Notice of Intent to Levy: What You Need to Know

No one likes getting mail from the IRS. But when a Notice of Intent to Levy shows up, it’s a different level of serious. This isn't just another letter; it's the final warning shot before the IRS can legally start taking your property. The moment you open it, a critical 30-day countdown begins.

What a Notice of Intent to Levy Really Means

Getting a Notice of Intent to Levy means one thing for sure: this isn't the IRS's first attempt to get in touch about your unpaid taxes. They've sent other letters. You're now at the end of the line.

This notice, which often comes as an LT11 or Letter 1058, is the most aggressive step in their collection process. It's the agency’s way of saying the grace period is over, and they’re gearing up for forceful action.

But here’s the most important thing to grasp: they haven't seized anything yet. This notice is a legally required step that gives you a clear window to prevent a levy from ever happening. It’s a call to action, not a done deal.

To help you quickly grasp what's at stake, this table breaks down the key parts of the notice.

Decoding Your IRS Notice of Intent to Levy

Here's a quick summary of the most critical elements of the notice and what they signify for you.

| Element | What It Means For You | Your Immediate Action |

|---|---|---|

| Notice Date | This is Day 1 of your 30-day window to respond before the IRS can legally seize your assets. | Mark this date on your calendar. Do not let it pass without taking action. |

| Total Amount Due | The full tax debt the IRS believes you owe, including penalties and interest that have accumulated. | Review the amount. If it seems wrong, you'll need to prepare to challenge it. |

| Your Right to a Hearing | The notice explains your right to request a Collection Due Process (CDP) hearing to dispute the levy. | This is your most powerful tool. Consider filing Form 12153 to request a hearing immediately. |

| Response Deadline | The hard stop date, exactly 30 days from the notice date. After this, the IRS has the green light to take action. | Plan to contact the IRS or a tax professional well before this deadline to discuss your options. |

Understanding these components is your first step toward taking back control of the situation.

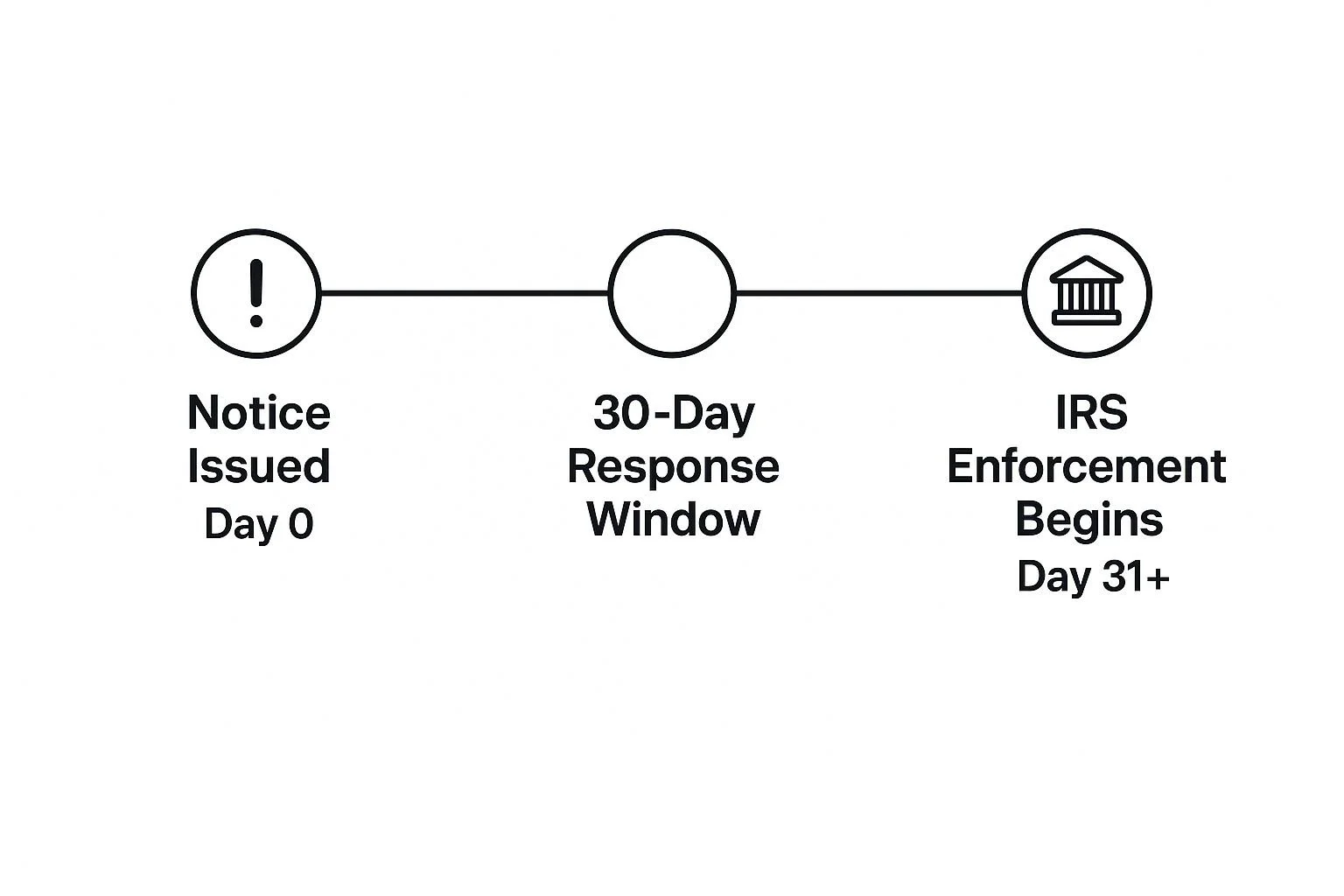

The 30-Day Response Window Is Critical

That date printed on your notice? It kicks off a 30-day period that you cannot afford to waste. This is your chance—your right—to respond and figure out a solution before the IRS can legally touch your bank accounts, garnish your wages, or seize other property.

If you let this deadline slide, you're essentially giving the IRS the legal authority to move forward with its most aggressive collection tactics.

Think of this notice as the IRS putting its cards on the table. They are stating their intentions clearly, giving you one last, formal opportunity to resolve the debt on your terms before they start doing it on theirs.

This is a make-or-break moment. Acting now can stop the collection machine in its tracks and put you on a path to resolution. It's far, far better than trying to claw back money after a levy has already hit your account. Knowing your rights is paramount, especially when you consider real-world examples of IRS levy misuse.

What Triggers This Final Notice

A Notice of Intent to Levy doesn't come out of the blue. It’s the final act in a long play that started months, or even years, earlier. The journey to this point usually involves a series of increasingly urgent letters:

Initial Bill (CP14): The very first notice telling you that you owe money.

Reminder Notices (CP501, CP503): Follow-up letters that get a bit more persistent.

Notice of Intent to Seize (CP504): A more serious warning that signals a levy is on the horizon.

The IRS is required by law to send this final notice. Internal Revenue Code Section 6331(d) mandates that taxpayers get at least 30 days' notice before the agency can start seizing assets. This isn't a courtesy; it's a legal safeguard designed to give you one final chance to avert disaster.

The Path to a Final Levy Notice

Let’s get one thing straight: an IRS Notice of Intent to Levy never just shows up out of the blue. It’s the final, loud clang of a bell at the end of a long, predictable series of communications that likely started months, if not years, ago.

Knowing this timeline is your first line of defense, because it shows the IRS isn’t playing "gotcha." They follow a clear, escalating process that gives you multiple chances to act before things get serious.

Think of it as a series of warning shots, each one landing a little closer. The process almost always starts with a simple tax bill.

The Initial Bill and Gentle Reminders

It all begins with the CP14 notice. This is just a standard, straightforward bill letting you know you have a balance due. It's the most common and least scary notice the IRS sends. If that first letter gets ignored, the IRS will follow up with reminders that get progressively more firm in tone.

These next letters, usually a CP501 and then a CP503, are essentially follow-up alerts. They restate what you owe—now with penalties and interest tacked on—and strongly encourage you to pay up or work out a deal. Each one of these is a valuable opportunity to resolve your tax debt before the situation escalates.

The Final Warning Before the Levy Notice

The last stop on the warning train, right before the official levy notice, is typically the CP504, Notice of Intent to Seize Your Property or Rights to Property. I know, the name sounds terrifying, but it's still just a warning.

This notice specifically tells you the IRS plans to take your state tax refund and put it toward your federal tax debt. It’s a very clear signal that the agency's patience has run out and much more serious actions are on the horizon.

It’s only after all these previous attempts to get your attention have failed that the IRS sends the final, legally required Notice of Intent to Levy and Notice of Your Right to a Hearing (often labeled Letter 1058 or LT11). This is the big one. This is the document that officially starts your 30-day countdown.

This predictable sequence is actually good news. It shows the IRS gives you numerous off-ramps before it threatens to seize your assets. Every notice you ignore is a missed chance to negotiate from a stronger position. Figuring out where you are in this process is the first step to taking back control.

This visual timeline breaks down what happens during that critical 30-day window after you receive the final notice.

As the infographic makes crystal clear, that 30-day window is your last real line of defense. It’s the period where you still have rights and options before the IRS is legally allowed to start enforced collection. Once Day 30 passes, that protective barrier disappears.

By understanding this path, you can see that a notice of intent to levy isn’t some random, aggressive act. It’s the result of a well-documented process.

That knowledge should empower you to act decisively within the time you’re given, knowing it’s your final chance to prevent a seizure.

Understanding Your Taxpayer Rights and Options

Getting an IRS notice of intent to levy can feel like the end of the road, but it’s actually the exact opposite. This letter isn’t just a threat; it's the key that unlocks a whole set of taxpayer rights specifically designed to protect you. It’s a formal invitation to step up, state your case, and find a workable solution.

The most powerful right you have at this moment is the ability to request a Collection Due Process (CDP) hearing. Think of it as hitting a legal pause button on the entire IRS collection machine.

Filing for a CDP hearing on time legally stops most IRS collection actions in their tracks, including levies on your wages and bank accounts. This buys you precious time—breathing room to get organized, figure out your finances, and build a strategy without the immediate fear of having your assets seized.

Your Right to a CDP Hearing

The CDP hearing is your official chance to challenge the IRS's plan to take your property. It's not just a meeting; it's a formal review handled by the IRS Independent Office of Appeals, which is a totally separate branch from the collection agents who sent the notice. This separation exists to give you a fair, impartial review of your situation.

During the hearing, you can accomplish a few critical things:

Challenge the Levy: Argue that the levy would create an extreme economic hardship for you and your family.

Dispute the Debt: If you haven't had a chance before, you can question the amount of tax the IRS says you owe.

Propose Alternatives: This is your best opportunity to formally present other ways to pay off the debt, which the Appeals Office is required to consider.

To make this happen, you must file Form 12153, Request for a Collection Due Process or Equivalent Hearing. This isn't just a suggestion—it's the required form to officially trigger your rights.

CRITICAL DEADLINE: You have just 30 days from the date printed on your levy notice to file Form 12153. This is a hard-and-fast deadline. If you miss it, you lose your right to a CDP hearing and any chance to take your case to the U.S. Tax Court later.

The Right to Propose Solutions

Beyond just stopping the levy, the CDP hearing process gives you the power to propose a real solution. The IRS would much rather work out a reliable payment solution than go through the hassle of seizing your property. That’s a last resort for them.

This is your chance to get on the offensive and suggest a better path forward. Your main options are:

Installment Agreement (IA): A straightforward payment plan. You agree to make fixed monthly payments over time to clear your tax debt. It’s a great fit for taxpayers who have a steady income but just can't pay the full balance at once.

Offer in Compromise (OIC): An OIC allows some taxpayers to settle their tax liability for less than the total amount owed. This is typically reserved for people facing true financial hardship, where there's little chance the IRS could ever collect the full debt.

Currently Not Collectible (CNC) Status: If you can prove that you can’t even cover your basic living expenses, the IRS may place your account in CNC status. This temporarily stops all collection activity until your financial situation gets better.

Your Right to Representation

You don't have to go through this alone. You have a fundamental right to have a qualified tax professional—like a tax attorney or a CPA—represent you.

A pro can handle all the calls with the IRS, file the complex paperwork, and negotiate for you. To build the strongest case, many professionals now use advanced legal research software to dig into relevant case law and statutes.

That level of expertise can be the difference-maker. To learn more about the specifics of the appeals process, there is excellent information available on taxpayer appeal rights and how to use them effectively.

The Real-World Impact of an IRS Levy

So what happens if that crucial 30-day window slams shut before you’ve reached a resolution with the IRS? This is the moment when the theoretical threat on your notice of intent to levy becomes a painful financial reality. Ignoring that final notice gives the IRS the legal green light to stop warning and start taking.

And when they start, the consequences can trigger a devastating domino effect that ripples through every corner of your financial life. This isn't just about a single seizure; the IRS has a powerful collection arsenal, and once they deploy it, clawing your way back to stability can feel nearly impossible.

Frozen Bank Accounts and Financial Paralysis

One of the most common and jarring actions the IRS takes is levying a bank account. And no, this isn't a partial measure. The IRS can freeze and take every single dollar in your accounts—checking, savings, you name it—up to the full amount you owe on the day the levy hits.

Imagine waking up to find your bank balance at zero. The fallout is immediate and catastrophic:

Bounced Checks and Missed Payments: Any checks you've written will bounce.

Failed Automatic Payments: Your rent, mortgage, car payment, and utility bills will all fail, racking up late fees and putting you at risk of foreclosure, eviction, or having your power shut off.

Inability to Access Cash: You’re completely locked out of your own money. You can’t even buy groceries or put gas in your car.

The shock of a bank levy is often the wake-up call that finally forces people to act. The problem is, by then you’re playing defense, desperately trying to recover funds you need to survive instead of proactively preventing the crisis in the first place.

The Continuous Drain of Wage Garnishment

While a bank levy is a one-time gut punch, a wage garnishment is a slow, continuous bleed. When the IRS levies your wages, they don't ask you for the money—they go straight to your employer. Your HR department is then legally required to send a huge chunk of your pay directly to the IRS before you ever see a dime.

This isn’t a one-and-done deal. It happens with every single paycheck until the tax debt is paid in full or you successfully negotiate a release. The amount they take is significant, often leaving you with barely enough to scrape by.

Beyond the Bank Account: Seizures of Other Assets

The IRS’s authority doesn't stop with your bank account and your job. They can seize a surprisingly wide range of other assets, including:

Social Security benefits (up to 15% is fair game under the Federal Payment Levy Program)

Retirement accounts like your 401(k) or IRA

State tax refunds

Investment dividends and commissions

Business assets, equipment, and even your accounts receivable

This broad power means that once that 30-day notice period expires, almost no part of your financial world is truly safe.

Lasting Damage from a Federal Tax Lien

As if a levy wasn't bad enough, it's often accompanied by a Notice of Federal Tax Lien. This is a public document that essentially gives the IRS a legal claim against all your current and future property. It screams to the world—and to all potential creditors—that you have a significant federal debt.

The lien immediately torpedoes your credit score, making it nearly impossible to get a mortgage, a car loan, or even a basic credit card.

Under the FAST Act, things can get even worse. If your tax debt is considered "seriously delinquent" (over $62,000 in 2024, a figure that adjusts for inflation), the IRS can report it to the State Department.

The State Department can then deny your passport application or even revoke your existing passport, turning a tax problem into a severe restriction on your personal freedom.

Your Action Plan for Responding to the IRS

When an IRS notice of intent to levy shows up in your mailbox, it’s time to shift gears from worry to action. This is the moment to build a solid game plan. That 30-day window starts ticking immediately, but with a clear, strategic response, you can absolutely navigate this and keep your assets safe.

The most critical first step is also the simplest: do not ignore the notice. Tucking it away in a drawer and hoping it disappears is the worst thing you can do. Ignoring it all but guarantees the IRS will move forward with the levy. Taking action, however, puts you right back in the driver's seat.

Step 1: Gather Your Financial Information

Before you can even think about proposing a solution, you need a perfectly clear picture of your financial reality. The IRS needs this information to consider any alternative to a levy, so coming to the table prepared is non-negotiable.

Start by pulling together the key documents that tell your complete financial story. This means getting your hands on:

Proof of Income: Your recent pay stubs, profit and loss statements if you run your own business, and any records of other income sources.

List of Expenses: A realistic budget outlining your necessary living costs—think housing, utilities, groceries, car payments, and so on.

Asset and Debt Information: Statements from your bank accounts, retirement funds, car loans, and credit card balances.

This isn't just busy work for the IRS; it's for you. This process forces you to understand exactly what you can realistically afford to pay, which is the cornerstone of any successful negotiation.

Step 2: Contact the IRS or a Tax Professional

With your financial documents organized, it's time to make contact. You can always call the IRS directly using the phone number on your notice. But let's be honest, for most people, that's an intimidating and confusing conversation to have.

This is where bringing in a qualified tax professional can be a game-changer. An experienced tax attorney can step in and handle all IRS communications for you.

They make sure your rights are protected and know how to present your case in the best possible light. They’ve been down this road before and can guide you to the best outcome for your unique situation.

Facing the IRS alone can feel like entering a maze without a map. A professional acts as your guide, helping you avoid common pitfalls and find the most direct path to resolving your tax debt. Their expertise can be invaluable when the stakes are this high.

Step 3: Choose Your Resolution Pathway

Once you’ve opened a line of communication, your goal is to present a collection alternative. The truth is, the IRS would generally rather work out a payment solution with you than go through the hassle of seizing assets. Your primary options fall into a few main categories, each designed for different financial circumstances.

Comparing Your Tax Debt Resolution Options

Choosing the right path forward is the most critical decision you'll make. This table breaks down the main strategies for resolving your tax debt after receiving a levy notice.

| Resolution Option | Who It's Best For | Key Consideration |

|---|---|---|

| Pay in Full | Taxpayers who have the cash or can access funds to cover the entire debt. | This is the fastest way to resolve the issue and stops all future penalties and interest from accruing. |

| Installment Agreement | Individuals with a steady income who can't pay the full balance at once. | You make fixed monthly payments over time, often up to 72 months, to clear the debt. |

| Offer in Compromise (OIC) | People facing significant financial hardship who cannot possibly pay the full amount. | This allows you to settle the debt for less, but requires extensive financial proof and is not guaranteed. |

Each of these options has its place, and the best one depends entirely on your financial reality.

An Installment Agreement is a practical and very common solution for many taxpayers. You can learn more about how these structured payment options work in our detailed guide to IRS Payment Plans.

An Offer in Compromise, while it sounds like the perfect solution, comes with very strict eligibility rules based on your ability to pay, income, expenses, and asset equity. Your response to the notice must be strategic and grounded in what's truly achievable.

Frequently Asked Questions About the Levy Process

Even after you understand the basics, the reality of an IRS notice of intent to levy can kick up a storm of specific, high-stakes questions.

The legal language alone is enough to cause confusion and anxiety, and I get it. This section is designed to give you direct, no-nonsense answers to the questions I hear most often from taxpayers in this exact situation.

My goal here is simple: cut through the jargon and give you the practical clarity you need. Getting a handle on these key points can dial down the fear and give you the confidence to make smart decisions.

What Is the Difference Between a Levy and a Lien?

This is easily one of the most common points of confusion. People often use "levy" and "lien" as if they're the same thing, but in the eyes of the IRS, they are two very different tools. Knowing the difference is critical to understanding what’s actually happening.

A Notice of Federal Tax Lien is a public claim against your property. Think of it as the IRS planting a flag on everything you own—your house, car, even future assets—to secure their spot in line as a creditor.

It’s a public document that screams to other lenders, "We get paid first!" A lien doesn’t take anything from you, but it crushes your credit and ties your hands if you try to sell property.

A levy, on the other hand, is the action. It's the physical seizure of your assets. If the lien is the warning sign, the levy is the tow truck actually hooking up your car. It’s the enforcement step where the IRS actively takes your property to satisfy the debt.

To put it simply: a lien secures the debt; a levy collects it.

Can the IRS Seize My Social Security Payments?

This is a deeply personal and valid fear for anyone relying on Social Security for their livelihood. And unfortunately, the answer is yes, the IRS has the legal authority to take a portion of your Social Security benefits.

This is done through an automated system called the Federal Payment Levy Program (FPLP). It allows the IRS to continuously intercept a piece of certain federal payments, including Social Security.

There are, however, firm rules around this:

The Limit: The law caps the seizure at 15% of your monthly Social Security payment.

The Process: Once triggered by a final notice, the process is automatic. The Social Security Administration will start sending that 15% directly to the IRS every month.

Now, there is a silver lining. Certain benefits, like Supplemental Security Income (SSI), are completely exempt. More importantly, if this levy would cause you a significant economic hardship—meaning you couldn't afford basic living expenses—you can fight to have it stopped. But you have to be the one to raise your hand and prove it to the IRS.

A levy on Social Security is a powerful reminder of how far the IRS can reach. It’s exactly why you must respond to the Notice of Intent to Levy—it’s your last clear chance to prevent this before your essential income is hit.

Could I Go to Jail for Not Paying My Tax Bill?

Let's put this fear to rest right now. Receiving a Notice of Intent to Levy is a civil matter, not a criminal one. It means the government sees you as a debtor, not a criminal. You will not go to jail simply because you owe taxes and can't afford to pay.

Criminal charges, and the potential for prison time, are reserved for things like willful tax evasion or tax fraud. That requires a deliberate, illegal intent to cheat the system.

What does that look like in the real world?

Intentionally hiding income or stashing assets offshore.

Creating fake invoices or falsifying business records.

Claiming dependents or deductions you know you're not entitled to.

Deliberately not filing tax returns for years on end to hide from the IRS.

Being in a tough financial spot is not a crime. The levy notice is about collecting a debt. While the financial consequences are severe, they don't include jail time.

How Long Does an IRS Levy Last?

The answer really depends on what the IRS is taking. Levies aren't a one-size-fits-all tool, and how long one lasts is determined by its type.

Bank Levy (A One-Time Hit): When the IRS levies a bank account, it's a snapshot in time. Your bank freezes the account for a mandatory 21-day holding period. After those 21 days, the bank sends whatever was in the account (up to the amount you owe) to the IRS. Then, that specific levy is finished. The IRS can, however, issue another one later if your debt isn't fully paid.

Wage Garnishment (A Continuous Drain): This is the most common and damaging type of levy. The IRS instructs your employer to send them a large chunk of every single paycheck. This doesn't stop. It continues with every pay period until one of three things happens:

Your tax debt is paid in full.

You successfully negotiate a levy release with the IRS, usually by setting up another resolution like a payment plan.

The legal time limit for collection, known as the Collection Statute Expiration Date (CSED), runs out—typically 10 years from when the tax was assessed.

Because a wage garnishment is ongoing, it can be absolutely devastating. Resolving it has to be your top priority.

Facing an IRS levy is a daunting experience, but you don't have to navigate it alone. With over a decade of experience, Attorney Stephen A Weisberg has successfully represented countless individuals and businesses, resolving complex tax issues and stopping aggressive IRS collection actions. I start with a FREE Tax Debt Analysis to determine the best path forward before you ever pay a fee. Take the first step toward peace of mind and visit https://weisberg.tax to schedule your free consultation today.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034