What Is a State Tax Lien Explained for Taxpayers

When you hear the words "state tax lien," it's easy to picture agents showing up at your door to seize your belongings. But that's not quite how it works.

A state tax lien is essentially the government's legal claim against your property because of unpaid taxes. It’s not about taking your stuff right away.

Instead, think of it as the state putting a giant, official "dibs" on your assets. This claim ensures that if you sell your property, the state gets its cut of the money first, before most other creditors. This legal hold can attach to almost anything you own—your house, your car, even your bank accounts.

Decoding the State Tax Lien

Let’s try a simple analogy. Say you owe a friend a significant amount of money. To make sure they get paid back, they publicly announce to all your other friends, "He owes me money, so I get first claim on his next paycheck." A state tax lien is the legally binding version of that announcement, and it carries a lot more weight.

It’s a formal declaration, filed in public records, that you have an outstanding tax debt. This is usually the first serious step a state takes after its initial letters and payment demands have gone unanswered. A lien doesn't mean they're foreclosing on your house tomorrow, but it does create a massive headache by "clouding" the title to your property.

To get a clearer picture, let's break down the essential components of a state tax lien. This table offers a quick snapshot of what you need to know right away.

State Tax Lien at a Glance Key Concepts

| Concept | Simple Explanation | Key Implication |

|---|---|---|

| Legal Claim | The state's right to your property's value. | It secures the debt without immediate seizure. |

| Public Record | The lien is filed publicly, for all to see. | It severely damages your credit and financial reputation. |

| Priority Status | The state gets paid before most other creditors. | Selling or refinancing property becomes extremely difficult. |

| Broad Attachment | Attaches to all current and future assets. | It's not just about your house; it covers everything. |

This table covers the basics, but the real impact is felt when you try to live your financial life with a lien hanging over your head.

The Lien as a Public Record

The moment a state tax lien is filed, it becomes part of the public record. This is a game-changer. It’s no longer a private matter between you and the tax agency; now, anyone can see it. Banks, lenders, business partners—they all have access.

This public filing has a few immediate and painful consequences:

The state jumps to the front of the line. This lien solidifies the government's place as a priority creditor. If you sell your house, they get paid from the proceeds before your other debts are settled.

It’s an all-encompassing claim. A state tax lien is sticky. It attaches to all the property you own now and can even latch onto assets you acquire in the future, as long as the lien remains active.

Your credit takes a nosedive. Trying to get a new loan, mortgage, or even a credit card with an active tax lien is next to impossible. Lenders see it as a massive red flag.

A state tax lien is fundamentally a security interest. It’s the government’s way of saying, "We are first in line for payment." Ignoring it allows the state to pursue more aggressive collection actions, like a levy, down the road.

Every state has its own playbook for enforcing liens. For example, California’s State Tax Lien Notice attaches to any property you own within the state, giving them powerful leverage. While this article covers the general landscape, remember that a federal lien operates a bit differently.

How a State Tax Lien Gets Filed Against You

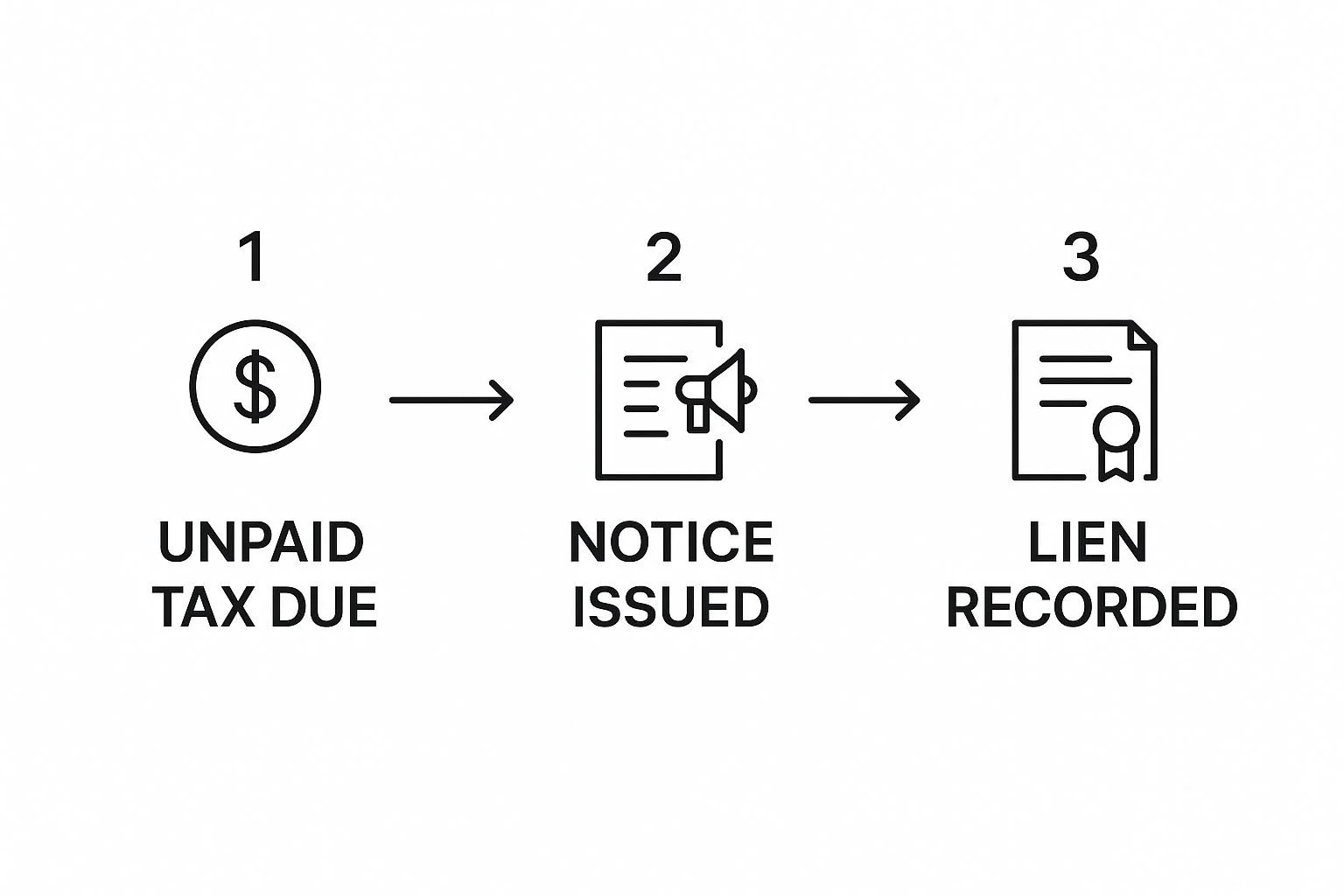

A state tax lien doesn't just appear out of the blue. It’s the final stop on a long, predictable road that starts the moment a tax bill goes unpaid. Knowing the steps in this journey is your best defense because it gives you several chances to step in and fix the problem before a lien ever sees the light of day.

It all kicks off with one thing: a missed or underpaid tax obligation. From there, the state tax agency starts reaching out. These first communications aren't meant to be threatening; they're just official nudges to let you know about the balance and encourage you to pay up. It's when these early warnings are ignored that things start to get serious.

The entire process follows a clear path, moving from simple paper notices to a powerful legal claim against everything you own.

The Initial Assessment and First Notices

The first domino to fall is the state's formal assessment of what you owe. This typically happens after you file a return showing a balance due or when the state’s auditors figure out you owe taxes you never reported. Once that debt is officially recorded, the letters start coming.

You'll first get a bill, usually called something like a "Notice of Tax Due." This document breaks down how much you owe, including the original tax, plus any penalties and interest that are already piling up. It will give you a clear deadline and instructions on how to pay.

If you don't respond to that first notice, you can expect more letters to follow. Each one will sound a little more serious than the last, making it crystal clear that ignoring the problem will lead to bigger consequences.

The Final Warning: The Demand for Payment

After the initial notices have gone unanswered, the state plays its final card before taking formal action: the Demand for Payment. This isn't just another bill in the mail; it's a critical legal step required before a lien can be filed.

This notice clearly states the total amount you owe and warns you that if you don't pay within a short timeframe (usually 10 to 30 days), the state has the right to secure its claim.

Think of the Demand for Payment as your last chance to keep things private. If you pay the debt or call the agency to work out a payment plan at this stage, you can still head off the lien. But if you ignore this final demand, you’re essentially telling the state you have no intention of paying voluntarily. That forces their hand.

The Demand for Payment is the state's last attempt to get you to settle the debt quietly. Once that deadline passes without any action from you, the state is legally cleared to file a public notice of lien and secure its interest in your assets.

This infographic breaks down the simple progression from an unpaid tax bill to a publicly recorded lien.

As you can see, the lien is a direct result of inaction, not some random, unfortunate event.

Making It Official: The Public Filing

Once the grace period on the Demand for Payment is up, the state drafts a document called a "Notice of State Tax Lien." This is the legal paperwork that makes their claim official. To lock it in, they file this notice with the local county office where you live or own property—usually the County Recorder or Clerk of Court.

This simple act of filing has two major, immediate impacts:

Your Debt Becomes Public Knowledge: This is no longer a private matter between you and the tax agency. Anyone—creditors, banks, business partners, even nosy neighbors—can now see that you have a significant tax debt.

The Lien Attaches to Your Property: The lien automatically latches onto all your property in that county, both real estate and personal assets. This puts a "cloud on the title," making it virtually impossible for you to sell or refinance your home or other property until the debt is cleared.

This public filing is what gives the lien its teeth, instantly damaging your credit and freezing your financial flexibility.

The Real-World Impact of a State Tax Lien

A state tax lien isn't just some piece of paper filed away in a dusty government office. It’s a powerful legal claim that sends shockwaves through your entire financial life. Once it’s filed, it becomes public record—a bright red flag for anyone looking into your finances.

Think of it as a heavy anchor dropped on your financial ship. Suddenly, your ability to move forward is severely restricted, and the ripple effects can feel overwhelming almost immediately.

The first domino to fall is usually your creditworthiness. While it’s true that tax liens don’t show up on your personal credit reports from Experian, Equifax, or TransUnion anymore, don't let that fool you.

Lenders, mortgage brokers, and other financial institutions dig deeper. They routinely check public records, and finding a tax lien is a deal-breaker for many of them.

Your Ability to Borrow Money Vanishes

So, you’ve found your dream home and are ready to apply for a mortgage. Or maybe your family needs a more reliable car. With an active tax lien hanging over your head, your chances of getting approved are slim to none.

To a lender, that lien means someone else has a claim to your assets before they do. It screams "high risk."

Even if you find a subprime lender willing to work with you, the terms will be brutal. You can expect:

Sky-high interest rates to make up for the risk they’re taking on.

Harsh borrowing terms, like demanding a massive down payment.

Outright denial for most mainstream loans, credit cards, or lines of credit.

The lien basically tells the financial world you have a history of not paying your debts, making it incredibly difficult to get the funds you need for life’s biggest moments.

Selling or Refinancing Property Becomes a Nightmare

One of the most paralyzing parts of having a tax lien is the "cloud" it puts on your property’s title. This is a legal term, but the effect is very real: you can't give a buyer a "clear title," which is a non-negotiable part of nearly every real estate deal.

Let's say you need to sell your house. As soon as the buyer’s attorney runs a title search, that lien will pop right up. The sale will grind to a halt. No buyer—and certainly no mortgage company—will move forward until your tax debt is paid and the state officially releases the lien.

You’re effectively stuck. Selling is off the table. Refinancing is impossible. Major life plans, like moving for a new job or downsizing for retirement, are put on indefinite hold.

Professional and Business Reputations Suffer

The damage doesn't stop with your personal finances. Because a tax lien is a public document, it can easily spill over into your professional life. Clients, potential business partners, and even professional licensing boards can find it.

This can do serious harm to your reputation and career:

Loss of Professional Licenses: For professions like law, accounting, or real estate, a tax lien can be seen as a sign of financial irresponsibility, putting your license at risk.

Difficulty Securing Business Credit: If you're a business owner, forget about getting a business loan, a line of credit, or good payment terms from suppliers.

Eroded Trust: Partners and investors might see the lien as a sign of poor management, shaking their confidence and damaging crucial business relationships.

The presence of a state tax lien can derail major financial decisions, from buying a home to funding a business. Using a comprehensive due diligence checklist is exactly how potential buyers and lenders uncover these kinds of problems. Ultimately, the impact of a lien goes far beyond the money you owe; it can create widespread financial paralysis.

Comparing State Tax Liens and Federal IRS Liens

When you hear "tax lien," it's easy to lump everything into one big, stressful category. But here’s the thing: a state tax lien and a federal IRS lien are two completely different animals.

While both are legal claims against your property for unpaid taxes, they come from different government bodies and play by an entirely different set of rules. Figuring out who you’re up against—your state’s department of revenue or the IRS—is the absolute first step.

A state tax lien gets filed by, you guessed it, your state’s tax agency for debts like state income tax, sales tax, or franchise tax. An IRS lien, on the other hand, is for federal debts, like your personal income taxes. And yes, it’s entirely possible to be hit with both at the same time.

The Governing Authority and Applicable Laws

The biggest split between these two liens comes down to who’s in charge. A federal tax lien is governed by federal law, meaning the rules are the same whether you’re in Maine or Hawaii. The IRS operates under one consistent legal playbook.

State tax liens are a different beast altogether. They’re governed by the specific laws of that particular state, which means the process, your rights, and the collection tactics can vary wildly from one state line to the next. For instance, the statute of limitations—how long they have to collect the debt—might be 10 years in one state but 20 years just across the border.

This decentralized system is uniquely American. Other parts of the world, like the European Union, often have more centralized tax collection. In the U.S., every state having its own rulebook can make things incredibly confusing. You can get a broader sense of how tax liens work globally on Wikipedia.

Think of it this way: An IRS lien is a federal issue with a national standard. A state lien is a local problem, governed by local rules. Same end goal, but a totally different journey to get there.

Key Differences at a Glance

To really get a handle on this, it helps to see the differences laid out side-by-side. Both liens can attach to your home, your car, and other property, but how they’re placed and how you get them removed are two separate paths.

Let’s break down the core distinctions in a simple table.

State Tax Lien vs Federal IRS Lien Key Differences

This table highlights the crucial differences between a lien from your state and one from the IRS.

| Feature | State Tax Lien | Federal (IRS) Tax Lien |

|---|---|---|

| Issuing Authority | State tax agency (e.g., California Franchise Tax Board) | Internal Revenue Service (IRS) |

| Type of Tax Debt | State income tax, sales tax, employment tax, etc. | Federal income tax, payroll tax, estate tax, etc. |

| Governing Law | Varies significantly by individual state laws | Uniform federal laws apply nationwide |

| Resolution Process | Must negotiate directly with the specific state agency | Must work with the IRS through its established programs |

| Payment Plans | State-specific installment agreements or Offer in Compromise | IRS Fresh Start initiative, installment agreements, OIC |

At the end of the day, you can't solve a state tax problem by talking to the IRS, and you can’t fix an IRS issue by calling your state's tax office. They are two separate problems that demand two separate, tailored solutions.

Your Action Plan for Resolving a State Tax Lien

Finding out a state tax lien has been filed against you can feel like hitting a brick wall. It's paralyzing. But it’s definitely not a dead end.

Instead of freezing up, now is the time to get moving. There are several proven ways to tackle the underlying debt and finally get that lien off your back. The key is to figure out which option actually fits your financial reality. Ignoring it? That’s just asking for more aggressive collection actions later on. A proactive approach is the only way to go.

Think of this as your playbook for taking back control.

Pay the Tax Debt in Full

Let’s start with the most direct route: paying the tax debt in full. It's the cleanest, fastest way to make the problem go away. Doing this immediately stops the clock on any more penalties and interest piling up, putting you on the express lane to getting the lien released.

Once the state tax agency gets your final payment and processes it, they’re legally required to issue a Certificate of Release. They file this document in the same county office where the original lien was recorded. Just like that, it's officially scrubbed from the public record, and the cloud over your property title disappears.

Of course, not everyone can just write a check for the full amount. If that sounds like you, don't sweat it—there are other solid options on the table.

Set Up a State Installment Agreement

If you can't pay it all at once, an installment agreement is often the next best thing. This is basically a formal payment plan you set up with the state tax agency. You agree to pay off your debt through a series of manageable monthly payments over a fixed amount of time.

Every state has its own rules and applications for these plans. Generally, you’ll need to be caught up on all your current tax filings to even qualify.

But getting into an installment agreement is a huge step. It can stop further collection actions and, in some cases, might even get the lien withdrawn from public records before the debt is fully paid off.

Key Takeaway: An installment agreement is your way of showing the state you’re acting in good faith. But you have to stick to it. Missing payments can void the whole deal and put you right back at square one with aggressive collectors.

For a lot of people, this structured plan provides the breathing room they need to steadily chip away at the debt without getting crushed by financial pressure.

Settle for Less with an Offer in Compromise

What happens when the debt is so big that even a payment plan feels impossible? If you’re facing serious financial hardship, you might be a candidate for an Offer in Compromise (OIC). This is a state program that allows certain taxpayers to settle their debt for less—sometimes much less—than the full amount they owe.

Be warned: qualifying for an OIC is tough. It’s an intensive process where you have to lay your financial life bare. You’ll need to provide exhaustive documentation proving you simply don’t have the income or assets to pay what they’re asking. The state will put your finances under a microscope, looking at:

Ability to Pay: Your current income, essential living expenses, and what you could potentially earn.

Asset Equity: They’ll assess the value of your home, cars, bank accounts—everything.

Future Income Potential: They'll make a judgment call on whether your financial situation is likely to improve.

If your offer is accepted and you pay the settled amount, your entire tax liability is wiped clean, and the state releases the lien.

Explore Advanced Lien Resolution Strategies

Beyond these main routes, there are a few more advanced strategies that can help in specific scenarios, especially if you need to sell or refinance a property that’s currently under a lien.

Lien Subordination: This move doesn’t remove the lien, but it cleverly bumps it down the pecking order. Subordination lets another creditor—like your mortgage lender—jump ahead of the state to get paid first. This is a common tactic when you want to refinance your home for a better interest rate, which can free up cash to pay the state back faster.

Discharge of Property: This option completely removes the lien from a single piece of property (like your house) while leaving it attached to your other assets. A state will typically grant this if you're selling the property and the proceeds from the sale will go toward paying down a big chunk of your tax bill.

Navigating these choices can get complicated, and picking the right path for your situation is critical. For a more detailed breakdown of the nuts and bolts, you can read our guide on how to remove a tax lien. Each strategy requires careful thought, but with the right one, you can get this resolved and clear your name.

How to Prevent a State Tax Lien in the Future

The best way to deal with a state tax lien is to make sure one never gets filed against you in the first place. This isn't about complex legal tricks; it's about solid, proactive financial habits. Preventing a lien really comes down to staying organized, planning ahead, and speaking up before a small problem becomes a big one.

Think of it like preventative medicine for your finances. A little bit of care and attention now can save you from a world of hurt later.

Build Strong Financial Habits

Good tax compliance starts with good record-keeping. If you're a freelancer or run a small business, this is an absolute must. You have to track your income and expenses diligently all year long, not just in a mad dash at tax time. Whether you use accounting software or a simple spreadsheet doesn't matter—find a system that works for you and stick with it.

Next, get serious about deadlines. Every state has its own schedule for filing returns and paying estimated taxes. Put these dates on your calendar. Set reminders. Missing a deadline is one of the fastest ways to get on the state's bad side.

A classic mistake for the self-employed is not setting aside money for taxes. A great rule of thumb is to sock away 25-30% of every single payment you receive into a separate bank account. That way, the cash is ready and waiting when tax day rolls around.

Communicate Before It Becomes a Crisis

Look, life happens. A sudden job loss, a medical emergency, or a business hitting a rough patch can make paying your taxes feel impossible. The single worst thing you can do is stick your head in the sand and ignore the problem. State tax agencies are surprisingly willing to work with people who are honest about their struggles.

If you know you're going to have trouble paying, call the agency right away. Don't wait for the scary-looking notices to start piling up in your mailbox.

Explain your situation and ask what your options are. Most states offer things like short-term payment extensions or more formal installment agreements to help you get back on your feet without slapping a lien on you.

Reaching out shows good faith and can stop a manageable issue from exploding into a public financial nightmare. Even if you can't pay anything close to the full amount, you might have other outs. Exploring a settlement like an Offer in Compromise could be an option if you're facing real hardship.

Common Questions About State Tax Liens

When you're staring down a tax problem, the questions and what-ifs can feel overwhelming. A state tax lien, in particular, tends to kick up a lot of confusion and anxiety. Getting straight answers is the first real step toward taking back control.

Let's cut through the jargon and tackle some of the most common questions people have when a state tax lien enters the picture.

How Long Does a State Tax Lien Stay on My Record?

This is usually the first question on everyone's mind, and it's a two-part answer.

First, the lien itself becomes part of the public record. It stays there until you either pay the tax debt in full or the state's time to collect runs out (the statute of limitations). This window varies quite a bit by state, but it's often a long time—think 10 to 20 years.

Second is the credit report issue. A few years ago, the major credit bureaus (Experian, Equifax, and TransUnion) stopped including tax liens on personal credit reports. That's good news, but it's not the whole story.

Lenders, title companies, and anyone doing a serious background check will still pull public records, and they will see the lien. So, while it won't tank your FICO score directly, its presence is far from a secret.

Can the State Take My House Because of a Lien?

This question gets right to the heart of the fear a lien creates. It also highlights the critical difference between a lien and a levy.

A state tax lien, by itself, doesn't mean the state is seizing your home. Think of the lien as the state putting a legal "dibs" on your property. It’s a claim that gets attached to your title, securing their spot in line to get paid. This prevents you from selling the house or refinancing your mortgage without settling the tax debt first.

A levy is something else entirely. A levy is the actual seizure of your property. An ignored lien can absolutely escalate into a levy, but they are two very different actions. The lien is the warning shot; the levy is when they come to collect.

A lien is a claim against your assets, securing the debt. A levy is the act of taking those assets to satisfy the debt. They are not the same thing, but an ignored lien can absolutely lead to a levy.

Does Bankruptcy Get Rid of a State Tax Lien?

This is where things get tricky. Filing for bankruptcy might wipe out your personal liability for certain tax debts. This means the state can no longer chase you personally for the money with things like wage garnishments.

However, bankruptcy typically does not remove a secured tax lien that was already in place before you filed. The lien remains firmly attached to your property like a barnacle. If you go to sell that property down the road, the state's claim is still there, and they have a right to the proceeds. In some cases, negotiating a settlement is a much more direct way to resolve the underlying debt.

At Attorney Stephen A Weisberg, we know every tax problem has its own unique story. We don’t do high-pressure sales pitches. Instead, we start with a FREE Tax Debt Analysis to map out the best path forward for your specific situation. If you're dealing with a state tax lien, let us help you find the best possible outcome.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034