What Is a State Tax Levy? How It Affects Your Assets

When you hear the term "state tax levy," it’s easy to feel a knot in your stomach. And for good reason. A state tax levy is the government's legal right to seize your property to cover an unpaid tax bill.

This isn't a friendly reminder or a warning shot. It's the state taking direct, forceful action after previous attempts to collect the debt have gone unanswered. Understanding what this really means is your first critical step to getting back on solid ground.

The Difference Between a State Tax Levy and a Lien

People throw the words "levy" and "lien" around like they’re the same thing, but they are worlds apart in the tax collection process. Getting this straight is essential—it tells you just how serious your situation has become and what you need to do next.

Think of It This Way

Imagine you have a mortgage. A tax lien is like the bank putting a public note on your property title that says, "This person owes us money, and this house is the collateral." The bank hasn't kicked you out. The lien just secures their claim and makes it tough for you to sell the house without paying them first. It’s a public flag on your property and a black mark on your credit.

Now, a state tax levy is the bank showing up with a truck to change the locks and repossess the house. It’s no longer just a claim; it’s the actual seizure. The state has moved past securing its interest and is now actively taking your assets to settle the score.

State Tax Levy vs State Tax Lien Key Differences

It’s easy to get tangled up in the terminology, but the distinction is simple when you see it side-by-side. A lien is a claim, while a levy is the act of taking. This table breaks it down clearly.

| Aspect | Tax Levy | Tax Lien |

|---|---|---|

| Action | Seizure of Assets | Claim on Assets |

| Purpose | To satisfy the tax debt immediately. | To secure the government's interest in your property. |

| Impact | Loss of property, frozen bank accounts, wage garnishment. | Harms credit score, complicates selling property. |

While a lien is a serious problem that clouds your financial future, a levy is an immediate crisis that can drain your bank account overnight or take a chunk out of your paycheck before you even see it.

Crucial Takeaway: A lien is a claim, while a levy is an action. A lien secures the debt, but a levy actively collects it by taking what you own. This escalation from a passive claim to an active seizure signals a critical point in your tax dispute.

The principles behind a state levy are quite similar to a federal one. You can learn more about how the federal government handles this process on the official IRS website.

The Path to a State Levy

Let’s be clear: a state tax levy isn't a random event that comes out of nowhere. It's the final, dramatic act in a long, predictable process. Think of it less as a surprise attack and more as the inevitable conclusion after a series of warnings have been ignored.

Knowing the timeline is your best defense. It pulls back the curtain on the process, showing you exactly where you stand and what moves you can make before things get serious.

The entire journey almost always kicks off with an unpaid tax bill. Maybe you have unfiled returns, underpaid on a return you did file, or a state tax audit found you owe more than you thought.

Whatever the reason, the state now believes you have a tax debt. This is the absolute best time to sort things out. If you’re behind, getting a handle on how to file back taxes can be a crucial first step.

From First Notice to Final Demand

Once the state flags an outstanding debt, its collection machine starts to turn. But it doesn't immediately jump to seizing your property. Instead, you'll receive a methodical series of letters, each designed to get your attention and get you to pay.

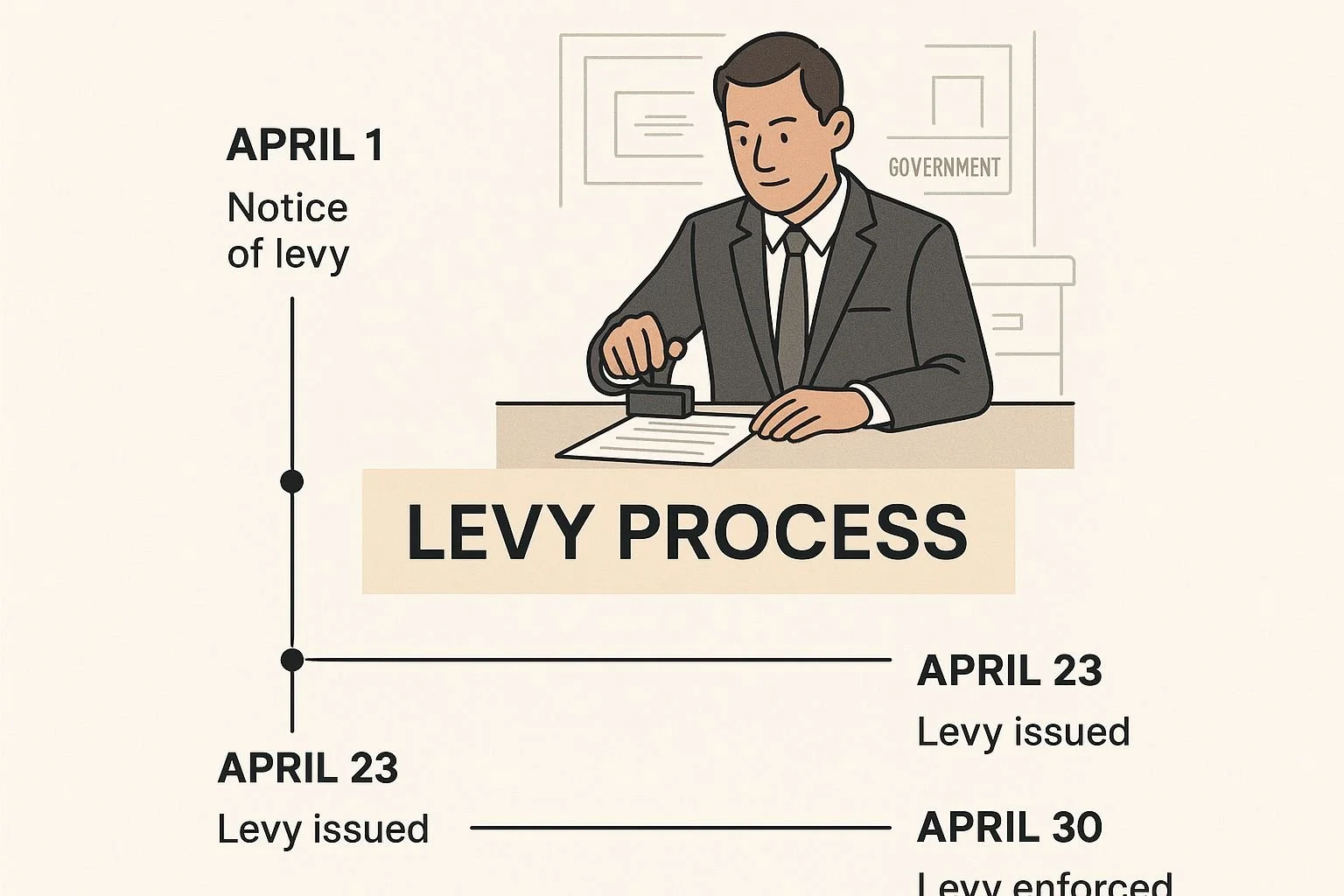

First up is the Tax Assessment Notice. This is the official document that legally establishes the debt. It lays out exactly how much you owe, for which tax period, and why.

If that notice goes unanswered, the next letter you’ll get is a Demand for Payment. This one is more direct. The tone gets more urgent, clearly stating the amount due and demanding you pay up. Most states will send a few of these, and each one will sound a little more serious than the last.

This graphic shows the typical road to a levy, with each step leading to the next.

As you can see, a levy is what happens after a long period of inaction, not an overnight surprise.

The Point of No Return

The last stop before the state takes your assets is the Notice of Intent to Levy. This is it—the final warning. This is a legally required notice telling you that the state is preparing to seize your property if you don't resolve the debt within a specific timeframe, usually 30 days.

This notice is your last chance to get ahead of the problem. It will also explain your rights to appeal, which often involves requesting a Collection Due Process (CDP) hearing or a similar state-level review.

If you ignore this letter, a levy is almost guaranteed. At this stage, the state has done its legal duty to warn you. The path is now clear for them to start garnishing your wages, cleaning out your bank accounts, or taking other property to settle the debt.

What Assets Can a State Tax Levy Target?

When a state issues a tax levy, it’s not just some theoretical threat—it’s the government’s green light to start taking your property to settle up. Understanding exactly what’s on the table is the first step in grasping how serious this is and protecting what you’ve worked for.

State tax agencies almost always go after the low-hanging fruit first. That means they’re looking for the assets that are easiest to find, seize, and turn into cash.

Common Targets for Seizure

A state levy can cast a surprisingly wide net, touching nearly every corner of your financial life. While the exact rules differ from state to state, some assets are almost always at the top of their list.

Wages and Salary: This is what’s known as a wage garnishment, and it’s a favorite tool for tax agencies. They send a notice to your employer, who then has no choice but to withhold a chunk of your paycheck and send it straight to the state.

Bank Accounts: This one can be a real shock. A levy can freeze your checking and savings accounts instantly, often without any prior warning. Your bank is then legally required to hand over any funds in the account, up to the amount of your debt.

Physical Property: Yes, the state can seize physical assets like your car, boat, or even your home. But this is usually a last resort because of the hassle and expense involved in taking and selling property.

Business Assets: If you’re a business owner, the state can levy your company’s bank accounts, accounts receivable (the money your clients owe you), and even physical equipment.

State Tax Refunds: If you’re expecting a refund from the state, think again. Any refund you’re due will be automatically intercepted and put toward your outstanding tax bill.

Wage garnishments and bank account seizures became standard practice back in the mid-1900s, as financial systems became more sophisticated. As tax codes grew more complicated and states relied more heavily on tax revenue, the levy became a powerful and essential tool for collection.

Important Note: When the state does seize physical property, it has to be sold at a public auction. To do this, they need to determine its value. Understanding the concept of fair market value is key to seeing how this process works.

Are Any Assets Safe?

Thankfully, yes. State laws recognize that you can’t be left with absolutely nothing. There are specific exemptions in place to prevent a tax levy from pushing you into complete financial ruin.

Here are some of the assets that are typically protected:

A certain portion of your wages needed for basic living expenses.

Public benefits like unemployment, workers' compensation, and some disability payments.

Certain retirement accounts and pensions, though the rules here can vary wildly from one state to another.

The protections for retirement funds are especially complex. To get a better handle on how these assets are treated, particularly by the feds, take a look at our guide on whether the IRS can take your 401k. But remember, you should always double-check your own state's specific exemption laws—these protections are far from universal.

Know Your Rights When Facing a Levy

Getting a letter about a state tax levy is a gut-punch. It can feel like you’re powerless against a huge, faceless government agency. But I need you to know this: you are not without options. State laws give you real, meaningful rights to ensure the process is fair and you get a chance to make your case.

Knowing your rights is the first step to defending them. The state’s power to levy is built on a legal foundation called due process. This isn't just jargon; it means they can't just take your stuff. They have to follow a specific, legally required procedure.

It starts with a tax assessment, then a demand for payment. If you don't pay, they must send a final notice of their intent to levy. That final notice is key—it also tells you about your right to an appeal or hearing before they seize anything.

Your Right to Appeal and Challenge the Levy

One of the most powerful tools in your toolbox is the right to formally challenge the state’s action. This is usually done by requesting a Collection Due Process (CDP) hearing (or whatever your state calls its equivalent). This isn't just some bureaucratic hoop to jump through; it's a critical moment.

During this hearing, you can:

Challenge the levy itself. Maybe they made a procedural error or it’s simply improper.

Propose a different solution. This is your chance to ask for an installment agreement or an Offer in Compromise.

Question the tax bill itself. You can typically only do this if you haven't had a prior opportunity, like at an audit.

A CDP hearing temporarily freezes the levy process. This gives you precious breathing room to negotiate a solution without the immediate threat of seizure hanging over your head. It shifts the power dynamic from pure defense to proactive problem-solving.

This legal framework is there to protect you from unfair collection tactics. While a state levy is dead serious, these rights give you a formal path to fight back. Understanding how to use these tools is everything, and our guide on how to fight the IRS has some great strategies that often work just as well in state-level disputes. When you know your rights, you can start to take back control and work toward a fair outcome.

Your Action Plan to Resolve a State Tax Levy

When a state tax levy notice shows up in your mailbox, it's time to act. Immediately. This isn't a problem that just goes away on its own—in fact, ignoring it is the fastest way to escalate the situation into a frozen bank account or garnished wages.

The single most important thing you can do is take that first step. Your mission is to get the levy released and figure out a real, sustainable plan to handle the tax debt behind it. The good news? State tax agencies have pathways to help you do just that. Knowing what they are is how you start to take back control.

Explore Your Resolution Strategies

Once you’ve decided to tackle this head-on, it’s time to figure out which solution makes sense for your financial reality. Each option is designed for a different situation, from breaking the debt into manageable chunks to finding relief when you're in serious financial trouble.

Here are the three most common ways to resolve a state tax levy:

Installment Agreement (IA): Think of this as a formal payment plan. You agree to pay off your entire tax bill through regular monthly payments over a set amount of time. It’s a fantastic option if you can afford the total debt but just can't pay it all in one lump sum. As long as you stick to the plan, the state backs off from other collection actions.

Offer in Compromise (OIC): An OIC is a deal that allows you to settle your tax debt for less than you actually owe. States don't hand these out lightly. They're typically for people facing genuine financial hardship who have no realistic way of ever paying the full amount. Be prepared to open up your books and prove your inability to pay.

Currently Not Collectible (CNC) Status: If paying your tax bill would mean you couldn't cover basic living costs—like rent, groceries, or medical care—the state might agree to put your account in CNC status. This hits the pause button on collections, giving you breathing room until your finances improve.

Key Insight: Simply proposing a solution like a payment plan shows the tax agency you’re serious about making things right. That good-faith effort is often enough to stop a levy in its tracks and prevent future seizures.

Taking the Next Steps

Figuring out the right move can feel overwhelming. Each path has its own rules, paperwork, and eligibility requirements. Setting up a payment plan is a very different process from proving the kind of hardship needed for an OIC, for instance.

These strategies often look a lot like their federal counterparts. You can learn a lot by reading about negotiating tax debt with the IRS, since many of the core principles are the same.

To help you get started, here's a quick breakdown of your main options.

Options for Resolving a State Tax Levy

The table below summarizes the most common strategies. Use it to get a quick sense of which path might be the best fit for your circumstances.

| Resolution Method | Best For | Key Consideration |

|---|---|---|

| Installment Agreement | Taxpayers who can pay the full debt over time. | Requires consistent monthly payments to remain in good standing. |

| Offer in Compromise | Those with genuine inability to pay the full tax liability. | Involves a rigorous review of your income, assets, and expenses. |

| Currently Not Collectible | Individuals facing severe, immediate financial hardship. | This is a temporary solution; the debt does not disappear. |

In the end, choosing the right strategy comes down to an honest look at your finances. Acting fast and keeping the lines of communication open with the state are the most powerful tools you have to stop a levy and start down the path to a resolution.

When You Should Hire a Tax Professional

Look, I'm all for handling things yourself, but a state tax levy isn't a DIY project. This is a high-stakes game where one wrong move can set you back years. Knowing when to wave the white flag and call in a pro is one of the smartest things you can do for your financial health.

If the amount of tax you owe is getting into scary territory, it’s time for an expert. Once a debt gets big, it's not just about the original tax anymore—it's a tangled mess of compounding interest and penalties. A seasoned pro knows how to unravel that mess and fight for a resolution you can actually live with.

The same goes if you think the state got it wrong. Maybe they disallowed legitimate deductions or miscalculated something. Disputing their assessment is an uphill battle, and you'll need someone in your corner who can build a solid case, find the errors, and present a defense that the state will actually listen to.

Knowing When to Call an Expert

Not sure if you need to make the call? Here are some dead giveaways that you're in over your head:

You're completely overwhelmed. The stress of a levy is no joke. A good professional takes that weight off your shoulders so you can breathe again.

The debt is snowballing. If penalties and interest are piling up faster than you can track, an expert can often negotiate to get them reduced or even waived.

You're getting the silent treatment. When the state revenue office won't return your calls, a tax pro knows exactly who to contact to cut through the bureaucracy.

You need to file an appeal. This isn't just filling out a form. It's a formal legal process with strict rules and deadlines. You don't want to go into that fight alone.

A tax professional brings two crucial things to the table: objectivity and experience. They don’t get emotional. They just build the strongest possible case and make sure every option—from an Offer in Compromise to a simple Installment Agreement—is on the table.

When you're staring down a levy, hiring help is about more than just getting the state off your back. It’s an investment in your future. Much like preparing for a tax audit, it's about getting your facts straight, presenting them correctly, and ultimately, securing your financial stability.

State Tax Levy FAQs

When you get that notice about a state tax levy, your head is probably swimming with questions. It’s a stressful situation, and you need straight answers. Let's tackle some of the most pressing questions I hear from clients to give you some clarity.

How Long Does a State Tax Levy Last?

This is a big one, and the answer isn't always simple. It really hinges on what, exactly, the state is targeting.

A bank levy is like a lightning strike—it happens once. The state grabs whatever money is in your account on that specific day, up to the total you owe. If the account doesn't have enough to cover the full debt, the levy is done, but you're still on the hook for the rest of the tax bill.

A wage garnishment is a whole different animal. It's a slow, steady drain that stays active, siphoning off a piece of every single paycheck until one of three things happens:

The tax debt is finally paid off in full.

You work out a different deal with the state, like an installment agreement.

The state tax agency officially releases the levy.

Can a State Tax Levy Be Reversed or Released?

Absolutely. But you have to act fast and be proactive. A levy release doesn't make the tax debt disappear, but it does stop the state from actively taking your property.

To get a levy released, you generally have to show the state that the seizure is putting you in an impossible financial spot—an immediate, significant economic hardship. This means proving you can't cover basic living expenses like rent, food, or critical medical care. Another path to release is to set up a formal payment plan, like an installment agreement or an Offer in Compromise.

What Is the Difference Between a State Levy and an IRS Levy?

While they both involve seizing your assets to settle a tax debt, the rulebooks they play by are worlds apart. The IRS has one set of rules that applies nationwide. Simple enough.

But state tax levies? They're governed by the laws of that specific state. That means how much they can take from your paycheck, what assets are off-limits, and even the warning notices you get can be completely different from one state to the next. Don't ever assume the process in California mirrors what happens in New York. Each state has its own playbook.

Trying to figure out a state tax levy on your own is incredibly tough, and a misstep can be costly. At Attorney Stephen A Weisberg, I offer a free, no-obligation Tax Debt Analysis to look at your specific case and walk you through your real options.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034