Understanding the Tax Debt Statute of Limitations

If you're staring down a mountain of old tax debt, the one question that probably keeps you up at night is: does this ever just go away?

The answer, surprisingly, is yes. The IRS doesn't have an infinite amount of time to come after you for old taxes.

They generally get a 10-year window to collect, a deadline officially known as the Collection Statute Expiration Date (CSED). Once that date passes, your debt is effectively off the books.

Cracking the Code of the 10-Year Collection Clock

For anyone feeling crushed by a seemingly endless tax burden, the idea of a tax debt statute of limitations can feel like a lifeline. It's a very real legal boundary that prevents the IRS from pursuing old debts forever.

Think of it like this: the moment the IRS officially calculates what you owe and puts it on your account—a process called "assessment"—a stopwatch starts.

From that exact day, a 10-year countdown begins. This isn't just some administrative quirk; it's a fundamental part of your rights as a taxpayer.

It gives you finality, ensuring you know the absolute maximum amount of time the government has to collect.

Why Does This Time Limit Even Exist?

This 10-year rule isn't some loophole someone discovered. It's a deliberate part of the tax code, written to give everyone—both the government and the taxpayer—a sense of certainty and closure. Imagine a world without it.

The IRS could chase you for a debt from 30 years ago, creating a lifetime of financial instability. This rule ensures that at some point, everyone can move on.

The U.S. isn't alone in this, but policies vary wildly from one country to the next. Some nations have scrapped time limits entirely out of fear of tax evasion, while others, like the United States, stick to a clearly defined collection period.

It’s a constant balancing act between government revenue needs and taxpayer rights.

For a quick reference, here’s a breakdown of the key elements we’ve just discussed.

IRS Collection Statute Fundamentals

This table simplifies the core components of the IRS's 10-year collection rule.

| Component | General Rule | What It Means for You |

|---|---|---|

| The Rule | 10-Year Statute of Limitations | The IRS has ten years from the date of assessment to collect the tax you owe. |

| The Trigger | Date of Assessment | The clock starts ticking the day the IRS officially records your tax liability. |

| The Deadline | Collection Statute Expiration Date (CSED) | This is the final day the IRS can use legal action like levies or liens to collect. |

| The Purpose | Finality and Certainty | It provides a clear end date, preventing the IRS from pursuing the debt forever. |

Understanding these fundamentals is the first step, but it's important to see how they fit into the larger legal landscape.

Tax rules are just one piece of a massive puzzle of regulatory compliance solutions that govern our financial lives.

Now, here's the critical part: this 10-year clock isn't always a straight shot. Certain actions you take can actually pause or "toll" the clock, extending the CSED.

We'll dive into those exceptions later, but if you want to get a head start, you can learn more about how the IRS statute of limitations works in our more detailed guide.

It's crucial to have the full picture of how that CSED is calculated and what you might do to accidentally extend it.

Finding Your Collection Statute Expiration Date

Figuring out your Collection Statute Expiration Date (CSED) is probably the single most empowering thing you can do when you're facing down an old tax debt.

This isn't some fuzzy, made-up deadline; it's a hard stop. It's the exact date the IRS legally loses its power to collect from you. But to find it, you have to know where the 10-year race officially began: the tax assessment date.

Think of this date as the moment the IRS fires the starting pistol. It’s when your tax liability is officially entered into their system, and the 10-year clock starts ticking. Without this specific date, you're just guessing. Pinpointing it is job number one.

Where to Find Your Tax Assessment Date

The only truly reliable place to get this information is straight from the source: your official IRS account transcript. You can pull this document yourself directly from the IRS website.

Once you have the transcript for the right tax year, you’re looking for a specific entry. Scan the list of transactions for code “150”.

The date right next to it is almost always your official tax assessment date. It's the day your return was processed and the debt became official.

Consider it the birth certificate for your tax debt—the day its 10-year life began.

Sure, you might find an assessment date on old letters from the IRS, like a Notice of Deficiency or a Notice and Demand for Payment. But honestly, the account transcript is the gold standard. It’s the most complete and definitive record you can get.

Key Takeaway: The "assessment date" on your IRS account transcript is what triggers the 10-year tax debt statute of limitations. That date, typically found next to transaction code 150, is the most critical piece of the puzzle for calculating your CSED.

Let's walk through how this looks in the real world.

A Practical Walkthrough with Alex

Let's meet Alex. He’s a freelance graphic designer who filed his 2018 tax return on schedule back in April 2019. He ended up owing $15,000 but just didn't have the cash to pay it. The IRS processed his return, and the debt was officially on the books.

Alex needs to know when that 10-year collection window slams shut. Here’s exactly how he’d figure it out:

Request the Transcript: First, Alex heads over to the IRS website and requests his "Account Transcript" for the 2018 tax year.

Locate the Assessment Date: He gets the document and skims through it until he spots the magic words: "150 Tax return filed" next to a date of May 20, 2019. That's it. That's his assessment date.

Calculate the Preliminary CSED: Now for the simple math. Alex just adds exactly 10 years to that date.

Assessment Date: May 20, 2019

Add 10 Years: + 10 Years

Preliminary CSED: May 20, 2029

So, based on this initial look, Alex's CSED is May 20, 2029. After that day, the IRS shouldn't be able to touch his paychecks or his bank accounts for this particular tax debt.

This calculation gives Alex a crucial baseline. It takes a vague, looming dread and turns it into a concrete date he can plan around. But—and this is a big but—it's critical to know this is only the preliminary date.

This is your foundation, but it's not the final answer on the tax debt statute of limitations. Certain things Alex might have done since 2019 could have hit the "pause" button on that 10-year clock. This is a concept known as "tolling," and understanding what causes it is the next vital step to confirming your real CSED.

Actions That Pause the 10-Year Collection Clock

That 10-year countdown on your tax debt is a hard legal limit, but it’s not always a straight shot from start to finish. It's less like a wall clock that ticks away relentlessly and more like a stopwatch. Certain actions you take can hit the "pause" button, temporarily stopping the clock.

This legal concept is called tolling, and it's probably the most critical—and most misunderstood—part of the whole statute of limitations game.

Getting the tolling calculation wrong is a classic mistake. You might think you're in the clear, with your debt about to vanish, when in reality you’ve unknowingly tacked on months or even years to your Collection Statute Expiration Date (CSED).

The IRS doesn't just pause the clock for fun; it happens when you start a process that legally ties their hands and stops them from collecting. While they wait for that to play out, the clock is frozen.

What Triggers a Pause on the CSED Clock?

So, what kind of actions actually hit that pause button? Several common things a taxpayer might do will toll the statute of limitations.

Each one stops the clock for a specific amount of time, usually for however long the issue is being reviewed, plus a little extra breathing room.

Let's look at the most frequent culprits.

An Offer in Compromise (OIC) is a big one. This is when you ask the IRS to let you settle your tax bill for less than the full amount owed. The moment you file a valid OIC, the CSED clock stops dead.

It stays paused the entire time the IRS is reviewing your offer. If they turn you down, the clock remains paused for another 30 days to give you a chance to appeal. And if you do appeal? You guessed it—the clock stays frozen during that whole process, too.

Requesting an Installment Agreement can also do it. While the IRS considers your application for a monthly payment plan, the CSED is tolled.

This makes sense; they can't very well be levying your bank account while they're also deciding whether to approve your payment plan.

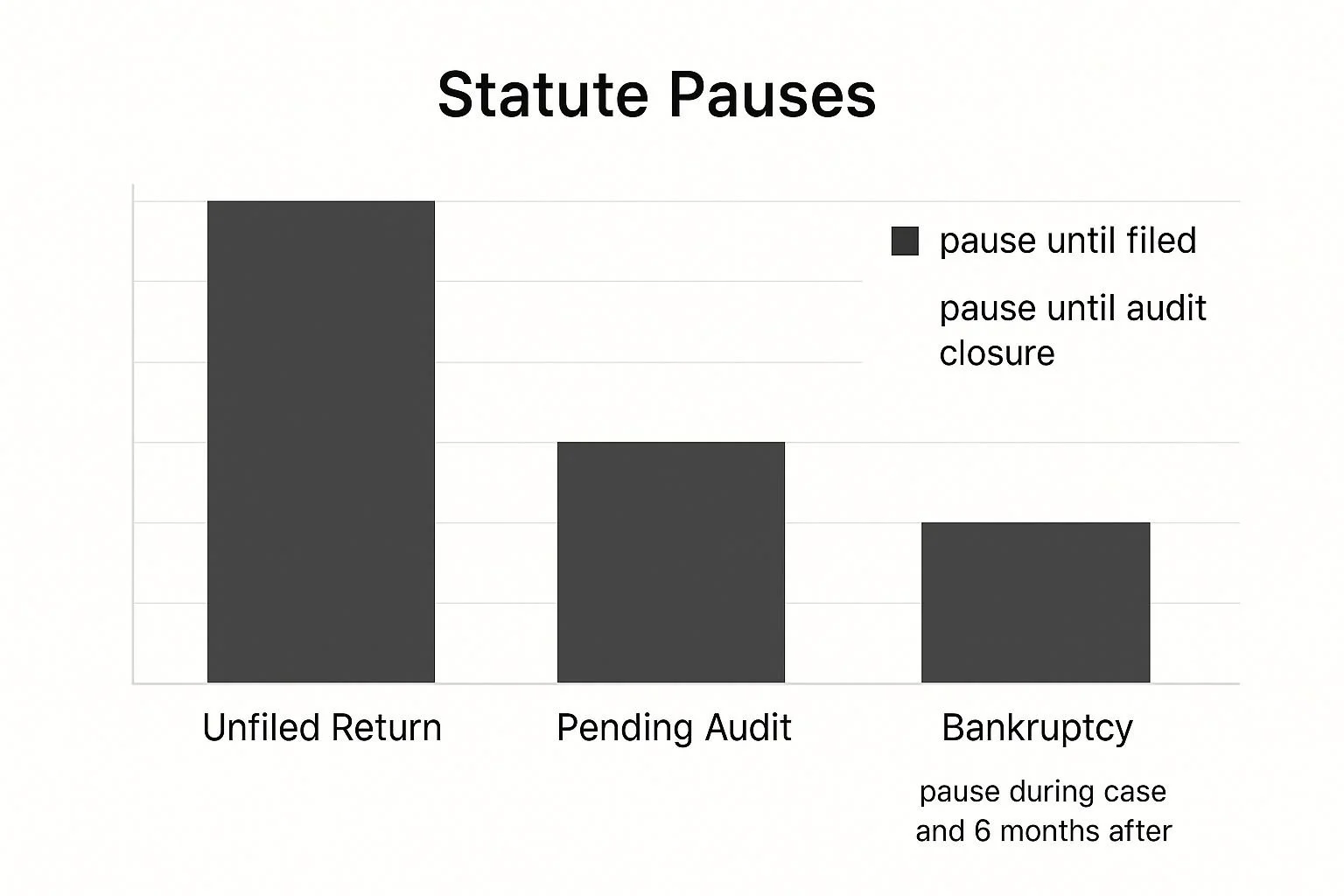

This chart gives you a good visual of how certain events throw a wrench in the timeline.

As you can see, things like bankruptcy or just not filing a return can put that collection clock on hold for a very long time.

Many taxpayer actions can stop the collection clock, and knowing which ones is key to accurately calculating your CSED. Below is a table breaking down some of the most common tolling events.

Common Actions That Pause (Toll) the IRS Collection Clock

| Action or Event | Does It Pause the Clock? | Typical Duration of Pause |

|---|---|---|

| Offer in Compromise (OIC) | Yes | During the OIC review, plus 30 days after rejection, and for the duration of any appeal. |

| Installment Agreement Request | Yes | During the review of your request. |

| Bankruptcy Filing | Yes | For the entire bankruptcy proceeding, plus an additional six months. |

| Collection Due Process (CDP) Hearing | Yes | From the date of the request until the appeals decision becomes final. |

| Living Outside the U.S. | Yes | For any continuous period of at least six months spent abroad. |

| Innocent Spouse Relief Request | Yes | While the IRS is considering your claim. |

This isn't an exhaustive list, but it covers the main triggers. Each of these events adds time back to the clock, pushing your debt's expiration date further into the future.

Bankruptcy and Other Major Tolling Events

Filing for bankruptcy is one of the most significant tolling events. The second you file, an "automatic stay" slams on the brakes, legally blocking all creditors—including the IRS—from any attempt to collect.

The CSED is tolled for the entire duration of the bankruptcy proceeding, plus an additional six months after it concludes. This is a massive pause and one of the most common reasons a 10-year clock stretches out much longer.

Another key event is a Collection Due Process (CDP) Hearing. When you get that "Final Notice of Intent to Levy," you have a right to request a CDP hearing to contest it.

From the moment you submit that timely request, the clock is paused. It only starts ticking again once the appeals office's decision is final and no longer appealable.

Here are a couple of other situations that will stop the clock:

Living Outside the U.S. If you’re out of the country for at least six months straight, the CSED clock is paused for the entire time you're gone.

Requesting Innocent Spouse Relief. If you ask the IRS to absolve you of tax debt your spouse or ex-spouse racked up, the statute is tolled while they review your request.

Filing a Lawsuit Against the IRS. Suing the IRS over what you believe was an improper collection action will also pause the clock.

This is exactly why just marking 10 years on a calendar from your assessment date doesn't work. You have to go back and account for every single action that might have hit that pause button.

If you don't, you could be in for a nasty shock when you think you're free and clear, only to have the IRS resume collections.

Critical Exceptions to the 10-Year Rule

While the ten-year clock on tax debt feels like a firm finish line, it’s not set in stone. In fact, certain situations don't just pause the collection clock—they prevent it from ever starting. For some, the tax debt statute of limitations can become infinite, giving the IRS a lifetime to collect.

This isn't just trivia for obscure tax cases. Understanding these exceptions is crucial for knowing where you truly stand with the IRS.

It's easy to fall into a false sense of security, thinking a tax debt is getting older and closer to expiring when, in reality, the countdown hasn't even begun. These aren't minor technicalities; they're absolute game-changers.

When the Clock Never Starts Ticking

The whole concept of the Collection Statute Expiration Date (CSED) rests on one thing: a valid tax assessment by the IRS.

But what happens if the IRS can't make that assessment? A couple of scenarios completely derail the process, leaving you exposed to collection action indefinitely.

The most common reason is also the simplest: never filing a tax return. If you don’t file, the IRS can't officially assess the tax.

Without an assessment, there's no start date for the 10-year clock. It’s a harsh but straightforward reality—no return means no CSED.

The debt hangs over your head forever, or at least until you file and the tax is formally assessed.

The second major exception is filing a fraudulent return. If the IRS determines you deliberately filed a false return to evade taxes, all time limits are off the table.

This isn't about an honest mistake; it's about intentional deception. In cases of proven fraud, the law gives the IRS unlimited time to assess and collect the tax.

Warning: Tax fraud is a criminal offense. If the IRS suspects it, you’re facing much more than just an unlimited collection window. The consequences can escalate to severe financial penalties and even prosecution.

This challenge isn't unique to the U.S. Across the European Union, countries struggle with collecting tax debt, often due to their own statutory limitations.

In one striking example, Greece reported its uncollected tax debt was nearly 90% of its annual tax revenue, a sign that weak enforcement timelines can cripple a nation's finances. You can dig deeper into how these rules impact public finances in the full report from the European Commission.

Other Actions That Create Unlimited Exposure

Besides not filing or committing fraud, a few other actions can give the IRS an unlimited runway to collect what you owe.

Willful Attempt to Evade or Defeat Tax: This is a broad category that covers more than just filing a bogus return. It includes things like hiding assets, using offshore accounts to conceal income, or any other scheme designed to keep the IRS from figuring out and collecting the right amount of tax.

Living Abroad to Evade Payment: Simply living outside the U.S. for six months can pause the clock. But if the IRS can prove you're doing it specifically to dodge your tax bill, the rules change drastically, and the statute of limitations could be suspended indefinitely.

If you find yourself in one of these situations, waiting it out is not a strategy. You need a proactive solution. The first step is always to get compliant, especially if you have unfiled returns.

For many, exploring resolution programs is the best path forward. A great place to start is by learning how to qualify for offer. It's a powerful tool when the statute of limitations offers no escape.

What Happens When Your Tax Debt Finally Expires

Finally hitting the end of that ten-year collection period is a huge deal. Once that Collection Statute Expiration Date (CSED) arrives, the IRS officially loses its legal right to come after you for that specific tax debt.

For many people, this is the light at the end of a very long, dark tunnel. The debt becomes legally unenforceable. This means the IRS has to stop all its aggressive collection tactics for that liability.

No more wage garnishments, no more bank levies, and no more seizing your property for that old debt.

The Immediate, Tangible Benefits

The best part? When the tax debt statute of limitations runs out, the resolution is automatic. You don’t have to fill out a form or call anyone to make it happen. The law simply kicks in on its own, bringing instant and significant relief.

One of the most powerful consequences is the release of federal tax liens. If the IRS slapped a Notice of Federal Tax Lien on your property because of that debt, they are legally required to release it after the CSED passes.

This clears the title to your property, making it much easier to sell assets or get a loan.

Key Insight: The CSED expiring isn't a negotiation or some kind of settlement you have to apply for—it's a hard legal stop. The debt is no longer collectible through administrative action, period. It’s a clean break.

This provides a fresh start, finally getting rid of the constant stress of enforced collection that can loom over your head for a decade. It's a definitive end to a long and difficult chapter.

Understanding the Reality of Uncollectible Debt

While the ten-year rule is a firm deadline, the truth is that the government is already fighting an uphill battle long before that date arrives.

The IRS is juggling a massive portfolio of delinquent accounts. Back in 2019, the total amount of outstanding tax debt was over $20.5 billion. The odds of collecting on a debt drop dramatically the older it gets.

People move, assets become harder to trace, and the practical challenges of enforcement just pile up. You can dig into the numbers yourself in the official Treasury Inspector General for Tax Administration report.

This practical reality is exactly why the CSED is so important. It acts as a final backstop, acknowledging that after ten years of trying, the chances of getting that money are slim to none. It gives both the taxpayer and the government a clear point to finally move on.

Using Your CSED to Make Smart Financial Decisions

Knowing your Collection Statute Expiration Date (CSED) is more than just trivia. It’s a powerful piece of intelligence that can completely change how you approach your tax problem.

Think of it as moving from being a passenger to getting in the driver's seat. The goal isn’t to simply survive until the clock runs out; it's to find the best possible resolution for you.

Let’s be clear: trying to "wait out the clock" is almost always a terrible idea. It’s a high-stakes gamble that usually leads to a decade of misery, escalating penalties, and increasingly aggressive collection tactics from the IRS. As the CSED gets closer, they don't back off—they turn up the pressure.

A much smarter approach is to use your CSED as a strategic benchmark. It allows you to realistically weigh your options and pick the path that truly fits your financial situation.

Aligning Your Strategy with Your Timeline

Your CSED is your North Star. It guides you toward the most logical solution based on how much time is left on the clock. A strategy that makes perfect sense for someone with nine years to go could be a disaster for someone with only two years remaining.

For instance, if your CSED is a long way off, an Offer in Compromise (OIC) might be a fantastic option. It gives you a shot at settling your tax debt for a fraction of the total. But applying for an OIC pauses the statute of limitations, which is why it's a tool best used when you have plenty of time to spare.

Strategic Insight: If your CSED is just a year or two away, a short-term solution suddenly becomes much more attractive than a long-term one that stops the clock. The less time the IRS has, the more leverage you might have to negotiate a manageable outcome without extending the process.

This is where being proactive really pays dividends. Understanding your timeline helps you sidestep actions that could accidentally work against you by pausing that all-important collection clock.

Making an Informed Choice

With your CSED firmly in mind, you can start to evaluate the different paths forward. Each one has a different impact on your finances and the tax debt statute of limitations.

Short-Term Payment Plan: If your CSED is on the horizon, a short-term plan could let you clear a smaller balance before the time expires.

Offer in Compromise (OIC): This is generally best for taxpayers with a distant CSED who have no realistic way to pay their full debt. It tolls the statute but can provide a permanent fresh start.

Currently Not Collectible (CNC) Status: If you're going through a period of intense financial hardship, the IRS might temporarily halt collection efforts. The clock keeps ticking under CNC, making it a viable move for those nearing their CSED.

Using Other Funds: Sometimes, the most direct route is to pay the debt in full. If the amount is within reach, you might explore options like personal loans to pay off tax debt to get instant closure and sidestep any further complications with the IRS.

At the end of the day, your CSED is one of the most critical variables in your tax resolution equation. It's not just a deadline; it's a strategic tool that empowers you to take control, choose the right path, and finally put your tax debt behind you for good.

Your Questions Answered: Tax Debt Expiration

When you start digging into the details of the tax debt statute of limitations, a lot of very specific, real-world questions pop up. It's completely normal.

Getting the right answers is crucial, because a small misunderstanding can lead to some big problems down the road. Let's tackle some of the most common questions I hear from clients.

Does the 10-Year Rule Apply to State Tax Debt?

Absolutely not. This is a critical point that trips a lot of people up. The famous 10-year IRS statute of limitations is a federal rule for federal taxes only.

Your state has its own rulebook. Every single state sets its own timeline for collecting debts like state income tax or sales tax, and they are all over the map. Some states give themselves as long as 20 years to collect, while others might have a much shorter window.

You absolutely cannot assume the federal rule applies to your state tax bill. Always check your specific state's tax laws to know where you stand.

Will the IRS Contact Me After My CSED Has Passed?

Legally, they shouldn’t. Once your Collection Statute Expiration Date (CSED) arrives, the IRS loses its power to take collection actions like levying your bank account or garnishing your wages for that specific tax debt. The debt is essentially unenforceable, and any tax liens tied to it have to be released.

Now, you might see an automated notice get sent out right around the CSED—sometimes the computers are a little slow to catch up. But persistent collection letters after the date has passed?

That’s a major red flag. It almost always means a "tolling" event happened that you weren't aware of, which paused the clock and pushed your CSED further into the future.

Important Note: A debt that has legally expired isn't the same as a debt that has been paid or settled. If you still have a balance, it's worth exploring your options.

Does an Installment Agreement Restart the 10-Year Clock?

This is one of the most dangerous myths out there. The answer is a firm no. Applying for an IRS Installment Agreement does not reset the 10-year collection clock back to day one.

What it does do is "toll," or pause, the clock. While the IRS is considering your application, the countdown is temporarily on hold. Once your plan is approved and you start making payments, the clock usually starts ticking again right where it left off.

Keep in mind, if you later default on that agreement, the clock can be paused again during the default period. So, these actions extend the final CSED—they don't restart it. It's a pause button, not a reset button.

At Attorney Stephen A Weisberg, we know every tax situation has its own story. We don't use high-pressure sales pitches. Instead, we start with a FREE Tax Debt Analysis to see exactly what's going on and figure out the best way we can help you.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034