Trust Fund Penalty Abatement – Protect Your Assets Today

When a business falls behind on payroll taxes, the IRS can get personal. Really personal. Trust fund penalty abatement is the formal process you go through to ask the IRS to cancel a devastating personal penalty that they've assessed against you for those unpaid business taxes.

Winning an abatement case isn't easy. It comes down to proving one of two things: either you weren’t a “responsible person” with the authority to make tax payments, or you didn't “willfully” fail to pay them. To succeed, you need a rock-solid appeal that clearly shows you lacked the control or the specific intent the IRS requires to apply the penalty.

What Is the Trust Fund Recovery Penalty?

When a business withholds taxes from an employee's paycheck—like federal income tax, Social Security, and Medicare—that money doesn't belong to the company. Not for a single second. The business is merely a temporary custodian, holding those funds in trust for the employee and the U.S. Treasury.

The Trust Fund Recovery Penalty (TFRP) is the IRS’s hammer for when that trust is broken. If a business fails to hand over those withheld funds, the TFRP allows the IRS to smash through the corporate veil of an LLC or corporation and hold key individuals personally liable for the entire unpaid amount.

This isn't just another business debt; it becomes your personal debt, one that can haunt you long after the company doors have closed for good.

The Components of Trust Fund Taxes

So, what exactly makes up these "trust fund" taxes? It's crucial to understand which specific parts of payroll tax fall under this category, as the TFRP only applies to them.

Here’s a breakdown of the key components:

| Tax Component | Description | Subject to TFRP? |

|---|---|---|

| Federal Income Tax Withholding | Money withheld from an employee's wages for their personal income tax liability. | Yes |

| Employee's Share of FICA | The employee's portion of Social Security and Medicare taxes withheld from their check. | Yes |

| Employer's Share of FICA | The matching portion of Social Security and Medicare taxes paid by the employer. | No |

| Federal Unemployment Tax (FUTA) | A tax paid solely by the employer to fund unemployment benefits. | No |

As you can see, the TFRP is laser-focused on the money that was actually withheld from employees' paychecks. The IRS doesn't hold individuals personally responsible for the taxes the business was supposed to pay from its own funds.

The Sacred Trust Analogy

Let's make this simple. Imagine you give your friend $100 to hold and deliver to a local charity on your behalf. But instead of passing it on, your friend uses that cash to pay their own power bill. That money was never theirs to spend; they were just holding it in trust for the charity.

The IRS sees payroll taxes in exactly the same light. When a business owner, bookkeeper, or anyone with financial control uses withheld tax money to pay other company bills—like rent, suppliers, or even their own salary—they've betrayed that trust.

The TFRP is the direct result of that broken promise. The IRS basically says, "The business didn't pay us the money it held for us, so we're collecting it from the person who decided to spend it elsewhere." This is why understanding this penalty and the potential for trust fund penalty abatement is so critical.

Why the IRS Pursues These Taxes So Aggressively

The entire federal government runs on the reliable flow of payroll taxes. These funds are the lifeblood of massive programs like Social Security and Medicare.

When businesses fail to remit them, it blows a huge hole in the national budget. Because of this, the IRS collection of trust fund taxes is one of its highest priorities, taking precedence over almost any other tax debt.

The penalty is intentionally severe to scare people into compliance. The TFRP is usually a 100% penalty, which means the individual targeted can be held personally liable for every single dollar of the unpaid trust fund taxes. As the IRS itself explains, the penalty equals the total unpaid withheld income taxes plus the employee's share of FICA taxes.

The key takeaway is that the TFRP is not a punishment for a business's failure. It is a mechanism to collect the actual tax dollars that were withheld from employees but never turned over to the government.

This distinction is everything. It’s why the TFRP is notoriously difficult to discharge in bankruptcy and why the IRS can go after your personal assets—your home, your savings, and your future income. In their eyes, the logic is simple: you were holding their money, and you spent it. Now you have to pay it back. Personally.

How the IRS Determines Responsibility and Willfulness

If you’re facing a Trust Fund Recovery Penalty (TFRP), your entire defense rests on disproving two key things the IRS needs to establish: that you were a “responsible person” and that your failure to pay was “willful.” These aren't just suggestions; they are the legal pillars the IRS must build its case on.

To have any hope of getting a penalty abatement, you have to understand how the IRS thinks about these concepts. They look right past job titles and org charts to find out who really held the financial reins. Your job is to show them you don't meet at least one of their definitions.

Defining a Responsible Person

The term “responsible person” trips a lot of people up. It has absolutely nothing to do with your job performance or your official title. In the world of the IRS, "responsibility" is all about one thing: control over the company's money.

You're considered responsible if you had the power to decide which bills got paid and when. It’s about who had the authority to direct funds. This could be an owner, a director, an officer, or even a bookkeeper with significant financial say-so.

So, how does the IRS pinpoint these individuals? They investigate several factors:

Check-Signing Authority: Can you sign checks on the company’s accounts, especially the main operating account?

Financial Decision-Making: Were you in the room when decisions were made about which creditors to pay? Critically, did you have the power to pay the IRS, even if someone else told you not to?

Control Over Payroll: Did you oversee the payroll process and have the ability to disburse those funds?

Hiring and Firing Power: Could you hire or fire people, particularly in accounting or financial roles?

Keep in mind, there can be more than one responsible person. The IRS isn't shy about assessing the TFRP against multiple people for the very same tax debt.

A Tale of Two Financial Roles

Let's paint a picture. Imagine a business with a CFO and an office manager who handles the mechanics of payroll.

The CFO: He has signature authority on every bank account. He negotiates with suppliers and has the final say on which bills get paid when cash is tight. The owner pulls him aside and says, "We have to make payroll. Pay the employees and our biggest supplier, but we'll have to wait on the IRS." The CFO does as he's told.

The Office Manager: She takes the payroll data from HR, prints the physical checks, and gives them to the CFO to sign. She has zero authority to issue a payment on her own.

In this scenario, the CFO is clearly a responsible person. He had the power and made a conscious choice to pay other creditors instead of the IRS. The office manager? She almost certainly isn't. She was simply following direct orders and lacked any real power to pay the taxes herself.

The IRS focuses on the locus of control. It’s not about who physically prints the check, but who has the ultimate say-so over the funds in the company's bank account.

Decoding Willfulness

Once the IRS decides you’re a responsible person, they still have to prove your actions were “willful.” This is another word that causes a ton of confusion. "Willfulness" here doesn't mean you had some evil plan to defraud the government.

It's much simpler than that.

Willfulness is the act of knowingly, consciously, and voluntarily paying other creditors when you knew—or should have known—that the trust fund taxes were outstanding.

This standard also includes "reckless disregard." If you suspected the taxes weren't being paid but you chose to look the other way and not ask questions, the IRS can find you willful.

Intentionally burying your head in the sand is no defense. This is where the fundamental role of accounting records becomes so critical; the paper trail often tells the whole story.

At the end of the day, if someone with financial authority chooses to pay any other bill—rent, a vendor, or even just the employees' net paychecks—before sending the withheld taxes to the IRS, that decision is considered willful.

Navigating the Trust Fund Penalty Abatement Process

Getting a notice from the IRS about a proposed Trust Fund Recovery Penalty (TFRP) is enough to make anyone’s heart stop. This letter, usually an IRS Letter 1153, is more than just a piece of mail; it's the starting gun for a very serious process.

The moment you open that letter, a 60-day clock starts ticking. That’s how long you have to formally protest the assessment. If you miss that deadline, your chance to appeal vanishes, and the penalty becomes a real, collectible debt.

This isn't just a bill—it's the IRS formally accusing you of being a "responsible person" who "willfully" failed to pay critical taxes. Your mission over the next two months is to build a rock-solid case proving you weren't.

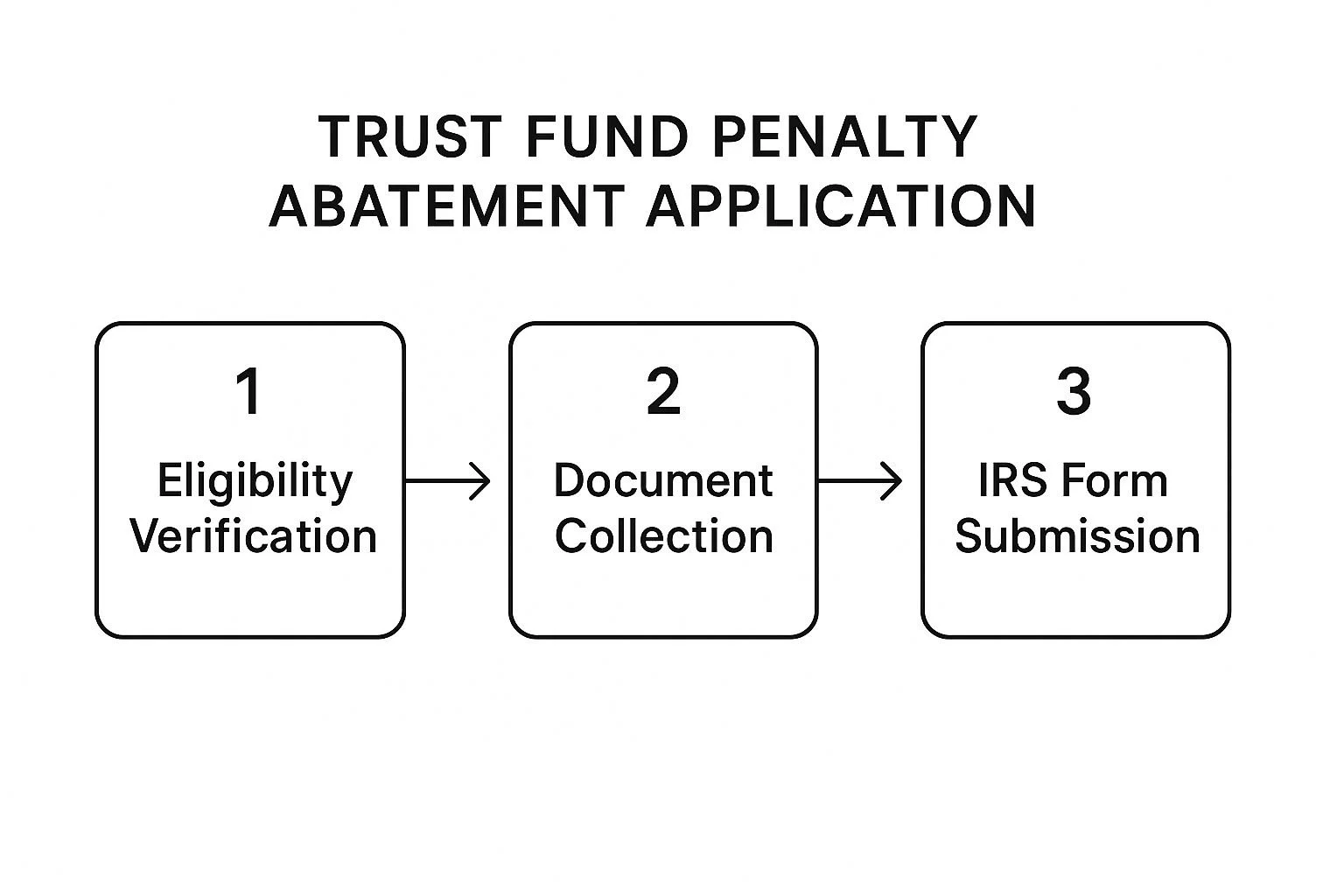

The Initial Response and Critical Interview

Your first move is to draft a formal protest letter to the IRS. This isn't a simple note; it's a legal document that officially states your disagreement and requests a conference with the IRS Independent Office of Appeals. This is how you get your side of the story on the record.

But the real make-or-break moment comes next: the Form 4180 interview. This is not a friendly chat. It's a formal investigation where an IRS Revenue Officer will grill you with questions directly from Form 4180, the "Report of Interview with Individual Relative to Trust Fund Recovery Penalty."

The entire point is for them to gather facts that lock you into the legal definitions of "responsible" and "willful."

Your answers are recorded and become a permanent part of your case file. If you go in unprepared or give inconsistent answers, you could sink your case before it even starts. You absolutely must be ready to clearly explain your role, duties, and—most importantly—the limits of your financial authority.

Gathering Your Evidence

A powerful protest needs more than just your word against theirs. It needs a foundation of hard evidence. Your goal is to create a paper trail proving you either didn't have the authority to pay the taxes or that your failure to do so wasn't willful.

Start digging for these essential documents:

Corporate Documents: Pull out the articles of incorporation, bylaws, and any shareholder agreements. These documents officially define the duties and power of officers and managers.

Bank Records: Bank signature cards are gold. They show exactly who had the legal authority to sign checks and move company funds. Bank statements can also reveal who was actually signing the checks.

Meeting Minutes: Any notes from board or shareholder meetings can be crucial. They often show who was calling the shots on financial matters and giving orders about which bills to pay.

Internal Communications: Don't overlook emails, memos, or even text messages. An email from a partner or superior telling you to pay a supplier instead of the IRS is a slam-dunk piece of evidence to disprove willfulness.

This image breaks down the key phases you'll go through.

As you can see, it's a multi-stage journey. A successful outcome really hinges on being methodical from the very beginning to the final decision.

Writing a Persuasive Formal Protest

Your formal protest letter is where you lay out your argument. It needs to be structured, professional, and persuasive, presenting the facts of your case logically. This isn't the place for emotional appeals; it's for a clear, evidence-based takedown of the IRS's position.

Your letter should directly address why you don't meet the legal test for the penalty. For instance, if you're arguing you weren't a responsible person, state it clearly and then point to the evidence—like the corporate bylaws or the fact you couldn't sign checks. If you're arguing against willfulness, you might explain you were kept in the dark about the unpaid taxes and provide documents showing your lack of access to financial reports.

Key Takeaway: The whole point of your protest is to make it incredibly easy for the IRS appeals officer to follow your logic and see how your evidence directly contradicts their claims that you were "responsible" and "willful."

This is a complicated process with incredibly high stakes. For some people facing overwhelming tax debt, other avenues might be a better fit. When it comes to the TFRP, though, a laser-focused, evidence-backed appeal is your main line of defense.

Building a Winning Argument for Your Appeal

Let's get one thing straight: you won't win a trust fund penalty abatement appeal with a good story or a heartfelt plea. The IRS doesn't operate on emotion; it runs on proof. A successful appeal is built on a mountain of cold, hard evidence.

Your job is to construct a logical, evidence-backed case that systematically proves the IRS was wrong to hold you responsible. This isn't about simply saying, "It wasn't me."

It's about showing them, with documents and records, why you lacked the authority or why your actions weren't willful. Think like a detective building a case—your words lay out the theory, but the evidence is what makes it undeniable.

Proving You Lacked Financial Authority

The cleanest path to getting a penalty removed is to demonstrate you were not a "responsible person." This means proving you didn't have the final word on which bills got paid. Your job title doesn't matter nearly as much as your actual, day-to-day power.

To build this part of your case, you'll need to gather concrete proof:

Corporate Bylaws or Operating Agreements: These official documents are your best friend. They often spell out exactly who has financial authority. If they show your role was hands-off when it came to paying bills, that's a huge point in your favor.

Bank Signature Cards: This is simple but powerful. If you weren't an authorized signatory on the company’s bank accounts, it’s strong evidence you couldn't have paid the taxes even if you wanted to.

Signed Affidavits: A sworn statement from an owner, partner, or even a manager confirming you had no power to decide which creditors to pay can be incredibly persuasive.

Together, these documents paint a clear picture for the IRS agent reviewing your case, showing that you were structurally blocked from making the tax payments.

Arguing Against Willfulness

What if you were a responsible person? Your strategy has to shift. Now, you must prove your failure to pay wasn't willful. This usually means showing you either didn't know about the unpaid taxes or, more commonly, you were explicitly ordered by a superior not to pay them.

Think about a common scenario: the owner tells the bookkeeper, "We have to pay our main supplier or they'll shut us down. The IRS will have to wait." That direct order is your key piece of evidence.

You can use emails, signed memos, or witness testimony to prove your actions were a direct result of following orders, not a choice you made on your own.

Weak Argument: "I didn't want to break the law, but my boss told me to pay other bills first."

Strong, Evidence-Backed Argument: "As you can see in the attached email from CEO John Smith, dated October 15, I was explicitly instructed to prioritize payment to our primary vendor. I had no power to override this directive, which proves my actions were not willful but a direct result of superior orders."

See the difference? One is a claim, the other is a verifiable fact. The IRS is far more likely to grant a trust fund penalty abatement when you present them with irrefutable proof.

Ultimately, your appeal needs to tell one consistent story. Every document, every statement, and every interview should reinforce your central argument.

Real-World Abatement Success Stories

It's one thing to talk about the theory behind a trust fund penalty abatement, but it's another thing entirely to see it work in the real world. Can you actually go up against the IRS when they’ve hit you with a Trust Fund Recovery Penalty (TFRP) and win?

Absolutely. But success never comes easy. It depends entirely on building a rock-solid case backed by undeniable evidence.

These anonymized stories aren't just hypotheticals; they're tangible proof of how people, even those who seem to be squarely in the IRS's crosshairs, can successfully fight back. The key is to systematically dismantle the IRS's arguments about who was "responsible" and whether they acted "willfully."

The Department Head Who Lacked Final Authority

Let's look at the case of a department head at a respectable tech company. His duties included managing his department's budget and approving expenses.

He even had signature authority on a secondary bank account for his team's operational needs. So when the company went under and failed to pay its payroll taxes, the IRS pegged him as a responsible party.

But during his appeal, he successfully proved that while he managed his own little corner of the company, he had zero control or oversight over the main operating accounts or tax compliance.

His winning evidence included:

Company bylaws that explicitly stated only the CEO and CFO had authority over tax matters.

Bank records showing he never once signed a check from the main accounts used to pay taxes.

Email chains where his requests for company-wide financial information were shut down by senior management.

He proved his authority was limited and didn't extend to paying federal taxes. As a result, he wasn't a "responsible person" under the law, and the penalty was completely abated.

The Partner Deceived by a Managing Partner

Here's another situation I see all the time. A non-managing partner in a professional services firm was hit with the TFRP. On paper, he looked guilty—he was an owner with check-signing authority. But his entire defense hinged on proving he wasn't "willful."

He laid out a compelling case showing the managing partner had actively and intentionally hidden the firm's disastrous financial situation. This managing partner had cooked the books, created phony financial reports, and repeatedly lied to the other partners, assuring them all taxes were paid in full.

The heart of his argument was simple: he couldn't have willfully failed to pay a tax debt that he was manipulated into believing didn't exist.

His lack of knowledge, created by another partner's deliberate deception, was the key. This story is a powerful reminder that just being an owner or having your name on the bank account isn't an automatic guilty verdict.

If you were genuinely kept in the dark and didn't act with reckless disregard, you have a strong defense. To learn more, you can dive into the fundamentals of the Trust Fund Recovery Penalty in our detailed guide.

Abatement Success in Complex Cases

Even when the numbers are staggering and the tax law is a tangled mess, these cases can be won. The IRS is aggressive with the TFRP, but history is filled with successful abatements that have saved people millions.

In one notable instance, a corporate officer was assessed a TFRP related to employer Social Security taxes deferred under the CARES Act.

The company had done everything right, paying the employee's share while legally deferring the employer's portion. After the officer left the company, the IRS incorrectly came after them personally for the deferred amount.

With a meticulously argued appeal, and with support from the Taxpayer Advocate Service, the penalty was completely erased, saving the former officer from a devastating multi-million-dollar liability.

As this success story from the Taxpayer Advocate Service shows, even when you're facing down a seemingly impossible assessment, an appeal built on facts and law can lead to a victory.

Answering Your Top Questions About Trust Fund Penalty Abatement

It's completely understandable to have questions when you're staring down a Trust Fund Recovery Penalty (TFRP). The process is complicated and the stakes are high. Let's cut through the noise and answer some of the most pressing concerns people have when trying to get a trust fund penalty abated.

Can I Get Trust Fund Penalty Abatement if My Business Closed?

Yes, absolutely. The fact that your business is no longer operating has no bearing on your ability to fight the penalty.

This is a critical point to understand: The TFRP is a personal liability. The IRS is coming after you, not the defunct business entity. Whether the company was dissolved, sold, or went bankrupt is irrelevant to their case against you personally.

Your entire defense for a trust fund penalty abatement hinges on what happened while the business was still active. The IRS needs to prove two things:

That you were a "responsible person" for collecting and paying the taxes.

And that you "willfully" failed to do so.

Your argument must prove you didn't meet one or both of these legal tests, regardless of what happened to the company later. And don't forget, that 60-day deadline to appeal after you get IRS Letter 1153 is ironclad, whether your business sign is still up or not.

What Happens if My Abatement Request Is Denied?

Getting a "no" from the Revenue Officer or their manager isn't the end of the road. Not by a long shot. It can feel defeating, but you have powerful appeal rights. Your immediate next move is to take your case to the IRS Independent Office of Appeals.

This is your best opportunity for a fair shake. Your case will be reviewed by a neutral Appeals Officer who had nothing to do with the initial denial. They look at the facts with a fresh set of eyes, considering the arguments from both you and the IRS, and they have far more authority to settle cases.

The Office of Appeals can weigh the "hazards of litigation"—the risk that the IRS might lose if the case went to court. This gives them the flexibility to negotiate a settlement or even concede the entire penalty if you present a compelling case.

If Appeals also denies your request, your last resort is the court system. You can sue the government for a refund in either a U.S. District Court or the U.S. Court of Federal Claims. To do this, you first have to pay a small piece of the tax—often just the payroll tax for one employee for one quarter—and then file your lawsuit. A federal judge will then make the final call.

Does Hiring a Tax Professional Improve My Abatement Chances?

While you technically can represent yourself, going up against the IRS in a TFRP case without an experienced tax professional is a massive gamble. Think of it like trying to perform your own surgery. It's not impossible, but the risk of a catastrophic mistake is incredibly high.

Bringing in a seasoned tax attorney or Enrolled Agent who specializes in this area gives you an immediate and significant advantage. Here’s what they bring to the table:

Expert Knowledge: They live and breathe the tax code. They know the nuanced definitions of "responsibility" and "willfulness" and, more importantly, how the IRS applies those definitions in the real world.

Strategic Evidence Building: They know what kind of proof impresses an IRS officer and what gets tossed aside. They’ll help you build a case designed for maximum impact.

Skilled Representation: They handle the crucial Form 4180 interview, steering you away from statements that could sink your case. This alone is worth its weight in gold.

Masterful Negotiation: They are trained negotiators who know how to speak the language of the IRS Appeals Office and frame your arguments in the most persuasive way possible.

The sheer complexity of a trust fund penalty abatement case makes professional guidance essential. The money you invest in an expert is often the single most critical factor in achieving a successful abatement and avoiding a financially crippling personal liability.

Navigating the complexities of a Trust Fund Recovery Penalty appeal requires deep expertise. At Attorney Stephen A Weisberg, I provide a FREE Tax Debt Analysis to determine exactly how I can help you fight the IRS and protect your personal assets. Don't face this challenge alone. Contact me today for a free analysis of your case.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034