How to Remove a Tax Lien: Easy Steps to Restore Financial Health

Understanding Tax Liens: What’s at Stake For Your Future

A tax lien is the government's legal claim against your assets when you have unpaid taxes. This claim can affect various assets, including real estate, vehicles, bank accounts, and investments. The lien remains until the debt is resolved.

Discovering an IRS lien notice can be alarming, potentially disrupting loan approvals and property sales. Understanding how these liens work is crucial for regaining financial control.

Types Of Tax Liens And How They Attach

Not all tax liens are the same. While federal, state, and local liens share some similarities, they differ in filing requirements and public notice procedures.

Federal Tax Liens: Filed by the IRS under IRC §§ 6321 and 6322.

State Tax Liens: Governed by individual state statutes and often recorded at the county level.

Local Tax Liens: Typically for unpaid property taxes and may lead to municipal auctions.

This distinction explains why multiple liens might appear on different assets across various jurisdictions, each requiring a specific approach.

Real-World Consequences And Credit Reporting

The impact of tax liens goes beyond property restrictions. Prior to April 2018, tax liens could significantly lower credit scores, often by more than 100 points. However, major credit bureaus removed tax liens from consumer reports to improve accuracy.

While liens no longer appear on credit reports, they can still hinder refinancing, home equity loans, and other credit options until the debt is paid.

Full payment remains the quickest way to lift a lien. The IRS usually issues a release within 30 days of clearing the debt.

Learn more about understanding a federal tax lien.

Comparing Liens At A Glance

| Resolution Factor | Federal Lien | State Lien | Local Lien |

|---|---|---|---|

| Filing Authority | IRS | State Department of Revenue | County or City Tax Office |

| Public Record | UCC-1 filing | County recorder | Municipal records |

| Release Timeline | 30 days after payment | Varies by state law | Often within 60 days |

| Credit Report Impact* | No longer reported (post-2018) | Similar removal policies may vary | Generally not reported |

| Priority | Superior to most mortgages | Depends on state statutes | Often junior to other liens |

*Liens removed from credit reports by major bureaus as of April 2018.

Next Steps For Safeguarding Your Assets

Even after a lien is released, rebuilding credit and planning for future tax obligations is essential. This requires a comprehensive strategy.

Developing a plan, perhaps using a business continuity plan checklist, can help you establish savings buffers, allocate funds for taxes, and implement monitoring practices. These steps can help prevent future liens and improve your credit standing.

Full Payment Strategy: The Direct Path to Lien Removal

Paying your tax debt in full is the simplest way to remove a tax lien. This approach offers immediate resolution and provides peace of mind.

However, it's essential to understand what "full payment" entails. It encompasses not only the original tax amount but also any accrued penalties and interest.

Calculating Your Total Tax Liability

Figuring out your total payoff amount involves more than just the initial tax assessment. Penalties, often a percentage of the unpaid taxes, accumulate over time.

Interest also accrues on both the original tax and the penalties, increasing the total due. You might want to learn how to stop IRS wage garnishment to protect your earnings.

For instance, a $5,000 tax debt with a 25% penalty adds $1,250 to your liability. Interest then compounds on the combined $6,250. Addressing tax issues promptly is crucial to avoid a much larger debt than initially expected.

Confirming Your Payoff Amount and Payment Methods

Contacting the IRS directly is vital to confirm your exact payoff amount. This ensures accuracy and prevents future issues.

The IRS offers several payment options, including online payments, checks, money orders, and debit or credit cards. The best method depends on your specific situation and resources.

Understanding the implications of each payment method is important. Some methods may have fees, while others offer immediate processing. Informed decisions about payment can save you both time and money.

Post-Payment Steps: Securing Lien Release and Documentation

After full payment, obtaining the official lien release is the next critical step. This document confirms the lien's removal from your assets, protecting your property rights and financial standing. It's vital to verify the lien release is correctly recorded with the relevant county authorities.

Within 30 days of full payment, the IRS releases the lien. It's important to distinguish between a release (removal) and a withdrawal (deletion from credit history).

A withdrawal can potentially improve credit scores. The IRS might withdraw a lien if it benefits both the taxpayer and the government.

Learn more about lien release vs. withdrawal. Ensuring accurate public records reflects your resolved tax debt safeguards your financial future.

Payment Plans That Actually Work: IRS Installment Options

If paying off your tax debt in full feels impossible, IRS installment agreements can offer a structured solution to help remove a tax lien. These agreements break down your debt into manageable monthly payments. Choosing the right type of installment agreement is key, so understanding your options is important.

Streamlined Vs. Non-Streamlined Installment Agreements

The IRS offers several installment agreement options. Each has specific requirements and advantages.

A streamlined installment agreement is generally the easiest to qualify for, requiring less paperwork if your total tax debt is relatively low.

These agreements are typically available if you owe less than $50,000, including penalties and interest. Often, these agreements are set up with automatic payments via direct debit.

For larger tax debts exceeding $50,000, a non-streamlined installment agreement may be necessary. These agreements involve a more in-depth review by the IRS and require more detailed financial documentation.

This means the application process is more complex, but it can handle higher debt amounts. Be prepared for a longer processing time and potential ongoing communication with the IRS.

You may find helpful information in our ultimate guide to IRS back taxes payment plan strategies.

Partial Payment Installment Agreements: An Option for Unique Circumstances

In some situations, a partial payment installment agreement (PPIA) might be an option. A PPIA lets you make monthly payments based on what you can reasonably afford.

These agreements are usually reserved for taxpayers facing significant financial hardship. The IRS assesses your income, expenses, and assets to determine an affordable payment amount. While a PPIA helps you work towards resolving your tax debt, it might not remove the lien entirely.

Lien Subordination and Withdrawal During Installment Agreements

While on an installment agreement, you might be able to negotiate lien subordination or withdrawal. Subordination allows other creditors to have priority over the IRS lien. This can be helpful for refinancing or securing new loans.

Withdrawal completely removes the lien, providing more financial flexibility. Successfully negotiating either option requires showing responsible financial behavior and adherence to your installment agreement. This often includes a consistent payment history and a plan for future tax compliance.

Structuring a Successful Installment Agreement Application

Submitting a well-organized application increases your chances of approval. Include accurate and complete financial information, clearly document your income and expenses, and propose a realistic payment plan.

Working with a tax professional can be extremely beneficial. They can help you understand complex IRS procedures and ensure your application meets all requirements. This professional guidance can significantly improve your chances of a successful outcome.

Settling For Less: Navigating Offers in Compromise

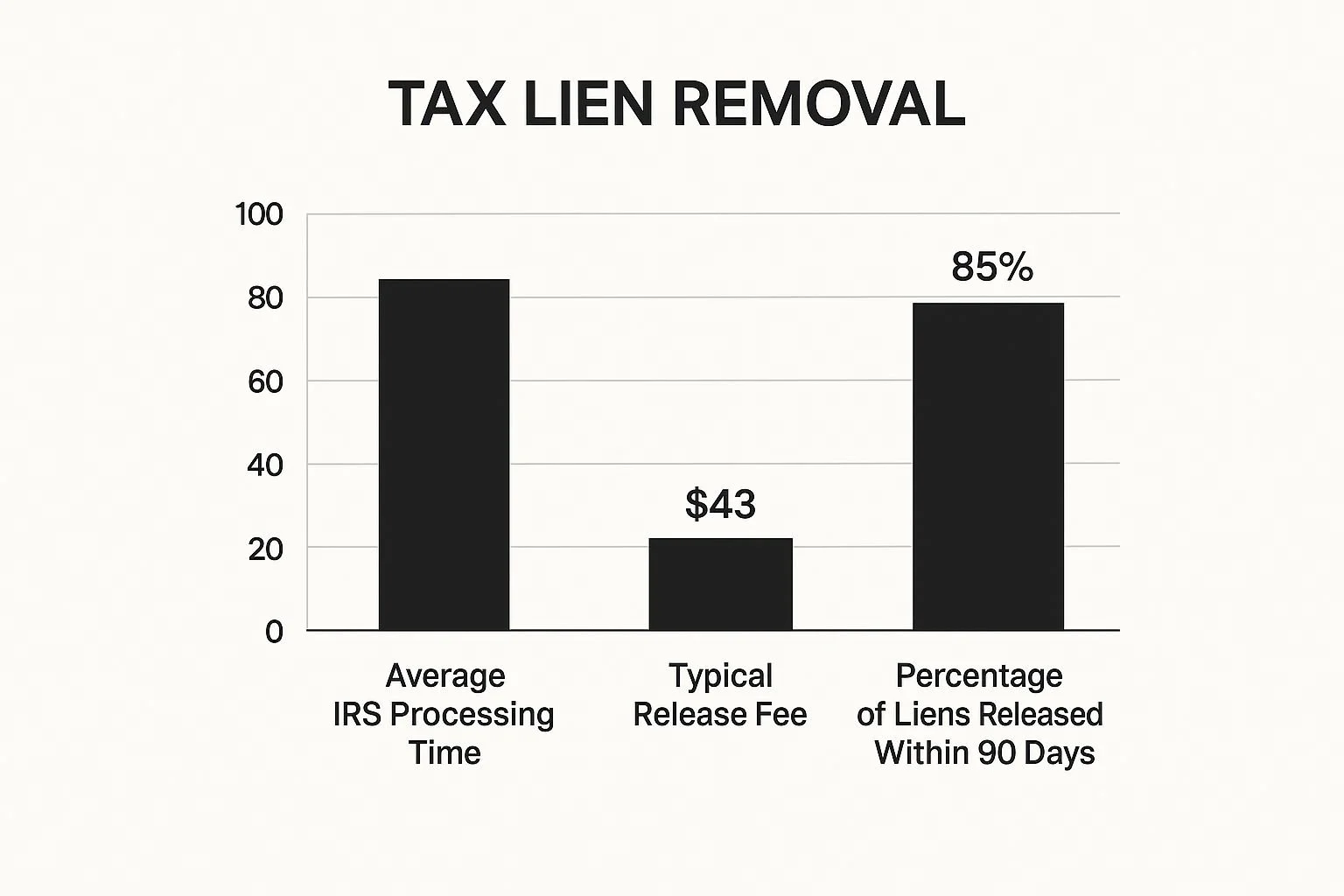

The infographic above illustrates key metrics about removing a tax lien. It covers average IRS processing times, typical release fees, and the percentage of liens released within 90 days. The data reveals that the IRS generally processes lien releases within six weeks, with a minimal release fee of $43.

Furthermore, 85% of liens are released within 90 days. This suggests a relatively quick process once the underlying tax debt is resolved. Beyond installment agreements, there's a powerful option many taxpayers overlook: the Offer in Compromise (OIC).

This program allows you to settle your tax debt for less than the full amount. It can be a significant help for those struggling with a substantial tax burden.

For a deeper dive, check out our complete guide to tax debt settlement.

Three Pathways to an Offer in Compromise

The IRS doesn't broadly publicize the three primary ways to qualify for an OIC. Understanding these pathways can significantly boost your chances of approval. These pathways revolve around your ability to pay, doubt as to liability, and effective tax administration.

Ability to Pay: This pathway examines your assets, income, and expenses. It determines whether you can realistically pay your full tax debt.

Doubt as to Liability: If you have valid questions about the accuracy of the assessed tax, this pathway may be suitable.

Effective Tax Administration: This is rarely used. It applies when collecting the full debt would create extreme hardship or be unjust due to specific circumstances.

Determining a Realistic Offer Amount

Creating a successful OIC involves finding a balance between what you can manage and what the IRS will find acceptable. A thorough review of your finances is key.

Consider factors like your reasonable living expenses, the liquidation value of your assets, and your future income potential.

The IRS aims to collect what is reasonably collectible, not to impoverish taxpayers. Demonstrating a genuine inability to pay the full amount is crucial.

Documentation Strategies and Timing

Thorough documentation is vital for a successful OIC. Collect detailed records of your income, expenses, assets, and liabilities. This documentation supports your claim and shows your commitment to resolving the debt.

Timing is also important. Submitting an OIC during financial hardship strengthens your case. However, prioritize accuracy and completeness over speed. Don't submit a rushed offer.

The following table summarizes different tax lien resolution options:

Comparison of Tax Lien Resolution Options

| Resolution Method | Requirements | Timeline | Effect on Credit | Pros | Cons |

|---|---|---|---|---|---|

| Offer in Compromise (OIC) | Demonstrated inability to pay full amount; Doubt as to liability; Effective Tax Administration | Varies, can take several months | Can negatively impact credit, but less than ongoing tax lien | Can significantly reduce tax debt; Fresh start financially | Complex process; Requires thorough documentation; Not always approved |

| Installment Agreement | Regular income; Ability to make monthly payments | Depends on the amount owed and payment plan | Can still negatively impact credit, but shows effort to repay | More manageable monthly payments | Debt takes longer to pay off; Accrues interest and penalties |

| Currently Not Collectible (CNC) | Severe financial hardship; Inability to pay basic living expenses | Temporary suspension of collection efforts; Can last for years | Negative impact on credit | Immediate relief from collection actions | Doesn't eliminate the debt; Can be revoked if financial situation improves |

This table outlines various methods for addressing tax liens, highlighting their respective requirements, timelines, impact on credit scores, advantages, and disadvantages. Choosing the right strategy depends on individual circumstances and financial capabilities.

Resubmission and Alternative Options

If your initial OIC is rejected, you can resubmit a revised offer. Address any concerns the IRS raised. Alternatively, consider other options like Currently Not Collectible (CNC) status.

CNC temporarily halts collection efforts while you rebuild your financial standing. This can provide much-needed relief and give you time to regain stability.

Beyond Release: The Power of Lien Withdrawal

Releasing a tax lien stops the IRS from collecting further. However, it doesn't remove the lien's public record. This lingering record can still negatively impact your financial future.

Withdrawal, on the other hand, completely removes the lien from public records. It's as if the lien never existed. This is a crucial difference for your financial recovery.

When Does The IRS Consider Withdrawal?

The IRS considers lien withdrawal under certain circumstances. One common scenario is when you enter a Direct Debit Installment Agreement (DDIA).

A DDIA automates your monthly tax payments, demonstrating responsible financial behavior.

This proactive step can increase your likelihood of lien withdrawal approval.

Another scenario involves situations where withdrawing the lien benefits both the taxpayer and the government.

For example, if the lien prevents you from securing a loan necessary for repaying the tax debt, the IRS might consider withdrawal.

When negotiating with the IRS, explore options like settling for less through an Offer in Compromise (OIC). This can relate to strategies such as Tax Pooling.

Crafting A Compelling Form 12277 Application

To request lien withdrawal, you must submit Form 12277, Application for Withdrawal of Filed Notice of Federal Tax Lien.

This application requires detailed information about your finances and your reasons for requesting withdrawal. Emphasize how withdrawal benefits both you and the IRS.

For instance, explain how removing the lien will help you secure financing to repay your debt or improve your job prospects. Supporting documentation strengthens your application.

Financial statements

Tax returns

Relevant IRS correspondence

These documents validate your claims and show your commitment to resolving your tax liability. A significant portion of tax liens result in substantial debt collection for the government.

A study revealed that approximately 93% of collected dollars from taxpayers with filed federal tax liens came from those with income exceeding allowable living expenses or with assets that could cover the balance. This highlights the IRS’s focus on taxpayers with adequate resources.

Timing Your Request And Comparing Strategies

The timing of your withdrawal request matters. Submitting the request after demonstrating a consistent period of responsible financial management, such as regular payments under a DDIA, improves your chances of approval.

Finally, compare withdrawal to subordination. Withdrawal removes the lien entirely. Subordination allows other creditors to take priority over the IRS lien.

This can be helpful for specific financial transactions, but it doesn't eliminate the lien. The best approach depends on your unique situation and financial objectives. Consulting a tax professional can provide personalized guidance.

Fighting Back: Appeals Strategies That Get Results

Sometimes, a tax lien is filed incorrectly or unfairly. You have more rights than you realize. This section explores how to effectively navigate the appeals process, from Collection Due Process (CDP) hearings to Tax Court proceedings.

Understanding Your Appeals Options

Several avenues exist for challenging a tax lien. Choosing the right one depends on your specific situation. The Collection Appeals Program (CAP) offers a less formal route than Tax Court for disputes related to lien notices, levies, and seizures.

A CDP hearing allows you to challenge IRS collection actions before they escalate. For more complex cases, appealing directly to the U.S. Tax Court might be necessary.

Critical Timing and Documentation

Timing is crucial in tax lien appeals. Strict deadlines apply, and missing them can severely limit your options. You typically have 30 days after receiving a Notice of Federal Tax Lien to request a CDP hearing.

Persuasive documentation is essential for a successful appeal. This includes records of your tax payments, communications with the IRS, and any evidence supporting your claim. Organized and comprehensive documentation demonstrates your commitment to resolving the issue.

Framing Your Arguments for Maximum Impact

Presenting your arguments clearly and concisely strengthens your appeal. Focus on the specific facts of your case and the applicable tax laws.

For example, if the lien is based on an incorrect tax assessment, provide evidence of the correct amount. If you believe the IRS didn't follow proper procedures, explain the deviations and their impact. Build your case with evidence and clear explanations.

CAP vs. Tax Court: Choosing the Right Venue

The CAP offers a more streamlined process than Tax Court. CAP appeals are handled administratively within the IRS, while Tax Court proceedings are more formal and involve court hearings.

CAP is often better for less complex disputes, while Tax Court is more appropriate for challenging the underlying tax liability. This distinction is important in choosing the most effective approach.

The Impact of Bankruptcy on Tax Liens

Bankruptcy can significantly affect your tax lien. While it doesn't automatically eliminate tax debt, it can temporarily halt collection actions and potentially discharge certain tax liabilities.

However, the interaction between bankruptcy and tax liens is complex. The outcome depends on the type of bankruptcy filed and the nature of the tax debt. Consult with a tax attorney specializing in bankruptcy to understand the implications for your situation.

Securing a Certificate of Release and Correcting Credit Reports

If your challenge is successful, the IRS will issue a Certificate of Release. This document officially removes the lien from your assets. Ensure this certificate is correctly filed with the appropriate county authorities.

Once the release is recorded, follow up with all three major credit bureaus (Experian, Equifax, and TransUnion) to ensure its removal from your credit reports. Proactively monitoring your credit reports after a lien release protects your financial reputation.

Rebuilding After The Storm: Your Financial Recovery Plan

Removing a tax lien is a big step toward financial recovery. But it's just the beginning. Think of it like repairing a house after major damage. You've patched the roof (removed the lien), but now it's time to rebuild and reinforce your financial foundation for the future.

Repairing Your Creditworthiness

While tax liens no longer show up directly on credit reports, the underlying problems that led to the lien can still impact your creditworthiness. Late payments or outstanding debts, for example, can significantly lower your credit score. This means rebuilding credit requires a focused, proactive strategy.

Consistent On-Time Payments: The most effective way to boost your credit score is by consistently making all payments on time. This shows lenders you’re committed to responsible financial behavior.

Reduce Debt Levels: Aim to reduce outstanding balances on credit cards and other loans. A lower debt-to-credit ratio indicates improved financial health.

Diversify Credit: Having a mix of credit types (credit cards, installment loans, etc.) can positively influence your score over time.

Communicating With Lenders

You might need to explain the tax lien situation to potential lenders, even if it's not on your credit report. Honesty and transparency are key. Frame the experience as a learning opportunity and emphasize the improvements you've made.

Provide Context: Explain the circumstances that resulted in the tax lien. This shows you understand the issue and have taken steps to prevent it from happening again.

Highlight Positive Changes: Focus on the positive steps you've taken, such as budgeting, automatic payments, or working with a financial advisor.

Documentation: Keep documentation of the lien release or withdrawal to reassure lenders and provide proof of the resolved tax issue.

Preventative Tax Strategies For A Stronger Future

Preventing future tax liens requires proactive planning and solid financial habits. Think of this as strengthening your financial “house” to weather future storms.

You may want to check out our guide on finding expert help with tax debt relief companies.

Automated Savings: Setting up automatic transfers to a savings account specifically for taxes can help ensure you have the funds when they are due.

Strategic Tax Planning: Understanding tax laws and deductions can minimize your tax burden. Consult with a tax professional to explore personalized strategies.

Regular Monitoring: Regularly reviewing your financial statements and tax documents lets you catch potential problems early and take corrective action.

Monitoring Your Credit Reports

Even though tax liens are no longer directly reported, regular credit monitoring is vital for maintaining good financial health. This allows you to identify errors or inaccuracies on your report and address them quickly.

To better understand the credit recovery timeline, take a look at the table below. It outlines the typical progression after a tax lien is removed, alongside recommended actions and potential obstacles.

| Time Period | Expected Credit Impact | Recommended Actions | Common Obstacles |

|---|---|---|---|

| First 30 Days | Little to no immediate change | Request updated credit reports from all three major bureaus (Experian, Equifax, and TransUnion). | Difficulties obtaining updated reports. |

| 3-6 Months | Gradual improvement as positive payment history accumulates. | Continue making on-time payments and reducing debt. Consider a secured credit card if necessary. | Old negative information may still impact credit applications. |

| 6-12 Months | Continued improvement. May qualify for better loan terms. | Focus on diversifying credit and maintaining a low credit utilization ratio. | Securing new credit may still be challenging. |

| 12+ Months | Significant improvement. Access to more credit options at favorable rates. | Maintain healthy financial habits and regularly monitor credit reports. | Recovery can be slower if other negative items remain on your credit report. |

As this table shows, credit repair takes time and consistent effort. By following these recommended actions, you can steadily improve your financial standing.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: sweisberg@wtaxattorney.com

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034