Notice of Levy from IRS: Your Essential Guide to Acting Fast

An IRS notice of levy isn't a friendly reminder. It's the final step in the collection process—a legally binding action to seize your property to cover an overdue tax debt.

It’s less like a bill and more like a court-ordered seizure of your assets, whether that's cash from your bank account or a chunk of your upcoming paycheck.

What an IRS Notice of Levy Actually Means for You

Getting any official mail from the IRS can be nerve-wracking, but a Notice of Levy demands your immediate attention.

Unlike other letters you might receive, this notice means the IRS has moved past warnings and is now actively taking your property to collect what you owe.

This is the government's final move after a long collections game that should have included several prior notices.

This isn't just another request for payment. A levy is the legal seizure of your property. The notice itself is often sent directly to third parties who hold your assets—think your employer or your bank—ordering them to hand over your property to the IRS.

For example, if a levy hits your bank account, the bank is required to freeze your funds for 21 days before sending them to the government.

IRS Tax Levy vs IRS Tax Lien

One of the biggest points of confusion for taxpayers is the difference between a tax levy and a tax lien. People use the terms interchangeably, but they are completely different tools the IRS uses to collect on a debt. Getting this straight is critical to understanding what's happening.

A lien is a claim, while a levy is an action. Here’s a quick breakdown:

| Feature | IRS Tax Lien | IRS Tax Levy |

|---|---|---|

| Primary Function | Secures the government's interest in your property. It’s a public claim against your assets. | The actual seizure of your property to satisfy the tax debt. |

| What It Does | Acts as a public record that the IRS has a legal right to your property. It can harm your credit and prevent you from selling assets. | Takes your property. This can be your wages, bank account funds, car, or even your home. |

| Impact on You | A claim is placed on your property. | Your property is taken from you. |

In short, a tax lien is like the government putting a "dibs" on your property, securing its place in line as a creditor. A tax levy is when the government actually comes to collect on that "dibs" and takes the property away.

The Legal Groundwork for a Levy

The IRS can't just decide to levy your assets out of the blue. There are strict legal procedures they must follow. By law, the agency has to send you a final warning first, which is the Final Notice of Intent to Levy and Notice of Your Right to a Hearing.

This crucial preceding notice gives you at least 30 days to either pay the debt or formally request a hearing to dispute the action. The Notice of Levy you’re holding now is what comes after that 30-day window has closed.

This authority comes from Internal Revenue Code Section 6331, which gives the IRS the power to issue this formal notice and seize property. It can be delivered in person, left at your home or business, or sent via certified mail.

The Path That Led to Your Levy Notice

An IRS levy doesn't just show up out of the blue. It’s the final, and most severe, move in a long, predictable collection playbook the IRS follows. Understanding how you got here is the first step to taking back control. This wasn't a sudden ambush; it was the last step in a documented series of warnings.

The whole process almost always kicks off with a simple tax bill. This happens after you file a return showing you owe money, or when the IRS figures out a tax debt for you on their own.

Initial Bill (Notice and Demand for Payment): This is the first official ask for the money. It's often a notice like a CP14, and it clearly lays out the tax you owe, plus any penalties and interest that have already started piling up.

If you don’t respond to that first bill, the IRS will send more notices. Each one gets a little more serious, and all the while, the penalties and interest keep ticking upward, making your total debt grow every month.

The Critical Warning Shot

Before the IRS can legally take your property, they are required by law to send one last, very specific warning. This is, without a doubt, the most important piece of mail in the entire sequence leading up to the levy itself.

This formal letter is usually called a Final Notice of Intent to Levy and Notice of Your Right to a Hearing (Letter 1058 or LT11).

When this letter arrives, it’s your last clear chance to stop the seizure process cold. It tells you in no uncertain terms that the IRS plans to levy your property and gives you 30 days to request a Collection Due Process (CDP) hearing to fight it.

Key Takeaway: The "Final Notice of Intent to Levy" is the IRS's final warning shot. It starts a 30-day countdown, giving you a crucial window to appeal or set up a payment plan before they actually take anything. Ignoring this letter is what directly triggers a levy.

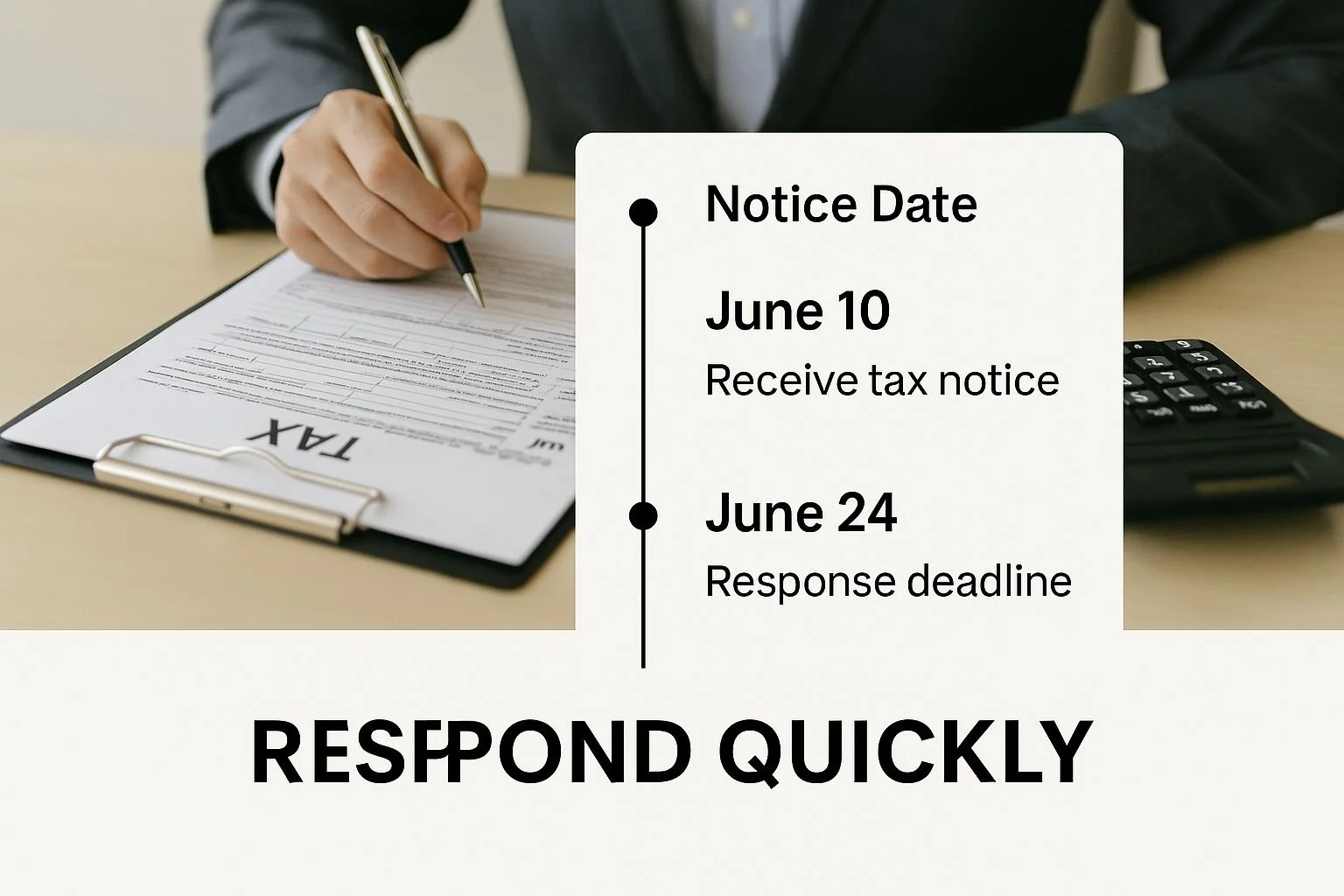

The following infographic really drives home why you need to act fast when the IRS gets in touch.

This image highlights a fundamental truth in dealing with tax problems: quick responses are your best defense against the IRS’s collection machine.

If you didn’t reply within that 30-day window from the Final Notice, you essentially gave the IRS the green light to issue the Notice of Levy—the document you're looking at now.

They send this notice to third parties, like your boss or your bank, telling them to hand over your assets. The path from that first bill to a final notice of levy from IRS is paved with missed chances to communicate and find a solution.

What Assets the IRS Can Actually Seize

When a notice of levy from the IRS lands in your mailbox, the abstract fear of seizure suddenly gets very specific. The big question is: what can they actually take?

The IRS has surprisingly broad powers to seize assets, so it's vital to know what they usually go after first to understand the immediate threat to your financial stability.

Make no mistake, a levy isn't a suggestion. It's a legal seizure. The IRS can divert money from your paycheck, clean out your bank account, and even take physical property. What they target first usually depends on what's easiest to get.

Common Types of IRS Levies

The IRS almost always goes for liquid assets first. Why? Because it’s the fastest and cleanest way to turn your assets into cash to cover your tax debt.

They aren't trying to make your life miserable by taking your grandmother's wedding ring; they're simply trying to collect what they're owed as efficiently as possible.

Here are the most common things the IRS will target:

Wages and Salaries: This is the big one. Often called a wage garnishment, it's probably the most frequent type of levy. Unlike a one-time bank levy, this is a continuous drain. Your employer is legally obligated to send a chunk of every single paycheck directly to the IRS. This continues until the debt is paid in full or you manage to get the levy released. The exact amount they can take depends on your filing status and the number of dependents you claim.

Bank Accounts: This is another go-to for the IRS. When they hit your account with a levy, your bank has no choice but to freeze your funds up to the amount you owe. They are required by law to hold this money for 21 days. This is your last-ditch, critical window to negotiate with the IRS. If you can't get the levy released in time, the bank sends the funds to the government on the 22nd day.

Social Security and Other Federal Payments: Yes, even federal payments are on the table. Through a program called the Federal Payment Levy Program (FPLP), the IRS can take a slice of your Social Security retirement benefits. This automated system can grab up to 15% of your monthly check before you ever see it.

Can the IRS Take Your Car or House?

So, what about the big-ticket items? While the IRS can technically seize your house, car, or other valuable physical property, it’s a lot less common. Think of it as a last resort.

Seizing and selling a primary home is a complex legal process with a lot of hoops for the IRS to jump through. They typically only go down this road for very large debts and only after a taxpayer has completely ignored all other attempts to collect.

An IRS levy is an incredibly powerful tool, and the agency uses it frequently. In a given year, the IRS issues hundreds of thousands of levies across the country, collecting billions from taxpayers through both automated programs and direct collection actions.

These automated levies often snatch state tax refunds and federal payments, while the more traditional levies handled by the Automated Collection System (ACS) are the ones that target your wages and bank accounts. You can learn more about how the IRS uses levies directly from their data. Knowing what they target helps you see exactly where you're most vulnerable when that notice arrives.

Your Critical First Steps After Receiving a Levy

When an official-looking envelope from the IRS arrives, the absolute worst thing you can do is pretend you never saw it.

A notice of levy from the IRS isn't just another bill; it’s a flashing red light signaling that their collection process has hit its final, most serious stage.

Ignoring it is a direct path to seized assets. But this is a moment where you still have options. Acting quickly—and correctly—can stop the process cold and open the door to a real resolution.

What you do in the next few hours and days will decide whether the IRS takes money from your bank account, garnishes your paycheck, or seizes other property.

Immediately Review and Understand the Notice

Your first job is to sit down and read the notice. All of it. Don't just glance at the scary-looking amount at the top. You're looking for specific details that arm you with the information you need to fight back effectively.

Look for these key pieces of information:

The Amount Owed: This will be broken down into the original tax, plus all the penalties and interest that have piled up.

The Tax Periods: The notice will specify exactly which tax years are involved. This is critical, especially if you have unfiled returns from those years. If you need help with that, our guide on how to file back taxes is a great place to start.

IRS Contact Information: Find the phone number and the specific IRS unit or department listed on your notice. This isn't a general helpline; it's your direct point of contact.

When you pull out these details, that terrifying notice transforms into a simple, actionable checklist. You now have the facts you need to have a productive conversation with the IRS or a tax professional.

Crucial Insight: Right now, your most powerful tool is communication. The IRS only sends a levy notice when they think you've gone silent. Picking up the phone and re-establishing contact proves you're taking this seriously and is the first step to getting the levy released.

Open a Line of Communication

Your next move is just as urgent: call the IRS. You can do this yourself, or you can have a qualified tax professional make the call on your behalf. The mission is simple: let them know you’ve received the notice and you want to work this out.

Hoping the problem will just go away guarantees the levy will proceed. Making that call flips the script. It stops you from being a passive victim and makes you an active player in finding a solution. You can start discussing options, whether that’s a payment plan or another resolution.

Even if you don't have a penny to send them right now, the simple act of engaging shows good faith. It’s a massive step in the right direction. Remember, at its core, the IRS is the world's most powerful collection agency.

Their main goal is to collect what’s owed, and it's far easier for them to work with a cooperative taxpayer on a payment plan than to go through the administrative hassle of seizing your assets.

Proven Ways to Resolve an IRS Levy

Getting a levy notice from the IRS can feel like hitting a brick wall. It’s scary, and it feels final. But I want you to reframe that thinking—this isn't the end of the road.

In many ways, it's the start of a conversation. You now have the IRS's full attention, which creates an opportunity to move from crisis mode to finding a real, long-term solution.

The good news is that the IRS has several structured programs for resolving tax debt. These aren't secret loopholes; they are established paths designed for taxpayers in different financial situations.

Instead of just letting the government seize your assets, you can get into the driver's seat and work toward a resolution that lets you meet your obligations without losing everything.

Summary of IRS Levy Resolution Options

Before we dive deep, it helps to see the main options side-by-side. Each one serves a different purpose, and knowing which one might fit your situation is the first step toward taking control.

| Resolution Option | Description | Best For Taxpayers Who... |

|---|---|---|

| Installment Agreement | A structured payment plan to pay off the full tax debt over time through monthly payments. | Have a steady income and can afford to make consistent monthly payments to clear their debt. |

| Offer in Compromise | An agreement to settle the tax debt for a lower amount than what is originally owed. | Have significant debt they cannot realistically pay in full and can prove severe financial hardship. |

| Currently Not Collectible | A temporary pause on IRS collection efforts due to severe financial hardship. | Cannot afford basic living expenses and need immediate, short-term relief from collections. |

Now, let's break down what each of these really means for you.

Negotiate an Installment Agreement

For many people, the most direct path forward is an Installment Agreement (IA). It’s exactly what it sounds like: a payment plan for your tax debt.

If you owe a hefty sum but just can't pay it all in one go, an IA breaks it down into manageable monthly payments over a set period.

This is an excellent choice if you have a reliable income and can realistically chip away at the balance. The IRS is surprisingly cooperative with these agreements because it ensures they get paid.

As soon as your IA is approved and you make that first payment, the IRS is required to release the levy on your wages or bank account.

Settle for Less with an Offer in Compromise

But what happens when the debt is so overwhelming that you know, deep down, you could never pay it all back?

That’s what the Offer in Compromise (OIC) program was created for. An OIC allows certain taxpayers to completely resolve their tax liability for less—sometimes much less—than the original amount.

Don't mistake this for a simple "get out of debt free" card. The IRS is a tough negotiator. They will only accept an OIC if they're convinced it’s the absolute most they could ever hope to collect from you.

To even be considered, you have to open up your entire financial life to them, proving that paying in full would cause a legitimate economic hardship. The IRS will scrutinize your:

Ability to pay, based on your income versus necessary living expenses.

The equity you have in assets like your home, vehicles, or retirement accounts.

Your realistic future earning potential.

Getting an OIC approved is a complex and document-intensive process. A thorough review of your financial and tax records is non-negotiable, and tools that provide AI-powered tax document analysis can help organize your information before you apply.

Prove Financial Hardship for a Pause

Sometimes, things are just too tight. Your financial situation might be so precarious that you can't afford any payments right now. If you can prove this to the IRS, they may agree to place your account in Currently Not Collectible (CNC) status.

Important Note: CNC is not debt forgiveness. Think of it as hitting the pause button on collections. Interest and penalties continue to pile up on your balance, and the IRS will periodically review your finances to see if you can start paying again.

To qualify for CNC, you must show the IRS that taking any money from you would prevent you from covering basic, necessary living expenses—we're talking about things like rent, food, and utilities.

It’s a critical safety net for people facing genuine hardship, giving them the breathing room they need to get back on their feet without the constant threat of a notice of levy from the IRS.

Common Questions About IRS Levies

When you’re staring down a notice of levy from the IRS, it’s natural for a thousand questions to start racing through your mind. It's a stressful, high-stakes situation, but getting clear, direct answers is the first step toward getting back on solid ground.

Let's cut through the noise and tackle the most pressing questions taxpayers have when facing a levy.

Can the IRS Really Take My House or Car?

The short answer is yes, the IRS has the legal authority to seize physical assets like your home or car. But—and this is a big but—it’s incredibly rare and always a last resort.

Think about it from their perspective. Seizing liquid assets like cash from a bank account or funds from your paycheck is fast and easy.

Taking a house, on the other hand, is a bureaucratic nightmare. It involves a mountain of paperwork and requires court approval, a step not needed for most other levies.

This drastic measure is almost exclusively reserved for people who owe a very large amount, haven't paid in years, and have ignored every single attempt the IRS has made to contact them.

You would have received a stack of specific warnings long before the seizure of your home was ever a realistic possibility.

How Long Does a Bank Account Levy Last?

A bank levy isn't a continuous drain; it’s a one-time snapshot. The moment your bank gets the levy notice, they are legally required to freeze the funds in your account, up to the total amount of your tax debt.

Those funds are then held for a 21-day period. This isn't just an arbitrary waiting game—it's a critical, legally mandated window of opportunity. It's your last chance for you or your tax professional to negotiate with the IRS to get the levy released.

If you can't reach a resolution in those 21 days, the bank sends the money to the IRS on day 22. At that point, the levy is over.

For the IRS to get any more money, like your next deposit, they would have to start the entire process over again and issue a brand new levy.

Key Insight: The 21-day hold on a bank levy is not a negotiation tactic; it is a legally mandated grace period. It is your absolute last chance to act before the money is gone for good.

What Is the Difference Between a Levy Notice and an Intent to Levy Notice?

This is a critical distinction that trips a lot of people up. The easiest way to think about it is a warning shot versus the real thing.

Notice of Intent to Levy: This is the warning. The IRS must, by law, send you this notice (usually Letter 1058 or LT11) at least 30 days before they can actually take anything. It's their way of saying, "We are planning to levy your assets, and here's your right to appeal by requesting a Collection Due Process (CDP) hearing."

Notice of Levy: This is the action. This document isn't sent to you first—it goes directly to your bank, your employer, or another third party. It instructs them to seize your assets and turn them over. If you get a copy of this, it means the levy is already happening.

Receiving a "Notice of Intent" is your single best chance to get ahead of the problem and prevent the seizure from ever starting.

Can I Stop an IRS Wage Garnishment After It Starts?

Yes, you absolutely can stop an ongoing wage garnishment, but you have to act fast. Your employer can’t stop it for you; the release order has to come directly from the IRS.

To make that happen, you need to contact the IRS and work out an alternative. This usually means setting up a formal Installment Agreement or proving you qualify for another resolution.

For instance, you might be able to explore options for IRS debt forgiveness if you can demonstrate that the garnishment is causing you significant financial hardship.

Once you and the IRS agree on a solution, they will send a release notice to your employer. Just be aware that payroll systems can be slow, so it might take a pay cycle or two for the deductions to actually stop.

Navigating a notice of levy from the IRS can be overwhelming, but you don't have to face it alone.

At Attorney Stephen A Weisberg, we specialize in resolving complex tax issues and protecting taxpayers' rights. We start with a FREE Tax Debt Analysis to understand your situation and determine the best path forward before you ever pay a fee. Get your free analysis and find your solution today.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034