IRS Lien or Levy Navigating Tax Collection

When you’re staring at a stack of notices about unpaid taxes, words like lien and levy can sound terrifying and, frankly, a little confusing. They’re often used together, but they mean very different things. Getting a handle on the distinction is your first real step toward getting out from under the weight of tax debt.

At its core, the difference is pretty straightforward: a lien is the government’s legal claim on your property to secure a debt. A levy is the actual seizure of that property to pay off the debt. One is a warning shot, the other is the cannonball.

What Happens When You Owe Unpaid Taxes

Let's be clear: the IRS doesn't just show up one day and take your house. There’s a formal process that starts with a series of letters and notices. The absolute worst thing you can do is pretend they don't exist. Ignoring this official mail only makes the problem worse and pushes the IRS toward more aggressive actions.

Typically, the first major step the IRS takes is filing a federal tax lien. This happens after they've assessed what you owe, sent you a bill (a "Notice and Demand for Payment"), and you haven't paid it.

The lien is a public record that essentially tells the world—including banks, lenders, and other creditors—that the government has first dibs on all your property. That includes your home, your car, and even your financial assets. You can dig into the official specifics of federal tax liens right from the IRS.

From Claim to Seizure

It's crucial to understand how a lien can escalate into a levy. A lien just secures the government's interest in your assets; a levy is when they actively take them.

Think of it like this:

Lien: This is a security measure. It’s like the government putting a legal chain on your property, making it nearly impossible to sell or refinance until you settle up.

Levy: This is the enforcement action. It’s the IRS actually yanking money from your bank account, garnishing your wages, or seizing physical property to cover what you owe.

This table breaks down the key differences between these two powerful collection tools.

| Attribute | Tax Lien | Tax Levy |

|---|---|---|

| Purpose | To secure the government's claim on your property. | To seize and sell property to satisfy the tax debt. |

| Action | A legal claim filed against your property. | The actual seizure of your assets. |

| Impact | Damages credit; complicates property sales. | Immediate loss of assets (cash, wages, property). |

| Timing | Usually the first major collection step. | Occurs after a lien and multiple notices. |

The Federal Tax Lien Explained

When people hear "tax lien," they often picture the government immediately taking their property. That’s not quite right. A federal tax lien is the government’s legal claim against your property because you haven't paid your tax debt.

It's less of a seizure and more like the IRS putting a public, legal "hold" on everything you own—and will own in the future. This is a critical distinction in the lien or levy conversation because the lien almost always comes first.

The lien itself is born automatically behind the scenes after three things happen: the IRS assesses your liability, sends you a Notice and Demand for Payment, and you don’t pay up. The real trouble starts when the IRS files a Notice of Federal Tax Lien. This move makes your debt public, alerting creditors that the government gets first dibs on your assets if you try to sell anything.

The Real-World Consequences of a Lien

Even without the IRS taking a single thing, the financial fallout from a Notice of Federal Tax Lien can be devastating. Its existence is a massive red flag to the entire financial world.

First off, a lien torpedoes your ability to get credit. Since it's a public record, credit bureaus will see it, and your credit score often takes a nosedive. Need a car loan or a business line of credit? It just became incredibly difficult.

Key Insight: A tax lien doesn't take your property. Instead, it freezes your financial mobility by attaching a government claim to your assets, making it nearly impossible to sell or borrow against them until the debt is resolved.

Think about a small business owner whose company is otherwise thriving. They might apply for a critical line of credit to buy inventory, only to be denied because of a tax lien. To the bank, that lien screams "high risk," placing the government at the front of the line for repayment.

It’s the same story for homeowners. You might want to refinance your mortgage for a better rate or tap into your home's equity, but you'll find it's impossible. No new lender will touch the property until the lien is settled, leaving you stuck.

The only way out is to resolve the underlying tax debt, which can be a complex and frustrating process. We cover the specific steps in our guide on how to remove a tax lien. Until you do, that lien will hang over your head, obstructing your financial health and setting the stage for more aggressive actions, like a levy, if the debt goes unpaid.

The IRS Tax Levy Explained

If a tax lien is the government’s claim, a tax levy is the aggressive follow-through. It’s the actual, legal seizure of your assets to pay off an unpaid tax bill. When you're weighing the seriousness of a lien or levy, make no mistake: a levy is a major escalation and a much more immediate threat to your financial well-being.

The IRS can't just show up and take your property on a whim, though. The law demands they follow a strict notification process. After assessing your tax liability and sending a payment demand, the IRS must issue a Final Notice of Intent to Levy and Notice of Your Right to a Hearing. This is your last official warning, and it typically gives you 30 days to respond before the seizure starts.

Ignoring this notice is one of the worst things you can do. It's the green light the IRS needs to start taking your property, often without ever having to step foot in a courtroom.

The Different Forms of a Tax Levy

A lien is a single claim that attaches to all your property, but a levy is much more targeted. The IRS can deploy several types of levies, choosing the one they think will be most effective at collecting the money you owe.

Bank Levy: The IRS can instruct your bank to freeze your account for 21 days. After that holding period, the bank is required to send the IRS whatever is in the account, up to the full amount of your tax debt. This is a one-time hit, but it can drain your checking and savings without any further notice.

Wage Garnishment: This is a continuous levy—it doesn't stop. The IRS orders your employer to withhold a substantial part of every paycheck and send the funds directly to them. This will continue until your entire tax debt is paid in full.

Property Seizure: In the most serious situations, the IRS has the power to seize physical assets like your house, car, or even business equipment. They will then sell these assets at a public auction and apply the money to what you owe.

Key Difference: A lien is a public claim that secures the government's interest in everything you own. A levy is the direct action of taking a specific asset, whether it's the cash in your bank or the wages from your job.

The consequences of a levy are immediate and often devastating. A bank levy can cause your checks to bounce and automatic bill payments to fail. A wage garnishment can make it nearly impossible to cover basic living expenses like rent and groceries.

Because the process is so aggressive, responding to a Final Notice of Intent to Levy immediately is non-negotiable. Acting fast is the only way to protect your hard-earned assets from seizure.

Comparing a Tax Lien and Tax Levy Head to Head

To really get to the heart of what separates a tax lien or levy, it helps to put them side-by-side. While they both come from unpaid tax debt, their purpose, power, timing, and the financial pain they cause are worlds apart. For any taxpayer staring down an IRS collection notice, understanding these differences is absolutely critical.

Think of it this way: a lien is a passive claim, while a levy is an active seizure. One secures the government’s place in line to get paid; the other physically takes your property to settle the score.

Purpose and Legal Power

The fundamental difference between the two really boils down to intent. A tax lien is all about securing the debt. When the IRS files a Notice of Federal Tax Lien, it’s a public declaration that they have a legal claim to your property. This ensures they get paid before most other creditors if you sell your assets. It’s a protective move, not an act of collection.

A tax levy, on the other hand, is designed to collect the debt. This is an enforcement action where the IRS actively seizes your assets. The legal power of a levy is far more immediate and disruptive, directly hitting your cash flow and your ownership of property.

Timing and Escalation

Timing is another huge giveaway. A tax lien almost always comes first. It’s the foundational step the IRS takes after assessing your tax bill and sending you a demand for payment. The lien serves as a serious warning shot, signaling that more aggressive actions are on the table if the debt isn't handled.

A levy is a major escalation. It only happens after the IRS has already sent you multiple notices, including the all-important Final Notice of Intent to Levy. This sequence shows a clear, deliberate progression from just securing a claim (the lien) to enforcing collection (the levy).

A lien is the government putting a "reserved" sign on your property. A levy is the government towing that property away. The first wrecks your credit and financial flexibility; the second causes immediate, tangible loss.

Financial Impact

The financial consequences of a lien versus a levy couldn't be more different.

Tax Lien Impact: The damage here is mostly to your financial reputation and future options. A lien will tank your credit score, making it incredibly difficult to get new loans or sell property. It’s a long-term headache that eats away at your financial standing.

Tax Levy Impact: The damage is immediate and very real. A bank levy can empty your account in a single day, while a wage garnishment will take a slice out of every paycheck. It directly threatens your ability to cover basic living expenses.

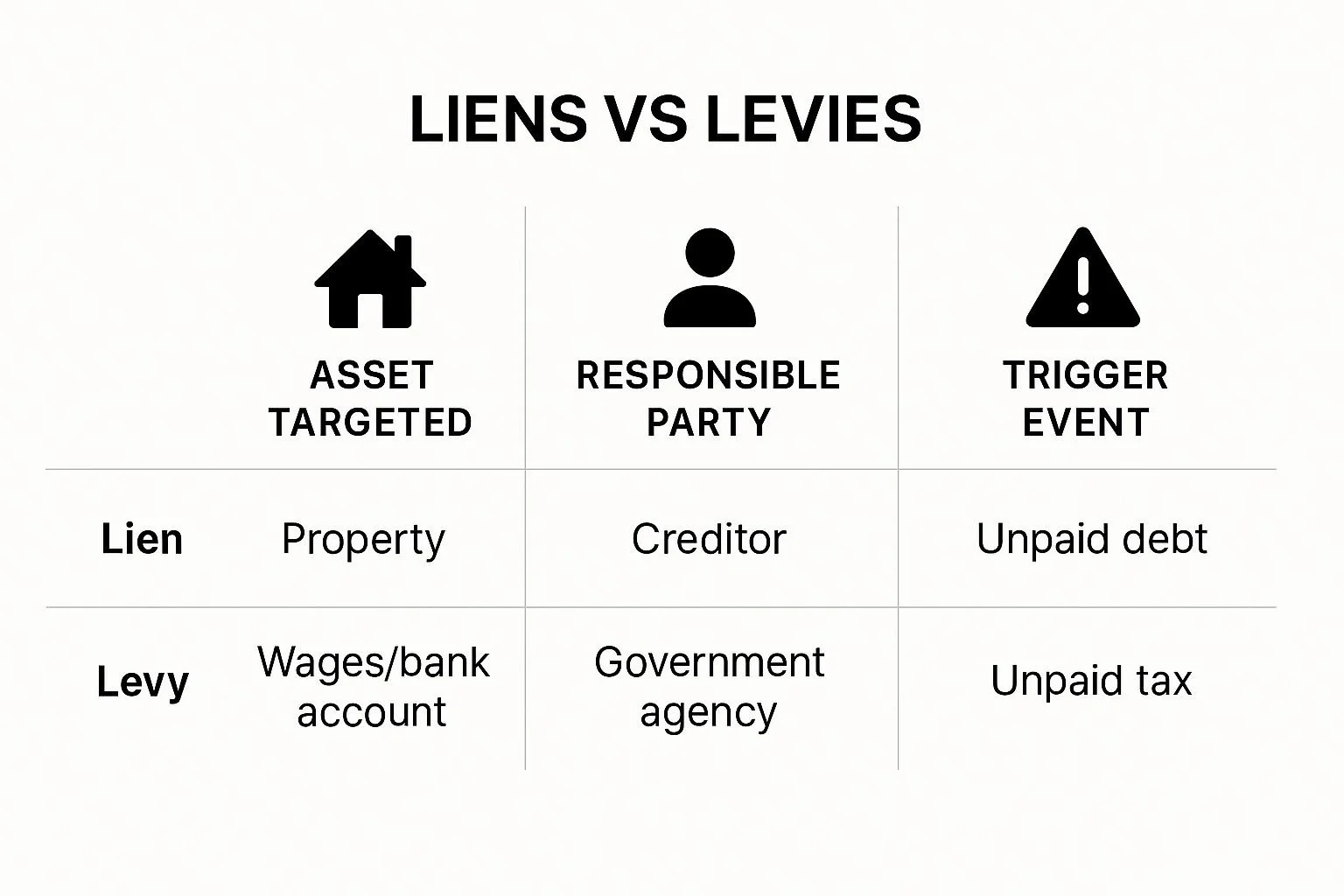

This image really simplifies what a lien versus a levy targets.

As you can see, the lien is a broad claim that attaches to all your property, while the levy is a direct action targeting specific assets like your bank funds or wages.

For a quick reference, it helps to see these two actions laid out in a simple comparison.

Tax Lien vs Tax Levy At a Glance

This table breaks down the core attributes of each, so you can see exactly how they stack up against one another.

| Attribute | Tax Lien | Tax Levy |

|---|---|---|

| Primary Action | A legal claim against all your property. | The actual seizure of specific assets. |

| What It Does | Secures the government's interest in your assets. | Collects the tax debt by taking property. |

| Immediate Effect | Public notice is filed; damages credit score. | Loss of funds from bank accounts or wages. |

| Who It Affects | Primarily affects your creditors and credit standing. | Directly affects you by taking your money. |

| Resolution | Requires payment or negotiation to get it released. | Requires immediate action to stop the seizure. |

Ultimately, while both are serious, a levy represents a far more urgent threat to your day-to-day financial stability.

How to Resolve an IRS Lien or Levy

Seeing an official notice about an IRS lien or levy can be a gut-wrenching experience. It's intimidating, but the worst thing you can do is nothing. Burying your head in the sand only makes it worse, as penalties and interest keep piling up.

You have options, but your strategy needs to match the problem—resolving a lien (a claim on your property) is very different from stopping a levy (an active seizure).

A lien is about clearing the debt to free up your property. A levy, on the other hand, is a fire alarm. It requires an immediate response to stop the IRS from taking your money or assets. In either case, talking to the IRS is always the first step.

Strategies for Lien Resolution

When the IRS files a Notice of Federal Tax Lien, your main goal is to get it released. A released lien means you can finally sell or refinance your property without the government’s claim standing in the way, and it’s the first step toward cleaning up your credit report.

Here’s how most people tackle it:

Pay the Debt in Full: This is the most straightforward route. Pay what you owe, and the IRS must release the lien within 30 days. Simple as that.

Installment Agreement: If paying in a lump sum isn't realistic, an Installment Agreement breaks the debt into manageable monthly payments. The best part? After you’ve made a few on-time payments, you can often ask for a lien withdrawal. This pulls the public notice, making it invisible to lenders and credit bureaus, even while you're still paying off the balance.

Offer in Compromise (OIC): This is a lifeline for taxpayers in serious financial trouble. An OIC lets you settle your tax debt for less than you actually owe. It's not a given, though. The IRS pores over your finances—your income, expenses, and what your assets are worth—to decide if you qualify. It’s worth exploring if you’re in a tough spot, and you can learn more about how to qualify for an Offer in Compromise.

Expert Tip: A lien doesn't have to be an all-or-nothing fight. You can request a discharge to remove the lien from one specific asset, like a house you need to sell. Or you could seek subordination, which lets another creditor (like a mortgage lender) jump ahead of the IRS in line. These are powerful tools in complex situations.

Immediate Responses to a Levy

A levy is a whole different ballgame. It’s much more urgent than a lien. Once you get that "Final Notice of Intent to Levy," the clock starts ticking—you usually have just 30 days to act before the IRS starts taking your wages, bank funds, or other assets. Your mission is to stop it before it starts.

Here’s how you can request a levy release:

Pay Your Tax Debt: Just as with a lien, paying the debt in full stops a levy dead in its tracks.

Prove Economic Hardship: If the levy would leave you unable to pay for basic living expenses like housing, food, or medical care, the IRS may agree to back off. This typically involves getting your account classified as Currently Not Collectible (CNC).

Enter a Payment Plan: Setting up an Installment Agreement is one of the most reliable ways to stop a proposed levy.

Appeal the Decision: You absolutely have the right to appeal. By filing a Collection Due Process (CDP) hearing request within that 30-day window, you legally pause the levy. This gives you critical time to negotiate a better solution.

Whether it's a lien or a levy, the solution always starts with taking swift, informed action. Knowing your options gives you the power to take back control and work toward a resolution that lets you move forward.

The Global Context of Tax Enforcement

While we often think of tax problems as a national issue, the reality is that the lien and the levy are fundamental tools for governments everywhere. If your business operates on a global scale, you're not just dealing with the IRS; you're navigating a complex web of international tax collection rules, many of which can be surprisingly aggressive.

This isn't random. A country's economic health and national debt often dictate how hard they'll come after unpaid taxes. Nations with high debt or shaky economies tend to enforce their tax laws more forcefully to keep revenue flowing.

You can see this play out in corporate tax rates around the world. The average statutory rate across 181 countries is about 23.51%, but the range is huge. Some countries have rates topping 35%, while others keep them low to attract foreign investment. You can explore corporate tax rates across different countries to get a sense of this incredible variation.

Key Takeaway: A government's decision to pursue a lien or levy is not just about a single unpaid bill; it's often a reflection of broader economic policy and national fiscal stability.

Understanding this bigger picture is crucial. For any business, it drives home the point that solid tax compliance isn't just a local headache—it's a critical piece of your global strategy.

Frequently Asked Questions About Liens and Levies

When you're dealing with a tax lien or levy, it's natural to have a lot of questions. Let's get straight to the point and tackle some of the most common concerns I hear from taxpayers.

Can the IRS Levy My Property Without a Lien First?

This is a big one, and the short answer is yes, they can. While the IRS usually files a Notice of Federal Tax Lien before taking your property, it's not a legal must-have. The real trigger for a levy isn't the lien—it's the Final Notice of Intent to Levy.

Think of the lien as the IRS securing its spot in line against other creditors. The levy is the action. So, you could find your assets at risk even without a public lien filing, which is why responding to every single piece of IRS mail is absolutely critical.

How Long Does a Federal Tax Lien Last?

A federal tax lien doesn't stick around forever. It automatically expires after 10 years from the date the tax was officially assessed. This deadline is called the Collection Statute Expiration Date (CSED). Once the debt is paid or the CSED hits, the IRS has 30 days to release the lien.

Important Consideration: Be careful, because this 10-year clock can be paused. Actions like filing for bankruptcy or submitting an Offer in Compromise "toll" the statute, effectively giving the IRS more time to collect.

What Should I Do Immediately After Receiving a Levy Notice?

Do not hesitate. The moment you get a levy notice, your first step is to pick up the phone and call the IRS or a qualified tax professional. This is a serious, time-sensitive situation. You typically have only 30 days to act before the seizure of your assets begins.

Ignoring it is the worst thing you can do. You need to immediately figure out your options, which might include:

Requesting a levy release because it’s causing an economic hardship.

Setting up a formal payment plan or installment agreement.

Filing a timely appeal to stop the collection process in its tracks.

Prompt communication is your single most powerful defense against losing your wages, bank accounts, or other property.

Facing a lien, levy, or other complex tax problem can feel overwhelming. At Attorney Stephen A Weisberg, we begin with a FREE Tax Debt Analysis to determine the best path forward before you commit to anything. Find out how we can help resolve your IRS issues today.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034