IRS Notice of Deficiency Explained

An IRS Notice of Deficiency isn't a bill. It's a formal, legal determination from the IRS saying they believe you owe more in taxes than what you reported, usually after an audit or review.

Most tax professionals simply call it a “90-day letter,” and for good reason. That name highlights the most critical part of the notice: it fires the starting gun on a strict, 90-day window for you to formally challenge their findings in U.S. Tax Court—before you have to pay the amount they're proposing.

What an IRS Notice of Deficiency Really Means

Getting any letter from the IRS can send your stomach into knots, but let’s take a breath. Understanding what a Notice of Deficiency (or NOD) actually is puts you back in the driver's seat.

Think of it this way: this isn't a final, unchangeable demand for money. It’s a formal proposal. It’s the IRS officially putting on paper, "Hey, we've reviewed your return, we think there's a problem, and this is what we believe you owe." It’s an argument, not a verdict.

A better analogy might be a building inspector who, after checking your property, hands you a formal report with a list of required fixes. That report isn't a condemnation notice; it’s a documented assessment. More importantly, it kicks off a specific period where you can respond, bring in your own engineer, or contest the findings. The Notice of Deficiency works exactly the same way.

The Purpose of This Formal Notice

So, why does the IRS send this specific, formal letter? It's not just another piece of mail. The primary purpose is twofold: to inform you of their proposed tax adjustment and, crucially, to grant you specific legal rights.

This notice has to be sent by certified mail to your last known address, creating a legal paper trail of its delivery. This isn't just bureaucratic red tape; it’s a legally required step the IRS must take before they can officially assess the tax and start trying to collect it.

This process is your shield. Under Internal Revenue Code (IRC) Sections 6212 and 6213, the government is generally forbidden from assessing additional income, estate, or gift taxes until after it sends you a Notice of Deficiency and the 90-day clock has run out. You can dig into the full IRS procedures for these notices to see the legal framework for yourself.

The Key Takeaway: The Notice of Deficiency is your ticket to the U.S. Tax Court. It is the only IRS notice that gives you the right to have your case heard in court before you have to pay a single dollar of the disputed tax.

Understanding the Critical 90-Day Window

That nickname, the "90-day letter," is the most important thing to remember. It’s not just catchy—it's a literal, legally binding deadline.

From the date printed on your notice, you have precisely 90 days to file a petition with the U.S. Tax Court. If you live outside the United States, that window is extended to 150 days.

Let me be crystal clear: This deadline is absolute. It cannot be extended by you, the IRS, or even the Tax Court. Missing this deadline has serious, immediate consequences.

You lose your prepayment rights. Your chance to go to Tax Court before paying the disputed amount is gone.

The IRS assesses the tax. What was a "proposal" instantly becomes a legal debt you owe.

Collection actions begin. Once the tax is assessed, the IRS can move forward with things like liens and levies to collect the money.

The worst thing you can do is panic or ignore the letter. Your goal should be to shift from a place of fear to one of clear, strategic action. This notice isn't meant to scare you; it’s designed to empower you with a choice.

Key Elements of Your Notice of Deficiency

When you first open that envelope, it can feel overwhelming. This quick reference table breaks down the most important parts of your 90-day letter so you can quickly understand what you're looking at and what to do next.

| Element | What It Means for You | Your Next Step |

|---|---|---|

| Notice Date | This is the official start date of your 90-day or 150-day deadline. Every day counts. | Immediately circle this date and calculate your filing deadline. Do not delay. |

| Tax Year(s) in Question | The specific tax return(s) the IRS has audited and is proposing changes to. | Gather all your records, receipts, and documents for that specific year or years. |

| Amount of the Deficiency | This is the total additional tax the IRS believes you owe, broken down by tax, penalties, and interest. | Review the amount, but don't panic. This is the IRS's opening position, not the final number. |

| Explanation of Adjustments | This section (often in a separate form) explains why the IRS is making changes—disallowed deductions, unreported income, etc. | This is the heart of the dispute. Analyze these reasons carefully to build your counter-argument. |

| Your Response Options | The letter will outline your choices: agree, disagree and petition the Tax Court, or do nothing. | Decide on your strategy. The most common next step for a dispute is to prepare a Tax Court petition. |

Think of this table as your roadmap. By identifying these key pieces of information, you can demystify the document and begin planning your response methodically instead of emotionally.

Why the IRS Sent You This Notice

An IRS Notice of Deficiency doesn't just show up on your doorstep by accident. It's actually the final step in a very specific process, and figuring out what triggered it is the first move you need to make. Think of it less like a surprise attack and more like the IRS formally documenting its conclusions after a review or audit.

The "why" behind your notice is everything. It's like a doctor diagnosing an illness before even thinking about treatment. Once you pinpoint the exact reason for the notice, you can start gathering the right documents and building the strongest possible case to fight the IRS's proposed changes.

The Most Common Trigger: Automated Underreporter Programs

One of the most frequent reasons a Notice of Deficiency gets sent out starts with a simple data mismatch. The IRS uses a powerful, automated system that cross-references the income you reported on your tax return with the information it gets from third parties.

Those third parties—your employers, clients, and banks—are all legally required to report what they paid you.

W-2 Forms: Your employer reports your wages and salary.

1099-NEC Forms: Clients report what they paid you for freelance or contract work.

1099-INT/DIV Forms: Banks and investment firms report interest and dividend income.

1099-K Forms: Payment processors like PayPal or Square report transactions if you sell goods or services.

If the income you reported is lower than what these third parties told the IRS they paid you, a red flag immediately goes up. The IRS computer system, officially called the Automated Underreporter (AUR) program, will usually send an initial notice (like a CP2000) proposing changes. If you don't respond to that first notice or can't resolve the discrepancy, the situation can escalate into a formal IRS Notice of Deficiency.

Disagreements After an Audit

Another well-worn path to receiving a 90-day letter is an audit that ends in a stalemate. This can unfold in a couple of ways.

The IRS might have started with a correspondence audit, where they questioned specific deductions or credits through the mail. For example, they might challenge your Head of Household filing status or ask for receipts for large charitable donations. If the proof you send back doesn't convince the examiner, they’ll move to disallow the tax benefit.

Or, you may have gone through a more hands-on office audit or an intensive field audit. If you and the auditor just can't see eye-to-eye on the final numbers—meaning you stand by your return and the auditor disagrees—the auditor’s next move is to issue the formal Notice of Deficiency. This letter officially states the IRS's final position and opens the door for you to take your case to the next level.

For some taxpayers in especially difficult situations, it might be worth seeing if they qualify for a specialized IRS tax forgiveness program, though that's a separate avenue from the audit appeal process.

The Notice of Deficiency is essentially the IRS saying, "We've looked at everything, heard your side, and we are formally standing by our proposed changes. The ball is in your court now."

Understanding what triggered your notice is critical. It tells you exactly which part of your return is under the microscope—whether it's unsubstantiated business expenses, questionable deductions, or complex credits. Knowing the specific point of disagreement is your launching pad for a successful appeal.

Understanding Your Rights and the 90-Day Deadline

When an IRS Notice of Deficiency lands in your mailbox, your eyes might jump straight to the proposed tax bill. But the single most important piece of information on that letter is the date printed right at the top.

That date fires the starting gun on a countdown that is absolute, non-negotiable, and the key to protecting your rights. This is the infamous 90-day deadline, and letting it slip by is the biggest mistake you can make. The clock starts ticking from the day the IRS mails the notice, not the day it arrives in your mailbox or the day you finally open it.

The Power of the 90-Day Clock

Don't think of this as a friendly reminder from the IRS. It's a hard-and-fast deadline baked into federal law, and it is strictly enforced. No one—not the IRS, not even the U.S. Tax Court—can give you an extension. If that 90th day comes and goes, your most powerful right as a taxpayer is gone for good.

So what is this critical right? It's your ability to challenge the IRS's claims in U.S. Tax Court, where an independent judge will review your case before you have to pay a single dime of the disputed tax.

The 90-day window is your one and only chance to challenge the IRS on neutral ground without first writing a check for the tax they claim you owe. Missing it means you forfeit this right forever.

This “prepayment forum” is a massive advantage for taxpayers. It completely levels the playing field, letting you argue the facts of your case without the immense financial pressure of paying the disputed tax first and then suing to get it back—a far more complicated and expensive path.

How Filing a Petition Protects You

Taking action within those 90 days by filing a petition with the U.S. Tax Court does more than just get your foot in the courthouse door. It acts like a legal shield, instantly putting a freeze on all IRS activity.

Once your petition is properly filed, the IRS is legally blocked from two key actions:

Assessing the Tax: They cannot officially add the proposed deficiency to your tax account as a formal, collectible debt.

Initiating Collections: The agency can't start coming after you with tools like federal tax liens or bank levies for the amount you're disputing.

This legal pause gives you invaluable breathing room and flips the power dynamic. Suddenly, the IRS is on the defensive, required to formally respond to your petition and justify its position. Far from guaranteeing a dramatic courtroom trial, filing a petition is often the very thing that opens the door to more productive settlement talks.

The Consequences of Inaction

What happens if you ignore the notice and let the 90-day clock run out? The fallout is both swift and severe.

On day 91, what was just a "proposal" is no longer a proposal. The IRS will automatically assess the tax, turning it into a legally enforceable debt. Shortly after, the collection machine will whir to life, and you’ll start seeing bills and demands for payment show up.

At that point, your options for fighting back become incredibly limited and much more expensive. You’d have to pay the entire tax bill, penalties, and interest first, then file a formal claim asking for a refund.

If the IRS denies your claim, your only path forward is to sue them for a refund in either a U.S. District Court or the U.S. Court of Federal Claims—a route that is almost always more costly and procedurally difficult than the Tax Court.

Knowing how to appeal an IRS decision properly after filing a petition is crucial. Understanding what comes next, like the potential for settlement negotiations with the IRS Appeals Office, can make all the difference in reaching a better outcome. It's about staying in control of the process, not just reacting to the IRS's next move.

Your Three Strategic Response Options

Now that you understand what a Notice of Deficiency is and the hard-and-fast 90-day deadline it comes with, it's time to decide on your next move. This isn't a choice to take lightly. Each path you choose has dramatically different consequences for your finances and your legal standing with the IRS.

You're at a crossroads with three potential routes. Let's walk through what each one looks like in the real world so you can make an informed decision.

Path 1: Agree and Pay the Proposed Amount

The simplest path is to agree with the IRS's adjustments. If you review the notice and realize they're right—maybe you missed a 1099 or took a deduction you didn't qualify for—this could be your best bet.

To do this, you'll sign the Form 4089, Notice of Deficiency-Waiver, that came with your notice and mail it back. The big advantage here is that signing the waiver usually stops the clock on interest accumulation about 30 days after the IRS gets it, which can save you a decent amount of money.

Just be aware that signing is a final act. You're officially giving up your right to dispute the matter in Tax Court, and the IRS can now legally collect the full amount.

Path 2: Ignore the Notice

This isn't a strategy; it's a surrender. Doing nothing and letting that 90-day window slam shut is, without question, the worst possible choice you can make.

By ignoring the notice, you automatically forfeit your right to challenge the IRS in U.S. Tax Court before paying a dime. The moment day 91 hits, the proposed tax becomes a final, assessed liability. The IRS's powerful collection machine will fire up, and you'll soon be facing down federal tax liens, wage garnishments, and bank levies.

Choosing inaction is an active decision to surrender your rights. The IRS will proceed with assessment and collection, leaving you with fewer, more expensive options to fight back later.

Path 3: Challenge the IRS by Filing a Petition

Your third, and most powerful, option is to fight back. By filing a timely petition with the U.S. Tax Court, you preserve all your legal rights and put the ball back in your court.

This single step immediately freezes the IRS in its tracks. They are legally barred from assessing the tax or starting any collection actions against you.

It also moves your case out of the hands of the auditors and, in most situations, over to the IRS Independent Office of Appeals. This is a game-changer because Appeals officers are there to resolve disputes and broker settlements, not to find more problems.

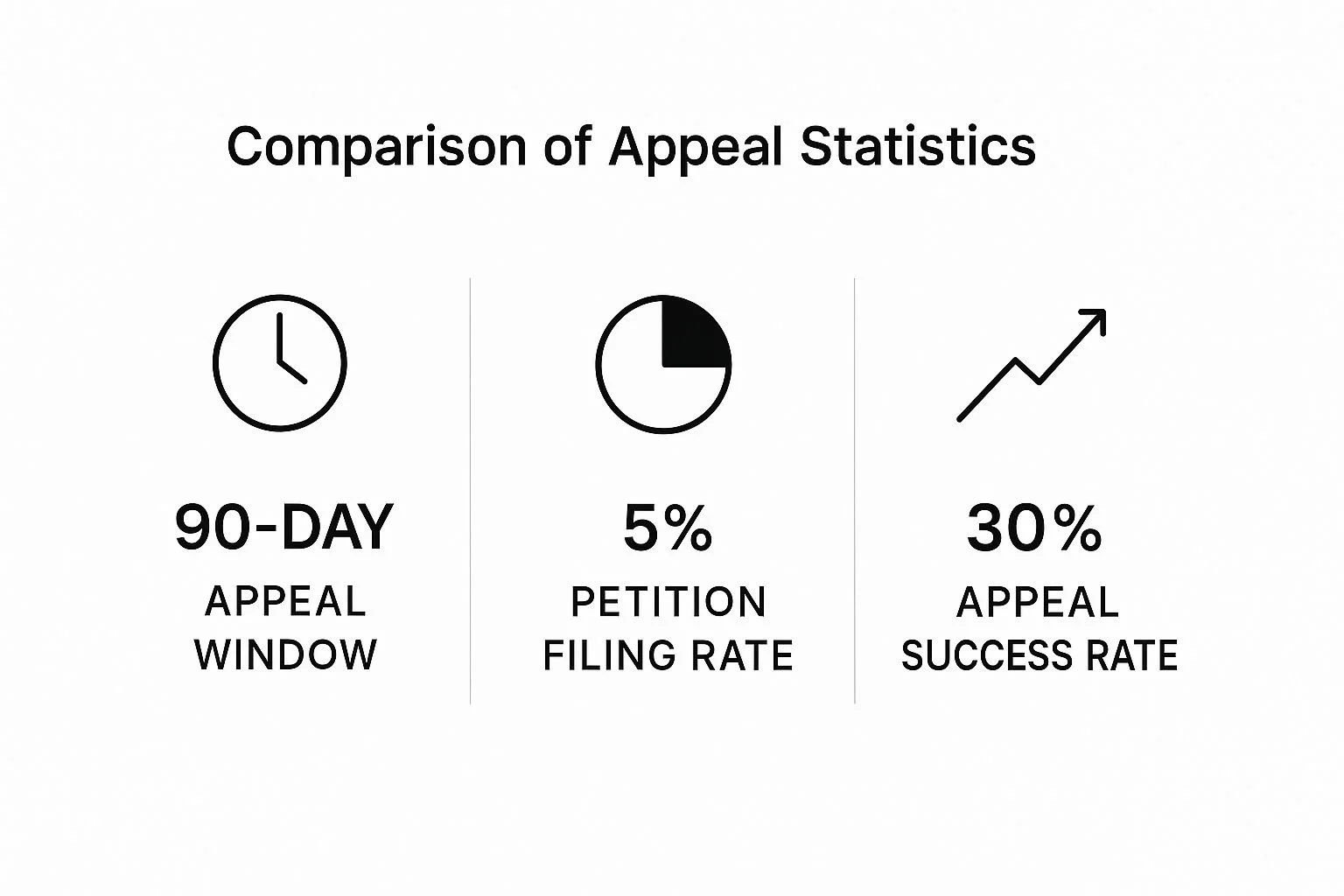

This image really drives home just how crucial this window is.

The numbers tell a powerful story: very few taxpayers challenge a notice, but those who do have a remarkably high success rate. It's a clear signal that it pays to contest an incorrect IRS notice of deficiency.

Choosing to fight doesn't mean you're signing up for a long, drawn-out court battle. Quite the opposite. The vast majority of cases petitioned to Tax Court are settled long before they ever see a judge. Filing a petition simply opens the door for a more structured, productive negotiation with the IRS.

Comparing Your Response Options to a Notice of Deficiency

To make the decision clearer, let's lay out the options side-by-side. This table breaks down what happens with each choice and what you should be thinking about strategically.

| Your Action | Likely Outcome | Key Strategic Consideration |

|---|---|---|

| Agree & Pay | The proposed tax is assessed, and you pay it. Interest stops accruing sooner. | You lose all rights to appeal or go to Tax Court. Best only if the IRS is 100% correct. |

| Ignore the Notice | The proposed tax is automatically assessed after 90 days. The IRS begins aggressive collections. | You forfeit your right to challenge the debt before paying. This is the worst possible option. |

| File a Tax Court Petition | IRS collections are paused. Your case moves to IRS Appeals for settlement negotiation. | This preserves all your rights and gives you the best chance to reduce or eliminate the proposed tax. |

This comparison highlights that your actions within the first 90 days have permanent consequences.

Even if you challenge the notice and still end up owing more than you can handle, other options might open up. For instance, you could explore programs designed to resolve overwhelming tax debt.

Ultimately, filing a petition is the only way to truly contest the IRS's position and work toward a fair outcome.

How to Prepare and File a Tax Court Petition

If you've decided to stand your ground and fight the IRS’s proposed changes, your next stop is the U.S. Tax Court. This might sound intimidating, but it’s really just a structured process that puts you back in the driver's seat. Filing a formal petition is the only way to protect your right to dispute the IRS notice of deficiency before having to pay a dime.

Think of it this way: filing the petition transforms the situation from a one-sided demand into a two-sided legal dispute. Let's walk through the essential steps to get your petition prepared and filed correctly, so you meet that critical deadline and start your challenge on solid footing.

Gathering the Right Information and Forms

Before you can file, you need to get your ducks in a row. The first step is getting your hands on the official Tax Court petition form. For many straightforward situations, the U.S. Tax Court provides Form 2, Petition (Small Tax Case). For more complex matters, there's a general petition kit available.

You can download these forms directly from the U.S. Tax Court's website. You’ll also need your Notice of Deficiency close by—it contains crucial information you must include in your petition, such as:

The exact date the notice was mailed.

The specific tax years in question.

The precise deficiency amount and any penalties the IRS has proposed.

Your petition is your formal, written objection. You have to be specific about which of the IRS's adjustments you disagree with and explain why. A vague statement like "I disagree with the IRS" won't cut it. You need to address each contested point from the notice directly.

Making the Small Tax Case (S-Case) Election

For many taxpayers, the Tax Court offers a simplified, less formal, and less expensive path known as a Small Tax Case, or "S-Case." This option is a real game-changer if you’re an individual or small business facing a more modest dispute.

You can choose the S-Case procedure if the total disputed tax and penalties for any single tax year is $50,000 or less. This simplified process has some major advantages:

Relaxed Rules of Evidence: The strict, formal rules of evidence you see in TV courtrooms don't apply, making it much easier to present your side of the story.

Faster and Less Formal: The proceedings are generally quicker and feel more like a structured meeting than a formal trial.

Lower Costs: The reduced complexity often translates to lower legal fees if you decide to hire a professional.

Choosing the S-Case is a strategic decision. While it offers simplicity, it comes with one significant trade-off: the final decision of the Tax Court in an S-Case is binding and cannot be appealed by either you or the IRS.

The Critical Importance of Professional Help

While you are legally allowed to represent yourself in Tax Court—what’s known as proceeding pro se—that path is riddled with potential pitfalls. The Tax Court has its own specific rules of procedure and practice, and one simple mistake could jeopardize your entire case.

Hiring a qualified tax attorney isn't just about having someone show up for you; it's about bringing in expertise to build the strongest possible argument.

An experienced attorney knows how to frame your disagreements in proper legal terms, negotiate effectively with the IRS Appeals Office (where most of these cases actually get settled), and navigate the procedural hurdles that trip up even the most prepared taxpayer.

You wouldn't perform surgery on yourself, right? Well, navigating a legal fight with the IRS is a job best left to a professional. The investment in expert guidance often pays for itself by securing a much better outcome than you could likely achieve on your own.

What Really Happens After You File Your Petition

So you’ve filed your petition with the U.S. Tax Court. This isn't the dramatic, gavel-banging courtroom scene from a legal drama. Not even close. Filing that petition is more like finding a key to a new room—a room where real, productive negotiations finally begin. The whole game changes the moment your case is officially on the court's docket.

Here’s the secret most taxpayers never learn: the vast majority of cases that are petitioned to the Tax Court never actually go to trial. It's not about arguing in front of a judge. In fact, statistics consistently show that over 90% of these cases are settled beforehand. Filing your petition is simply the most powerful way to get a better seat at the negotiating table.

Your Case Moves to IRS Appeals

Once your petition is filed and docketed, your case file gets a crucial transfer. It moves out of the hands of the auditor or collections officer and lands on the desk of someone at the IRS Independent Office of Appeals. This is a huge deal.

The Appeals Office is a completely different animal from the audit division. Its entire purpose is to resolve tax disputes without forcing everyone—you and the government—through the expensive and time-consuming litigation process.

An Appeals Officer thinks differently than a revenue agent. The agent's job is just to apply the law as they see it. An Appeals Officer, on the other hand, has a broader mandate. They are tasked with evaluating the "hazards of litigation."

In plain English, they look at your case from a practical standpoint. They weigh the strengths and weaknesses of both sides and ask, "What are the chances the IRS could actually lose this if it went to court?" This gives them the authority to compromise on the issues, which is something an auditor simply can't do.

Key Insight: Landing your case in Appeals is the single best shot you have at a favorable settlement. You're no longer dealing with the person who created the problem but with a neutral third party whose job is to find a reasonable path to close the case.

Preparing for Your Appeals Conference

The main event in this process is the Appeals conference. This is usually a pretty informal meeting, often just a phone call between your representative (ideally, a tax attorney) and the Appeals Officer. This is your moment to present your side of the story.

You have to be prepared. This is your chance to lay out, with clear evidence, exactly why the adjustments on your IRS notice of deficiency are wrong. You'll want to have your ducks in a row:

Specific Evidence: Bring everything. Receipts, bank statements, legal agreements, mileage logs—any piece of paper that backs up what you're saying.

Legal Arguments: If your dispute hinges on a fine point of the tax code, you should be ready to point to the laws or court cases that support your position.

A Settlement Offer: It's almost always a good idea to walk into that conference with a specific, well-reasoned settlement proposal ready to go.

The Art of the Compromise

The whole point of the Appeals process is to find a resolution both sides can live with. That almost always means compromise.

Let's say the IRS auditor disallowed 100% of your business vehicle expenses because your records weren't perfect. An Appeals Officer has the flexibility to look at your partial records and say, "Okay, this isn't perfect, but it's credible." They might agree to allow 50% or even 75% of the expenses just to settle the case and avoid the risk of trial.

This whole stage is about realistic negotiation. When you understand that filing a Tax Court petition is the starting pistol for this powerful settlement process—and not a fight to the death in court—you can build a strategy that gives you a much better chance of cutting down, or even wiping out, the tax the IRS says you owe.

Common Questions About the Notice of Deficiency

When you’re holding a Notice of Deficiency, your mind probably starts racing with questions. It’s not just the big picture that’s overwhelming; it’s the practical, nitty-gritty details that can really keep you up at night. Let's tackle some of the most common concerns head-on.

Getting straight answers is the first step toward taking back control. It helps you move forward with a clear head, making decisions based on facts, not fear.

Can I Get an Extension on the 90-Day Deadline?

I get this question all the time, and the answer is an unequivocal no. The 90-day deadline (or 150 days if you're outside the U.S.) is not just an IRS rule—it’s written into federal law.

It is absolute and non-negotiable. No one, not the IRS and not even the U.S. Tax Court, has the authority to grant you an extension for any reason whatsoever. If you miss that date, you lose your right to challenge the tax in Tax Court before paying it. Period.

What Is the Difference Between This and a CP2000?

It’s easy to get IRS notices mixed up, but these two are worlds apart in terms of severity. A CP2000 is essentially a preliminary proposal from the IRS. It’s usually automated, triggered when their computers spot a mismatch between the income you reported and the figures they received from employers or financial institutions.

The IRS Notice of Deficiency, however, is the IRS’s final legal determination. It’s the official letter that gives you the right to sue them in Tax Court. It’s far more serious and starts that unforgiving 90-day clock.

Key Difference: Think of a CP2000 as the IRS suggesting a change. A Notice of Deficiency is the IRS formally declaring its position and daring you to challenge it in court.

Do I Absolutely Need a Lawyer to File a Petition?

Technically, no. You are legally permitted to represent yourself in Tax Court, a process known as proceeding pro se. But I can tell you from experience, it is almost always a mistake.

The Tax Court has its own complex web of procedural rules, deadlines, and unwritten expectations. A seasoned tax attorney knows how to navigate this system, build a compelling legal argument, and negotiate effectively with IRS counsel. For nearly everyone, the complexity of tax law and court procedure makes professional representation essential.

What If I Agree with Some Changes but Not Others?

This is a very common scenario, and you should absolutely still file a petition. Your petition to the Tax Court isn't an all-or-nothing gamble. It’s a precise legal document where you pinpoint exactly which of the IRS’s proposed adjustments you dispute and explain why.

This allows you to concede the items you know are correct while fighting back against the ones that are wrong. The case then becomes focused only on those specific points of contention, which is exactly what you want.

Navigating an IRS notice of deficiency requires precision and expertise. Attorney Stephen A Weisberg works directly with taxpayers to challenge IRS positions and achieve the best possible outcomes. Don't face the IRS alone; start with a FREE Tax Debt Analysis to understand your options and build a winning strategy.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034