Understanding IRS Levy and Garnishment

When you’re facing a tax issue, you’ll often hear the terms “levy” and “garnishment” thrown around, sometimes even interchangeably.

But make no mistake, an IRS levy and garnishment are two very different beasts. Knowing which one you’re dealing with is the first step toward regaining control.

Think of it this way: a levy is like a lightning strike. It’s a one-time event where the IRS seizes whatever assets it can, right then and there.

A wage garnishment, on the other hand, is more like a slow, constant drain. It’s an ongoing order to your employer to siphon off a portion of your paycheck, week after week, month after month.

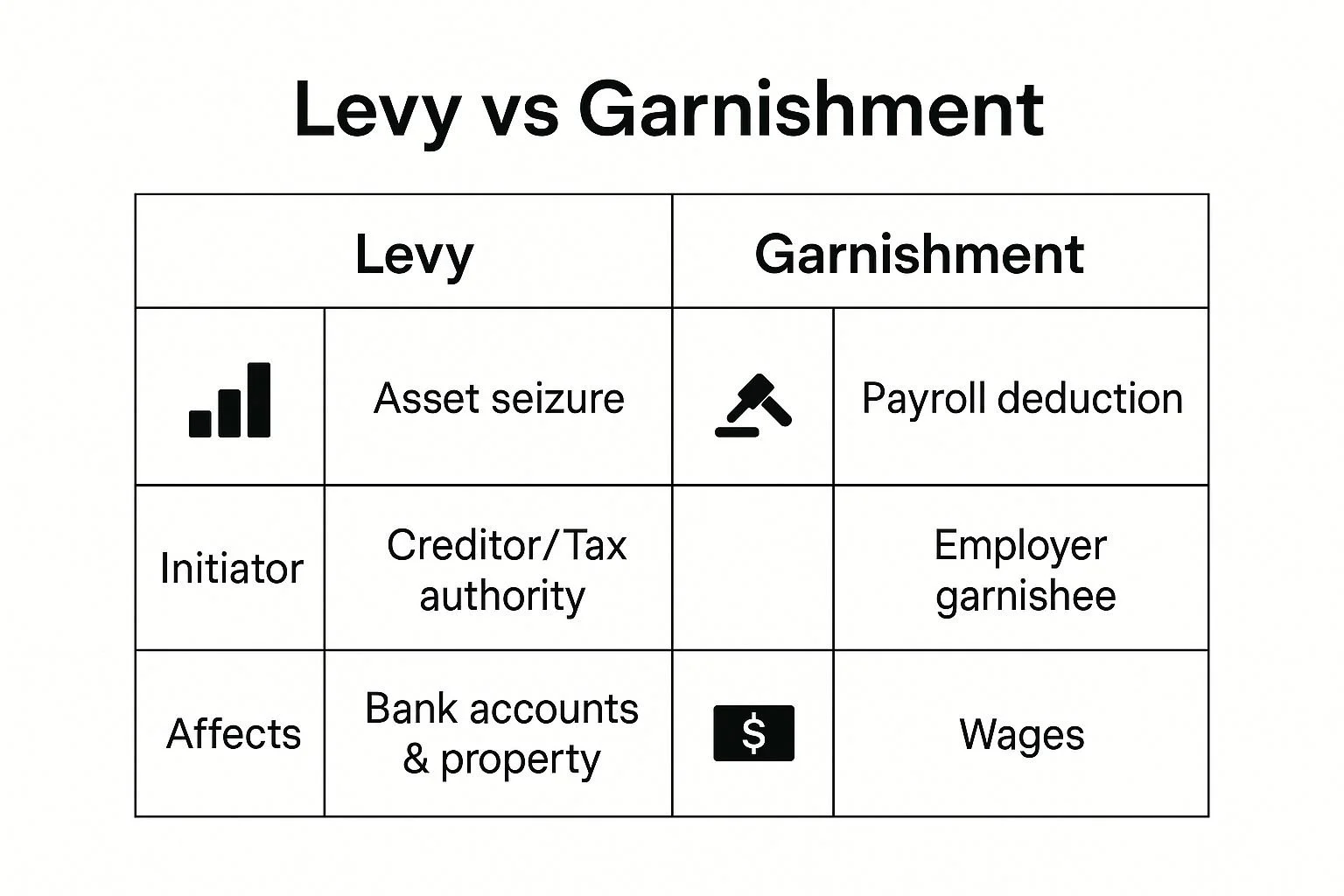

Levy vs. Garnishment: What’s the Real Difference?

The distinction really boils down to timing and the target of the collection action. When the IRS decides to levy your assets, they’re playing a short game.

They send a notice to your bank, and poof—the money in your account is frozen and sent to the government. It’s a swift, aggressive move designed to get their hands on a lump sum immediately.

A wage garnishment is the IRS playing the long game. Instead of hitting your bank account, they go straight to the source of your income: your employer.

They issue a legal order that forces your company to withhold a specific amount from your earnings before you even see your paycheck.

This creates a steady stream of payments that continues until the debt is paid off or you negotiate a different solution.

A Closer Look at the Mechanics

A levy is a formal, legal seizure of your property to cover a tax debt. While bank accounts are the most frequent target, the IRS isn’t shy about going after other things you own.

They can levy assets like:

Your house or other real estate

Cars, boats, and other vehicles

Retirement funds like a 401(k) or IRA

Social Security benefits (though there are limits)

A wage garnishment is much more specific. It exclusively targets the money you earn from your job. The IRS essentially deputizes your employer, legally requiring them to act as a collection agent and send a portion of your wages directly to the government.

Here's a simple way to keep them straight: A levy seizes what you already own. A garnishment intercepts what you’re about to earn. Both are incredibly serious, but they hit your finances from different angles.

To make this even clearer, let's break down the key differences in a quick comparison.

Levy vs. Garnishment at a Glance

| Feature | IRS Levy | Wage Garnishment |

|---|---|---|

| Nature of Action | A one-time seizure of assets. | An ongoing, continuous deduction from paychecks. |

| What's Targeted? | Bank accounts, property, vehicles, retirement funds. | Your wages, salary, and commissions. |

| Who is Involved? | You, the IRS, and the asset holder (e.g., your bank). | You, the IRS, and your employer. |

| Timing | Happens on a specific day. | Occurs every pay period until the debt is paid. |

This table neatly sums it up. A levy is a direct hit on your current assets, while a garnishment is a persistent drain on your future income.

As the visual above shows, the core difference lies in whether the IRS is taking from a creditor (like a bank) or directly from your employer. One impacts what you have, and the other impacts what you earn.

Understanding which path the IRS is taking is absolutely critical to crafting the right strategy to fight back and resolve your tax debt for good.

How an IRS Bank Levy Seizes Your Assets

Of all the collection actions the IRS can take, a bank levy is one of the most jarring. It feels sudden and incredibly disruptive.

Unlike a wage garnishment that takes a piece of your future paychecks, a levy is a one-time event that freezes your bank account and seizes the funds you rely on for everything.

While the final freeze might feel like it comes out of the blue, it’s actually the end of a long notification process. The IRS is legally required to send a series of notices about your tax debt.

The most important one to watch for is the Final Notice of Intent to Levy and Notice of Your Right to a Hearing, which usually arrives as Letter 1058 or LT11. This isn't a suggestion—it's your last warning shot, giving the IRS legal authority to seize your assets in 30 days.

The 21-Day Freeze and What It Means

The moment the IRS sends the levy notice to your bank, the institution is legally required to freeze your account. But here's a key detail: the money isn't immediately sent to the IRS. Instead, the bank must hold the funds for a mandatory 21-day period.

Think of it as putting your financial life on pause. During these three weeks, you are completely locked out of the levied funds. Any checks you've written will bounce. Automatic bill payments will fail. Trying to pull cash from an ATM will get you nowhere.

This 21-day hold is a critical—and often final—window of opportunity. It gives you a brief period to contact the IRS and try to negotiate a resolution before the bank is required to send your money to the government to pay off your tax liability.

Once those 21 days are up, if you haven't secured a release, your bank has no choice. It transfers the money directly to the IRS, up to the full amount you owe. Now the levy is complete, and you're left to pick up the pieces.

To get a clear picture of the damage and your overall financial situation, you might need to use tools for analyzing bank statements to sort through the transactions.

Beyond the Bank Account: Other Targeted Assets

Bank accounts are the most frequent target for an IRS levy, but they are certainly not the only asset on the table.

The IRS has startlingly broad authority to go after other types of property to settle a tax debt. Knowing what else is at risk is crucial to protecting your financial stability.

Other assets the IRS can come after include:

Retirement Accounts: Yes, the funds in your 401(k) or IRA can be levied. It’s a more complex process for the IRS, so it’s less common, but for large tax debts, it's a very real possibility.

Property and Real Estate: The IRS can seize and sell physical property. This includes your primary home, vacation properties, cars, boats, and other valuables.

Social Security Benefits: While some federal payments have protections, the IRS can take up to 15% of your Social Security benefits through its Federal Payment Levy Program (FPLP).

This broad power really highlights how serious an IRS notice is. What begins as a letter in the mail can escalate into the government seizing assets you've worked your entire life to build. The only surefire strategy is to take action before the levy ever hits.

How IRS Wage Garnishment Affects Your Paycheck

If an IRS levy is a sudden lightning strike, a wage garnishment is a slow, relentless drought.

While both a levy and garnishment are tools the IRS uses to collect tax debt, the ongoing nature of a garnishment creates a completely different kind of financial nightmare. It’s a long-term drain that can be absolutely devastating.

Unlike a levy, which grabs what you already have in the bank, a wage garnishment intercepts your money before you even see it. The IRS sends a legal order, Form 668-W(c)(DO), straight to your employer.

This isn't a friendly request—it’s a command that legally forces your company to withhold a huge chunk of your salary and send it directly to the government. This happens every single payday until the debt is gone or you work out another deal.

Decoding the Garnishment Calculation

The first question everyone asks is, "How much are they going to take?" It's not a random number. The IRS uses a specific formula to figure out how much of your pay they can legally snatch.

Your employer is required to use Publication 1494 to calculate the portion of your wages that’s exempt. This calculation boils down to two things:

Your Tax Filing Status: Are you single, married filing jointly, or head of household?

Number of Dependents: How many dependents do you claim on your tax return?

The IRS lets you keep an amount that roughly equals the standard deduction for your filing status. Everything else—what they consider your "disposable income"—is fair game.

The most important thing to understand is that the IRS calculates what you're allowed to keep, not what they take. Any income above that legally protected minimum goes straight to them, and it can be a shockingly high percentage of your paycheck.

A Real-World Garnishment Example

Let's see what this looks like in the real world. Imagine you’re a single person with no dependents, earning a gross salary of $2,000 every two weeks.

Based on the IRS exemption tables, you might be allowed to keep only about $519 of that paycheck. That means the IRS would garnish the remaining $1,481 from each check. Your monthly income just plummeted, making it nearly impossible to cover rent, groceries, and other basic bills.

And this isn't some rare, extreme scenario. As of 2019, wage garnishment for various debts hit over 1% of all U.S. workers.

On average, those employees lost 11% of their gross pay for about five months straight, showing just how much financial hardship this causes.

You can dig into the numbers and see the economic impact of wage garnishment trends for yourself.

The Long-Term Financial Squeeze

This constant hit to your income creates a brutal cycle of financial stress. A one-time bank levy is a sharp, painful event, but it's over.

A wage garnishment is a slow bleed that feels like it will never end. It makes it impossible to save money, pay down other debts, or even think about the future.

The pressure can feel completely overwhelming, but you need to know that you have options. The key is to act fast to protect what's left of your income.

If you're in this position, it is critical to learn how to stop an IRS wage garnishment by exploring solutions like an installment agreement or an Offer in Compromise.

Getting proactive and communicating with the IRS is the first step toward releasing the garnishment and getting your financial life back on track.

The Real-World Impact on Your Financial Health

Let's be clear: the financial pain of an IRS levy and garnishment isn't just about the initial money taken. It’s a gut punch that sets off a destructive ripple effect, throwing your daily life into chaos and creating a whole new set of problems that can feel just as overwhelming as the tax debt itself.

Think about a bank levy. It’s a sudden, jarring shock. One day, you have your money. The next, your account is completely frozen, and the consequences hit fast and hard.

The Domino Effect of a Bank Levy

When the IRS levies your bank account, the fallout is immediate. The funds you count on for your most basic needs simply vanish, triggering a chain reaction of financial emergencies.

This sudden freeze can cause:

Bounced Checks: Any checks you've written will suddenly be returned unpaid. This can seriously damage your standing with your landlord, utility companies, or anyone else you do business with.

Hefty Overdraft Fees: Your bank doesn't stop trying to process automatic payments for your mortgage, car loan, or subscriptions. Each attempt on a frozen account can rack up significant non-sufficient funds (NSF) fees.

Inability to Cover Essentials: You’re left without a way to pay for absolute necessities like rent, groceries, gas, or medicine, which creates a huge amount of personal stress.

Beyond the immediate chaos, these events can leave lasting scars on your financial record. Bounced checks and failed payments are red flags that can tank your credit score. For a deeper dive into this, understanding how credit bureaus work is a great place to start.

A levy doesn't just take your money; it temporarily shatters your financial infrastructure. The stress of scrambling to cover basic needs while dealing with mounting bank fees can be completely overwhelming for anyone.

The Chronic Stress of Wage Garnishment

While a levy is a single, sharp blow, a wage garnishment is more like a chronic illness—a long-term drain on your finances and your well-being. Trying to live on a drastically reduced income makes basic budgeting feel like an impossible task.

There’s a constant, grinding pressure that comes from knowing a chunk of every paycheck is gone before you even see it.

This ongoing hit to your take-home pay makes it incredibly difficult to stick to a budget, much less save for an emergency or plan for retirement.

Long-term goals can feel completely out of reach when you're just struggling to get by week to week.

This personal struggle is often magnified by broader economic conditions. Globally, wage garnishment laws and the economic environments around them reflect significant disparities.

For instance, while global real wage growth saw a modest recovery of 1.8% in 2023, this masked a stark division between different economies, with some advanced economies actually seeing a decline in real wages.

When wages are stagnant or falling, recovering from a garnishment becomes an even steeper uphill battle. You can explore more data on global wage trends to see the full picture.

Whether it’s the sudden crisis of a levy or the slow burn of a garnishment, the impact is profound. It’s not just about the money—it’s about losing your sense of security, stability, and control over your own life.

Your Options for Stopping IRS Collections

Getting hit with an IRS levy and garnishment can feel like the walls are closing in. It’s an incredibly stressful situation, and the financial pressure is immense. But I want to be clear: you are not out of options.

In fact, you have several powerful, well-defined paths to stop the collections machine and permanently resolve your tax debt.

The absolute worst thing you can do is nothing. Burying your head in the sand and ignoring IRS notices is what gets you into this mess in the first place—it's a fast track to a bank levy or wage garnishment.

The single most important thing you can do right now is to open a line of communication with them. Just by reaching out, you can often get a temporary hold on collections and start working toward a real solution.

The IRS Installment Agreement

For many people, the most direct route out is an IRS Installment Agreement (IA). It's exactly what it sounds like: a formal payment plan. This lets you chip away at your tax debt with manageable monthly payments, typically stretched out over as long as 72 months.

Once you set up an IA, the IRS backs off. They’ll stop any planned levies and release any active garnishments. It’s a great fit if you have the ability to pay what you owe in full, just not all at once.

Negotiating an Offer in Compromise

But what if you can't possibly pay the full amount, even with a payment plan? That’s what the Offer in Compromise (OIC) is for.

This is a game-changer. An OIC is a formal agreement with the IRS to settle your tax liability for less than the total amount you owe.

The IRS doesn't just hand these out, of course. They'll consider an OIC if paying your full tax debt would cause you genuine economic hardship.

This isn't a casual chat; you'll need to provide a complete and honest picture of your finances to prove you simply don't have the assets or income to cover the bill.

An Offer in Compromise is a lifeline for taxpayers who are truly in a financial bind. When it's accepted, you can put a massive tax debt behind you for pennies on the dollar and get a true financial fresh start.

The OIC process is notoriously tricky, with very specific rules. You have to know what you're doing. Getting this right can be the difference between years of crushing debt and finally achieving financial peace.

Qualifying for Currently Not Collectible Status

There’s another option for those in the most dire financial straits: Currently Not Collectible (CNC) status. If your income is so low that it only covers your basic, necessary living expenses, the IRS can agree to put a temporary stop to all collection attempts. They’ll release wage garnishments and won't pursue levies.

To get placed in CNC status, you have to open your books and prove to the IRS that you have no money left over to pay them. It's important to know this isn't a permanent fix.

The IRS will check back in on your financial situation periodically. If your income goes up, they’ll put you back into collections. Still, for someone with their back against the wall, it provides immediate and vital breathing room.

Comparing Your Top Resolution Options

So, which path makes the most sense for you? Here’s a quick side-by-side look at how these three core strategies stack up against each other.

| Strategy | Who It's For | Key Benefit | Main Consideration |

|---|---|---|---|

| Installment Agreement | People who can afford to pay their full tax debt over time. | Gives you a predictable payment schedule and stops all collection actions. | You’ll still pay the full tax debt, plus any penalties and interest that pile up. |

| Offer in Compromise | People who cannot afford to pay their full debt due to financial hardship. | Lets you settle your tax bill for a fraction of what you owe. | The application is intense and requires deep financial documentation. |

| Currently Not Collectible | People with no extra income after covering basic living expenses. | Immediately halts all collections, providing instant relief. | This is a temporary pause; the IRS will review your ability to pay later. |

No matter which option you pursue, communication is everything.

The IRS operates on procedure and paperwork, and small mistakes can have huge consequences, a point driven home by the lessons from a debt collection law firm's fax fumble.

Approaching this process with care and precision is how you get a levy lifted for good and finally move on from your tax problems.

Garnishments for Student Loans and Other Debts

While the IRS certainly has powerful collection tools, they aren't the only creditor that can take a piece of your paycheck. Other creditors, like credit card companies or hospitals, can also pursue garnishment to get what they're owed.

There's a big difference in how they do it, though. Most private creditors have to go through the courts first—they must sue you, win a judgment, and then get a specific court order to start garnishing your wages.

Federal student loans, however, play by a different set of rules. It’s a crucial distinction that catches many people completely off guard, as the process is far more direct.

The Unique Power of Student Loan Garnishment

Unlike a credit card company, the U.S. Department of Education doesn't need to bother with the court system to garnish your wages.

If you fall into default on a federal student loan, they can kick off an administrative wage garnishment all on their own. This means you get less warning and fewer chances to fight it before the money starts disappearing from your pay.

This special authority is a game-changer. By bypassing the courts entirely, the government makes the garnishment process quicker and much tougher for you to stop. The Department of Education simply sends a notice to your employer, and the withholding begins.

The most important thing to remember here is that federal agencies—like the Department of Education and the IRS—have special collection powers that most private creditors dream of. They can garnish your wages without a court judgment, which really drives home how seriously you need to take these specific kinds of debts.

How Student Loan Collections Differ

The rules for how much can be taken also set student loans apart. While an IRS wage garnishment is based on a somewhat complicated formula involving your filing status and number of dependents, student loan garnishments are much more straightforward. The Department of Education can take up to 15% of your disposable pay, period.

And the scale of this problem is staggering. After the pandemic-related pause on payments ended, projections showed that the number of borrowers in default could quickly climb past ten million. For every one of them, wage garnishment can mean losing up to 15% of their paycheck.

Worse yet, unlike most other debts, federal student loans don't have a statute of limitations. This means the government can keep coming after you for that money indefinitely.

This ongoing threat is why it's so critical to understand all the potential claims against your income. While a tax levy and garnishment is a major headache, other federal debts can be just as damaging to your financial stability. This is especially true when they put your long-term assets at risk.

Your Top Questions About IRS Levies and Garnishments

When you’re facing down the IRS, the questions come fast and furious. It’s a stressful, confusing time, so let’s get some direct, no-nonsense answers to the questions I hear most often from clients.

Can the IRS Really Take All the Money in My Bank Account?

The short answer is a hard yes. A bank levy is one of the most powerful tools the IRS has. They can seize every last dollar in your account, right up to the total amount you owe in taxes.

Unlike a wage garnishment, which has some built-in exemptions, a bank levy is a clean sweep. There are a few exceptions, though. Certain federal benefits, like Supplemental Security Income (SSI), are generally off-limits if they’re direct-deposited and easily identified as such.

How Much Warning Will I Get Before the IRS Takes Action?

The good news is, they can't just raid your account out of the blue. The IRS has to follow a strict notification process, sending you a series of letters that get progressively more serious.

The final, most critical warning is the "Final Notice of Intent to Levy and Notice of Your Right to a Hearing." This letter, usually a Letter 1058 or LT11, gives you 30 days before the levy can hit. That 30-day window is your last, best chance to act and head off the seizure.

Can the IRS Garnish My Paycheck and Levy My Bank Account at the Same Time?

Unfortunately, yes, they can. When the tax debt is significant, it's not uncommon for the IRS to use a multi-pronged attack. They might start taking a piece of your paycheck every week while also hitting your bank account with a one-time levy.

This is exactly why it's so important to get ahead of the problem. An aggressive, two-front collection effort is a sign that the situation has escalated to a critical point.

Is My Social Security Safe from an IRS Levy?

Not completely. While most of your Social Security benefits are protected, the IRS can use a specific tool called the Federal Payment Levy Program (FPLP).

Through this program, they are legally allowed to take up to 15% of your monthly Social Security retirement or disability benefits. The one silver lining is that this does not apply to SSI payments.

Facing an IRS levy and garnishment is a scary prospect, but you absolutely do not have to go through it alone. At the law office of Attorney Stephen A Weisberg, we begin with a FREE Tax Debt Analysis to map out a clear path forward before you ever pay a fee.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034