IRS Offer In Compromise Calculator: Your Complete Guide

Getting Real About Your Financial Situation

Before you even think about opening an IRS offer in compromise calculator, let's have a frank chat. So many people jump into this tool filled with hope, plugging in numbers that reflect what they wish they could pay, not the hard truth of their financial situation.

This is the number one reason offers get shot down before they even get a serious look. The calculator is just a machine; it runs on cold, hard data, not optimism. To get a result that's actually useful, you have to start with a brutally honest look at your own finances.

The point isn't just to make a list of your stuff and your bills. It's about seeing your situation through the same lens an IRS reviewer would use—which is critical and completely unsentimental.

Forget what Zillow says your home is worth if it needs a new roof. Don't value your 15-year-old car based on sentimental value. The IRS is focused on one thing: your "reasonable collection potential" (RCP).

This is a formula-driven calculation of what they could realistically get from you if they used their full collection powers. Your offer has to be at least that amount, or it's a non-starter.

Uncovering Your True Financial Picture

First, you need to separate what you feel you can afford from what the IRS formulas determine you can afford. The gap between these two can be massive. A classic mistake is underestimating your disposable income.

You might look at your budget and see only $100 left over each month. But the IRS applies strict national and local standards for living expenses. Any money you spend above those official amounts is often seen as disposable income that could go toward your tax debt.

It's the same story with your assets. Everything you own has a "quick sale value" (QSV). This is what you could get for an asset if you had to sell it fast, typically calculated as 80% of its fair market value. Imagine you had to sell your car or your stock portfolio within 30-60 days to pay off a debt.

What would you actually get for it? That’s the number the IRS will use.

Why a Realistic Assessment Matters

Putting in a half-hearted effort at this stage all but guarantees a rejection letter. The Offer in Compromise program isn't a simple "get out of debt free" card; the requirements are surprisingly tough. In 2023, the acceptance rate was around 40%, which means six out of every ten people who applied were turned away.

And that doesn't even count the many who were weeded out by pre-qualifier tools before they could even submit an application.

You can explore the reasons why many OIC applications fail to understand just how high the bar is set. This just goes to show how important it is to base your calculations on facts you can prove, not just hopeful guesses.

Getting this initial homework right is what separates a successful offer from a wasted application fee.

Assembling Your Financial Documentation Arsenal

The IRS offer in compromise calculator is a fantastic tool, but it's only as reliable as the numbers you put into it. Think of it less like a magic eight ball and more like a precise GPS navigator—it needs accurate coordinates to give you a useful route.

This isn't the time for guesstimates or "I think my car is worth about..." figures. The IRS operates on hard facts, so providing them with precise data is the first step toward a realistic outcome.

Before a tax pro even touches a calculator, they begin by gathering a specific pile of paperwork. This isn't just about being thorough; it's about building a credible financial story from the ground up. Simply grabbing your most recent bank statement and pay stub won’t be enough.

For instance, the IRS will want to see your income history for at least the last three to six months to spot any trends, which is especially important if your income fluctuates, like from freelance gigs or sales commissions.

Key Documents for Calculator Accuracy

To get a truly accurate picture, you need to compile a file that proves every detail of your financial life. This meticulous preparation forms the bedrock of your entire offer.

Before you start plugging numbers into the calculator, it’s a good idea to gather all the necessary documents. This checklist breaks down what you'll need, why you need it, and common mistakes to avoid.

| Document Type | Time Period Required | Purpose | Common Mistakes |

|---|---|---|---|

| Income Verification | Last 3–6 months | To establish your average monthly income. Includes pay stubs, 1099s, or P&L statements. | Forgetting to average out irregular income, leading to an inaccurate and inflated monthly figure. |

| Bank Statements | Last 3–6 months | To verify income, expenses, and look for unusual transfers or hidden cash assets. | Overlooking smaller accounts or failing to explain large, one-time deposits (like a gift from a relative). |

| Asset Valuation | Current | To determine the Quick Sale Value (QSV) of assets like homes, cars, and investments. | Using the trade-in value for a car instead of the higher private party value. Using an outdated property assessment. |

| Expense Records | Recent bills (last 1–3 months) | To prove your monthly living expenses. Includes mortgage/rent, utilities, insurance, etc. | Claiming expenses that exceed the IRS's national and local standards without strong justification and proof. |

Having this information organized and ready will make using the calculator much faster and more accurate. It also prepares you for the official Form 433-A (OIC) you'll eventually submit.

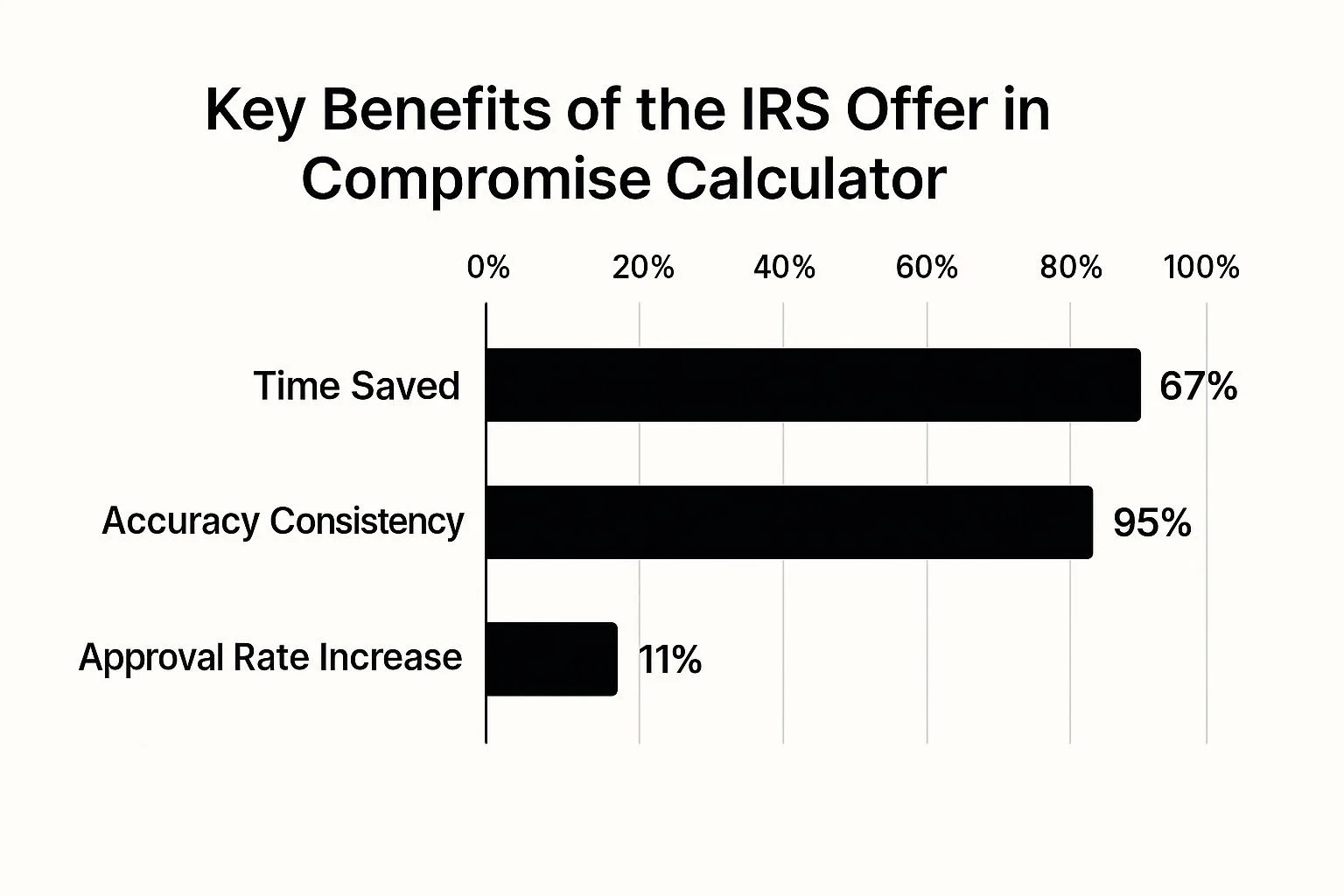

This infographic shows just how beneficial using a precise tool like the calculator can be once you have your data assembled correctly.

As the data shows, while a higher approval rate is the ultimate goal, the immediate benefits are significant gains in accuracy and time saved. This entire process is fundamentally about negotiation.

If you want to dive deeper into the strategy behind it, you might find our guide on how to negotiate IRS debt helpful. Being organized and credible from the very beginning is your strongest move, paving the way for a realistic and potentially successful offer.

Mastering The Calculator Like A Tax Professional

Alright, let's get into the nitty-gritty of the IRS offer in compromise calculator. This is where your preparation pays off. Forget just plugging in numbers and hoping for the best.

We’re going to be deliberate, understanding what each field really asks for and how your answers shape your entire offer. This isn't just about data entry; it's about telling your financial story in a way the IRS will actually consider.

Inputting Income With Precision

The income section is often the first place people get tripped up, especially if you don't have a simple, steady paycheck. The calculator wants a monthly average, so you have to be methodical if your income bounces around.

For example, if you're a freelance graphic designer who pulled in $7,000 one month but only $2,500 the next, you can't just pick the lower number. You'll need to average your income over the last three to six months to arrive at a figure you can defend.

Think about these real-life situations:

Seasonal Work: A roofer who makes most of their money from May to October needs to use a full 12-month period to find a realistic monthly average. Using only the busy months would give the IRS a misleading picture of their ability to pay.

Annual Bonuses: That $12,000 bonus you got last year isn't a one-off windfall in the eyes of the IRS. You need to prorate it over 12 months, which means adding $1,000 to your monthly income calculation.

Irregular Gigs: If you do occasional consulting work, add up what you've earned over the past six months and divide by six. That's the number you'll enter into the calculator.

Valuing Assets The IRS Way

The asset valuation part of the calculator is a make-or-break moment for many offers. When you list your home, cars, or retirement funds, you need to understand the difference between fair market value (FMV) and quick sale value (QSV).

The IRS is most interested in the QSV, which is what you could realistically get for an asset if you had to sell it quickly. This is often calculated as 80% of the FMV.

It might feel more "honest" to list your car at its highest possible private-party value, but the IRS is likely going to adjust it down to its QSV anyway.

On the other hand, if you lowball the value too much, it immediately erodes your credibility. The goal is to be realistic and have a basis for your number, like a Kelley Blue Book trade-in value.

Justifying Your Expenses

Finally, let's cover your expenses. The IRS allows for necessary living costs, but they compare your numbers to national and local standards. If your rent or car payment is way above the standard for your zip code, you need a very good reason and the paperwork to back it up.

For instance, claiming unusually high transportation costs makes sense if you have a long commute, which can be easily verified by your pay stubs listing your employer's address.

Your numbers need to tell a consistent story. If you claim expenses so high that you have zero disposable income, but your bank statements show weekly dinners out and streaming subscriptions, an IRS reviewer will catch that inconsistency in a heartbeat.

To see how these pieces come together inside the tool, you can learn more about the IRS offer of compromise calculator in our detailed article.

Decoding Your Calculator Results

Seeing that final number pop up on the IRS offer in compromise calculator can feel like the finish line, but it’s really where the strategy begins. That figure isn't just a random number; it's what the IRS calls your Reasonable Collection Potential (RCP).

Think of it as the absolute minimum amount the government thinks it can squeeze out of you, based on a rigid formula that looks at your assets and future income. This is critical to understand because it’s why the result might be way different from what you were hoping for.

The calculator's output is your moment of truth. If the number it gives you is pretty close to what you already owe, an Offer in Compromise is likely not the right move.

On the other hand, if the number seems almost too good to be true—like offering $500 on a $90,000 tax bill—it could signal that you’ve entered something incorrectly. An unrealistic offer can damage your credibility with the IRS right from the start.

From Calculation to Strategic Offer

So, you have your number. Now you need to decide how you’ll pay it, and this choice has major financial consequences. The calculator generally lays out two paths:

Lump Sum Cash Offer: With this option, you agree to pay the full offer amount within five months of its acceptance, in five or fewer payments. This is the fast track. The calculation is your total asset value plus your monthly disposable income multiplied by 12.

Periodic Payment Offer: This path gives you more time, letting you spread payments over as long as 24 months. Because you're paying over a longer period, the calculation is more involved: your total asset value plus your monthly disposable income multiplied by 24. This means a higher total offer, but it might be more manageable.

Deciding between these two isn't just about what seems easier on paper. The IRS tends to prefer the lump sum offer because it’s quicker and less risky for them. But before you commit, you have to be brutally honest with yourself about whether you can actually get your hands on that money in time.

Is Your Offer Realistic?

The offer you put forward must be believable and possible for you to fulfill. The OIC program is tough to get into. For example, during the 2024 fiscal year, the IRS only accepted 7,199 of the 33,591 offers it received. That's a success rate of just over 21%.

To get a better sense of how competitive this is, you can find out more about recent OIC acceptance statistics. This data makes it clear that only the most carefully prepared and realistic offers get approved.

Put your final number to the test: imagine an IRS agent going over every single figure you submitted. If you can't confidently defend it, it's not ready to send.

Avoiding The Fatal Calculator Mistakes

Even the most organized taxpayer can make a seemingly small mistake on the IRS Offer in Compromise calculator that has massive consequences.

These aren't just simple typos; they're strategic errors that can get your entire application tossed before it even gets a serious look.

I’ve seen it happen too many times: a minor miscalculation creates a ripple effect of doubt that completely shatters your credibility with the IRS reviewer.

Why Small Numbers Cause Big Problems

One of the most common traps is getting your income calculation wrong, especially if it fluctuates.

Imagine you're a freelance designer who had a great month and earned $6,000, but this month was slower, bringing in only $2,000. It’s tempting to plug that lower number into the calculator, but the IRS will average your income over several months.

Using the wrong figure doesn't just skew your offer amount; it makes you look like you’re hiding income, which is a huge red flag.

Another fatal error is underestimating the value of your assets. Many people list their car at its low trade-in value, thinking they're being clever.

But the moment the IRS agent pulls a Kelley Blue Book report and finds a private party value that's $3,000 higher, they’ll not only adjust your offer but also start questioning every other number you provided.

Credibility is everything in this process. Once you lose it, it's almost impossible to regain. The objective isn't to outsmart the system but to present a transparent, accurate financial picture that can hold up under intense review.

The Mindset That Gets Offers Rejected

Beyond the math, there's a psychological pitfall that many people stumble into: being too aggressive with their expenses. Claiming a $700 monthly food budget for one person or piling on unusually high "other" expenses without rock-solid documentation will almost certainly backfire.

The IRS operates using strict national and local standards for what it considers reasonable living expenses. Any claims that deviate wildly from these benchmarks are a direct invitation for a much deeper, more stressful examination of your finances.

It’s important to understand that the IRS scrutinizes different filers with varying levels of intensity, and businesses often face the toughest path. To give you a clearer picture, let's compare the success rates for individuals versus businesses.

| Taxpayer Type | Acceptance Rate | Common Rejection Reasons | Success Factors |

|---|---|---|---|

| Individual | Approx. 44% (2010-2017) | Income miscalculation, undervalued assets, excessive expense claims. | Accurate and verifiable financial data, reasonable expense claims that align with national standards, full compliance with tax filings. |

| Business | Approx. 24% (2010-2017) | Failure to stay current on payroll taxes, unviable business model, incomplete records. | Demonstrating the business is profitable moving forward, maintaining current tax compliance (especially payroll), having meticulous financial records. |

As the table shows, businesses have a significantly lower acceptance rate, often because ongoing tax compliance (like payroll deposits) is a major sticking point for the IRS. You can discover more about these OIC program statistics to see just how critical accuracy is.

If the offer amount from the calculator seems too good to be true, it probably is. On the other hand, if it's too high for you to manage, it might be time to explore other avenues. For many, a different strategy like an installment agreement could be a more practical solution.

You can learn more by checking out our guide on the IRS installment agreement calculator. The key is to be brutally honest with yourself and with the numbers you present.

Strategic Decisions After Your Calculation

So, you've plugged everything into the IRS offer in compromise calculator and have a number staring back at you. Think of this number not as the finish line, but as the starting block.

This figure is what the IRS calls your Reasonable Collection Potential (RCP), and it's the basis for some big decisions you're about to make.

Now's the time to put on your most skeptical hat—imagine you're the IRS agent reviewing your case—and decide if your offer has a real chance of success.

Is Your Calculated Offer Viable?

Let's put that number to the test with a real-world scenario. Imagine you owe $100,000 in back taxes, and the calculator suggests an offer of $15,000.

Before you celebrate, you need to ask yourself a tough question: "Can I prove, without a shadow of a doubt, that this is the absolute most the IRS could ever hope to collect from me?"

This isn't just about what you think is fair; it's about what you can document. An IRS agent will scrutinize every detail. You'll need solid proof for every asset value and every monthly expense you've claimed.

This means having bank statements, professional property appraisals, and meticulous records of your living costs ready to go. You must be prepared to defend every single dollar.

On the other hand, what if the calculator says your offer should be $85,000? This is a clear signal that an Offer in Compromise probably isn't the right move.

The IRS's own formula suggests you can pay back most of what you owe. Trying to push an OIC in this situation would likely be a waste of your time, energy, and the application fee. It's a strong sign to start looking at other options.

Exploring Your Alternatives

Seeing a high number from the calculator isn't a dead end. It’s simply guiding you toward a different solution that might be a much better fit for your financial reality. The IRS has other programs designed to help people in your exact situation:

Installment Agreements: This is a straightforward plan to pay your tax debt over time with monthly payments you can actually afford.

Currently Not Collectible (CNC) Status: If your financial situation is so tight that you can't even cover basic living expenses, the IRS might agree to temporarily stop collection efforts until your circumstances improve.

Knowing these alternatives exist is half the battle. The calculator's main purpose is to give you the clarity to make an informed choice—whether that's pursuing a formal OIC or moving toward another form of tax relief that's more likely to be approved.

Your Action Plan Moving Forward

Getting a positive result from the IRS offer in compromise calculator feels like a huge win, but it’s really just the starting whistle. Now the real work begins.

This is where you move from theory to action, putting together a solid plan to resolve your tax debt for good. This next phase isn't always quick or easy—it demands patience, persistence, and a realistic outlook on what's ahead.

Let's build your game plan, starting with a practical timeline and figuring out your next move.

Setting Realistic Timelines

The Offer in Compromise (OIC) process is definitely a marathon, not a sprint. Once you’ve submitted the official forms—Form 656 and Form 433-A (OIC)—you need to settle in for a wait. The IRS generally takes six to nine months to review an OIC application, and if your financial picture is complicated, it could take even longer.

During this waiting period, it's absolutely critical to stay on top of your current tax duties. This means filing all your returns on time and making any required estimated tax payments.

If you miss a deadline, the IRS can automatically reject your offer, and all that hard work goes down the drain. My advice? Stay compliant and be patient. Hearing nothing for months is often just a normal part of the process.

Knowing When to Call for Backup

One of the biggest decisions you'll make is whether to handle this yourself or bring in a professional. You might be able to go it alone if:

Your finances are simple. For example, you're a W-2 employee with a regular paycheck and not many assets.

The calculator gave you a clear, affordable offer amount that makes sense for your budget.

You're good with details, organized, and don't mind wading through government paperwork.

However, it's smart to think about getting expert help if you feel like you're in over your head. Big red flags include owning a business, having significant assets like real estate or investments, or getting a result from the calculator that seems way too high or just plain confusing. A seasoned tax professional can often spot weak points in an application you might overlook and can negotiate with the IRS from a position of experience.

The emotional weight of dealing with the IRS is real. It's easy to get discouraged, especially during the long wait or if your offer gets rejected. But remember, a rejection isn't the end of the road.

It usually comes with an explanation that you can use to build a stronger offer next time. People who successfully get an OIC approved almost always share one common trait: persistence.

If you've used the calculator and are now feeling stuck or unsure about how to proceed, let's talk. I offer a free, no-obligation Tax Debt Analysis to go over your specific situation and figure out the best way forward. Don't let confusion paralyze you to get some clarity and create a strategy for success.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034