How to Negotiate With the IRS and Win

Alright, let's talk about the reality of negotiating with the IRS. It's not about finding some secret loophole; it's about choosing the right strategy for your specific financial situation. The two main avenues you’ll encounter are an Offer in Compromise (OIC) and an Installment Agreement (IA).

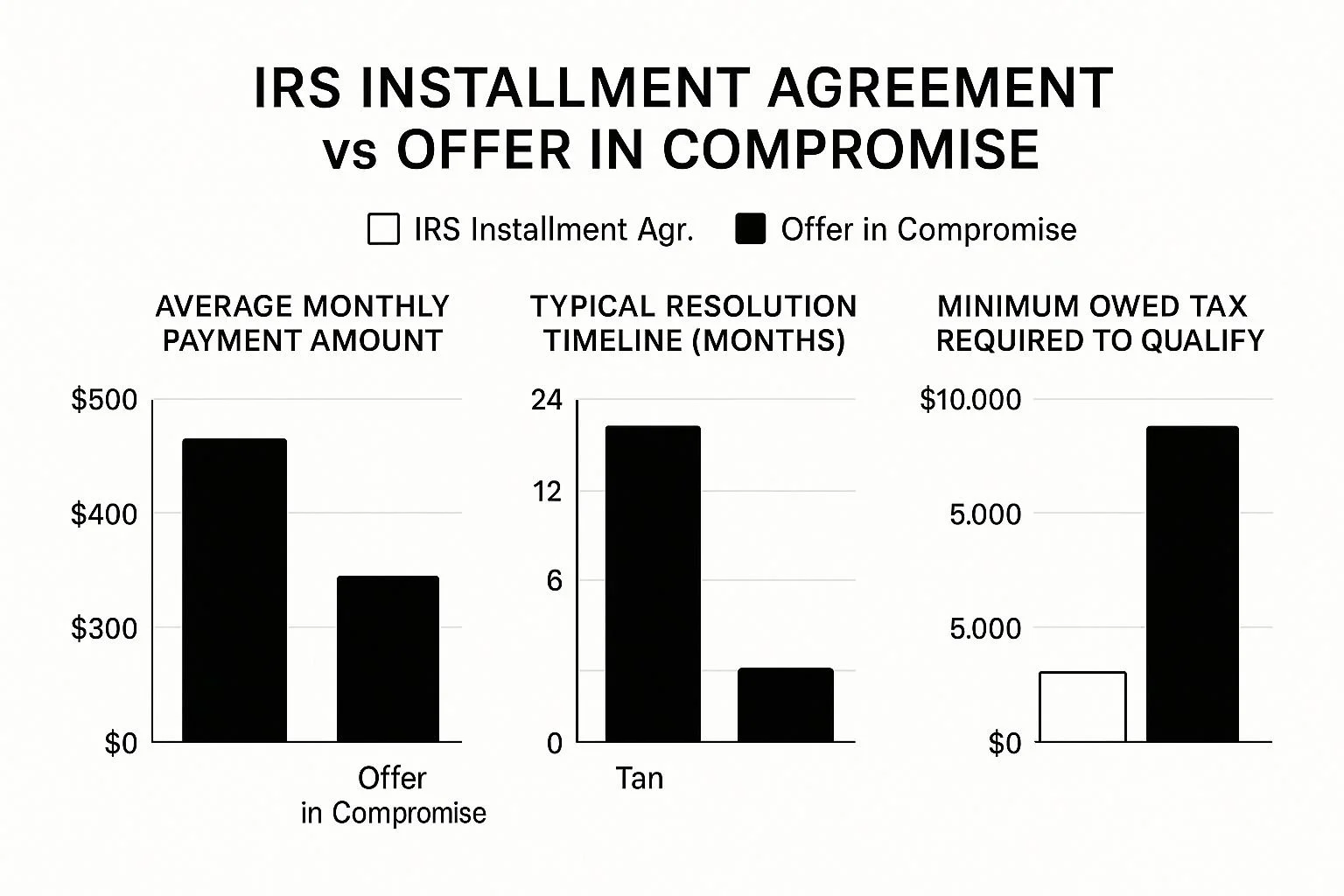

An OIC lets you settle your tax bill for less than the full amount, while an IA gives you more time to pay it all off. Figuring out which path is right for you is the most important decision you'll make in this entire process.

Getting Started: Your First Steps in IRS Negotiations

Staring at a massive tax bill can feel overwhelming, but you're not powerless. The trick is to be proactive and pick the right game plan from the get-go.

Your first move comes down to answering one tough, honest question: Can you realistically pay this debt in full if given more time, or is the total amount simply out of reach based on your current income and assets?

Your answer will point you directly toward one of two very different resolution paths.

Offer in Compromise: For True Financial Hardship

People often hear about the Offer in Compromise and think it’s the holy grail of tax relief. An OIC allows certain taxpayers to completely resolve their debt for a fraction of what they originally owed. But let’s be clear: this isn’t for everyone.

The IRS reserves this option for cases of genuine financial hardship. They will only accept an OIC if, after a deep dive into your finances, they conclude it's the absolute most they could ever realistically collect from you. You’re essentially proving that your ability to pay is permanently impaired.

It's a tough, documentation-heavy process. But for those who truly qualify, it's a legitimate financial fresh start.

Installment Agreement: When You Just Need More Time

What if you have the means to pay what you owe, just not all at once? That’s where an Installment Agreement comes in. An IA is simply a formal payment plan you set up with the IRS.

This lets you make manageable monthly payments over a longer period—often up to 72 months.

My Takeaway: An Installment Agreement doesn’t reduce your total debt; it just makes paying it off manageable. The IRS is far more inclined to approve an IA than an OIC because it guarantees they eventually get paid in full, along with any accrued interest and penalties.

To help you see the difference at a glance, here’s a quick breakdown of these two core negotiation strategies.

Comparing Your Main IRS Negotiation Options

This table offers a quick comparison of the two primary methods for negotiating tax debt with the IRS, helping you understand the best fit for your situation.

| Negotiation Method | Who It's For | Key Consideration | Typical Outcome |

|---|---|---|---|

| Offer in Compromise (OIC) | Taxpayers with significant financial hardship who can't pay their full tax debt. | Requires proving your "Reasonable Collection Potential" is less than the total debt. | Settle the tax debt for a lower amount. |

| Installment Agreement (IA) | Taxpayers who can pay the full amount but need more time to do so. | Your ability to make consistent monthly payments over a set period. | Pay the full tax debt, plus interest and penalties, over time (up to 72 months). |

Ultimately, choosing the right path from the start is what sets you up for success.

As you can see, Installment Agreements are built for wider accessibility and long-term repayment.

The Offer in Compromise, on the other hand, is an intensive, shorter-term resolution for those with serious financial limitations.

This distinction is everything. Trying to force an OIC when your situation really calls for an IA will only lead to a rejected proposal and wasted months.

A realistic assessment of your own finances isn't just helpful—it's essential.

Seeing Your Finances Through the IRS Lens

Before you even think about picking up the phone to negotiate with the IRS, you have to get one thing straight: your financial reality doesn't matter as much as their version of it. It’s a hard truth.

Your negotiation won’t be based on what you feel you can afford, but on what the IRS calculates you can pay using their strict, non-negotiable formulas.

Everything boils down to a single, critical number: your Reasonable Collection Potential (RCP).

Think of the RCP as the IRS’s bottom line. It’s their official estimate of how much they believe they can squeeze out of you.

This figure is a simple (but harsh) combination of your net monthly income (after they allow for certain expenses) plus the equity you hold in your assets.

Nailing this calculation is, without a doubt, the most important thing you can do to prepare for a successful negotiation.

Gathering Your Financial Arsenal

In my experience, IRS negotiations are won or lost long before the first conversation. They are won in the preparation stage, specifically with your documentation. You're not just filling out forms; you are building a case, and every document is a piece of evidence supporting your position.

Start gathering everything that tells your complete financial story.

You’ll need to pull together and organize:

Proof of Income: This means recent pay stubs, W-2s, 1099s, and any documentation for other income streams, like unemployment benefits, disability payments, or rental income.

Bank Statements: The IRS will want to see the last 3-6 months of statements for every single one of your accounts—checking, savings, and investments. Be ready for them to analyze every deposit and withdrawal.

Asset Details: Make a comprehensive list of everything you own. This includes your home, cars, boats, retirement accounts, and any other valuable personal property. You'll need fair market valuations and statements showing any loans you have against these assets.

Monthly Expense Records: Collect bills, receipts, and bank statements for all your regular living costs. This includes everything from your mortgage or rent and utilities to groceries, insurance, and car payments.

All of this paperwork feeds directly into the IRS Collection Information Statement—either Form 433-A (for individuals) or Form 433-B (for businesses). These forms are much more than just bureaucratic paperwork; they are the financial x-ray the IRS will use to dissect your life.

A classic mistake I see all the time is underestimating the level of detail required. If you pay a recurring bill in cash and don't have a receipt, the IRS might just disallow it. Document everything as if you're preparing for a court case, because in a way, you are.

Necessary vs. Conditional Expenses

Here’s where a lot of people get tripped up. The IRS doesn’t care about your budget; they care about their budget for you.

They split your expenses into two rigid categories, and this classification directly impacts what they think you can afford to pay them.

First, there are necessary expenses. The IRS uses a set of National and Local Standards to determine what you should be spending on basics like food, housing, and transportation.

If your actual costs are higher than their standardized amounts, you’ll need a very good, well-documented reason why the extra expense is critical to your family's health and basic welfare.

Everything else is often considered a conditional expense. This bucket includes things like private school tuition, charitable giving, or payments on unsecured debts like credit cards and personal loans.

The IRS may only allow you to keep paying these if you can prove you can still pay your tax debt in full within five years.

This is a major sticking point in negotiations. That $500 monthly payment on a high-interest credit card might feel essential to you, but to the IRS, it’s often just $500 that should be going to them instead.

By looking at your own budget through this unforgiving lens before you submit anything, you can build a proposal that’s grounded in their reality, not just yours.

This proactive approach shows the revenue officer you understand the rules of the game and are serious about finding a solution. That alone can make a world of difference.

Navigating the Offer in Compromise Path

The Offer in Compromise (OIC) is what many people think of when they dream of settling their tax debt.

It's the big one—the chance to resolve your liability for a fraction of what you originally owed. But let's be clear: this isn't a get-out-of-jail-free card.

The IRS doesn't hand these out easily. An OIC is reserved for very specific situations where they are convinced they can't collect the full amount from you, now or in the future.

Before the IRS will even look at your offer, you have to get your house in order. That means all your required tax returns must be filed, and you need to be current on any estimated tax payments for this year. This is a hard-and-fast rule with no exceptions.

Once that's done, you have to build your case on one of three specific arguments.

The Three Gates to an OIC

Your entire chance of success hinges on which of these three arguments you can prove.

Doubt as to Collectibility: This is the most well-trodden path and where the vast majority of successful OICs live. The argument is simple: "My financial situation is so dire that even if you seized my assets and garnished my wages, you still wouldn't get the full tax debt." This is a numbers game, and it all comes down to the Reasonable Collection Potential (RCP) we've talked about. Your offer must meet or beat that number.

Doubt as to Liability: This is a much rarer bird. Here, you aren't arguing that you can't pay the tax; you're arguing that you don't legally owe it in the first place. You need concrete proof that the IRS made a factual or legal mistake when they assessed the tax. This isn't about disagreeing with tax law—it's about proving the law was applied to you incorrectly.

Effective Tax Administration (ETA): This is the toughest and most subjective argument to win. With an ETA offer, you admit you owe the tax and technically have the assets to pay it. However, you argue that forcing you to pay would create an extreme economic hardship or would simply be unfair. Imagine a scenario where selling your home to pay the tax would leave your disabled spouse without necessary medical care. That's the level of severity we're talking about.

A Word of Caution: I've seen countless people try for an ETA offer and fail. The IRS approves these in only the most exceptional cases. You need to present a situation so compelling and unjust that it overrides their standard financial formulas. It’s a genuine uphill battle that requires immaculate documentation.

Why So Many OICs Get Rejected

The hard truth is that many, if not most, OICs are rejected or returned without even being considered. Knowing why they fail is the first step to building one that succeeds.

The Taxpayer Advocate Service (TAS) did a deep dive into this and found some shocking results. For many businesses, OIC acceptance rates can be as low as 30% to 45%.

What's truly stunning is that for a huge number of those rejections, the taxpayer’s offer was actually more than what the IRS’s own analysis determined it could collect. This shows a massive disconnect. You can see the full breakdown of these OIC negotiation challenges in the TAS study.

Besides a poorly calculated offer, here are a few other surefire ways to get rejected:

Incomplete Financials: Forgetting a bank account, an old 401(k), or a side gig's income is a fatal mistake. The IRS has ways of finding these things, and hiding them kills your credibility instantly.

Falling Out of Compliance: Your OIC is a living negotiation. If you stop filing new returns or miss a quarterly payment while the IRS is reviewing your offer, it's dead on arrival.

Making a "Lowball" Offer: Simply throwing a small number at the IRS without the financial data to back it up is a complete waste of everyone's time. Your offer has to be rooted in the reality of your RCP.

Crafting a Compelling Proposal

A successful OIC is built on a foundation of meticulous preparation. You're not just filling out forms; you are presenting a case. Every claim you make must be backed by indisputable proof.

Don't just write "I can't afford my rent." Show them. Provide bank statements, rent receipts, and a detailed budget that proves it. Your goal is to make it impossible for the IRS agent to deny the reality of your financial situation.

For instance, if you're self-employed with income that bounces around, don't cherry-pick a bad month. Give them a 12-month profit and loss statement to show the average and justify the income figure you're using.

If you have an expense that’s higher than the IRS national standards, write a detailed explanation for why it's essential for your family's health and safety.

Ultimately, you are telling a factual, evidence-based story that convinces the government that settling with you is the best and most logical financial decision they can make.

Securing a Manageable Payment Plan

So, an Offer in Compromise didn't pan out. Don't worry, that's not the end of the road. Far from it. The most common and reliable path for most people is actually an Installment Agreement (IA). This is your blueprint for getting on a payment plan that fits your life, not a plan that just sets you up to fail again down the line.

An IA is simply a formal deal with the IRS to pay what you owe in full through monthly payments. But while it sounds straightforward, it's not a one-size-fits-all solution. The right type of agreement for you hinges entirely on your financial picture and how much you owe.

Guaranteed and Streamlined Agreements

If you’re dealing with a smaller tax debt, the IRS has a couple of simplified options that cut out a lot of the back-and-forth negotiation.

Guaranteed Installment Agreement: Owe $10,000 or less in tax (not counting penalties and interest)? You're pretty much guaranteed an IA. The main catches are that you have to agree to pay it off within three years and you need a clean track record of filing and paying your taxes on time.

Streamlined Installment Agreement: This is the one most people end up with. If your total tab—tax, penalties, and interest combined—is under $50,000, you can usually get a plan to pay it off over 72 months (six years). The best part? You typically won't have to hand over a mountain of financial documents.

For many people, setting these up is as easy as using the IRS's Online Payment Agreement tool. It’s a quick way to get compliant and stop more aggressive collection actions in their tracks.

A word of caution from experience: Even if you qualify for a streamlined plan, don't just accept the monthly payment the IRS system spits out. That number might still wreck your budget. You can—and often should—propose a lower payment, but you’ll need to be ready to show them why.

Negotiating a Non-Streamlined Agreement

What if you owe more than $50,000? Or what if you just plain can't afford the monthly payment on a streamlined deal?

This is where the real negotiation begins. At this stage, you'll have to submit a Collection Information Statement (Form 433-A or 433-F) to prove you can't pay more.

The IRS playbook often pushes for repayment within a tight two-year window, a policy that can be a financial nightmare for someone with a large debt.

In fact, research from the Taxpayer Advocate Service has highlighted how these short repayment timelines and tough OIC standards create huge obstacles.

Their analysis shows a major disconnect between what the IRS thinks people can pay and what they realistically can pay. You can dig into the details in the TAS's comprehensive study.

Your entire goal here is to land on a payment you can actually stick with long-term. Defaulting on a payment plan is a serious misstep that can restart and even accelerate collection actions like wage garnishment.

To get a longer repayment term or a lower monthly payment, you need to build an ironclad case based on financial hardship.

Scenario: Justifying a Lower Payment

Let’s imagine you owe $80,000. On a standard 72-month plan, you’d be looking at a payment of over $1,100 a month, plus interest. But what if, after paying all your necessary living expenses, you only have $600 left over? That gap is your negotiating leverage.

Your argument isn't just a vague, "I can't afford it." It's a precise, evidence-backed statement: "Here is my financial data, which shows my maximum ability to pay is $600 per month without causing undue hardship."

By laying out meticulous documentation—pay stubs, bank statements, a detailed budget that aligns with the IRS's own expense standards—you change the conversation.

It's no longer about what the IRS wants; it's about what you can realistically deliver. This proactive, proof-based approach is the single best strategy for securing a payment plan that finally puts your tax debt behind you for good.

Mastering Communication and Documentation

When you’re negotiating with the IRS, your financial proposal is only one part of the equation. How you communicate—and how meticulously you document everything—can genuinely make or break your case. This isn't just about the numbers; it's about building credibility from the very first interaction.

One of the most powerful things you can do is make the first move. Don't wait for that dreaded certified letter to land in your mailbox.

By reaching out to the IRS before they come knocking, you immediately frame the situation as a good-faith effort to solve a problem.

That simple act puts you in control and sets a cooperative tone.

Professional Communication Is Non-Negotiable

Whether you find yourself on the phone with a Revenue Officer or you're drafting a formal response, your tone is everything. Keep every single interaction calm, respectful, and strictly focused on the facts.

Think about it from their perspective. IRS agents deal with angry, frustrated, and overwhelmed taxpayers all day long. Being the person who is organized, polite, and professional makes you stand out for all the right reasons.

This approach can build surprising goodwill and open the door to flexibility you wouldn't get otherwise. The agent on the other end is a person, not a faceless entity.

Treating them with respect can shift the entire dynamic from adversarial to collaborative. While overall satisfaction with IRS interactions has dipped to 75% as of 2024, my experience shows that clear, proactive dialogue is still the key to a better outcome.

The Power of the Paper Trail

I tell every client the same thing: if it isn't in writing, it didn't happen. Meticulous documentation is your single best defense and your strongest piece of evidence. Every letter, every phone call, every single interaction with the IRS must be recorded.

Expert Tip: After every phone call with an IRS agent, immediately send a follow-up letter. It doesn't have to be long. Just summarize the conversation, noting the date, time, agent’s name, and their employee ID number. Clearly state what was discussed and confirm the agreed-upon next steps. This creates an undisputed record.

This paper trail is critical for two reasons:

It creates accountability. It prevents "he said, she said" scenarios and holds the agent to their word. If your case gets reassigned, the new agent has a complete history to review.

It supports your case. Your detailed log becomes invaluable evidence. If you ever need to escalate the issue or challenge a decision, this documentation is your proof.

Dealing with the sheer volume of paperwork can be overwhelming. Some people are now looking into tools like AI for summarizing legal documents to help manage complex financial records. The concept is about taking a mountain of information and making it manageable—a principle that applies perfectly here.

By combining a proactive, respectful communication style with an ironclad paper trail, you build a powerful foundation of credibility.

This approach doesn't just strengthen your immediate proposal; it vastly improves your odds if a rejection forces you to figure out how to appeal an IRS decision. It proves you’re serious, organized, and committed to finding a fair resolution.

Answers to Your Toughest IRS Negotiation Questions

When you’re staring down a tax problem, squaring off with the IRS can feel like learning a whole new language. It’s only natural that a flood of questions will come up as you try to find your footing. Getting clear, honest answers is the first step toward making smart decisions and protecting your financial future.

Here, I’ll answer some of the most common questions I get from taxpayers, breaking down the jargon to give you the advice you need.

When Should I Bring in a Tax Professional?

This is probably the most important question to ask yourself right at the start. While you technically have the right to represent yourself before the IRS, knowing when to call in a pro is a strategic move that can save you an incredible amount of stress, time, and, ultimately, money.

I always tell people to seriously consider hiring a qualified tax attorney, CPA, or Enrolled Agent if they’re in one of these situations:

The debt is significant. If you owe the IRS more than $50,000, that’s my rule of thumb. The stakes are just too high, and the process gets exponentially more complex. Professional guidance isn't a luxury; it's a necessity.

You want to file an Offer in Compromise (OIC). This is the big one. The OIC process is notoriously difficult, with a high rejection rate and an avalanche of paperwork. An expert knows exactly how the IRS calculates your Reasonable Collection Potential (RCP) and can frame your offer to give you the best shot at getting it accepted.

You're completely overwhelmed. Let's be honest—if the letters, deadlines, and phone calls are causing you real anxiety, that’s more than enough reason to get help. A professional takes that weight off your shoulders so you can get back to your life.

Think of it this way: a seasoned tax pro has walked this path hundreds, if not thousands, of times. We know the pitfalls, the unwritten rules, and where to apply pressure to get a better deal than most people can secure on their own. Our experience is your greatest asset.

What Happens if the IRS Rejects My Offer?

Getting that rejection letter in the mail feels like a gut punch. I get it. But it is not the end of the line. Before you do anything else, take a breath and resist the urge to panic. That letter actually holds the key to your next move.

The IRS has to tell you why they rejected your offer. This isn't some vague denial; it's a specific critique of your proposal. Usually, it comes down to a few things, like a disagreement over your asset values, disallowed living expenses, or an offer amount they feel is too low based on their RCP calculation.

Key Insight: A rejection isn't a final "no." It's an invitation to do better. The IRS just gave you a roadmap detailing exactly what they didn’t like about your first attempt.

You have a few clear paths forward after a rejection:

Appeal the Decision: You have 30 days from the date on the letter to file an appeal. This sends your case to the IRS Office of Appeals, which is an independent division of the IRS, giving you a fresh set of eyes.

Submit a New Offer: Use the feedback from the rejection to fix your proposal. Maybe you need better documentation for an expense, or you need to adjust your offer to be more in line with what they expect.

Change Your Strategy: Sometimes, a rejection makes it clear an OIC just isn't in the cards. That's okay. You can immediately pivot and start negotiating an Installment Agreement, which is often a more straightforward solution.

The goal is to treat the rejection as a learning opportunity. You can find more detailed strategies in our complete guide on how to negotiate IRS debt and come back with an even stronger plan.

Can I Negotiate Away Penalties and Interest?

Yes, you can, but it’s crucial to understand how it works for each. The short answer is that negotiating penalties is very possible, while negotiating interest is extremely difficult.

Your best tool here is called Penalty Abatement. The IRS has the authority to remove penalties if you can show you had a reasonable cause for failing to file or pay on time. This has to be more than just a bad year; it needs to be a specific, unavoidable event.

Common Examples of Reasonable Cause:

A serious illness or death involving you or an immediate family member.

Your home or business records were destroyed in a fire, flood, or another disaster.

You relied on incorrect advice from a competent tax professional.

An error or significant delay on the IRS’s part caused the problem.

To make the request, you’ll file Form 843, Claim for Refund and Request for Abatement. You need to write a clear, detailed explanation and provide proof, like medical records or a letter from your accountant.

Interest is a different beast. By law, the IRS must charge interest on unpaid taxes. It can only be reduced in very rare cases, usually involving a major IRS error. But there’s a silver lining here: interest is charged on your outstanding tax and penalty balance.

What does that mean for you? It means that if you successfully lower your core tax debt with an Offer in Compromise or get your penalties abated, the amount of interest you owe will drop automatically. The best strategy is always to attack the principal tax and penalties first.

At Attorney Stephen A Weisberg, we know how overwhelming it is to face the IRS. That’s why we start with a FREE Tax Debt Analysis to map out the best path for your specific situation. If you're tired of struggling with tax debt and need an expert in your corner, visit us at weisberg.tax to see how we can help you get the best possible result.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034