IRS Lien vs Levy What You Need to Know

When you boil it all down, the difference between a tax lien and a tax levy is simple: a lien is a claim, but a levy is an action.

The IRS files a lien to secure its legal interest in your property when you have unpaid taxes. It’s essentially a public declaration that you owe the government money.

A levy, on the other hand, is the actual seizure of that property to settle the debt. Think of a lien as a warning sign planted on your assets; a levy is the government showing up to take them.

If you're facing IRS collection efforts, truly understanding the distinction between a lien and a levy is your first critical step toward finding a way out. While both are powerful tools the IRS uses to collect tax debt, their impact on your financial health couldn't be more different.

A tax lien is a public record that gives the government a legal claim to your property as security for what you owe. In contrast, a levy isn't made public, but it's far more severe. It gives the IRS the power to take your property—like cleaning out your bank account or garnishing your wages—to pay your tax bill.

To help clarify these core concepts, here's a quick comparison of the key differences between an IRS tax lien and a tax levy.

Quick Comparison Lien vs Levy at a Glance

| Attribute | Tax Lien | Tax Levy |

|---|---|---|

| Primary Function | A legal claim against your property to secure a debt. | The actual seizure of your property to pay a debt. |

| Impact on Property | You keep possession of your property. | The IRS takes possession of your property or funds. |

| Public Record | Yes, it is a public record that can damage your credit. | No, it is a private action between you and the IRS. |

| Urgency | A serious warning that demands a response. | An immediate and critical threat to your assets. |

Seeing it laid out like this really highlights the escalation from one to the other.

Navigating the dense language of these legal documents can be overwhelming for anyone. Sometimes, applying strategies to simplify legal documents for small businesses can bring much-needed clarity to the situation.

The lien is the foundational step; it’s the government saying, “You owe us money, and we have a right to your property.” The levy is the enforcement of that right—the moment the IRS acts on its claim.

It's absolutely crucial to resolve a lien before it escalates into a levy. If you’ve already received a Notice of Federal Tax Lien, you should check out our guide on how to remove tax lien for next steps.

How an IRS Tax Lien Impacts Your Financial Life

An IRS tax lien is so much more than a quiet disagreement between you and the government. It’s a public announcement of your debt, and it carries some serious and long-lasting financial weight.

Once the IRS files a Notice of Federal Tax Lien, your debt becomes a public record. This puts everyone—lenders, potential business partners, credit bureaus—on notice that the government has a claim against you.

The most immediate sting for many people is the blow to their financial reputation. While a tax levy involves the actual seizure of assets, a lien is the legal claim that paves the way for it.

The lien itself doesn't take your property, but because it’s publicly filed, it shows up on your credit report and can seriously torpedo your chances of getting a loan or refinancing a mortgage. You can get more background on the specific roles of liens and levies from TurboTax's website.

Your Assets Become Encumbered

A federal tax lien is incredibly far-reaching, attaching itself to all your current and future assets. Think about that for a second. It covers your home, your car, your business property, and even your financial accounts.

This legal claim essentially "encumbers" your property, making it a nightmare to sell or transfer anything without dealing with the IRS first.

Let’s say you want to sell your house. That tax lien has to be paid off from the sale proceeds before you see a dime. This can completely derail the sale or, at the very least, take a massive bite out of your profit. The same logic applies if you try to refinance your mortgage—most lenders won’t touch a property that already has a government claim on it.

A tax lien acts like a legal "cloud" hanging over your property. It doesn't mean you no longer own it, but it casts a shadow over nearly every financial move you try to make, from selling a car to getting a business loan.

Understanding Superpriority and Future Assets

One of the most potent features of a federal tax lien is its "superpriority" status. This isn’t just jargon; it means the IRS gets to cut to the front of the line to get paid, often ahead of other creditors who may have had a claim long before the tax lien was ever filed. This superpriority gives the government a rock-solid position.

And it doesn't stop with the assets you have today. The lien automatically latches onto any property you get your hands on as long as the debt is outstanding. This includes:

Future real estate purchases: Buy a new property, and the lien instantly attaches to it.

Inheritances: If you inherit money or property, the IRS's claim extends to that, too.

Business assets: As your business grows and acquires new equipment or inventory, the lien grows with it.

This forward-looking power is what keeps the pressure on. It makes it incredibly difficult to rebuild your financial life or plan for the future until you finally resolve the underlying tax debt.

What Happens When the IRS Issues a Tax Levy

If a tax lien is a warning shot across the bow, a tax levy is the IRS actively seizing your ship. This isn't just a passive claim against your property; it’s a direct, aggressive action to take what you own to cover your tax debt. In the lien vs. levy discussion, this distinction is everything. A levy means things have escalated, and you need to act immediately.

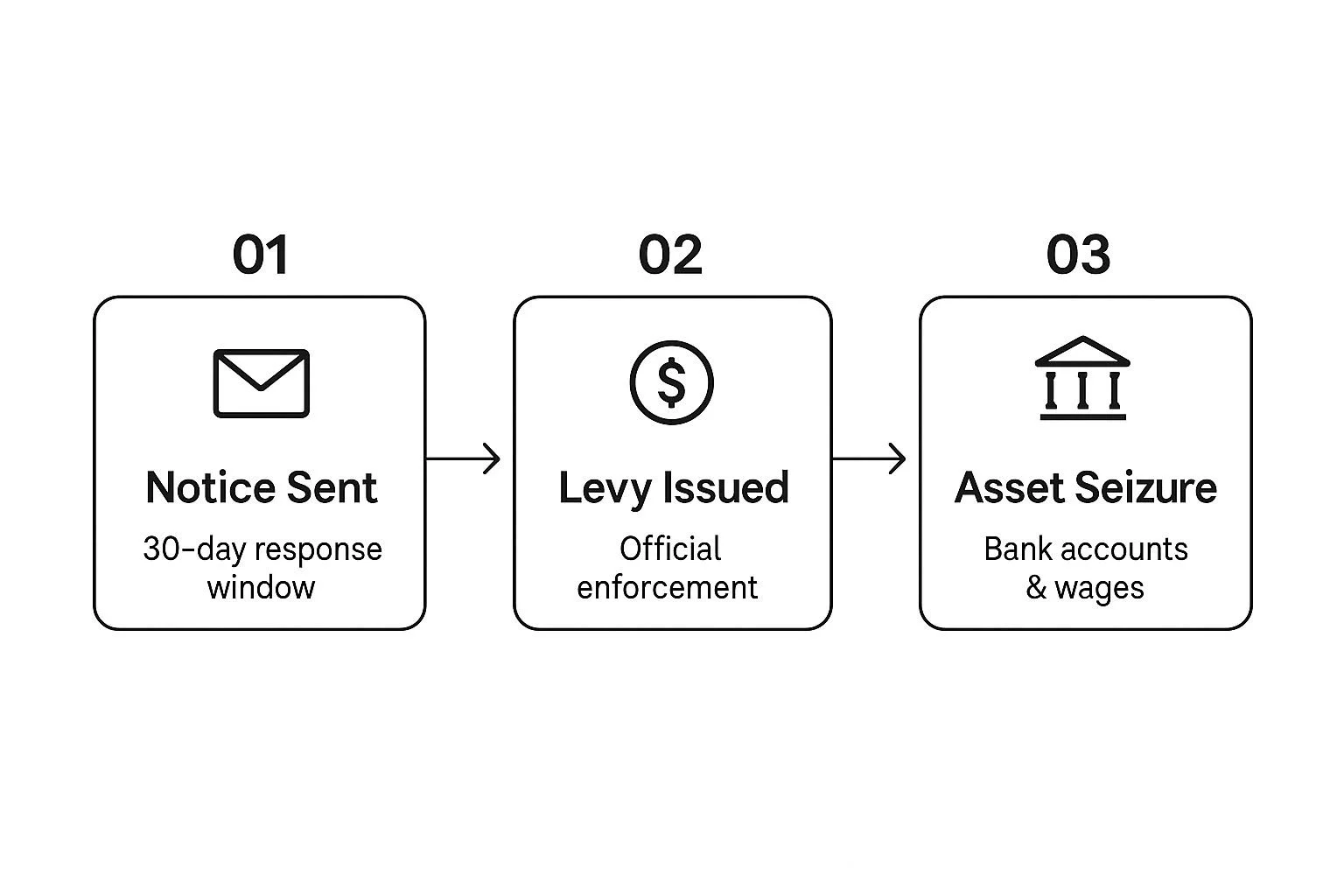

The whole process usually kicks off after you’ve ignored previous notices. The final step is a letter called Final Notice of Intent to Levy and Notice of Your Right to a Hearing.

This is your last official warning. It gives you 30 days to figure things out before the IRS can start taking your assets. Getting a handle on this timeline is critical, and you can dive deeper into what to do by checking out our ultimate guide for taxpayers who have received an IRS levy notice.

Assets Subject to Seizure

Once that 30-day window slams shut, the IRS has startlingly broad authority to seize your property. A levy feels much more immediate and disruptive than a lien because it directly hits the cash and assets you rely on every single day.

Here are the assets most commonly targeted:

Bank Accounts: The IRS can levy your checking and savings. When they do, your bank is legally required to freeze the account for 21 days before handing the funds over.

Wages and Income: A continuous wage garnishment is one of the most frequent types of levies. Your employer will be ordered to send a chunk of every paycheck straight to the IRS.

Retirement Accounts: Don't assume your retirement is safe. Funds in a 401(k) or IRA can absolutely be targeted.

Physical Property: In more severe situations, the IRS can seize and sell physical assets like your car, boat, or even your house. Thankfully, seizing a primary residence is rare and requires a court order to proceed.

A tax levy moves beyond a legal claim on paper and becomes a tangible event that can drain your bank account overnight or reduce your take-home pay significantly. It is the government’s most powerful collection tool, designed to force compliance when all other methods have failed.

Understanding Exemptions and Urgency

While the IRS’s power to levy is extensive, they can't take absolutely everything. Federal law protects certain property from seizure to ensure a taxpayer isn't left completely destitute.

Some of the key exemptions include:

A portion of your wages, calculated based on your filing status and number of dependents.

Certain unemployment and workers' compensation benefits.

Undelivered mail.

Basic necessities like essential clothing, fuel, and provisions.

School books and a certain value of tools you need for your job or business.

But don't get too comfortable—these exemptions are quite limited. The hard truth is that a levy can be financially devastating. It’s the clearest possible signal that your time for negotiation is running out. If you fail to act now, your assets will be forcibly collected.

Comparing the Legal Timelines for Liens and Levies

It’s one thing to understand the definitions of a lien and a levy. It’s another thing entirely to know how each one plays out in the real world. This is where the power shifts back to you. The IRS can’t just do whatever it wants; it has to follow strict legal procedures and timelines before taking action against you.

Those timelines are your window of opportunity. While both a lien and a levy are born from the same problem—unpaid taxes—their legal journeys are very different.

The path to a tax lien starts quietly. After the IRS figures out what you owe (the assessment), they’ll send you a bill called a Notice and Demand for Payment.

If that bill goes unpaid, a "statutory lien" automatically pops into existence, giving the government a legal claim to your property behind the scenes.

To make that claim public and have it impact your credit, the IRS files a Notice of Federal Tax Lien (NFTL). That’s when it becomes a real headache for your financial life.

The Levy Process: A Faster Escalation

The timeline for a levy feels much more aggressive because it is. This isn't just a claim on paper anymore; a levy is the IRS actively moving to take your property. It’s a serious escalation designed to force payment when all other attempts have failed.

Before the IRS can start garnishing your wages or clearing out your bank account, they must send a Final Notice of Intent to Levy and Notice of Your Right to a Hearing. This critical notice gives you at least 30 days to respond.

A levy is almost always the government's last resort, used only after a lien has been filed and other collection notices have been ignored. You can find more detail on the IRS approach by reviewing their official guidance on tax collection.

The infographic below shows just how direct and fast this process is once the IRS decides to levy your assets.

As you can see, once that final notice goes out, the clock starts ticking. That 30-day window is your last, best chance to act before seizure begins.

Key Procedural Differences and Your Rights

The single most important difference between the lien and levy timelines is your opportunity for a formal hearing. Both the filing of an NFTL and a Final Notice of Intent to Levy give you the right to request a Collection Due Process (CDP) hearing.

A CDP hearing is your formal chance to appeal the IRS collection action. It puts a temporary hold on everything, giving you a crucial opening to negotiate alternatives like an installment plan or an Offer in Compromise.

This is a powerful right that shouldn't be overlooked. The table below breaks down the procedural steps side-by-side so you can see the critical differences.

Procedural Timeline: Lien vs. Levy

This table compares the step-by-step notification process the IRS must follow for both a lien and a levy. Notice the key differences in timing and consequences.

| Procedural Step | Tax Lien | Tax Levy |

|---|---|---|

| Initial Notice | Notice and Demand for Payment (CP14) | Notice and Demand for Payment (CP14) |

| Warning Notice | Letter 3172 (Notice of Federal Tax Lien Filing and Your Right to a Hearing) | Letter 1058/LT11 (Final Notice of Intent to Levy and Notice of Your Right to a Hearing) |

| Response Window | 30 days to request a CDP hearing after the lien is filed. | 30 days to request a CDP hearing before the levy can begin. |

| Key Consequence | Public record is created, damaging credit and encumbering property. | IRS can begin seizing wages, bank accounts, and other assets. |

The takeaway here is all about timing. With a lien, the notice about your hearing rights arrives after the damage to your public record is already done. With a levy, that notice is a final warning shot that arrives before the seizure, giving you a brief but critical chance to stop it.

Actionable Strategies to Resolve Tax Liens and Levies

Getting a notice about an IRS lien or levy is daunting, to say the least. But the absolute worst thing you can do is nothing. The real work begins when you shift from just understanding the problem to actively solving it.

Fortunately, there are several proven strategies to get your tax debt under control, stop the IRS’s aggressive collection tactics, and start rebuilding your financial standing.

The simplest, most direct route is to pay the debt in full. It's the cleanest way to get both a lien and a levy lifted. Once you satisfy the entire tax bill—including all the interest and penalties that have piled up—the IRS is required to release its claim on your property.

This isn't just a U.S. tax concept; it’s a fundamental principle in tax enforcement around the world.

Negotiating a Path Forward

Of course, writing a check for the full amount isn't realistic for everyone. When it's not, proactive negotiation becomes your most powerful tool. The IRS actually has several programs designed specifically for taxpayers who can't pay their entire balance at once.

Installment Agreement: This is probably the most common solution. You work out a deal with the IRS to make manageable monthly payments over a set period, often up to 72 months. Once this formal agreement is in place, it will stop an active levy and prevent new ones from being issued, as long as you keep up with your payments.

Offer in Compromise (OIC): An OIC is an agreement that allows certain taxpayers to settle their tax debt for less than the total amount they owe. To qualify, the IRS takes a hard look at your ability to pay, factoring in your income, expenses, and the value of your assets. If your offer is accepted, the lien can be withdrawn after you’ve met the terms of the deal.

To move forward with these options, you’ll have to file the right paperwork. It helps to get familiar with the required documents beforehand; you can access relevant IRS tax forms to see what's involved.

Resolving a tax issue is rarely about a single grand gesture. It's about taking a calculated, strategic step—like setting up a payment plan or negotiating a settlement—that halts the immediate threat and puts you back in control of your financial future.

For those whose situations are more complex, it’s smart to explore a professional tailored to your specific circumstances.

Specialized Solutions for Property Liens

What happens when a tax lien throws a wrench into a real estate deal? You have two very specific, powerful options: a discharge or a subordination. It’s critical to know which one you need.

A lien discharge removes the federal tax lien from one particular piece of property. You'll see this most often when someone needs to sell their home. The IRS agrees to "discharge" its lien, which lets the sale go through. In return, the IRS typically gets the net proceeds from the sale to put toward your tax bill.

A lien subordination, however, works differently. It doesn’t remove the lien. Instead, it lets another creditor (like a mortgage lender) jump ahead of the IRS in the repayment line.

This is crucial if you're trying to refinance. Lenders almost always refuse to fund a new loan unless they have first priority, and subordination is what makes that possible.

How IRS Enforcement Strategies Have Evolved

To really understand the difference between a lien and a levy, it helps to look at how the IRS operates in the real world. Their enforcement playbook isn't static; it changes with new policies, technologies, and priorities.

While the threat of a lien or levy is always a serious matter, the data shows the agency has become much smarter and more strategic in how it collects unpaid taxes.

You might assume the IRS is always ramping up its enforcement, but that’s not the full story. There have been clear periods where the agency deliberately pulled back on aggressive actions while actually getting better at collecting what it was owed.

This tells us they've moved away from a brute-force approach of slapping liens and levies on everyone and are now focusing on more efficient collection methods.

A Shift Toward Targeted Enforcement

The numbers paint a really interesting picture. Between the 2010 and 2014 fiscal years, the number of new liens filed by the IRS plummeted by roughly 50%. Levies saw a similar drop, falling by 45%.

Now, you’d think that would mean less money collected, right? Wrong. During that same period, the percentage of collectible dollars the IRS successfully recovered actually ticked up, from 6.0% to 6.4%. You can dig into these stats yourself in the National Taxpayer Advocate’s analysis of IRS collection performance.

What does this mean for you as a taxpayer? It signals that the IRS is prioritizing efficiency. They've realized that working with taxpayers through solutions like an Installment Agreement or an Offer in Compromise is often more effective than just seizing property outright.

Frankly, this evolution is a good thing for taxpayers. It means that while a lien or levy is still a powerful and very real threat, it’s not always the first or only move the IRS will make.

Their modern strategy often leaves the door open for negotiation and structured payment plans, giving you a real chance to resolve your tax debt without facing the most severe consequences.

Answering Your Top Questions About Liens and Levies

When you're dealing with IRS collection actions, a lot of very specific and frankly, scary, questions pop into your head. Getting straight answers is the first step to feeling in control. Let's tackle some of the most common worries taxpayers have about liens and levies.

Can the IRS Really Take My House?

This is probably the biggest fear for most people. While the IRS can place a lien on your primary residence, actually seizing it (a levy) is extremely rare. It's a complicated legal process for them.

A lien simply secures the government's interest in your property. If you sell or refinance, the IRS gets its cut first. Actually taking your home requires court approval and is an absolute last resort, typically reserved for only the most severe cases of non-compliance.

How Long Does a Tax Lien Stay on My Credit Report?

This is a point of frequent confusion, but there’s some good news here. Since 2018, the three major credit bureaus—Equifax, Experian, and TransUnion—have completely removed tax liens from consumer credit reports.

So, while the Notice of Federal Tax Lien is still a public record that mortgage lenders and other creditors can find, it won't show up on your standard report or drag your credit score down directly.

The most critical takeaway is that while a lien won't hurt your credit score, it remains a public claim that can still block you from selling property or getting new loans until the debt is resolved.

Can the IRS Levy My Social Security Benefits?

Unfortunately, yes. The IRS has the legal power to garnish a portion of your Social Security benefits to satisfy a tax debt.

Through something called the Federal Payment Levy Program (FPLP), the IRS can automatically take up to 15% of your monthly benefit payment.

There are some exemptions for low-income individuals, but this isn't automatic—you have to proactively apply and prove you qualify.

Knowing your options is everything. If you're overwhelmed by tax debt, it's worth exploring the different ways you can settle IRS debt to find a resolution that works for you.

Facing an IRS issue can feel overwhelming, but you don't have to handle it alone. Attorney Stephen A. Weisberg offers a FREE Tax Debt Analysis to determine the best strategy for your specific situation before you ever pay a fee. Start your free analysis today.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034