.

To give you a clearer picture, here’s a breakdown of its primary responsibilities:

Key Functions of the IRS Automated Collection System

| Function | Description | What It Means for You |

|---|---|---|

| Automated Notices | The system automatically generates and mails a series of letters (like the CP14 and CP504). | You'll receive notices that get progressively more serious, each with a deadline for response. |

| Inbound Call Handling | Taxpayer calls are routed to IRS representatives working within ACS call centers. | When you call the number on your notice, you’ll be speaking with an ACS agent, not a field officer. |

| Enforced Collection | After sending final notices, the ACS can automatically issue levies on wages and bank accounts. | If you ignore the notices, the system is designed to escalate and start seizing assets without a human override. |

The most important thing to remember is that this system is impersonal. It treats every case the same way at the start—it's just following procedure.

The scale of this operation is staggering. In a single recent fiscal year, the ACS was responsible for managing a portfolio of $47 billion in delinquent tax accounts. While its computers directly collected around $3.4 billion, its role in setting up installment agreements brought in another $4.3 billion, according to a Taxpayer Advocate Service report.

Key Takeaway: The Automated Collection System isn't a special investigation into your life. It's the standard, high-volume starting point for almost all IRS collection cases, driven by computer logic.

Getting a notice from the ACS is simply a signal that it's time to act. It's your cue to pay what you owe, set up a payment plan, or figure out another way to resolve the debt.

Often, tax debt starts with unfiled returns, so if you're behind, the first step is always to get caught up.

The Automated Journey of a Tax Debt Case

The moment your tax account flags a balance due, a highly predictable, automated process springs to life. Think of it as a domino effect inside the Automated Collection System (ACS), where each step is programmed to escalate over time. Knowing how this journey unfolds takes the fear out of the equation and gives you a clear roadmap, showing you exactly when and how to step in.

It all starts with a simple trigger: an unpaid tax bill. As soon as your account is flagged, the system doesn't wait for a person to look at your file. It immediately starts sending a series of computerized notices, each one sounding more serious than the one before. This isn't personal; it's just the machine following its code.

The Initial Notice and Escalation

The very first letter you’ll almost always get is the CP14, Notice of Tax Due and Demand for Payment. This is the official starting pistol for the collections race. It’s a straightforward notice stating that you owe money and giving you a deadline to pay up.

If that deadline comes and goes without payment or contact, the system automatically kicks things to the next stage. A few weeks later, you can expect a follow-up, typically the CP501, Reminder - You Have a Balance Due. This one is a little more direct, but it's still fundamentally a reminder. The real heat starts to turn up if this notice is also ignored.

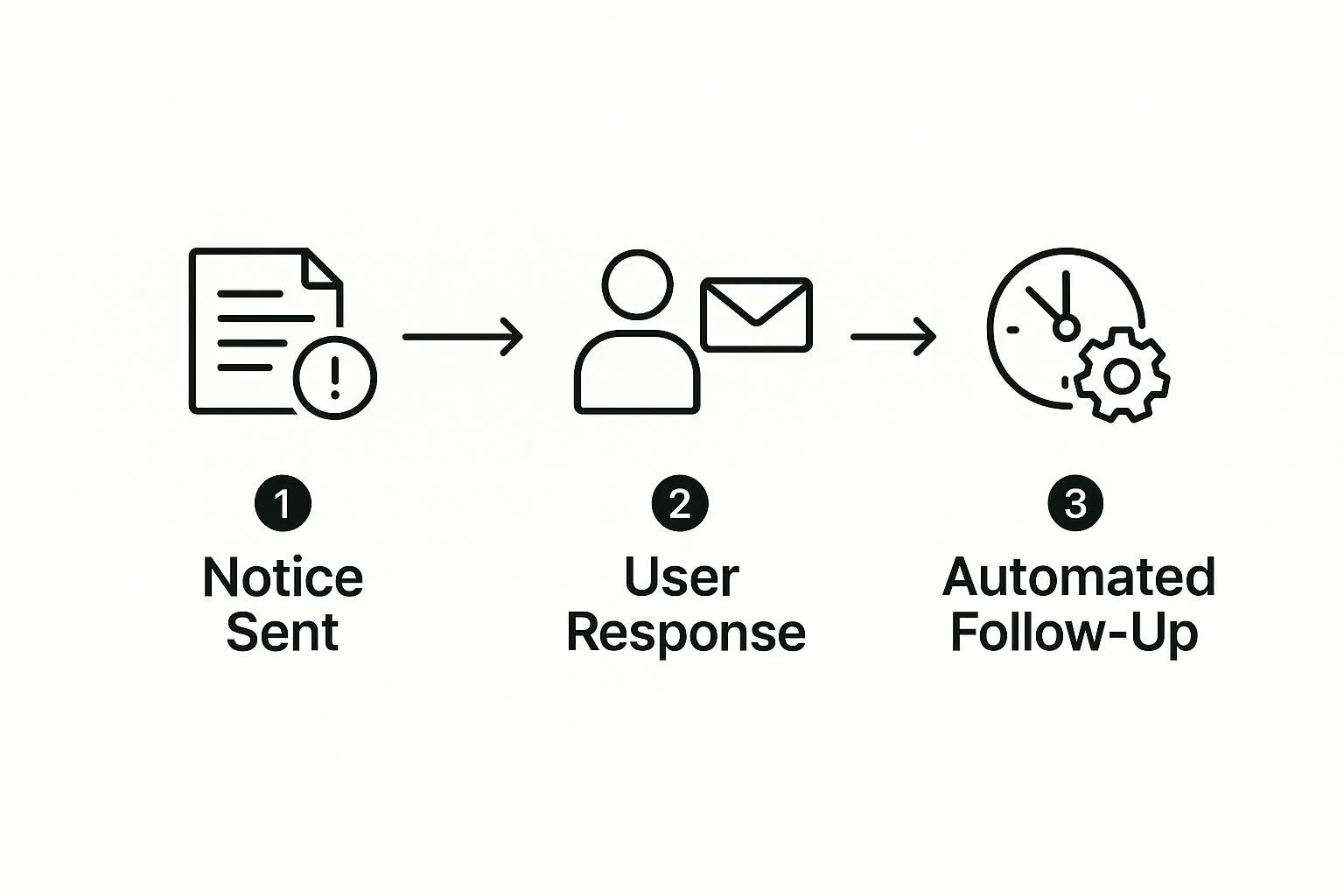

The following infographic gives you a bird's-eye view of this back-and-forth between the IRS system and the taxpayer.

This flow shows how your response—or your silence—directly tells the system what to do next. It really underscores why being proactive is so important.

The Critical Turning Point

After those first few reminders, the tone changes—a lot. The next notice you'll likely see is a CP504, Urgent Notice - We Intend to Levy Your Property or Rights to Property, which is a serious escalation. While it sounds final, the CP504 is still a warning shot across the bow. It means the IRS can take your state tax refund or other federal payments, but it doesn't yet have the authority to levy your bank account or garnish your wages.

That power only gets unlocked after the final, most important notice is sent.

The big one is the Letter 1058 or LT11, officially titled Final Notice of Intent to Levy and Notice of Your Right to a Hearing. This is the absolute legal prerequisite for any enforced collection action.

Once you receive this letter, a 30-day clock starts ticking. You have a few critical options during this window:

Pay the tax debt in full.

Set up a formal resolution, like a payment plan.

File an appeal to request a Collection Due Process (CDP) hearing.

Filing that appeal is a game-changer. It legally freezes the collection process, giving you time while your case is under review.

But if you let those 30 days run out without doing anything, the automated collection system IRS gets the green light to start seizing your assets.

We're talking about levying money straight from your bank accounts, garnishing a slice of every paycheck, and taking other property.

The entire journey, from the first CP14 to the final Letter 1058, is built to give you multiple chances to fix the problem.

When you understand this predictable sequence, you can pick the right moment to engage and guide your case toward a solution you can live with—long before forced collection even enters the picture.

How to Decode Common ACS Notices

Getting an official-looking envelope from the IRS can make your heart skip a beat. But understanding what's inside is the first step to taking control of the situation.

These letters aren't just random threats; they're specific messages sent by the automated collection system IRS computers. Each one has a clear purpose.

Once you learn to decode them, you can turn that initial anxiety into a straightforward plan of action.

Think of the notice sequence as a conversation. The first one is a polite request. If you don't reply, the tone gets much more serious. The key is knowing what each letter is really saying and how long you have to respond.

The IRS uses a wide variety of notices, but a few show up far more often than others in the automated collection process. Let's break down the most common ones you're likely to see.

| Notice Code | What It Means | Typical Deadline | Recommended Action |

|---|---|---|---|

| CP14 | This is the first bill. It states you have a balance due and breaks down the tax, penalties, and interest. | 21 days | Pay the balance if possible, or immediately explore other options like a payment plan. |

| CP501 / CP503 | These are follow-up reminders that your tax bill is overdue. The language becomes more firm. | Varies | The debt is not going away. This is your cue to respond before the situation escalates further. |

| CP504 | This is a formal warning that the IRS intends to levy your property, specifically your state tax refund. | 30 days | Act now. This is a clear signal that federal levies on wages and bank accounts are the next step. |

| Letter 1058 / LT11 | This is the final, legal notice before the IRS can seize assets like wages and bank accounts. | 30 days | This is critical. Immediately pay, set up a resolution, or file an appeal for a CDP Hearing to stop collection. |

Knowing what each notice means is half the battle. Now, let's look at the sequence in a bit more detail, because the order they arrive in tells its own story.

The Opening Salvo: CP14

The CP14 (Notice of Tax Due and Demand for Payment) is almost always the first letter you'll get. It's the system's official heads-up that you have a balance due. Think of it as a simple bill that spells out what you owe in tax, penalties, and interest. It will give you a payment deadline, usually 21 days.

Ignoring a CP14 doesn't make the problem vanish. It just signals the ACS computer to move to the next stage of its collection sequence. This is your best and simplest chance to deal with the debt before things get more complicated.

The Follow-Up Reminders: CP501 and CP503

If the CP14 deadline comes and goes without a response, the system will send follow-up letters. The CP501 (Reminder - You Have a Balance Due) and the CP503 (Important - Immediate Action Required) are exactly what they sound like: escalating reminders. While the language gets stronger, their function is the same as the first notice—to prompt you to pay the outstanding balance.

These letters are still part of the early phase of collections. The IRS doesn't gain any new enforcement power at this stage, but these notices are a clear sign that the system is gearing up for more serious action if it continues to be ignored.

The Urgent Warning: CP504

This is where things start to get serious. The CP504 (Urgent Notice - We Intend to Levy Your Property or Rights to Property) is a major warning shot. It officially informs you that the IRS has the right to seize certain assets, and the first one on its list is your state tax refund.

It's crucial to understand that the CP504 does not yet give the IRS the power to garnish your wages or take money from your bank account. It is a legally required notice before they can intercept state-level assets, but it’s also a powerful signal that federal levies are next on the agenda if you don’t act.

The Final Notice: Letter 1058 or LT11

Pay close attention to this one. The Letter 1058 or LT11 (Final Notice of Intent to Levy and Notice of Your Right to a Hearing) is the most critical piece of mail the ACS will ever send you. This letter is the legal key that unlocks the IRS's most powerful collection tools.

Once this letter arrives, a clock starts ticking. You have exactly 30 days to do one of three things:

Pay the tax debt in full.

Set up a formal resolution, like an Installment Agreement or Offer in Compromise.

File an appeal to request a Collection Due Process (CDP) hearing.

Requesting a CDP hearing within that 30-day window puts an immediate legal freeze on all collection actions while your case is reviewed by an independent appeals officer. But if you let that deadline pass without taking action, the automated collection system irs is legally free to start seizing your wages, levying your bank accounts, and taking other assets.

Understanding Your Rights With The IRS

Going head-to-head with the IRS, particularly its automated collection system, can feel incredibly daunting. When those official-looking envelopes land in your mailbox, it's easy to feel like the agency has all the power.

But that’s not the whole story. You’re actually protected by a powerful set of legal safeguards called the Taxpayer Bill of Rights.

These aren't just feel-good platitudes; they're concrete, actionable rights you can use to protect yourself. Knowing them is the first step in turning the tables, moving you from a passive target to an active participant who knows the rules of the game.

Your Right To Be Informed

You have a fundamental right to know exactly what the IRS expects from you to stay compliant. In simple terms, this means the IRS has to explain what you owe, why you owe it, and what happens next.

Every notice you get from the automated collection system irs is the agency fulfilling this duty—it's their way of informing you about a debt.

This right also empowers you to ask questions. If a notice is confusing, or you're certain the amount is wrong, you are fully entitled to ask for a clear explanation. This is the bedrock of any successful resolution; you can't fix a problem you don't understand.

"No matter what kind of collection notice you receive, don’t ignore it! Ignoring a collection notice can have costly consequences."

As the Taxpayer Advocate Service points out, this is a two-way street. The IRS informs you, but you have to use that information to take action. And that brings us to your next crucial right.

Your Right To Challenge The IRS

This is where you really get to stand up for yourself. You have the Right to Challenge the IRS’s Position and Be Heard. This is your legal green light to disagree with the IRS and have a neutral third party review your case.

This right is absolutely critical when you get a Final Notice of Intent to Levy (that's Letter 1058 or LT11). You have a 30-day window to formally exercise this right by requesting a Collection Due Process (CDP) hearing. Filing this request does two incredibly important things:

It puts an immediate stop to all collection activities from the ACS.

It kicks your case out of the automated system and sends it to the Independent Office of Appeals, where a real person will give your situation a fair look.

Your Right To Representation

Finally, remember this: you never have to face the IRS by yourself. You have the Right to Retain Representation. This means you can hire a qualified professional, like a tax attorney or an Enrolled Agent, to handle the IRS for you.

Once you file a power of attorney, the IRS is legally required to communicate with your representative, not you. This is a game-changer if you're feeling overwhelmed or if your case gets tangled.

It puts an expert in your corner who knows the system inside and out and can make sure your rights are always protected.

Your Resolution Options for Tax Debt

Getting a notice from the IRS doesn't mean your financial fate is sealed. Far from it. Think of it as a signal to take action, and the good news is you have several powerful strategies at your disposal to resolve the debt. This is your playbook for choosing the right path forward and getting back in control.

It’s all about picking the right tool for the job. You wouldn't use a hammer on a screw, right? In the same way, the best resolution depends entirely on your unique financial situation.

Installment Agreement

One of the most common and straightforward solutions is an Installment Agreement (IA). It's exactly what it sounds like: a monthly payment plan that lets you pay your tax debt over time, typically up to 72 months. This is a fantastic option if you can afford the full amount you owe, just not in one lump sum.

You can often set up an IA directly through the IRS website, making it a pretty accessible path to compliance. Once it's in place, an IA stops more aggressive collection actions, like bank levies, as long as you keep up with your payments.

Offer in Compromise

But what if you can't pay the full amount, even with a payment plan? This is where the Offer in Compromise (OIC) comes into play. An OIC allows certain taxpayers to settle their tax liability with the IRS for less than the total amount owed.

Be warned, though: the IRS has very strict eligibility rules. They will put your ability to pay, income, expenses, and asset equity under a microscope.

An OIC is designed for those in genuine financial hardship, not just for someone who’d prefer to pay less.

Currently Not Collectible

For people facing severe financial difficulty, there's another safety net: Currently Not Collectible (CNC) status. If the IRS determines that you truly cannot afford to pay both your basic living expenses and your tax debt, they can place your account in CNC status.

What CNC Means: While your account is in CNC status, the IRS temporarily halts collection actions. It’s important to understand this doesn't erase the debt—interest and penalties will continue to pile up—but it provides critical breathing room. The IRS will also check in on your financial situation periodically to see if your ability to pay has improved.

Interestingly, IRS collections have faced their own challenges recently. Between fiscal years 2019 and 2022, collections from the automated system actually dipped by $0.3 billion, despite an increase in staff. This was partly due to operational pauses after the pandemic, which left the active case inventory stuck at a massive 6.7 million.

Navigating these options demands an honest, clear-eyed look at your finances. While your immediate focus is on the tax debt, it can also be incredibly helpful to understand broader financial recovery strategies.

For instance, reading about lessons on saving a business from bankruptcy can offer valuable perspective on overcoming serious financial hurdles. By weighing each option against your own situation, you can build a realistic plan to finally put your tax problems behind you.

When You Should Hire a Tax Professional

Plenty of people can handle the first few IRS letters on their own, but it's just as important to know when you're out of your depth.

At a certain point, going it alone stops being brave and starts being risky. Trying to navigate complex tax issues without experience can backfire, leading to bigger problems and fewer ways out.

Certain situations are undeniable red flags, telling you it’s time to call in a professional. When you're dealing with the automated collection system irs, knowing when to get help is key.

For some, this might mean looking into professional assistance with personal taxes to get a handle on their financial strategy. A seasoned tax professional can step in, communicate effectively with the IRS, and start working toward a resolution right away.

Key Moments to Hire an Expert

You should seriously consider hiring representation the moment any of these things happen:

You get a Final Notice of Intent to Levy. This isn't a drill. It’s the last warning shot before the IRS can start seizing assets. An expert can often file an immediate appeal to stop the clock and open up negotiations.

You owe more than $50,000. Once your tax debt crosses this threshold, the solutions get more complicated. A simple online payment plan might not cut it, and professional negotiation becomes almost essential.

You own a business with tax debt. Tax problems for a business, especially those involving payroll taxes, are a whole different ballgame. The rules are stricter, and the penalties can be severe.

You think you might qualify for an Offer in Compromise. The OIC process is notoriously difficult, with a high rejection rate for a reason. While our guide on how to qualify for an Offer in Compromise is a great starting point, getting an offer accepted almost always requires professional help.

You're completely overwhelmed. Honestly, the stress and confusion of an IRS problem are reason enough. Bringing in an expert gives you peace of mind and ensures your rights are protected every step of the way.

The internal struggles at the IRS make a strong case for getting professional help. A recent government report found that in fiscal year 2022, taxpayers calling the Automated Collection System had to wait an average of 38 minutes on hold just to speak to a person. You can read more about it in the TIGTA report on ACS performance.

Hiring a professional isn't giving up. It's a strategic move to get an expert on your side of the table—one who can save you time, stress, and potentially a whole lot of money.

Common Questions About the ACS

It's only natural to have a few nagging questions even after getting a handle on the IRS process. Once you understand the basics of the automated collection system irs, the "what if" scenarios really start to bubble up. Let's tackle some of the most common ones to help you move forward with a clear head.

The big one is always about enforcement. Can the ACS really just take your money? Yes, it can, but not without giving you a chance to respond. The system is built to automatically trigger actions like wage garnishments and bank levies.

But—and this is a big but—it only does so after sending you a series of notices. The last and most critical one is the Letter 1058, your Final Notice of Intent to Levy. That letter is your final warning, giving you 30 days to act before any seizure happens.

Can You Speak to a Person?

Absolutely. While the system itself is automated, there are real people behind the curtain. When you call the number on your IRS notice, you'll reach a human employee working in an ACS call center.

They can pull up your file and discuss setting up a payment plan or other ways to resolve the debt. Just be ready for a potentially long wait on hold; these call centers are notoriously busy.

If you just ignore the letters, the system is designed to automatically kick things up a notch. The most serious consequence is the filing of a Notice of Federal Tax Lien. This makes your tax debt public record and can absolutely wreck your credit score.

The Bottom Line: The single worst thing you can do is ignore ACS notices. It’s a guaranteed way to see collection efforts escalate from letters to liens and, eventually, to levies on your paychecks and bank accounts.

Being proactive is your strongest shield. When you understand the system and respond right away, you keep control of the situation and preserve all your resolution options.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034