What Is an IRS Levy? How It Affects Your Tax Payment Options

An IRS levy is the legal seizure of your property to satisfy a tax debt. It’s one of the most powerful tools the IRS has to collect unpaid taxes, and it’s a step that’s taken very seriously.

While people often mix them up, a levy is fundamentally different from a tax lien. A lien is simply the government’s legal claim against your property to secure a debt. A levy, on the other hand, is the actual act of taking that property—like draining funds from your bank account or garnishing your paycheck.

Understanding the Power of an IRS Levy

Receiving a levy notice is, without a doubt, alarming. But knowing what you’re up against is the first step toward getting it under control. I like to use this analogy: think of a tax lien as the city putting a boot on your car for unpaid parking tickets. The boot secures their claim and stops you from selling the car, but you still have it.

An IRS levy is the tow truck showing up and physically hauling your car away to the impound lot. It’s the enforcement action. This process allows the IRS to seize your assets without first getting a court order. While that sounds harsh, a levy is usually the last resort in a long collection process.

The IRS sends multiple letters and warnings first because, frankly, they would much rather you just pay what you owe voluntarily. To clear up any confusion, let's look at the key differences between a levy and a lien side-by-side.

IRS Levy vs IRS Lien Key Differences

This table breaks down the crucial distinctions between an IRS levy and a tax lien. These two terms are often used interchangeably, but they represent very different stages and actions in the IRS collection process. Understanding these differences is key to knowing where you stand and what to expect.

| Aspect | IRS Levy | IRS Lien |

|---|---|---|

| Action | Actual seizure of assets. The IRS physically takes your property (e.g., money from your bank account). | Legal claim against your assets. It secures the government's interest in your property as collateral. |

| Purpose | To satisfy the tax debt by collecting funds or property to pay it off. | To secure the tax debt by giving the IRS a legal right to your property over other creditors. |

| Impact | Immediate loss of property or funds. Can lead to wage garnishments or bank account freezes. | Future impact. Damages your credit and prevents you from selling or refinancing property without paying the debt. |

| Trigger | Occurs after a Final Notice of Intent to Levy is issued and you fail to resolve the debt. | Generally filed after the IRS assesses the liability, sends a bill, and you neglect or refuse to pay. |

In short, a lien is a claim, while a levy is the action of taking. The lien is the warning shot; the levy is the direct hit.

The Scope of a Levy

An IRS levy is authorized by Internal Revenue Code (IRC) section 6331, which gives the agency incredibly broad authority to seize property. This isn't limited to just cash in the bank.

The IRS can legally take action against a wide range of your assets, including:

Wages, salaries, and commissions (wage garnishment)

Funds held in your bank or credit union accounts

Social Security benefits and other federal payments

Accounts receivable owed to you by clients or customers

Physical assets like your car, boat, or even your home

For self-employed individuals and business owners, the threat is even more pointed. A levy can cripple your operations overnight by seizing payments from your clients. You can read more about these specific challenges in our article covering the misuse of levies for self-employed clients.

The good news? A levy doesn't happen out of the blue. The IRS has to follow a strict legal procedure, which includes sending you multiple notices. The most critical one is the Final Notice of Intent to Levy, which gives you a 30-day window to respond and prevent the seizure from ever happening.

The Timeline Leading to an IRS Levy

An IRS levy doesn't just happen out of the blue. The IRS has to follow a strict, legally mandated process before they can touch your assets. Knowing this timeline is your single best defense, because it gives you the chance to get ahead of the problem instead of just reacting to it.

The whole thing kicks off after the IRS officially assesses a tax debt. From there, they start sending a series of letters designed to get your attention and push you to resolve what you owe. This predictable sequence gives you several opportunities to respond and stop things from getting worse.

The Initial Notices and Demands

The first letter you'll likely see in your mailbox is an initial bill, usually a Notice CP14. This is a straightforward letter telling you that you have a balance due and giving you a deadline to pay it. If you don't pay or get in touch, the IRS will send more notices, and each one will sound a little more serious than the last.

These follow-up letters, like the CP501, CP503, and CP504, are essentially reminders of your growing tax bill. They’ll spell out what you owe, including the penalties and interest that are piling up, and demand payment. While getting these can be stressful, they aren't the levy itself. Think of them as warning shots—clear signals that you need to address the debt before the IRS takes more forceful action.

The goal of this barrage of letters is actually to encourage you to work with them. The IRS would much rather you engage and find a solution than force them to start seizing your property.

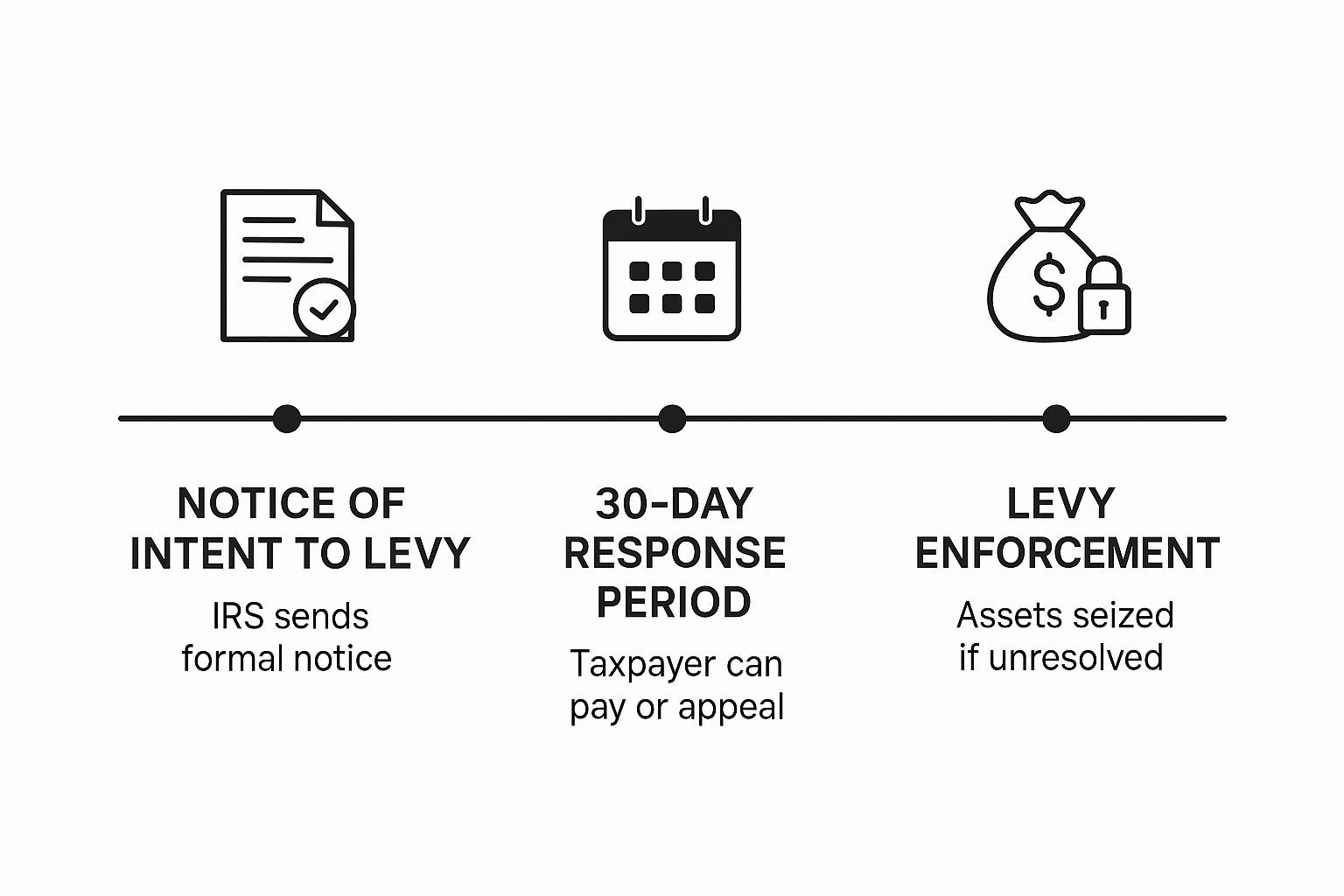

This infographic lays out the final, most critical steps before a levy can actually happen. As you can see, even after receiving the formal intent to levy notice, you still have a clear window of time to prevent the seizure of your assets.

The Final Notice and Your 30-Day Window

The most important letter in this whole process is the Final Notice of Intent to Levy and Notice of Your Right to a Hearing. This is the big one—your last official warning. The moment you get this letter, a critical clock starts ticking.

You have exactly 30 days from the date printed on the notice to do something. This 30-day window is your final chance to:

Pay the tax debt in full.

Set up a formal payment plan, known as an Installment Agreement.

Submit an Offer in Compromise to try and settle your debt for less than you owe.

Appeal the collection by requesting a Collection Due Process (CDP) hearing.

If you let that 30-day period pass without a response, the IRS is legally cleared to start seizing your assets. That could mean taking money directly from your bank account, garnishing your wages, or confiscating other property without any more warnings. Taking a hard look at your options, like those under the IRS Fresh Start Program, during this critical window is absolutely essential to protecting your financial future.

What Assets Can the IRS Actually Seize?

When you're facing down an IRS levy, the first question that usually pops into your head is a big one: what can they really take? It's a question that cuts right to the heart of the matter, because understanding the IRS's reach shows you just how serious this is. And their reach is broad, covering everything from the cash in your bank account to the car in your driveway.

Let's be clear—the point here isn't to scare you. It's to give you a realistic picture of what's on the line. Knowing which assets are vulnerable is the first step in figuring out how to protect them. The IRS typically goes after the low-hanging fruit first, which means the assets that are easiest to turn into cash.

Financial Accounts and Income Streams

More often than not, the IRS starts by going after your financial lifelines. These levies can happen fast, often through automated systems, once all the required notices have been sent and the waiting periods have expired.

Bank Accounts: This is usually target number one. A bank levy freezes the funds in your checking or savings account on the day the notice hits the bank, grabbing everything up to the amount you owe. The bank is legally required to hold that money for 21 days before sending it to the IRS. This gives you one last, very short window to fight back and get the levy released.

Wages and Salary: This is what’s known as a wage garnishment, and it’s a continuous levy. Essentially, the IRS sends an order to your employer, telling them to slice off a hefty portion of your paycheck and send it directly to them. This doesn’t just happen once; it happens every single payday until the debt is gone.

Retirement and Investment Accounts: Even your long-term savings aren't entirely safe. The IRS can levy payments and distributions coming out of your 401(k), IRA, or other retirement funds. While the principal balance might have some protections, any money you take out is fair game. They can also snatch dividends from stocks and other investment income.

The power to seize assets is the government’s ultimate collection tool. It’s a stark reminder of why you can’t just ignore IRS mail, especially a Final Notice of Intent to Levy. The consequences can be immediate and financially devastating.

Federal Payments and Other Receivables

The IRS’s reach extends beyond your own bank accounts and paychecks. They can also intercept money that other people—including the federal government itself—owe you. This is usually handled through the Federal Payment Levy Program (FPLP), an automated system that flags federal payments going out to taxpayers with outstanding debts.

This means the IRS can take a slice of payments you might be expecting, such as:

Social Security Benefits: They can take up to 15% of your monthly benefit.

Federal Employee Retirement Annuities: A portion of these payments can be levied.

Payments to Government Contractors: If you do business with a federal agency, the IRS can intercept your payments before they ever get to you.

When it comes to an IRS levy, wage garnishment is a powerful way for them to collect. The agency follows strict internal rules, laid out in the Internal Revenue Manual, and tracks everything through Collection Activity Reports.

Using systems like the Integrated Collection System (ICS), they can fire off levy notices to employers and banks with surprising efficiency. You can dig into the nitty-gritty of their formal procedures by reviewing the IRS levy policy guidelines.

Physical and Real Property

It's less common than a bank levy, but the IRS absolutely has the power to seize and sell your physical property. This is usually a last-ditch effort for them because it’s a much more involved and public process.

Assets they can seize include things like:

Real Estate: This could be your primary home, a vacation property, or rental real estate.

Vehicles: Your car, truck, boat, or motorcycle are all on the table.

Personal Property: In some cases, high-value personal items like expensive jewelry or art can be seized.

The seizure of a home or car is a drastic measure. It really hammers home the importance of getting ahead of your tax debt before things escalate to this critical point.

Which Assets Are Protected From an IRS Levy

The thought of an IRS levy is understandably scary, but it's important to realize they can't just take everything you own. Federal law draws a hard line in the sand, creating specific protections for certain assets and income streams. Knowing where that line is can go a long way in reducing stress and giving you a clear-eyed view of your situation.

The government gets it—even if you owe back taxes, you still need to survive. That's why a certain amount of your income and specific types of property are legally off-limits to an IRS levy.

Knowing what the IRS can't take is just as important as knowing what they can. These legal protections ensure that a tax debt doesn't leave you completely destitute, providing a small but vital safety net during a difficult financial period.

Legally Exempt Assets and Income

Federal law specifically shields certain assets from seizure. This is designed to ensure you can still cover basic living expenses while you work toward resolving your tax debt.

Generally, the exempt assets fall into a few key categories:

Certain Government Benefits: Key income sources like unemployment payments, some workers' compensation benefits, and certain disability payments are protected.

A Portion of Your Wages: The IRS isn’t allowed to grab your entire paycheck. A specific amount, which is calculated based on your filing status and the number of dependents you have, is exempt from garnishment.

Essential Property: The law protects basic necessities like schoolbooks, undelivered mail, and certain items of clothing.

Tools of the Trade: The equipment and tools you need for your job or business are exempt up to a certain value. This amount is adjusted each year for inflation.

Now, while many retirement accounts can become vulnerable once you start taking distributions, it’s worth digging into the specific rules for your type of account.

And while it's critical to understand these IRS-specific protections, it's never a bad idea to think about broader financial safeguards. Looking into options like asset protection insurance can help you build a more secure financial future against a whole range of potential risks, not just tax problems.

How to Stop an IRS Levy and Resolve Your Tax Debt

When you get that levy notice—or worse, discover your bank account is already frozen—the clock is ticking. This isn't the time to panic; it's the time to act. Fortunately, the IRS has several well-defined paths you can take to stop the bleeding and start working toward a resolution.

The absolute worst thing you can do is ignore it. That only guarantees the situation will escalate. By engaging with the IRS and choosing one of their formal resolution strategies, you can halt the collection process and get back on your feet financially. Let’s walk through the most common and effective ways to stop an IRS levy in its tracks.

Pay the Debt in Full

Let's start with the most straightforward solution: paying the tax debt in full. It’s not a realistic option for many, but if you have the resources, it’s the quickest way to end the nightmare. Once your payment clears and your balance hits zero, the IRS will release any active levies on your wages or bank accounts.

This move immediately stops the bleeding from penalties and interest, giving you a completely clean slate. It’s the fastest way to get the IRS out of your life for good.

Negotiate an Installment Agreement

If paying in a lump sum is out of the question, an IRS Installment Agreement is your next best friend. Think of it as a formal payment plan that lets you chip away at your tax debt with manageable monthly payments. Once the IRS approves your agreement, they will typically release active levies, provided you stick to the payment schedule.

There's one catch: you have to be current on filing all your past tax returns to qualify. The process for setting one up is often surprisingly simple and can be done online, over the phone, or through the mail. For a deeper dive into negotiating the best terms, check out our guide on how to stop an IRS levy.

Key Insight: An approved Installment Agreement isn't just a payment plan; it's a formal truce with the IRS. It signals you're serious about paying what you owe, and in return, they agree to call off the aggressive collection tactics like levies.

Apply for an Offer in Compromise

An Offer in Compromise (OIC) is a powerful tool that allows some taxpayers to settle their tax debt for less than the full amount owed. This isn't a get-out-of-jail-free card; it’s reserved for people facing genuine financial hardship who have no realistic way to pay their full tax bill. The IRS will scrutinize your ability to pay, looking at your income, expenses, and the value of your assets.

Be warned, the application is a beast. It requires extensive financial disclosure and documentation. While your OIC application is being reviewed, the IRS will pause any levy actions. Given the complexity, many people seek professional document preparation consultation services to make sure every 'i' is dotted and 't' is crossed.

Request Currently Not Collectible Status

What if your financial situation is so severe you can't even afford basic living expenses, let alone a payment plan? You can ask the IRS to place your account in Currently Not Collectible (CNC) status. If they agree, they’ll temporarily stop all collection attempts, including levies.

This isn't a permanent fix. Interest and penalties will keep piling up, and the IRS will check in on your financial health periodically. But for someone in a true crisis, CNC status provides immediate and desperately needed breathing room.

One of the most powerful automated tools the IRS uses is the Treasury Offset Program (TOP). This system is a prime example of how the IRS can levy federal payments, like Social Security benefits, automatically. The program is set up to continuously withhold 15% of any matched payments until the tax debt is fully paid. It’s a relentless system that underscores why taking action is so critical.

Common Questions About Dealing With an IRS Levy

Once you understand the basics of an IRS levy, the theory gives way to some very real and urgent questions. The "what ifs" can feel overwhelming, and you need straight answers to figure out what to do next. This is where we get into the practical, nitty-gritty concerns people have when facing a levy.

Let's tackle the questions that probably keep you up at night. The goal here is to give you the clarity and confidence to handle whatever the IRS throws your way.

How Long Does a Wage Garnishment Last?

A wage garnishment isn't a one-and-done event. It's what the IRS calls a "continuous levy." Once that notice hits your employer's desk, they are legally required to start taking a chunk out of your pay.

This will happen every single payday, without fail, until one of three things occurs:

The tax debt is paid off completely. Once the original tax, plus all the accrued penalties and interest, is paid in full, the garnishment must stop.

You work out a different deal with the IRS. If you successfully negotiate a formal Installment Agreement or an Offer in Compromise, the IRS will release the wage levy.

The clock runs out. The IRS typically has 10 years to collect a tax debt, a deadline known as the Collection Statute Expiration Date (CSED). Once that date passes, they can no longer legally collect, and the levy must be released.

The most important thing to remember is that the garnishment will not stop on its own. You have to take action to resolve the tax debt to get your full paycheck back. Ignoring it just means the financial pain will continue indefinitely.

Can the IRS Take Money from a Joint Bank Account?

This is a huge point of confusion and anxiety for married couples and anyone who shares a bank account. And the answer, unfortunately, is yes. The IRS can absolutely levy a joint bank account, even if the tax debt belongs to only one of you.

Here's why: The IRS is authorized to seize a taxpayer's "property or rights to property." In a joint bank account, each owner typically has the right to withdraw 100% of the funds. The IRS sees that right and concludes they can take the full amount, up to what you owe, regardless of who actually earned or deposited the money.

Important Note: If your spouse's money gets swept up in a levy for your debt, they aren't completely out of luck. The non-liable spouse can file a claim to get their portion of the money back. But this is a reactive, uphill battle that involves proving exactly which funds belonged to whom, a process that can be frustrating and take a long time.

What Is the Difference Between a Levy Release and a Levy Return?

These two terms sound almost identical, but they mean vastly different things for your money and property. It's critical to know the distinction.

A Levy Release means the IRS has stopped its active collection efforts. For instance, they'll notify your employer to stop garnishing your wages. But here's the catch: a release does not get you back what they've already taken. The money from past garnished paychecks or the funds they grabbed from your bank account is gone—it's been applied to your debt. A release just stops the bleeding.

A Levy Return is much more powerful and much less common. This is when the IRS actually gives your seized money or property back to you. This usually only happens if the levy was a mistake (they didn't follow the rules), if it's causing an immediate and severe economic hardship, or if returning the asset will actually help you pay off your tax debt faster.

Think of it like this: a release is a ceasefire, while a return is the IRS giving back captured territory. Most of the time, we're fighting for a release so you can breathe and work out a permanent solution.

Do I Still Get My 30-Day Notice If I Move?

The IRS is legally required to send the Final Notice of Intent to Levy to your last known address. This is a specific term that means the address on your most recently filed and processed tax return.

If you move and don't tell the IRS—either by filing a return with your new address or submitting Form 8822, Change of Address—that final notice will go to your old place. Legally, the IRS can consider it delivered even if it's sitting in your old mailbox.

This means the 30-day clock to appeal starts ticking whether you know about it or not. It's entirely your responsibility to keep your address current with the IRS. Failing to do so can cause you to lose your appeal rights and get hit with a levy completely out of the blue.

Navigating the complexities of an IRS levy can feel overwhelming, but you don't have to face it alone. At Attorney Stephen A Weisberg, we begin with a FREE Tax Debt Analysis to understand your unique situation and determine the best path forward before you ever pay a fee.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034