Setting up a Payment Plan with the IRS: Easy Steps

Getting that dreaded letter from the IRS with a tax bill you can't possibly pay is a gut-punch. But before you panic, I want you to know one thing: you have options. Setting up a payment plan with the IRS, which they officially call an installment agreement, is a very common and straightforward way to get back on track.

It immediately puts a stop to the more aggressive collection tactics and gives you a clear, manageable path forward.

Why An IRS Payment Plan Is A Smart Move For Tax Debt

Let’s be real—staring down a massive tax bill is stressful. But the absolute worst thing you can do is stick your head in the sand. Ignoring the problem only makes it worse. Penalties and interest keep piling up, and the IRS will eventually escalate its collection efforts. An installment agreement is your proactive solution.

This is a formal deal with the IRS that lets you make monthly payments for up to 72 months. It’s a powerful signal to the agency that you’re taking this seriously and intend to pay what you owe. In my experience, showing this good faith is often enough to prevent scary actions like bank account levies or wage garnishments.

You Are Not Alone

If you're in this boat, you've got plenty of company. Many taxpayers find themselves in this exact position every single year.

In fact, roughly 10-15% of taxpayers with back taxes can't pay their bill in full right away. This makes the installment agreement one of the most frequently used tools for resolving an outstanding balance. You can dig into more official filing season statistics on the IRS website if you're curious.

This guide is designed to be your roadmap. We're going to walk through everything, step-by-step:

Figuring out if you qualify for a plan.

Getting all your financial documents in order.

Navigating both the online and paper application process.

Understanding the setup fees and ongoing costs.

Knowing how to manage your plan once it's approved.

The goal here is to trade that financial anxiety for a solid, actionable strategy. When you understand the process, you can take back control of your tax situation with confidence.

A Practical Solution, But Not The Only One

Think of an IRS installment agreement as a lifeline. It gives you breathing room and a predictable payment schedule, so you can budget properly without constantly looking over your shoulder.

Before you jump in, it’s worth taking a moment to see the full picture. The IRS offers several ways to handle tax debt, and the best one for you depends entirely on your situation.

Here's a quick look at the main options:

IRS Tax Debt Options at a Glance

| Payment Option | Best For | Typical Timeframe | Key Consideration |

|---|---|---|---|

| Installment Agreement | Taxpayers who can pay their full debt over time (up to 72 months). | 30 - 120 days to set up. | Interest and penalties continue to accrue until the debt is paid. |

| Offer in Compromise (OIC) | Taxpayers in significant financial hardship who can't pay their full debt. | 6 - 12 months (or longer). | Requires extensive financial disclosure; no guarantee of acceptance. |

| Currently Not Collectible | Taxpayers who truly cannot afford any payments due to extreme hardship. | Temporary; reviewed annually. | Pauses collections but the debt (plus interest/penalties) still exists. |

| Short-Term Payment Plan | Taxpayers who can pay in full within 180 days. | Immediate setup online. | Fewer fees, but the payment window is much shorter. |

While an installment agreement is an excellent tool, it's just one of several.

This guide will demystify the process, turning what feels like a complex chore into a series of simple, manageable steps. By the end, you'll know exactly how to approach the IRS, what to expect, and how to set up a payment plan that works for you.

Confirming You Qualify for a Payment Plan

Before you even think about filling out an application for an IRS payment plan, let's pump the brakes. There's nothing more frustrating than doing all the legwork only to find out you were never eligible to begin with. The IRS has very specific criteria, and getting familiar with them is your first real step toward putting this tax issue behind you.

The quickest route is the short-term payment plan. This gives you up to 180 days to clear your entire tax debt. It’s a great option with fewer hoops to jump through and lower fees, but it's really only for folks who can realistically pay everything off in about six months.

For most people, a long-term installment agreement is the way to go. This can stretch your payments out for up to 72 months (that's six years). As you might expect, the eligibility rules here are a bit tighter, focusing on how much you owe and whether you're up-to-date with your tax filings.

The Debt Thresholds for Individuals and Businesses

The IRS draws a line in the sand based on your total debt—that’s your combined tax, penalties, and interest. Knowing these numbers helps you know what kind of application process to expect.

For Individuals: If your total balance is under $50,000, you can usually apply for a long-term plan online without having to submit a mountain of financial paperwork. This is the most common path for individual taxpayers.

For Businesses: The magic number is lower for businesses, especially those with payroll tax debt. The streamlined online application process is generally available if you owe $25,000 or less.

What if your debt is higher than these amounts? Don't panic. It doesn't mean you're out of luck. It just means the IRS needs to take a much closer look at your finances. You'll be required to submit a Collection Information Statement (Form 433-F) with your payment plan request.

Key Takeaway: The amount you owe is a huge deal. Keeping your debt under the $50,000 (individual) or $25,000 (business) threshold makes getting a payment plan approved much, much easier.

The Non-Negotiable Filing Requirement

This is the absolute deal-breaker: you must have filed all your required tax returns. Let me be clear—the IRS will not even entertain a payment plan request from someone who isn't current on their filings. It's a non-starter.

"Being current" means every single tax return that is due has been submitted. If you have a few years of unfiled returns sitting in a pile somewhere, you have to tackle that mess before you can ask for a payment plan.

Think about it from their perspective. How can they agree to a payment arrangement for your 2023 taxes if they have no idea what you might owe for an unfiled 2022 return? They need the full picture.

What to Do If You Have Unfiled Returns

If you just had that "uh-oh" moment realizing you have unfiled returns, that's your new top priority. It can feel overwhelming, especially if records are spotty, but it's a mandatory step.

Here’s a practical game plan:

Figure Out What's Missing: The best way is to log into your IRS online account and pull your tax transcripts. They'll show exactly which years the IRS has a return for and which they don't.

Hunt for Your Documents: Start digging up any W-2s, 1099s, and other income and expense documents you can find for those missing years.

Call in a Pro: If this feels like too much to handle, now is the time to bring in a tax professional. They are pros at reconstructing income, preparing old returns, and getting you fully compliant before you make your request to the IRS.

Before you apply, you’ll also want to get a realistic handle on what you can afford to pay each month. A great way to start is to calculate your disposable income, as this is a key metric the IRS looks at. By confirming your eligibility and filing status first, you set yourself up for a much smoother, and ultimately successful, application.

Gathering Your Financial Documents for the Application

When it comes to setting up an IRS payment plan, the entire process hinges on one thing: preparation. I've seen countless applications get delayed or flat-out denied simply because the taxpayer didn't have their paperwork in order from the start.

Think of it this way: you're building a case. The more complete and organized your information is, the smoother the process will be. The IRS isn't trying to make your life difficult; they just need to verify who you are, what you owe, and what you can realistically afford to pay each month. An incomplete application just throws a wrench in the works and forces everyone to wait.

Your Personal and Tax Bill Details

First things first, let's get the basics down. This is the "who and what" of your application, confirming your identity and the specific tax debt you need to address.

You’ll want to have these items handy:

Personal Identifiers: This means your full name, current mailing address, date of birth, and your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN).

The Tax Bill: Go find that most recent IRS notice you received (a CP14 is a common one). You'll need the notice number, the tax year(s) in question, and the type of tax form (like Form 1040).

Taking a little time now by organizing your financial documents is one of the smartest moves you can make. It prevents a lot of scrambling and headaches later on.

Proving Your Income and Ability to Pay

Now we get into the nitty-gritty. The IRS needs a crystal-clear picture of all money coming into your household. Don't eyeball these numbers—you'll need the documents to back them up.

Pull together recent proof for all your income sources. This might include:

Pay stubs from the last 30-60 days.

Profit and loss statements or bank statements showing business deposits if you're self-employed.

Documentation for any other income, like Social Security, pension payments, or unemployment benefits.

A common mistake I see is people underreporting their income. The IRS can easily spot this by checking their own records, so full transparency is your best friend here. It builds trust and is absolutely critical when asking for a payment plan.

Pro Tip: If your income is irregular—maybe you're a freelancer or do seasonal work—calculate an average from the past six to twelve months. This gives the IRS a much more realistic figure and shows them you've put serious thought into what you can afford.

Detailing Your Monthly Living Expenses

Just as important as what you earn is what you spend. This is your chance to show the IRS your actual cost of living. They use this info, which gets captured on Form 433-F (Collection Information Statement), to make sure the payment plan they approve won't put you in a financial bind.

I always recommend my clients create a simple spreadsheet to track their necessary monthly living expenses. Get specific with your average spending on:

Housing & Utilities: Your mortgage or rent, property taxes, power, gas, water, etc.

Food & Personal Care: Groceries, toiletries, and other household necessities.

Transportation: Car payments, gas, insurance, and public transit passes.

Healthcare: Insurance premiums and any out-of-pocket medical or prescription costs.

Other Obligations: Any court-ordered payments like child support.

While the IRS has its own national and local standards for some of these costs, providing your actual numbers is what tells your unique story. Having all this ready to go makes filling out Form 9465 (Installment Agreement Request) or the online application a far less stressful experience.

Alright, you’ve got your financial paperwork lined up and you’re ready to tackle that IRS payment plan. So, what’s next?

You’ve basically got two ways to go about it: the fast, digital route through the IRS website or the old-school paper-and-mail method. Each has its place, and the best choice really comes down to your comfort level with technology and how complicated your tax situation is.

Let's break down both options so you can move forward with confidence and get on the path to resolving your tax debt.

Using the Online Payment Agreement Tool

By far, the quickest way to get this done is with the IRS Online Payment Agreement (OPA) tool. I always recommend this first. The biggest advantage? It’s designed to give you an immediate answer, which can be a massive weight off your shoulders. For most people who qualify, you can have a plan in place in just a few minutes.

To get started, you'll have to verify your identity. The IRS uses a secure third-party service called ID.me for this. Be prepared with a government-issued photo ID (like a driver's license), your Social Security number, and a phone with a camera. It’s a one-time setup, and once you’re verified, you can access the OPA portal.

Once you’re in, the system guides you through the process:

Confirm Your Tax Debt: The tool shows the exact balance the IRS has on record for you. Your first step is simply to confirm this is the amount you need to set up a plan for.

Propose Your Terms: You’ll enter a monthly payment amount you can afford and pick a due date that aligns with your budget.

Set Up Payments: You can choose to have payments automatically withdrawn from your bank account (this usually gets you a lower setup fee) or opt to pay manually each month by check, card, or money order.

After you submit your proposal, the system tells you right then and there if it's accepted. It’s a very straightforward process that delivers instant results.

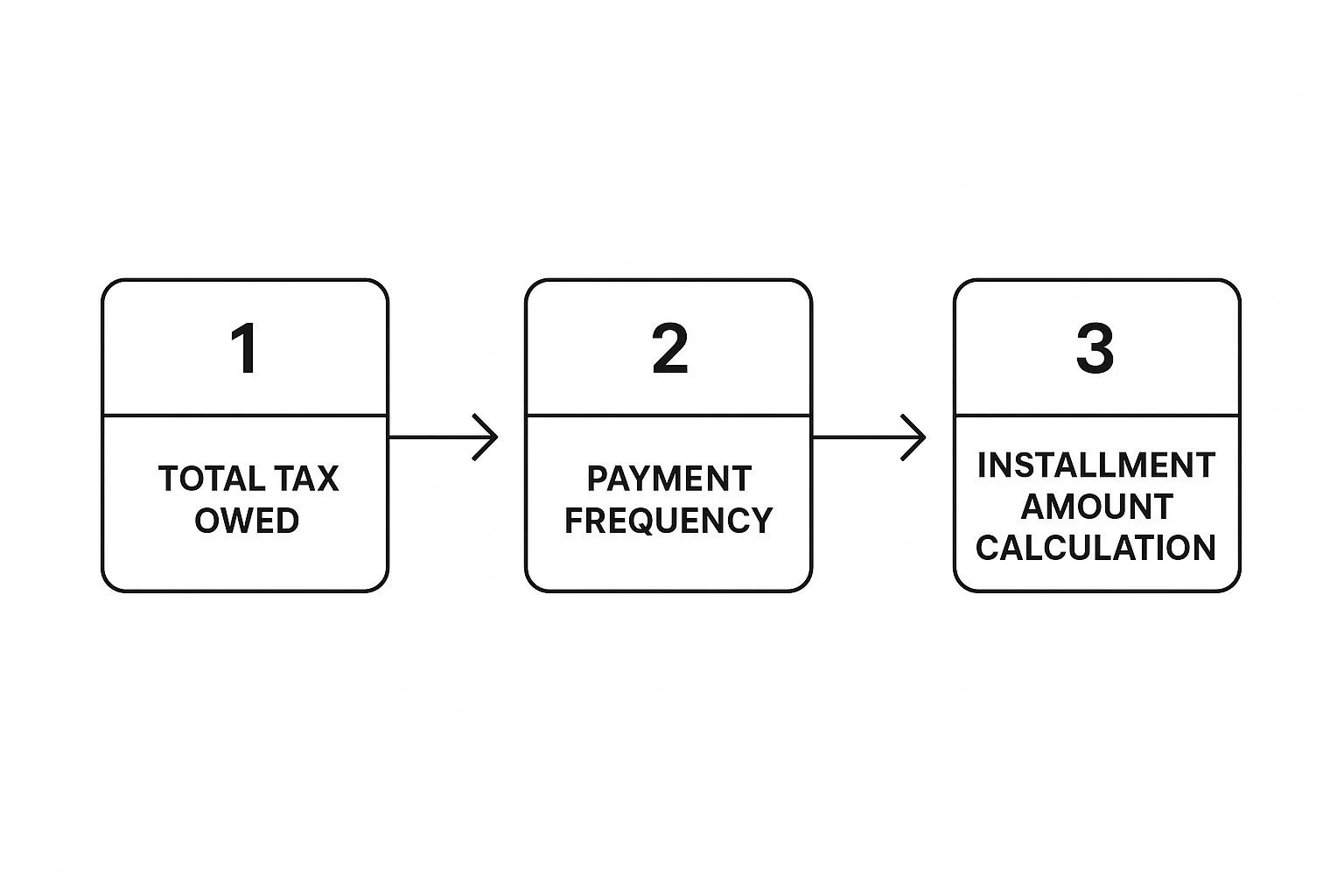

This simple infographic breaks down the core calculation you'll need to make, whether you're applying online or on paper.

It really just comes down to dividing what you owe by the number of months you have to pay, which helps you land on a manageable installment amount.

Filing the Paper Form 9465

The online tool is great, but it’s not a one-size-fits-all solution. Maybe you’re just not a fan of doing financial stuff online, or maybe your tax debt is too high for the OPA system's limits. In those situations, you'll need to use Form 9465, Installment Agreement Request.

You can download this two-page form right from the IRS website. Don't let its short length fool you—every field needs to be filled out perfectly to avoid getting it sent back, which just causes more delays. This is where all that financial info you gathered earlier comes into play.

A crucial step on Form 9465 is calculating your proposed monthly payment. This is a common sticking point. You have to propose a payment that you can realistically keep up with, but also one the IRS is likely to accept.

Expert Insight: My advice is to propose a payment that will pay off your total tax debt within the 72-month maximum timeframe. For instance, if you owe $36,000, a good starting point for your proposal would be at least $500 per month ($36,000 / 72). This shows the IRS you're serious.

If you’re struggling with the math or just want to double-check your numbers, using a specialized tool can be a huge help. After you've filled it out, you’ll mail the form to the address provided in the instructions. And one very important note: if you owe more than $50,000, you must also include a completed Form 433-F, Collection Information Statement, which is a detailed snapshot of your financial health.

Online vs. Paper Application: A Quick Comparison

Trying to decide between the online portal and a paper form? It's a common question. Each route has clear pros and cons. Here’s a simple, side-by-side look at the key differences to help you choose the best method for getting your IRS payment plan set up.

| Feature | Online Payment Agreement (OPA) | Paper Form 9465 |

|---|---|---|

| Speed | Instant decision and confirmation. | Can take 30-90 days or more for a response. |

| Convenience | Apply from anywhere, 24/7. | Requires printing, filling out, and mailing. |

| Debt Limits | Usually for debts under $50,000 for individuals. | No debt limit; required for higher balances. |

| Documentation | No extra financial forms needed for most plans. | May require attaching Form 433-F. |

| Setup Fees | Generally lower, especially with direct debit. | Higher setup fees for most taxpayers. |

At the end of the day, if you qualify for the OPA system, it’s almost always the better choice because it's so much faster and easier. But for those with more complex tax situations or higher balances, the paper Form 9465 is still a reliable and essential tool.

Understanding the True Cost of Your Payment Plan

Getting an IRS payment plan approved brings a huge wave of relief, but it’s crucial to understand that this solution isn't free. While an installment agreement gets the IRS off your back and stops aggressive collection actions, it absolutely does not stop the clock on what you owe.

Knowing all the costs upfront is the key to managing your tax debt without any nasty surprises down the road.

Breaking Down the Setup Fees

First things first, you'll have a one-time setup fee. The IRS charges this when your plan is officially locked in, and the amount you pay really depends on how you apply and how you decide to make your payments.

The IRS clearly prefers you to use their online systems, and they offer a pretty big financial carrot to get you to do it.

Online Application with Direct Debit: This is your cheapest ticket. If you apply online and set up automatic payments from your bank account, the fee is just $31.

Online Application without Direct Debit: Still applying online but want to send payments manually each month? The fee jumps up to $107.

Paper Application (Mail or Phone): Going the old-school route by mailing in a form or applying over the phone is the most expensive option, with a setup fee of $225.

There's a bit of help if you're struggling financially. If your income is below certain federal poverty guidelines, you might qualify for a reduced fee of $43. You’ll have to specifically request this low-income rate on your application.

The message from the IRS couldn't be clearer: go online and set up automatic payments. It saves you a significant amount of money right from the start and helps avoid the simple mistake of forgetting a payment.

The Ongoing Costs of Interest and Penalties

That setup fee? It’s just the cost of admission. The real, ongoing costs of an IRS payment plan are the interest and penalties that keep piling up on your unpaid balance. Even with an approved agreement, these charges don’t stop until every last penny of your debt is gone.

This is the part many people miss. As of recently, the IRS interest rate for underpayments is sitting at 7% per year, and it’s compounded daily. When you add the Failure to Pay penalty on top of that—usually 0.5% per month—your debt can grow a lot faster than you’d think.

A Real-World Cost Example

Let's put this into perspective. Say you owe $20,000 in back taxes and you get approved for a 72-month payment plan. Your monthly payment might be something like $278, but that's not the full picture.

Over those six years, interest and penalties are constantly being added. That initial $20,000 could easily swell by several thousand dollars by the time you've made your final payment. This is exactly why it’s so important to pay more than the minimum whenever you can. Every extra dollar goes toward the principal, saving you a fortune in these ongoing charges.

Understanding these costs from the get-go gives you the motivation to knock out the debt as quickly as your budget allows. For some, seeing the total potential cost pushes them to explore other options. Our guide on how to settle IRS debt can show you what those alternatives look like.

And once your plan is active, staying on top of it is everything; using strategies for effective tracking of contract obligations can help you manage your payments and avoid any future trouble with the IRS.

Common Questions About IRS Payment Plans

Once you've navigated the initial setup of an IRS payment plan, you enter the day-to-day reality of managing it. This is where the real questions start to pop up.

Knowing the answers to these common "what if" scenarios ahead of time is more than just helpful—it can be the key to keeping your agreement on track and avoiding a whole lot of unnecessary stress.

Let's walk through some of the questions I hear most often from my clients.

What Happens If the IRS Rejects My Payment Plan Request?

Getting a rejection notice can feel like a punch to the gut, but don't panic. It’s not the end of the line. That notice is your starting point—it will spell out exactly why the IRS said no.

Usually, it's something fixable. Maybe you left a field blank on the application, proposed a monthly payment the IRS considers too low, or you still have unfiled tax returns hanging out there.

Your first step should always be to call the number on the rejection notice. I've seen many situations get cleared up with a single phone call. You might be able to provide the missing piece of information or negotiate a new payment amount right then and there.

If a direct call doesn't do the trick, you have official appeal rights. You can file Form 9423, Collection Appeal Request, but you have to act fast. The deadline is typically 30 days from the date on your rejection letter. While an appeal is a solid option, trying to work it out with the collections department first is almost always the simpler, quicker route.

Can I Change My Monthly Payment Amount?

Life is unpredictable. A job loss, an unexpected medical bill, or any major hit to your income can suddenly make that agreed-upon payment impossible. So, can you change it? Absolutely.

The secret is to be proactive. Do not just stop paying and hope the IRS doesn't notice. They will. The moment you realize your financial situation has changed for the worse, you need to contact them. You can often request a modification through the same Online Payment Agreement (OPA) tool you used to apply, or simply by calling them.

Be ready to show them why you need the change. They'll want to see updated financial details that back up your request for a lower payment. In my experience, the IRS is far more willing to work with taxpayers who are upfront and communicative.

Key Takeaway: Communication is everything. The IRS is far more flexible with taxpayers who reach out before a problem occurs than with those who simply stop paying.

Does an IRS Payment Plan Affect My Credit Score?

This is a huge point of confusion, so let's set the record straight. The installment agreement itself is a private matter between you and the IRS. It is not reported to the big credit bureaus like Equifax, Experian, or TransUnion. So, being on a payment plan won't directly impact your credit score.

But—and this is a big "but"—the story changes if the IRS files a Notice of Federal Tax Lien.

A tax lien is a public claim against your property, and it's typically filed for larger tax debts (historically, over $10,000). Because it's a public record, credit reporting agencies will see it, and it can seriously damage your credit score. The payment plan is the solution to getting the debt handled, not the cause of the credit problem. In fact, making consistent payments can eventually help you get the lien withdrawn.

What if I Owe More Than the Online Limit?

The IRS Online Payment Agreement system is fantastic for its convenience, but it has its limits. That streamlined online process is generally reserved for people who owe a combined total of less than $50,000 in tax, penalties, and interest.

If your tax bill is higher than that, the online portal won't work for you. You'll need to go the paper route by filing Form 9465, Installment Agreement Request.

For these larger debts, the IRS requires a much more detailed financial picture. This means you'll also need to fill out and attach Form 433-F, Collection Information Statement, which is a comprehensive breakdown of your assets, income, and expenses.

It's more paperwork, for sure, but it’s the necessary path for larger tax liabilities. When dealing with a debt of this size, it's also a good idea to explore all types of IRS debt forgiveness to see if other powerful solutions might be a better fit for your situation.

At Attorney Stephen A Weisberg, we understand that every tax situation is unique. Instead of a one-size-fits-all approach, we start with a FREE Tax Debt Analysis to determine the best path forward for you.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034