Negotiating with the IRS A How-To Guide

That official IRS envelope in your mailbox is enough to make anyone’s heart skip a beat. But before you panic, take a breath. Seeing that notice isn't a catastrophe; it’s a prompt to take action.

The absolute worst thing you can do is ignore it. That just gives penalties and interest more time to pile up, inviting more aggressive collection actions like liens or levies down the road. The key is to open the letter, figure out what the IRS wants, and start planning your response.

This isn’t just about being responsible—it’s strategic. The IRS is a colossal agency, dealing with over 266 million tax returns and forms annually.

You might be surprised to learn that taxpayer satisfaction with personal interactions is actually quite high. My experience confirms this: when you engage constructively, you open the door to much better outcomes.

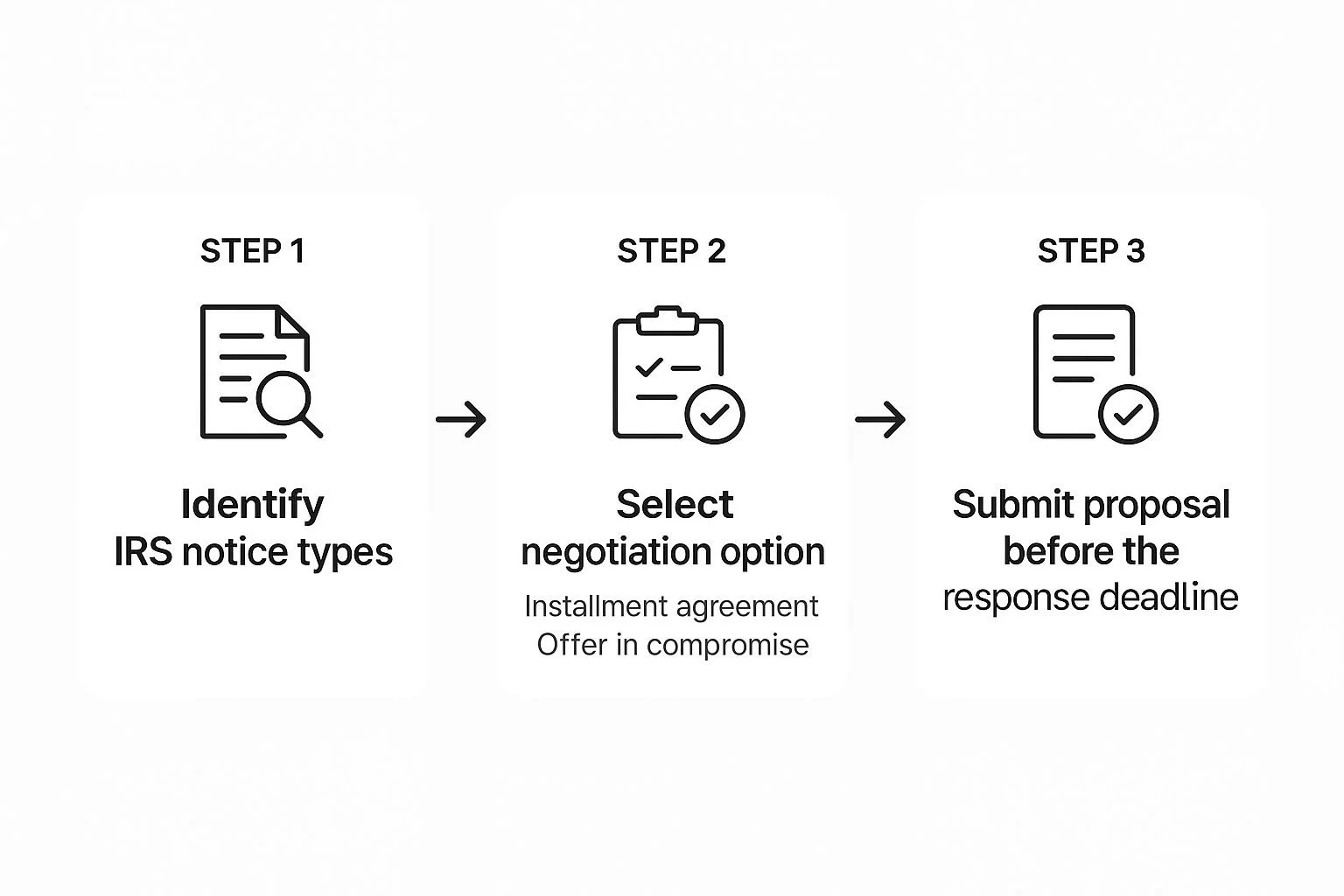

Your First Steps When Negotiating With The IRS

So, what do you do first? You need to understand exactly what you're dealing with.

Decode the Notice and Figure Out Your Options

Every IRS notice has a code, usually printed in the top right corner. You'll see things like CP2000 or CP504. This little code is your first clue—it tells you precisely why they’re reaching out.

Is it a proposed change to your return? A balance due notice? Or a more serious intent to levy? Knowing the notice type dictates how quickly you need to act and what your next move should be.

Once you know why they're contacting you, you can start exploring your resolution options. Most people find themselves on one of two main paths:

Installment Agreement (IA): This is your classic payment plan. You agree to pay your tax debt in full through monthly payments for up to 72 months. It's a great option if you can realistically afford the full amount, just not all at once.

Offer in Compromise (OIC): Think of this as a settlement. An OIC allows you to resolve your tax liability for less than the total you owe. This path is reserved for taxpayers facing true financial hardship who can prove they simply don't have the ability to pay the full debt.

Your financial reality is what ultimately decides the right path. An Installment Agreement is about managing a debt you can pay, while an Offer in Compromise is about proving a debt is uncollectible and settling for a realistic amount.

Before you jump into filling out forms, it's helpful to understand the basic tax relief options available. This table gives you a quick snapshot.

IRS Tax Relief Options At a Glance

Here’s a summary of common ways to resolve tax debt, helping you understand the basics of each path.

| Resolution Option | Best For | Key Requirement |

|---|---|---|

| Installment Agreement | Taxpayers who can pay the full debt over time. | Ability to make consistent monthly payments. |

| Offer in Compromise | Taxpayers with significant financial hardship. | Proving you cannot pay the full amount owed. |

| Currently Not Collectible | Those with no ability to pay living expenses. | Demonstrating severe financial distress. |

| Penalty Abatement | Taxpayers with a valid reason for failing to pay. | Showing "reasonable cause" for the failure. |

Each of these avenues has its own set of rules and required documentation. Choosing the right one from the start is half the battle.

The process always starts with a clear-eyed analysis of your situation, not a knee-jerk reaction. This visual helps lay out the flow from that initial notice to submitting a solid proposal.

As you can see, the path forward requires careful thought. Making the right choice at this stage really does set the foundation for everything that follows.

Assembling Your Financial Documentation for the IRS

When you're facing the IRS, strong arguments don't win the day. Clear, undeniable proof does. Before you even think about proposing a payment plan or an Offer in Compromise, you have to build a rock-solid case with your financial documents.

This isn't just about tallying up what you owe. It’s about painting a credible picture of what you can realistically afford to pay back.

The IRS will dig deep into your finances to calculate your Reasonable Collection Potential (RCP). Think of this as their magic number—what they believe they can squeeze out of you over time.

Your goal is to present a complete and honest financial story that backs up the resolution you're asking for. If they find gaps or inconsistencies, your credibility is shot, and your proposal will likely be rejected.

The Core Financial Documents You Need

Think of yourself as an evidence collector for your own case. You need to create a transparent, 360-degree view of every dollar that comes in and goes out. I always tell my clients to start by gathering documents covering the last three to six months.

Here's your essential checklist:

Proof of Income: Grab recent pay stubs, W-2s, and any 1099s if you do freelance or contract work. If you own a business, you'll need your profit and loss statements.

Bank Statements: Pull statements for all your accounts, including checking and savings. Be ready to explain any large, one-off deposits—they will ask.

Monthly Living Expenses: This is where you document your reality. Collect utility bills, rent or mortgage statements, car payments, insurance bills, and even grocery receipts.

Asset Information: The IRS needs to know what you own. Get statements for your 401(k) or IRA, brokerage accounts, and have valuations ready for real estate, vehicles, or any other significant property.

Debt Information: Finally, gather all your liability statements. This includes credit cards, student loans, medical bills, and anything else you owe.

Key Takeaway: All this information is used by the IRS to fill out their official forms—either Form 433-A for individuals or 433-B for businesses. The data you provide goes directly onto these forms, which are the absolute foundation of any negotiation. Being organized here isn't just a good idea; it's mandatory.

Organizing Your Information for Maximum Impact

Simply handing the IRS a shoebox full of papers is a recipe for disaster. You need to organize everything logically so it tells a clear story.

Group your documents into categories: income, assets, and expenses. I highly recommend creating a simple summary sheet that totals your monthly income and itemizes your necessary living expenses.

This simple step does two critical things. First, it makes the examiner’s job easier, which can generate a surprising amount of goodwill. Second, it forces you to look at the hard numbers, ensuring that whatever offer you make is one you can actually stick to.

Having a firm grasp on your complete financial situation is non-negotiable when dealing with tax issues. If you run a company, it’s even more critical to master financial management for small business effectively.

This whole process isn't just about checking boxes for the IRS; it's about taking control of the situation.

By meticulously assembling your financial story, you start negotiating with the IRS from a position of strength and transparency. It dramatically improves your chances of getting a deal you can live with.

Remember, the better your documentation, the stronger your case. It’s as simple as that.

Using an Offer In Compromise to Reduce Tax Debt

An Offer in Compromise, or OIC, is what many people think of as the holy grail of IRS negotiations. It's an agreement that lets you settle your tax liability for a fraction of what you originally owed.

But let’s be clear: this isn't a get-out-of-jail-free card for anyone who simply wants a discount. The IRS reserves this path for taxpayers in very specific, and often dire, financial straits.

Before you even think about filling out paperwork, you have to understand the three distinct grounds the IRS considers for an OIC. Your entire case will be built on one of these foundations.

The Three Paths to an OIC

Each reason for an OIC is designed to solve a different fundamental problem with your tax bill.

Doubt as to Collectibility: This is, by far, the most common route. You’re essentially telling the IRS, "Look at my income, my assets, and my basic living costs. There is no realistic way I can ever pay you back in full."

Doubt as to Liability: This path is much rarer. Here, your argument isn't about your ability to pay; it's that the tax itself was assessed incorrectly. You're claiming you don't actually owe the money, and you'll need solid evidence to prove the IRS made a mistake.

Effective Tax Administration (ETA): This is the special circumstances clause. You might technically have the assets to pay the debt, but doing so would cause an exceptional economic hardship, or it would be unfair and inequitable for other reasons.

For most people reading this, the journey will be through "Doubt as to Collectibility." This means you're about to get very familiar with your own finances, documenting everything on either a Form 433-A (for individuals) or 433-B (for businesses) to build an undeniable case.

Building Your Case for an OIC

A successful OIC comes down to one thing: the financial story you tell. The IRS examiner reviewing your case won't be swayed by emotion; they operate on hard data. You have to prove, with meticulous documentation, that you simply cannot pay.

And when it works, the results can be life-changing. I’ve seen cases where a small business owner settled a $37,202 payroll tax debt for just $160.

In another incredible instance, a taxpayer facing over $1 million in tax debt was able to settle for $16,194—that's a reduction of more than 99%.

The IRS even provides a starting point on its website to see if you're in the ballpark.

This is a screenshot of the official IRS Offer in Compromise Pre-Qualifier tool. It’s a great reality check, asking you about your filing history, bankruptcy status, and ability to make an initial payment. It gives you a quick, preliminary look at whether you should even proceed.

Submitting an OIC is a serious commitment. The process is lengthy, often taking 6 to 12 months, and requires you to remain fully compliant with all tax filing and payment obligations while your offer is under review.

Because the details are so critical, you’ll want to absorb as much information as you can. This guide on Understanding IRS Offer in Compromise is a fantastic external resource.

What To Do If Your Offer In Compromise Is Rejected

Getting that rejection letter for your Offer in Compromise can feel like a punch to the gut. After all the time you spent gathering documents and carefully filling out forms, a "no" is the last thing you want to see.

But don't toss that letter in the trash just yet. This isn't the end of the road. In fact, that rejection letter is one of the most valuable pieces of the puzzle when you're negotiating with the IRS. It contains the exact roadmap for your next move.

The IRS won’t just send a rejection without an explanation. The letter will spell out precisely why they turned down your offer.

Maybe they think your Reasonable Collection Potential (RCP) is higher than what you offered, or perhaps a key document was missing. This isn't just a denial; it's direct, actionable feedback from the examiner.

Key Insight: A rejection is not a final "no." It's an invitation to refine your strategy. Use the specific reasons provided by the IRS to build a stronger case, whether through an appeal or a new, more informed offer.

Your first job is to dissect that letter. I mean really study it. Understanding exactly where you went wrong is the most important information you can have right now.

Analyzing the Rejection and Planning Your Response

Once you get to the "why," you have a couple of primary paths forward: you can appeal the decision, or you can submit a completely new offer. The right choice depends entirely on the reason for the rejection.

An appeal is the right move if you believe the IRS examiner flat-out made a mistake. Did they miscalculate your ability to pay? Did they misunderstand the information you sent? If so, it’s time to appeal.

You have 30 days from the date on the rejection letter to file a request for a hearing with the IRS Independent Office of Appeals. This is your opportunity to argue your case before a fresh, neutral set of eyes.

On the other hand, if the rejection was because you missed something—like a bank statement or a pay stub—an appeal is overkill. The better route is to simply gather the missing pieces and submit a new, stronger OIC package.

To help you decide, let's look at some of the most common reasons an OIC gets rejected and what you should do about it.

Common Reasons for OIC Rejection and How to Respond

The table below breaks down typical rejection scenarios and provides clear next steps. Think of it as your cheat sheet for turning a denial into a future acceptance.

| Reason for Rejection | What It Means | Your Next Step |

|---|---|---|

| Incorrect RCP Calculation | The IRS analyzed your income and assets and believes you can afford to pay more than you offered. | Scrutinize their math. If you spot an error, file an appeal and provide the evidence to back up your corrected figures. |

| Missing Information | You didn't include all the required documents, or the information you sent was incomplete. | Don't appeal. Just gather the missing documents and submit a new, complete OIC package. |

| Public Policy | In very rare situations, the IRS rejects an offer because accepting it could harm public trust in the tax system. | This is a tough one and usually requires professional guidance. An appeal is almost always your only option here. |

This table covers the big ones, but every case is unique. The key is to use the specific feedback in your letter to guide your response.

The Power of Persistence

It’s incredibly easy to feel defeated at this stage, but persistence is your most powerful asset. The OIC program has an acceptance rate of around 40%, which might sound low, but many of those successful taxpayers got their "yes" on the second or even third attempt.

In fact, the Taxpayer Advocate Service found that for nearly 40% of rejected OICs, the amount offered was higher than what the IRS ultimately collected from the taxpayer later. This tells me that a well-argued case, even after an initial rejection, has a very real chance of success.

So, whether you decide to appeal or resubmit, treat the rejection as a learning experience. By directly addressing the IRS’s concerns, you dramatically improve your odds of finally getting that tax debt resolved.

What If an Offer in Compromise Isn't the Right Fit?

An Offer in Compromise gets a lot of attention, and for good reason—it can be a lifesaver. But let's be realistic: it's not for everyone. The IRS has incredibly strict rules for who qualifies, and many people simply don't make the cut.

That doesn't mean you're out of options. Far from it. When you're facing down the IRS, it’s crucial to know all the tools available. Often, a different, more direct path can get you the relief you need without the grueling OIC process.

Securing an IRS Installment Agreement

The most common and straightforward alternative is an Installment Agreement (IA). Think of it as a formal payment plan with the IRS. You agree to pay what you owe in full, but you get to do it over time in monthly payments you can actually manage.

If your total tax bill—including all the penalties and interest—is under $50,000, you might be eligible for a streamlined agreement. You can often set these up online in just a few minutes. It's that simple.

For debts over that amount, the paperwork gets a bit more involved, but it's still a very achievable goal. You'll need to share some financial information, but it’s nowhere near the deep dive required for an OIC.

An IA is perfect for anyone who can eventually pay their tax debt but needs breathing room to do it without the threat of a bank levy or wage garnishment.

When You Truly Cannot Pay Right Now

What happens when your finances are in such dire straits that even a small monthly payment is impossible? This is exactly why the IRS created the Currently Not Collectible (CNC) status.

CNC is a temporary hold the IRS places on your account when you're experiencing severe financial hardship.

To be clear, CNC does not erase your debt. It's a pause button. The IRS agrees to halt collection activities, giving you breathing room. However, interest and penalties continue to accrue, and the IRS will review your financial situation periodically to see if your ability to pay has improved.

To get into CNC status, you have to prove that your necessary living expenses eat up more than your monthly income. It’s a critical safety net for people in a genuine financial crisis.

Asking for Penalty Abatement

Sometimes, the penalties are the real killer. A huge chunk of your total tax debt might just be penalties tacked on for filing or paying late. The good news is the IRS can remove them if you had a reasonable cause for the delay.

What counts as a valid reason? Things like:

A serious illness or the death of an immediate family member.

Your home or business records were destroyed in a fire, flood, or another disaster.

You received incorrect advice from a tax professional you trusted.

There's also the First Time Abatement (FTA) policy. If you’ve had a clean record for the past three years (meaning you filed and paid on time), the IRS might agree to waive penalties as a one-time courtesy.

Getting penalties removed can slash your total balance, making what's left much more manageable.

Common Questions About IRS Negotiations

When you're staring down a tax problem, questions are bound to pop up. Getting straight answers is the first step toward taking control of the situation. Let's break down some of the most common things people ask when they're getting ready to negotiate with the IRS.

Can I Negotiate With the IRS On My Own?

Technically, yes. You have every right to represent yourself in front of the IRS. But I have to be honest—it's a minefield. The IRS has its own language, strict deadlines, and a mountain of procedural rules. It's incredibly easy for an everyday taxpayer to get tripped up.

This is exactly why most people bring in a professional, like a tax attorney, CPA, or Enrolled Agent. An expert doesn't just know the tax code; they live and breathe negotiation strategy. They become a critical buffer between you and the IRS, making sure your case is presented correctly and persuasively.

How Long Does the Negotiation Process Take?

There's no single answer here—the timeline really depends on the resolution you're aiming for.

Simple Installment Agreement: If you qualify for a streamlined agreement, you can often get it set up online in minutes. It's the quickest path.

Offer in Compromise (OIC): This is a marathon, not a sprint. From the day you submit your OIC package, you can expect the IRS to take anywhere from 6 to 12 months, and sometimes longer, to investigate and give you a final decision. Patience is a must.

Will Negotiating Stop IRS Collection Actions?

For the most part, yes. When you take a formal step to resolve your debt, like submitting an Offer in Compromise or requesting an Installment Agreement, the IRS usually hits pause on aggressive collection actions. This means things like wage garnishments and bank levies are put on hold while they review your case.

This gives you some much-needed breathing room to focus on the negotiation without the constant threat of your assets being seized.

Important Note: This temporary protection only works if you play by the rules. If you miss deadlines for sending in documents or fall behind on your current taxes, the IRS can—and will—restart collections.

Sometimes, the tax debt isn't even yours—it might stem from a spouse or ex-spouse. If you find yourself in that situation, it's crucial to look into the rules for IRS innocent spouse relief to see if you can be absolved of the liability.

At the end of the day, being proactive is your best defense. The IRS is always more cooperative with taxpayers who are making a genuine effort to find a solution.

Feeling overwhelmed by your tax situation? At Attorney Stephen A Weisberg, I start with a FREE Tax Debt Analysis to determine the best path forward for your specific case. Get in touch today to resolve your IRS issues with confidence.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034