A Guide to Self Employed Tax Forms

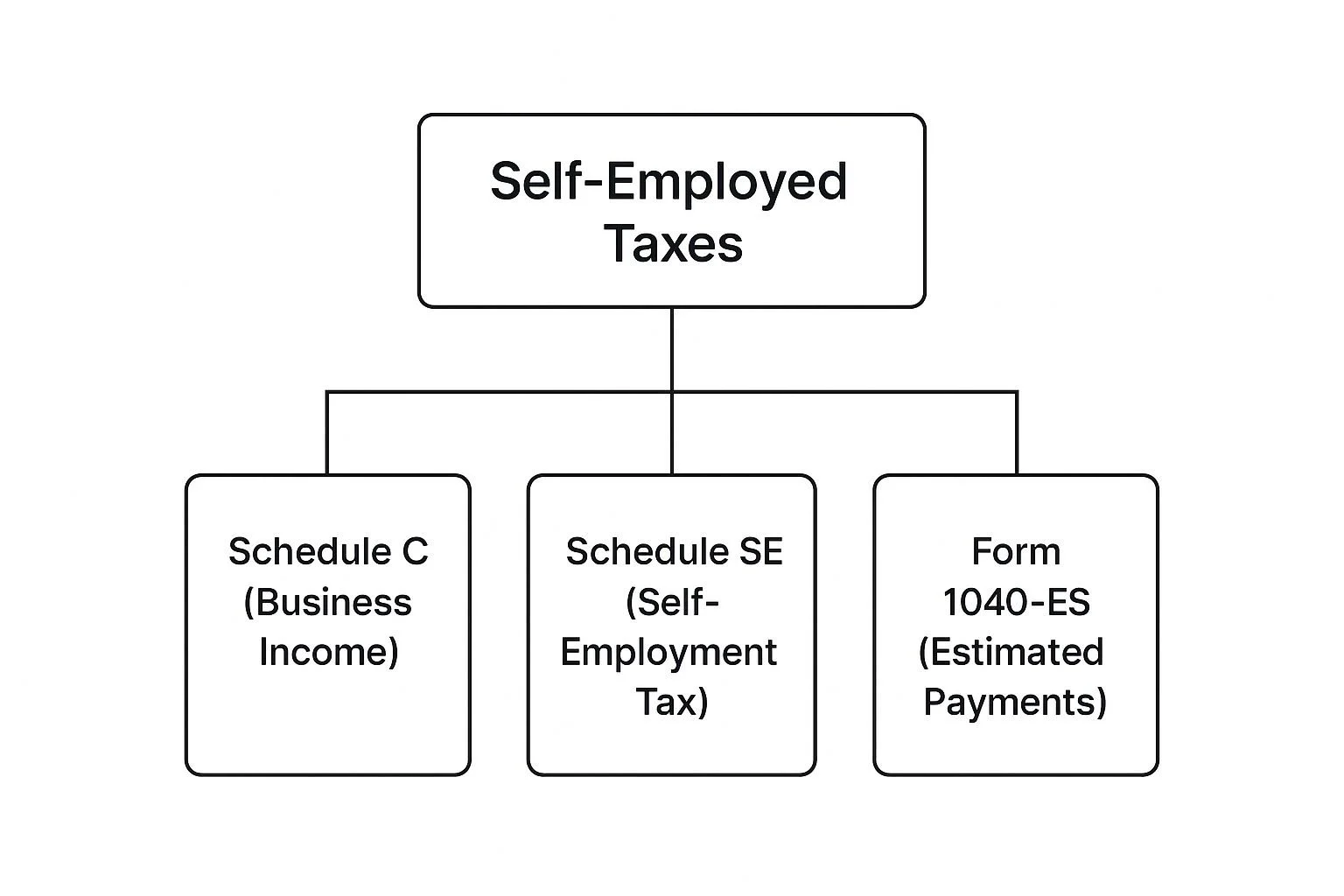

Navigating the world of self employed tax forms can feel like trying to read a map in a foreign language. But once you get the hang of it, you'll see it really comes down to three key documents: Schedule C, Schedule SE, and Form 1040-ES.

Getting these three forms right is the cornerstone of managing your finances and staying on the right side of the IRS. Think of it as your financial game plan for the year.

Your Essential Roadmap to Self Employment Taxes

When you go into business for yourself, you're not just the CEO—you're also the entire accounting department. That means getting comfortable with the paperwork the IRS uses to understand your business's financial story.

It helps to visualize how it all fits together. Imagine your total business income is a river. The various payments you receive (often reported on forms like the 1099-NEC) are the small streams that feed it. Your Schedule C is where you calculate the river's total flow, and your main tax return, Form 1040, is the ocean where everything ultimately ends up.

To give you a quick reference, here are the main players you'll be dealing with.

Core Tax Forms for the Self-Employed at a Glance

| Form Name | Primary Purpose | Filed With |

|---|---|---|

| Schedule C | Reports your business's profit or loss for the year. | Your annual Form 1040 tax return. |

| Schedule SE | Calculates the Social Security & Medicare taxes you owe. | Your annual Form 1040 tax return. |

| Form 1040-ES | Used to pay your income and self-employment taxes quarterly. | Sent directly to the IRS four times a year. |

As you can see, these forms work together to paint a complete picture of your self-employment journey for the IRS.

The Three Pillars of Self-Employment Tax Filing

Your tax responsibilities as a freelancer or business owner rest on three foundational forms. Each one has a specific job to do in reporting your income and figuring out what you owe.

This is how the puzzle pieces connect:

The income you report on Schedule C is the starting point. That number then flows directly to Schedule SE to calculate your self-employment tax, and both of those calculations inform the estimated payments you make with Form 1040-ES.

Understanding Your Core Responsibilities

Let's break down exactly what each of these forms does. They aren't just bureaucratic hoops to jump through; they are the tools you use to accurately report your business's performance.

Schedule C (Profit or Loss from Business): This is your business's income statement for the IRS. You’ll tally up all your gross revenue and then subtract all your legitimate business expenses. The final number is your net profit or loss.

Schedule SE (Self-Employment Tax): Once you have your net profit from Schedule C, you use this form to calculate the taxes you owe for Social Security and Medicare. It’s essentially the self-employed version of the FICA taxes an employer would withhold.

Form 1040-ES (Estimated Tax for Individuals): As a self-employed person, you don't have an employer withholding taxes from a paycheck. This form is how you pay your taxes to the government in four installments throughout the year, preventing a massive bill (and penalties) come April.

The key thing to remember is that these forms are all connected. The result from one directly impacts the next. Your Schedule C profit dictates your Schedule SE tax, and both of those numbers tell you how much to pay with your quarterly 1040-ES vouchers.

Beyond just filing, you'll want to be strategic about lowering your tax bill. A fantastic place to start is by understanding health insurance tax benefits, as this is one of the most significant deductions available to the self-employed.

Tracking Your Income with 1099s and Schedule C

For a self-employed person, tax season really kicks off the moment you start adding up every dollar you made. This whole process starts with a few key income forms and leads directly to the single most important document for any sole proprietor: Schedule C, Profit or Loss from Business.

Think of it like building a financial story for the IRS. Your income forms are the first chapter, setting the scene. Schedule C is the climax, where everything comes together.

Decoding Your Income Reporting Forms

Before you can even touch your main tax return, you have to collect all the "receipts" from your clients and payment apps. These forms show how much they paid you throughout the year, and they're non-negotiable—the IRS gets a copy of them, too. It's how they double-check that you're reporting everything you earned.

You'll mainly be on the lookout for two forms:

Form 1099-NEC (Nonemployee Compensation): This is the bread and butter for most freelancers and contractors. If any single client pays you $600 or more in a year, they are legally required to send one to you and the IRS.

Form 1099-K (Payment Card and Third Party Network Transactions): This one comes from payment processors like PayPal, Stripe, or Square. It reports the total dollar amount of payments they handled for you. The rules and dollar thresholds for this form have been a moving target lately, so always check the specifics for the current tax year.

Here’s a rookie mistake I see all the time: thinking that if you don't get a 1099, the income is off the books. That couldn't be more wrong. You are legally required to report all income, whether it’s on a 1099, a direct deposit, a check, or even cash.

Schedule C: The Heart of Your Business Tax Return

If your 1099s are the ingredients, then Schedule C is the recipe that brings it all together. This one form is a complete snapshot of your business's financial health for the year. Its main job is to figure out your net profit—the money you actually get to keep after subtracting all your business expenses.

That final net profit number is the foundation for almost everything else. It’s what determines how much income tax you pay and what you owe for self-employment taxes.

The process on Schedule C is pretty logical:

Report Gross Income: You start by adding up every single dollar your business brought in from all sources.

Subtract Business Expenses: Then, you deduct the costs of everything that was "ordinary and necessary" to run your business.

Calculate Net Profit (or Loss): What's left over is your taxable business income.

Your gross income on Schedule C needs to be at least the total of all the 1099s you received. The IRS has automated systems that will immediately flag your return if the income you report is less than what your clients reported paying you.

Strategically Claiming Your Business Deductions

The second half of Schedule C is where the magic happens—it’s where you can seriously reduce your tax bill by listing your business expenses. The IRS defines an "ordinary" expense as one that’s common in your line of work, and a "necessary" one as something that's helpful and appropriate for your business.

If you forget to track and claim these deductions, you're just paying taxes on money that was never truly your profit to begin with.

Here are some of the most common expense categories you’ll see on Schedule C, along with some real-world examples:

| Expense Category | Real-World Examples |

|---|---|

| Home Office Use | A percentage of your rent, mortgage interest, utilities, and insurance based on the square footage of your home used exclusively for business. |

| Software & Subscriptions | Your monthly Adobe Creative Cloud fee, accounting software like QuickBooks, or annual dues for a professional group. |

| Business Mileage | The miles you drive to meet a client, run to the office supply store, or attend a conference. You can use the standard mileage rate (e.g., 67 cents per mile in 2024) or track your actual car expenses. |

| Supplies & Equipment | Everyday office supplies like paper and ink, or bigger purchases like a new laptop or camera. Large items might need to be depreciated over time. |

| Professional Services | The money you paid your lawyer to review a contract, your accountant to do your taxes, or a consultant for business advice. |

By carefully tracking and reporting these costs, you make sure the net profit on your Schedule C is an honest reflection of how your business really did. This final number then flows directly to your other self employed tax forms, which we'll get into next.

Calculating Your Tax Bill with Schedule SE and Form 1040

Once you've wrestled with Schedule C and arrived at your net profit, you’ve hit a huge milestone. That final number is the bedrock for figuring out what you actually owe the government. The next step takes you into a couple more self employed tax forms that pin down your specific tax liability.

This is where Schedule SE and your main Form 1040 jump into the ring. Schedule C told you what your business earned; these next forms tell you what you owe on that money. Let's see how these pieces all fit together to give you the final number.

Decoding Your Self-Employment Tax on Schedule SE

Think back to a regular W-2 job. Your employer automatically withholds Social Security and Medicare taxes from your paycheck, and then they pay a matching amount out of their own pocket. This whole bundle is known as FICA tax.

But when you're self-employed, you're wearing both hats—you're the employee and the employer. That means you're on the hook for both halves of those taxes. The form you use to sort this all out is Schedule SE (Self-Employment Tax).

The self-employment tax rate is a flat 15.3% on your net earnings. It’s a combination of 12.4% for Social Security and 2.9% for Medicare. Schedule SE walks you through this math step by step.

It's not quite as simple as just multiplying your Schedule C profit by 15.3%, though. The IRS gives you a small break by letting you apply this tax rate to only 92.35% of your net earnings. This adjustment is meant to level the playing field, since W-2 employees don't pay FICA on their employer's contribution.

So, if your net profit on Schedule C was $60,000, you'd actually start your self-employment tax calculation with $55,410 ($60,000 x 0.9235). It's a small but important detail that trims your overall tax bill.

Important Limits and a Little History

Self-employment tax has come a long way. When it first appeared in 1951, the rate was just 2.25% on the first $3,600 of income—maxing out at a measly $81 tax bill.

Today, the rules are quite a bit different, especially for the Social Security part, which has an annual income limit.

Social Security Limit: For 2024, you only pay the 12.4% Social Security tax on the first $168,600 of your combined earnings (that includes income from both your business and any W-2 jobs).

Medicare Limit: The 2.9% Medicare tax applies to every single dollar of your net earnings, with no income cap.

If you also have a day job where you’ve already paid Social Security taxes, don’t worry—Schedule SE has lines to account for that so you won't overpay. If you've gotten behind on your tax filings, knowing these limits is key.

Bringing It All Together on Form 1040

After all that work on Schedule C and Schedule SE, the final leg of the journey is bringing everything onto your Form 1040. This is the main tax return everyone files, but as a business owner, you're bringing in the results from your business schedules.

Here’s how the numbers flow from your business forms onto your personal return:

Your Net Profit: The net profit you calculated on Schedule C travels over to Schedule 1 (Additional Income and Adjustments to Income), which is part of your Form 1040. This officially mixes your business income with any other income you might have.

Your Self-Employment Tax: The total SE tax you figured out on Schedule SE moves over to Schedule 2 of your Form 1040. This is where it gets added to your regular income tax bill.

A Helpful Deduction: Here's a nice little perk. The IRS lets you deduct one-half of what you paid in self-employment taxes. You claim this deduction on Schedule 1, and it lowers your adjusted gross income (AGI), which in turn lowers your income tax.

By the time you're done, your Form 1040 provides a complete snapshot, merging your business performance with your personal tax situation to land on your final tax due or refund.

Paying Taxes Throughout the Year Using Form 1040-ES

When you work a traditional W-2 job, your taxes are neatly handled for you. Your employer withholds a chunk from each paycheck and sends it straight to the IRS. Easy. But when you're self-employed, you are the employer, which means this job now lands squarely on your plate.

The IRS runs on what's called a "pay-as-you-go" system. They don’t want to wait until April to get their cut of the money you're making right now. This is where one of the most crucial self employed tax forms enters the picture: Form 1040-ES, Estimated Tax for Individuals.

Think of it this way: instead of getting hit with a massive, soul-crushing tax bill once a year, you pay it down in four smaller, more manageable installments. It's a lifesaver for your cash flow and helps you dodge some nasty underpayment penalties.

Estimating Your Annual Income and Tax

So, how do you know what to pay? This is the tricky part. You have to estimate what you'll owe for the whole year. It can feel a bit like reading tea leaves, especially if your income bounces around from month to month, but it's really just an educated guess.

The worksheet that comes with Form 1040-ES will walk you through it. You'll need to make a solid projection of:

Your Expected Adjusted Gross Income (AGI): This is your total estimated business profit for the year, after you subtract key deductions like one-half of your self-employment taxes.

Your Total Tax Liability: Based on your AGI, you'll figure out your expected income tax and self-employment tax.

Your Required Annual Payment: The general rule of thumb is to pay at least 90% of what you'll owe this year, or 100% of the tax you paid last year, whichever is less.

And don't panic if things change. If you land a huge project or have a surprisingly slow quarter, you can just adjust your numbers for the next payment. The IRS just wants to see you're making a good-faith effort.

The Four Key Deadlines for Estimated Taxes

Once you have your annual estimate, you just divide it by four. The hard part is remembering to actually pay it on time. These quarterly deadlines are notorious for tripping up freelancers and new business owners.

And to make things even more confusing, the "quarters" aren't spaced out evenly every three months.

Pro Tip: Seriously, put these dates in your calendar right now with alarms. Missing a deadline can trigger penalties, even if you pay your entire tax bill in full by April 15. The penalty isn't for not paying, it's for not paying on time as you earn.

To keep you on track, here is the official schedule for your Form 1040-ES payments.

Quarterly Estimated Tax Deadlines

This table outlines the payment periods and their corresponding due dates. Sticking to this schedule is key to staying compliant and penalty-free.

Payment PeriodDue DateJanuary 1 – March 31April 15April 1 – May 31June 15June 1 – August 31September 15September 1 – December 31January 15 (of the next year)

Just remember, if a due date ever lands on a weekend or holiday, your payment is due on the very next business day.

How to Make Your Payments Stress-Free

Paying up is easier than ever. You can still go old-school and mail a check with a payment voucher from the Form 1040-ES package, but why would you?

The IRS has several digital payment options. A great one is IRS Direct Pay, which lets you send a secure payment right from your bank account for free.

Here’s the best advice I can give: open a separate savings account just for taxes. Every single time a client pays you, immediately transfer a percentage (say, 25-30%) into that account. When the quarterly deadline rolls around, the money is already sitting there waiting. It turns a dreaded task into a simple, two-minute transfer. No sweat.

Navigating Advanced and Specialized Tax Forms

As your business grows, your tax situation gets more complex. You’re no longer just tracking income and basic expenses. Suddenly, you're buying assets, carving out a home office, or thinking about retirement. That's when you move beyond the basics of Schedule C and SE into more specialized self employed tax forms.

Think of these forms as the specialty tools in your financial workshop. Your Schedule C is the trusty hammer you use for everything, but sometimes you need a precision instrument to get the job done right and maximize your savings.

Claiming Your Home Office with Form 8829

For anyone running a business from home, the home office deduction is one of the best perks out there. While the simplified method (a flat rate per square foot) is easy, it often leaves money on the table.

Enter Form 8829, Expenses for Business Use of Your Home. This is where you can deduct the actual expenses tied to your workspace. Instead of a one-size-fits-all calculation, you’ll tally up a portion of your real home costs, which can lead to a much bigger deduction.

What you can deduct: A percentage of your rent or mortgage interest, utilities, insurance, and even home repairs, all based on the square footage of your office.

Who it's for: This is perfect for renters in pricey cities or homeowners with high utility bills who use a specific, dedicated area for their work.

The keyword from the IRS is exclusive. To qualify, your office has to be just that—an office. It can't double as the family playroom or guest bedroom.

Depreciating Assets with Form 4562

Did you buy a new computer, a work truck, or that fancy piece of equipment you’ve been saving for? You can’t just write off the full cost in one go. For big-ticket items that will last more than a year, you need to use Form 4562, Depreciation and Amortization.

Depreciation is simply the process of spreading the cost of an asset over its useful lifespan. So instead of one huge $30,000 deduction for a new vehicle, you might write off a piece of that cost over the next five years.

This form helps you manage those calculations and even unlocks powerful tools like Section 179 expensing, which can let you deduct the entire cost in the first year under certain rules.

Securing Your Future with Retirement and Health Forms

Being your own boss means you're also in charge of your own benefits. Smart entrepreneurs use tax-advantaged accounts to build for the future while cutting their tax bill today.

SEP IRA or Solo 401(k) Contributions: Putting money into these retirement plans is a fantastic way to lower your taxable income. Every dollar you contribute is a dollar you can deduct, all while building a nest egg. You’ll report these contributions right on Schedule 1 of your Form 1040.

Health Savings Account (HSA) Deductions: If you're on a high-deductible health plan, an HSA is a triple-threat tax-saver. Your contributions are deductible, the money grows tax-free, and withdrawals for medical costs are tax-free. You’ll track your contributions on Form 8889.

It’s also worth remembering that every penny you report on Schedule SE is being tracked by the Social Security Administration, building up your credits for future benefits. You can discover more insights about how the SSA tracks this income on ssa.gov. And if your tax situation ever feels like it's spiraling out of control, know that there are solutions.

Common Questions About Self-Employed Tax Forms

Once you get a handle on the main self-employed tax forms, the "what if" questions usually start popping up. Real life is messy, and your business income rarely fits into a neat little box. This is where people start to get tripped up.

Let's dig into some of the most common scenarios I see in my practice. Think of this as the troubleshooting guide for your tax journey—clear, straightforward answers to help you file with confidence.

What Happens If I Have Both 1099-NEC and Cash Income?

This is probably one of the most frequent situations for freelancers and small business owners. You get official Form 1099-NEC documents from your bigger clients, but you also collect cash, checks, or payments through apps like Zelle or Venmo for smaller jobs.

The rule here is simple and non-negotiable: you must report all income. It doesn't matter how you were paid or if you got a form for it. Your total gross receipts on Schedule C is the grand total of every single dollar your business brought in.

Here's the kicker: the IRS gets a copy of every 1099 with your name on it. Their computers will automatically flag your return if the income you report is less than what your 1099s show. Always start with your 1099 totals as a baseline and add all your other undocumented income on top of that.

Forgetting to report cash is one of the easiest ways to attract unwanted IRS attention and get hit with penalties. Good records are your best friend.

Do I Owe Self-Employment Tax on Small Earnings?

Yes, almost certainly. The threshold for paying self-employment tax is shockingly low, and it catches a lot of people with side hustles by surprise. If you have net earnings of $400 or more from your business activities, you're on the hook for filing a return and paying self-employment tax via Schedule SE.

Notice that $400 threshold applies to your net profit, not gross revenue. That means even one small project that nets you just over this amount triggers the requirement. This is true even if your total income from all sources is so low that you wouldn't otherwise have to file a personal tax return.

Can I Still Deduct Business Expenses If I Don't Make a Profit?

Absolutely. In fact, you must. You should report all your ordinary and necessary business expenses on your Schedule C, even if those deductions push you into a business loss for the year. This is one of the few silver linings when your business has a tough year.

A business loss can often be used to offset other income, like from your W-2 day job or investments, which can seriously lower your overall tax bill.

For example: Let's say you earned $50,000 from your 9-to-5 but your side gig had a $5,000 loss. That loss can reduce your total taxable income to $45,000, potentially saving you hundreds of dollars in taxes.

A word of caution, though. If you report losses year after year, the IRS might start to wonder if you have a real business or just an expensive hobby. The rules for deducting hobby losses are much stricter.

What Is the Difference Between Schedule C and Business Returns?

This all comes down to how your business is legally structured. The forms you use are entirely dependent on the entity type you've chosen.

| Form Type | Who Uses It | How It Works |

|---|---|---|

| Schedule C | Sole proprietors and single-member LLCs. | It's part of your personal Form 1040. Your business profit is your personal income. |

| Form 1065 | Partnerships and multi-member LLCs. | This is a separate business return. Profits are "passed through" to owners via a Schedule K-1. |

| Form 1120-S | S Corporations. | This is also a separate business return. Profits pass through to shareholders on a Schedule K-1. |

This is a separate business return. Profits are "passed through" to owners via a Schedule K-1.Form 1120-SS Corporations.This is also a separate business return. Profits pass through to shareholders on a Schedule K-1.

Choosing your business structure is a huge decision. Schedule C is the default for most people starting out on their own, while partnerships and S Corps involve filing formal business returns. While we're focused on tax here, if you have broader questions, checking out some general financial FAQs can provide helpful context. Knowing these distinctions is critical for staying compliant as your business grows.

At Attorney Stephen A Weisberg, we specialize in helping individuals and business owners navigate complex tax issues with the IRS. If you're facing tax debt, an audit, or other challenges, we start with a FREE Tax Debt Analysis to see exactly how we can help before you ever pay a fee.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034