What Is a Notice of Levy? A Complete Guide

No one likes getting a letter from the IRS, but a notice of levy is one you absolutely can't ignore. It's not just another bill—it's a formal, legal action that gives the IRS the power to seize your assets to cover an unpaid tax debt. Understanding what this letter truly means is your first, most critical step toward finding a solution.

What a Notice of Levy Means for You

Think of the IRS collection process as an escalation. A simple tax bill is just the beginning. A notice of levy shows up much later in the game, signaling that the IRS has moved past simple requests and is now legally authorized to take your property. This document is their official communication of that intent.

It's crucial to understand the difference between a levy and a lien. A tax lien is simply a claim against your property to secure the government's interest in what you owe. A levy, on the other hand, is the actual seizure of that property. The lien is the claim; the levy is the action.

The Key Players in a Levy Action

When the IRS issues a levy, it immediately creates a relationship between three parties. Each one has a specific role to play and certain legal obligations they must follow. Knowing who's who can help demystify the process and clarify your next moves.

To make this clearer, let's break down who is involved and what their responsibilities are.

Key Players in the IRS Levy Process

| Party | Role and Responsibility |

|---|---|

| The IRS | The government agency that has determined a tax debt is owed and is now using its legal authority to collect it by seizing assets. |

| The Taxpayer | You—the individual or business with the outstanding tax liability. You have specific rights and a limited time to respond and stop the seizure. |

| The Third Party | The person or entity holding your assets. This could be your bank, your employer, or another financial institution. They are legally required to comply with the levy. |

Understanding these roles is fundamental. Your immediate goal is to get in touch with the IRS to stop the third party—like your bank or employer—from handing over your assets.

A third party who receives a notice of levy must legally comply. For example, your bank must freeze funds in your account for 21 days before sending them to the IRS. This 21-day hold provides a crucial window to negotiate a release.

While this document is powerful and serious, it’s not the end of the road.

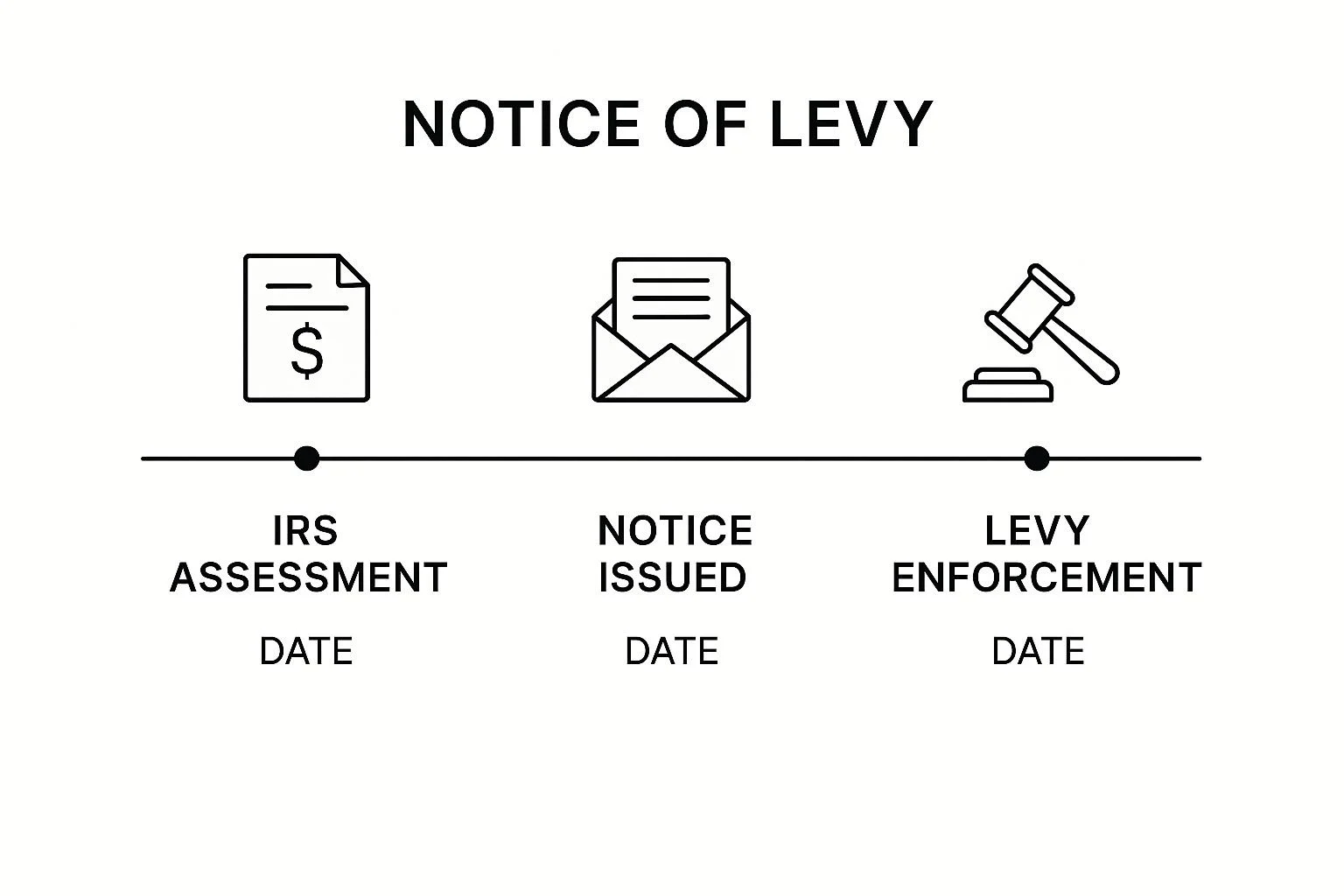

The Path to an IRS Levy

An IRS levy doesn't just materialize out of thin air. It’s the last and most serious move in a long, legally defined collection process. The key is to understand this timeline because it’s full of off-ramps—chances for you to resolve your tax problem long before your assets are on the line.

The journey starts simply. After you file your tax return (or the IRS files one on your behalf), the agency assesses the tax and officially records that you owe a balance. This is the official starting pistol.

From there, the IRS has to follow a very specific, legally required first step.

Step 1: The Initial Bill

The very first letter you'll get in the mail is a Notice and Demand for Payment. Think of it as the initial bill. It lays out how much you owe and, as the name implies, demands you pay it. This notice is a mandatory legal step; without sending it, the IRS can't legally escalate to more aggressive collection tactics like a levy.

This first letter gets the clock ticking, but you’re still a long way from the end of the road. The IRS will usually follow up with a series of reminder notices over the next several months. These letters, often coming from their Automated Collection System (ACS), will gradually become more firm in their tone.

The infographic below shows how this journey unfolds, from the first bill to the final enforcement action.

As you can see, the process isn't random. It's structured and predictable, giving you clear milestones and opportunities to step in and take control.

Step 2: The Final Warning

If you haven't resolved the debt after those initial reminders, the process hits its most critical point. The IRS will send one last, decisive letter.

This letter is officially called the "Final Notice of Intent to Levy and Notice of Your Right to a Hearing." This is it—the ultimate warning. It flat-out tells you the IRS plans to seize your property and that you have 30 days to do something about it.

This 30-day window is your single most important chance to formally challenge the levy or work out a solution. Ignoring this specific notice is what directly paves the way for the IRS to seize your bank account, garnish your wages, or take other property.

By law, the IRS has to follow these steps in this exact order:

Assess the Tax and Send a Notice and Demand for Payment: This is the first bill that officially puts the debt on the books.

Provide a Final Notice of Intent to Levy: This is the letter that gives you that critical 30-day warning before any seizure can happen.

Wait for the 30-Day Period to Expire: The IRS is legally barred from levying your property until after this window closes.

This sequence proves that a notice of levy isn’t a surprise attack. It's the predictable outcome of a documented process, one that gives you several chances to stop it from ever happening.

Understanding Different Types of IRS Levies

When the IRS decides to levy, they don't use a one-size-fits-all approach. Think of it as a toolbox—they have different instruments designed to seize specific kinds of assets. Knowing which tool they’re using is critical to understanding how a levy will hit your finances.

Generally, these actions boil down to two main categories.

The most common is a one-time levy. This is like the IRS taking a financial snapshot. They seize whatever funds are available in an account on the exact day they process the levy, and that’s it.

Then there’s the continuous levy, which is exactly what it sounds like: ongoing. This type of levy attaches itself to a stream of payments, siphoning off a portion of each one until your tax debt is completely cleared. You'll most often see this with wages and certain federal payments.

Levies on Financial Accounts and Paychecks

Your bank account is often the first place the IRS looks for a one-time levy. Once your bank gets that notice, they are legally required to freeze funds up to the amount you owe. Let's say you owe $5,000 and have $6,000 in your account; the bank freezes the $5,000. After a 21-day holding period, that money is sent straight to the IRS.

A wage garnishment is the classic example of a continuous levy. In this scenario, your employer gets the levy notice. From that point on, they must legally divert a portion of every single paycheck to the IRS. The exact amount they take is calculated based on your tax filing status and the number of dependents you claim, but it can easily eat up a huge chunk of your take-home pay.

Important Distinction: A bank levy is a single grab of what's there on one day. A wage garnishment is a recurring nightmare, hitting every paycheck until the debt is gone.

Levies on Federal Payments and Retirement Funds

The IRS also has the power to intercept money the federal government owes you through a system called the Federal Payment Levy Program (FPLP). This is another type of continuous levy, and it can target several different income sources.

Here are a few common examples of what the FPLP can go after:

Social Security Benefits: The IRS can take up to 15% of your monthly benefit payment.

Federal Employee Retirement Annuities: A portion of these pension payments can be garnished.

Federal Contractor Payments: If you provide goods or services to the government, the IRS can intercept your payments.

And yes, even your retirement accounts—like a 401(k) or an IRA—can be levied. While it’s a more complicated process for the IRS, these assets are absolutely not safe. A levy on a retirement fund is particularly devastating because it can trigger early withdrawal penalties on top of the tax debt itself, wiping out a significant portion of your nest egg in one fell swoop.

Your Legal Rights After Receiving a Levy Notice

Getting a letter titled "Final Notice of Intent to Levy" in the mail can make your heart stop. It feels final, like a judgment has been passed. But it's not. In fact, this letter is the starting gun—it kicks off your most important legal rights and opens a critical window for you to take back control.

The moment you get that notice, a 30-day clock starts ticking. This isn't just a courtesy; it's your legal shield. During these 30 days, the IRS is legally barred from taking your property or money. This gives you a brief, but incredibly valuable, opportunity to mount a defense.

Don't let that window close. Ignoring the deadline means giving up your best leverage.

The Power of a CDP Hearing

Your most powerful tool in this situation is the right to request a Collection Due Process (CDP) hearing. This isn't just another form letter; it's a formal proceeding with the IRS Independent Office of Appeals, a completely separate and impartial division from the revenue officers trying to collect.

Think of a CDP hearing less like a courtroom battle and more like a structured negotiation. It’s your chance to sit down with an impartial officer and:

Challenge the levy itself: You can argue that the levy is out of line or would cause you extreme financial harm.

Question the underlying tax debt: In certain situations, you can even dispute the amount of tax the IRS says you owe in the first place.

Propose a way out: This is where you can formally present alternatives to seizure, like a payment plan.

Requesting this hearing is a massive strategic advantage. The second the IRS gets your request, all collection activity has to legally stop. The levy is frozen until the hearing is over and the Appeals Office makes a decision. This buys you precious time and stops the immediate threat to your bank accounts and paycheck.

By formally requesting a CDP hearing, you put an immediate legal freeze on the IRS's collection activities. The levy cannot proceed until the Appeals Office issues a final determination.

To make it happen, you must file Form 12153, Request for a Collection Due Process or Equivalent Hearing. It has to be sent to the address on your levy notice and postmarked within that 30-day deadline. Missing it is a big deal.

You might get what's called an "Equivalent Hearing," but you lose the automatic power to stop the levy and the right to take your case to Tax Court if you disagree with the outcome.

What You Can Achieve in a Hearing

The whole point of a CDP hearing is to find a reasonable path forward that doesn't involve the IRS simply seizing your assets. The Appeals Officer is there to make sure the collectors followed all the rules and to evaluate whether the levy would create an unfair economic hardship for you and your family.

During the hearing, you (or your tax pro) can work to secure a better outcome, such as:

An Installment Agreement: A formal, structured monthly payment plan that you can actually afford.

An Offer in Compromise (OIC): If your financial situation is dire, you may be able to settle the entire tax debt for a fraction of what you originally owed.

Currently Not Collectible (CNC) Status: If you can prove you don't have enough money to cover basic living expenses, the IRS can agree to pause all collection attempts temporarily.

At the end of the day, that Final Notice is a call to action. It hands you the legal tools to defend yourself. By understanding your rights and using the CDP hearing process, you can go from being on the defensive to being in control, opening the door to a resolution you can live with.

How to Stop a Levy and Resolve Your Tax Debt

Getting an IRS levy notice is a shock. It’s stressful, intimidating, and designed to get your immediate attention. But it’s also a powerful call to action. You have options—real, practical strategies to stop the levy in its tracks, release any funds already seized, and finally resolve the underlying debt.

The most important thing to know is that you must act fast. Doing nothing is the worst possible move. It lets penalties and interest pile up, digging a deeper financial hole. So, let’s go over the playbook for taking back control.

Option 1: Installment Agreement

The most direct route for many people is an Installment Agreement (IA). It's exactly what it sounds like: a formal deal you make with the IRS to pay your tax debt over time through manageable monthly payments.

The moment your IA is approved, the levy process grinds to a halt. As long as you stick to the plan and make your payments on time, the IRS won’t touch your assets. This is the perfect solution if you have the ability to pay the debt over time, just not all at once.

Option 2: Offer in Compromise

If you're facing a genuine financial hardship, an Offer in Compromise (OIC) can feel like a lifesaver. This program allows you to settle your tax liability for less—sometimes much less—than the full amount you owe.

Be warned, this isn't a casual negotiation. It's a formal, rigorous process that requires you to open up your entire financial life to the IRS. They want to see detailed proof of your income, expenses, and assets.

Key Insight: An OIC is designed for people in a truly difficult spot. The IRS only accepts it if they are convinced it’s the absolute most they can ever hope to collect from you. The application is intense and approval isn't guaranteed, but for the right person, it offers a true fresh start.

As you explore how to stop a levy, it's helpful to get a broader perspective by understanding debt relief services and how the industry works.

Option 3: Currently Not Collectible Status

But what if you can’t even afford a small monthly payment? If you can prove to the IRS that paying anything toward your tax debt would keep you from affording basic living expenses—like rent, food, or transportation—you might qualify for Currently Not Collectible (CNC) status.

This isn't debt forgiveness. Your tax bill doesn’t vanish, and interest and penalties will unfortunately keep growing. CNC is a temporary pause. The IRS agrees to stop all collection efforts, including levies, giving you critical breathing room to get back on your feet. They will check in on your finances periodically to see if your situation has improved.

Each of these options provides a distinct path away from the immediate crisis of a levy. Seeing them side-by-side can help clarify which one might be right for you.

Comparing Tax Debt Resolution Options

This table breaks down the three main strategies to help you see how they stack up.

| Resolution Method | Best For... | Key Outcome |

|---|---|---|

| Installment Agreement | Taxpayers who can afford to pay their debt off over time in monthly installments. | The levy is stopped, and you have a predictable payment plan to clear your debt. |

| Offer in Compromise | Those with significant financial hardship who cannot possibly pay the full amount owed. | The total tax debt is settled for a reduced amount, providing a permanent solution. |

| Currently Not Collectible | Individuals who cannot afford basic living expenses, let alone a tax payment. | The IRS pauses all collection actions, providing immediate relief from levies. |

Ultimately, choosing the right strategy comes down to a clear-eyed analysis of your personal finances. For most people, making this decision alone can feel overwhelming. Exploring a comprehensive tax debt solution with a professional who knows the ins and outs of the IRS can make all the difference in achieving a successful outcome.

The Consequences of Ignoring a Levy Notice

Sometimes, the best motivation for taking action is understanding what happens if you do nothing. When that "Final Notice of Intent to Levy" arrives, that 30-day window to respond is your last real line of defense. Once it closes without you reaching out, the IRS has the green light to act.

They won't be sending you any more warnings. Instead, they’ll start contacting the third parties who hold your money and assets. This is it—the beginning of the actual seizure process.

The fallout is swift and severe. The IRS will send levy notices directly to your bank, your employer, or other financial institutions. The results are immediate and can completely derail your day-to-day life and long-term financial stability.

Real-World Impact of an IRS Levy

An IRS levy isn't some abstract threat; it materializes in very real ways that can turn your world upside down overnight. I'm not saying this to scare you, but to be perfectly clear about what’s at stake and why responding is so critical.

Here’s what this typically looks like:

Frozen Bank Accounts: Your bank is legally required to freeze funds in your account, up to the amount you owe. For 21 days, you lose access to that money. After that, the bank sends it straight to the IRS.

Wage Garnishment: Your employer will have to start sending a hefty portion of your paycheck to the IRS before you ever get it. This isn't a one-time thing; it happens with every single paycheck until the debt is paid in full.

Seizure of Property: While it’s less common, the IRS does have the authority to seize and sell your physical property. We're talking about cars, real estate, or other valuables.

A huge misconception I see all the time is people thinking a levy is a one-and-done event. While a bank levy is a single seizure of what's in the account at that moment, a wage garnishment is a continuous, relentless action. It can go on for months, or even years, making it nearly impossible to get your footing financially.

Ignoring the notice turns a problem you can solve into a full-blown financial crisis. It's also important to know that a levy is a separate issue from a tax lien, which acts as a public claim against all your property. If a lien is also part of your situation, you can learn more about how to remove a tax lien in our detailed guide. Doing nothing allows both problems to fester, causing profound damage to your financial health.

Your Top Questions About IRS Levies, Answered

Once you understand the basics of what an IRS levy is, a lot of specific questions usually pop up. Let's tackle some of the most common ones I hear from clients to give you clear, direct answers.

What Is the Difference Between a Levy and a Lien?

This is easily the most common point of confusion, and for good reason—the terms sound similar. But in the world of tax collection, they mean very different things.

A tax lien is the IRS laying a legal claim against your property. Think of it as a public announcement that you owe the government money. It secures their interest in your assets (like your house or car) and can make it nearly impossible to sell or refinance them.

A levy is the actual seizure. It's the lien in action.

Key Distinction: A lien is a claim on your property. A levy is the government taking your property.

Can the IRS Really Take My Social Security?

Yes, they can. While many private creditors can't touch Social Security benefits, the federal government plays by a different set of rules.

Through the Federal Payment Levy Program (FPLP), the IRS can automatically take up to 15% of your monthly Social Security payment. This isn't a one-time thing; it's a continuous levy that will chip away at every single check until your tax debt is gone. The FPLP can also target other federal payments, like retirement benefits for federal employees.

How Long Does a Bank Hold Funds for an IRS Levy?

When the IRS levies your bank account, the bank doesn't just hand the money over immediately. They are legally required to freeze your funds and hold them for a very specific amount of time.

That magic number is 21 days. This 21-day holding period is your critical window of opportunity. It gives you or your tax professional time to contact the IRS, fight the levy, and negotiate a release. If you don't take action within those three weeks, the bank sends the money to the IRS on the next business day, and it's gone.

If you've fallen behind, remember that getting current is the best defense.

Are you facing a Notice of Levy or another intimidating IRS issue? At Attorney Stephen A Weisberg, I start with a FREE, no-obligation Tax Debt Analysis to see if and how I can help. Don't face the IRS alone—let's find your solution together.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034