When Will IRS Garnish Wages? Find Out Now

Few things are more stressful than the thought of the IRS reaching directly into your paycheck. But let's get one thing straight: this doesn't happen out of the blue. An IRS wage garnishment is the last resort, not the first move.

The agency is legally required to follow a very specific, and frankly, slow-moving process. You will get multiple written warnings in the mail, giving you plenty of time and opportunity to resolve the issue long before your pay is touched.

The Path to an IRS Wage Garnishment

Think of an IRS wage garnishment as the final destination on a long road. It’s a predictable journey, and the good news is that the IRS has to post clear signs along the way. Once you know what to look for, you can spot the off-ramps and get yourself heading in a different direction.

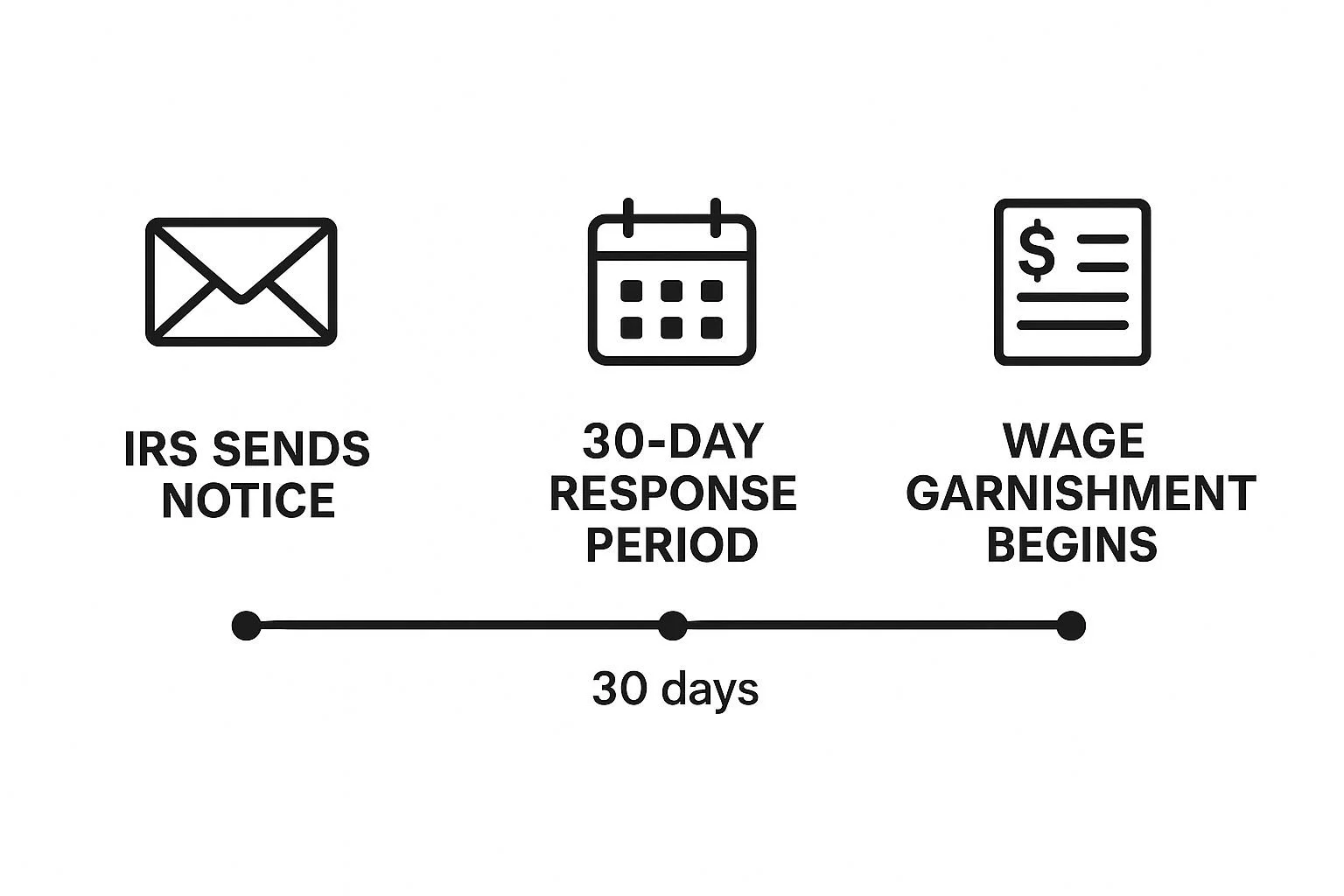

The whole process kicks off well after you’ve filed a return showing you owe money or after the IRS has assessed a tax debt against you for some other reason (like an audit). From there, they must start by simply asking for the money with a series of official notices sent to your last known address.

The Warning Shot Before the Levy

Before the IRS can legally touch your wages, they have to follow a strict sequence of notifications. It all starts with a few letters asking for payment. It's ignoring these letters that escalates the situation and puts a wage levy on the table.

The most critical piece of mail you'll receive is the Final Notice of Intent to Levy and Notice of Your Right to a Hearing. This isn't just another bill. This is the big one. It's the official, legally mandated 30-day warning that the IRS is preparing to take your money.

After sending this final notice, the IRS must give you a 30-day window to respond. This is your last, best chance to officially challenge the action, request a hearing, and work out an alternative before they ever contact your employer.

The process is fairly straightforward, and you have more control than you might think.

As you can see, there's a built-in waiting period designed to give you time to act. To give you a clearer picture, let's break down the typical sequence of events. The timeline isn't set in stone, but it gives you a solid idea of how the process unfolds.

IRS Wage Garnishment Timeline At a Glance

| Event | What It Means for You | Typical Timeframe |

|---|---|---|

| Tax Debt Assessed | The IRS officially records your tax liability. This could be from a tax return you filed or an audit adjustment. | At time of filing or audit finalization |

| First Notice (CP14) | You receive a basic bill in the mail showing the amount you owe, plus penalties and interest. | 1-2 months after assessment |

| Follow-Up Notices | The IRS sends a series of reminder notices (like CP501, CP503) with increasing urgency. | 2-4 months after the first notice |

| Final Notice of Intent to Levy | This is the critical, legally required warning. You now have 30 days to formally respond or appeal. | 4-6 months after the first notice |

| Wage Garnishment Issued | If you don't respond within the 30-day window, the IRS sends a levy notice to your employer. | 30+ days after the Final Notice |

This table shows that from the first bill to the actual garnishment, several months—and several opportunities to intervene—will pass.

Understanding the Legal Framework

The IRS doesn't get to make up its own rules here. Federal law dictates the entire process, and it’s designed to give you fair warning. The agency must send you a Final Notice of Intent to Levy and inform you of your right to a Collection Due Process (CDP) hearing.

This hearing is your chance to formally negotiate a solution and stop the collection process in its tracks. If you let that critical 30-day window lapse without taking action, the IRS is free to issue the levy order. At that point, your employer is legally required to comply and start withholding funds. You can dig into the specifics by reviewing the federal guidelines for garnishment for a more detailed look at the statutes.

How to Recognize an Official IRS Warning Notice

The IRS doesn’t just show up and start taking money from your paycheck. They have a very specific, legally required process of communication, and it all happens through the mail. Think of your mailbox as your own personal early-warning system.

Most letters from the IRS are just informational, but a few key notices are flashing red lights. They’re a clear signal that a wage garnishment could be just around the corner.

Ignoring these letters is the single fastest way to lose control of the situation. Learning to spot the specific notices that mean "act now" is your best defense. This isn't just about opening your mail; it’s about recognizing your last clear chance to deal with the problem before the IRS gets your employer involved.

The Two Most Critical IRS Notices

If you're wondering when the IRS will garnish your wages, the answer is almost always found in two specific documents. These aren't just gentle reminders—they are legally required warnings that start a countdown. When you see one of these in your mailbox, it’s time to pay very close attention.

The most important letters to watch for are:

CP504 Notice of Intent to Levy: This is a serious escalation. It’s the IRS telling you they are getting ready to seize your assets, including your wages. Think of it as the final warning shot before they send the legally binding notification.

Letter 1058 or LT11 (Final Notice of Intent to Levy and Notice of Your Right to a Hearing): This is it. This is the single most critical piece of mail you can get from the IRS regarding collections. This letter officially notifies you of your right to a Collection Due Process (CDP) hearing and, crucially, starts a 30-day clock.

Once you receive a Letter 1058 or LT11, the IRS has officially done its part. They've given you the required legal warning. If you let that 30-day window pass without responding, they are legally free to start the garnishment process and contact your employer.

Seeing a Letter 1058 or LT11 is your final call to action. It empowers you with the right to request a formal hearing, which immediately pauses the collection process and gives you time to negotiate. This 30-day period is your most powerful tool for preventing garnishment.

What to Look For on the Notice

Official IRS notices have distinct features that set them apart from junk mail or scams. The first thing to check is the notice number, which you can almost always find in the top-right corner of the page (e.g., CP504, LT11). The title of the document will also be very clear, stating "Notice of Intent to Levy" or "Final Notice of Intent to Levy."

The letter itself will break down how much you owe, including the penalties and interest that have been added on. Most importantly, the Final Notice will give you explicit instructions on how to request that CDP hearing using Form 12153.

For a closer look at these forms, our ultimate guide for taxpayers on understanding the Notice of Levy has more detailed examples. When you know what to look for, these scary-looking letters transform from a source of anxiety into a clear roadmap for protecting your income.

How Much the IRS Can Legally Take From Your Paycheck

After the shock of getting a garnishment notice, the next question is always the same: "How much are they going to take?" It’s a terrifying thought, but let's clear up a common misconception. The IRS doesn't just pick a number out of thin air and leave you with pennies.

Unlike a private creditor who is typically limited to a simple percentage of your disposable income, the IRS plays by a different rulebook. The amount they can legally garnish is based on a specific formula that hinges on three things: your filing status, how many dependents you claim, and your pay schedule.

This means a single person with no kids will see a very different amount taken from their check compared to a head of household with two children. The law actually requires the IRS to leave you with a base amount of money for living expenses.

Understanding Exempt Income

The entire calculation revolves around the concept of exempt income. Think of this as the protected portion of your paycheck—the amount the IRS is legally forbidden from touching.

Your employer determines this amount by looking up your specific situation in the tables found in IRS Publication 1494. This document is the official playbook for calculating garnishments, and it's what prevents the IRS from taking 100% of your earnings.

The exempt amount is based on your standard deduction plus any dependents you claimed on your last tax return. Your employer does the math, and anything left after subtracting this exempt portion is what the IRS can levy.

The key takeaway is that the IRS cannot take everything. The law ensures you are left with a baseline amount of money determined by your personal situation. This is a critical protection built into the system.

How Filing Status Changes the Calculation

Let's look at how this plays out in the real world. Imagine two people who earn the exact same salary and get paid bi-weekly.

Scenario A: Single Filer, No Dependents A single person has a lower standard deduction. Because of this, their exempt income is also lower, which means the IRS can legally take a larger slice of each paycheck.

Scenario B: Head of Household, Two Dependents Someone filing as head of household with two kids has a much larger standard deduction and more exemptions. Their exempt income is significantly higher, leaving a much smaller portion of their pay available for the IRS to garnish.

The system is designed this way to account for the financial realities of supporting a family. For your employer, this isn't optional; they are legally required to withhold the calculated amount and send it straight to the government. By understanding this formula, you can start to see how a garnishment might actually affect your bottom line, moving you from a place of fear to a position of informed awareness.

How to Stop a Wage Garnishment Before It Starts

Getting a Final Notice of Intent to Levy can feel like a punch to the gut. But it's not over yet. Think of it as the two-minute warning in a football game—it’s your last chance to make a play and change the outcome. You have a 30-day window to act, and making the right move here can stop the IRS collection machine dead in its tracks.

This is the moment to shift from defense to offense. The IRS actually has several well-established programs to help people resolve their tax debt without having to seize their paychecks. Your entire focus should be on getting into one of these programs before that 30-day clock hits zero.

Your Options for Resolving IRS Tax Debt

When you get ahead of the problem and communicate with the IRS, you can often find a resolution that saves you a world of hurt. The key is to officially request an alternative arrangement. While using reliable tax preparation software can help prevent these situations from happening in the first place, once the debt exists, you need a different game plan.

Here are the main paths you can take to head off a wage garnishment:

Installment Agreement (IA): This is the most straightforward and common solution. An IA is simply a formal payment plan with the IRS, allowing you to pay your debt over time in manageable monthly chunks. As long as you keep up with your payments, they won't touch your wages.

Offer in Compromise (OIC): An OIC is a powerful tool that allows certain taxpayers to settle their tax liability for less than the full amount owed. It's not for everyone, though. This option is generally reserved for people facing true financial hardship, and the IRS uses a strict pre-qualifier tool to see if you're even eligible to apply.

Currently Not Collectible (CNC) Status: If you can prove to the IRS that you can't even afford basic living expenses, let alone a tax payment, they might place your account in CNC status. This is a temporary pause on all collections, including wage garnishments, that lasts until your financial situation gets better.

The Most Powerful Defensive Move

Those options are your end goals, but there’s one specific action you can take that legally freezes the entire collection process. It's your single most powerful tool for self-defense.

Requesting a Collection Due Process (CDP) hearing is the absolute best way to stop an impending wage garnishment. You have to file Form 12153 within the 30-day window after receiving your Final Notice. The second the IRS receives this form, they are legally forbidden from levying your wages while your case is reviewed by the Independent Office of Appeals.

A CDP hearing isn't just a way to buy time; it's your formal right to negotiate. It forces the IRS to come to the table and gives you the crucial breathing room to work out one of the solutions we just talked about, like an Installment Agreement.

Ultimately, the right path forward depends entirely on your finances. A person with a stable income might find an Installment Agreement is the perfect fit. Someone else, buried under debt with few assets, might be a candidate for an Offer in Compromise. The most important thing is to do something. Doing nothing is the only choice that guarantees your wages will be garnished.

What To Do If Your Wages Are Already Being Garnished

That heart-stopping moment when you see your paycheck and realize the IRS has taken a huge chunk of it is something no one should have to experience. It’s a gut punch. You feel powerless, panicked, and maybe even a little hopeless. But here’s the most important thing to remember: this is not a permanent state of affairs. You have options. The key is to take swift, decisive action to get your full paycheck back.

Even though the levy is already active, the game plan doesn't really change. The solutions available now are the same ones that were on the table before the garnishment hit. Your mission is simple: get in touch with the IRS, work out a different way to pay, and get them to release the levy.

Taking Action to Release the Levy

The first move is always to open a line of communication. You—or a tax professional representing you—need to get on the phone with the IRS and start negotiating. The goal is to swap out that painful garnishment for something you can actually live with, like a formal Installment Agreement.

Once you and the IRS reach an agreement, they will send Form 668-D, Release of Levy/Release of Property from Levy, to your employer. This is the official document that tells your HR department to stop the withholding. It’s not an overnight fix, but it's the direct path to reclaiming your income.

It's a common and dangerous myth that once a wage garnishment starts, you're stuck with it until the debt is paid. Absolutely not true. By proactively engaging with the IRS and setting up an alternative payment plan, you can stop the bleeding and get the levy released.

The Power of Demonstrating Economic Hardship

One of your strongest arguments is proving that the garnishment is causing economic hardship. If the amount they're taking makes it impossible for you to cover basic needs—we’re talking rent, groceries, utilities, or critical medical bills—the IRS has the authority to reduce or even temporarily pause the levy. This can provide the crucial breathing room you need to get back on your feet.

To make this case, you'll have to lay your financial cards on the table using Form 433-F, Collection Information Statement. This form is a detailed snapshot of your income, assets, and monthly expenses. A carefully completed statement can paint a clear picture for the IRS, showing them why the current situation just isn't sustainable for you or your family.

And if paying the full debt seems impossible, don't give up. An IRS Offer in Compromise is a complete guide to settling for less than you owe and could be the right move if you qualify. Keep in mind, IRS enforcement actions are part of a massive, well-oiled collection machine.

While the government doesn't publish exact numbers on how many people are garnished each year, its ability to collect trillions in taxes is powered by these very tools. This incredible scale underscores why it’s so important to act. The system is designed to collect, but it also has built-in relief valves for taxpayers who step up and engage. You can get a sense of the sheer scope of IRS operations by looking at their official data and reports.

Frequently Asked Questions About IRS Garnishments

Even after you understand the basics, the reality of an IRS wage garnishment brings up a lot of specific, practical questions. When you're staring down the possibility of a levy, you want to know exactly how it’s going to impact your daily life and your job.

Let's walk through some of the most common concerns I hear from clients. Getting clear, straightforward answers is the first step toward finding some peace of mind.

What Is My Employer's Role in a Wage Garnishment?

Once the IRS sends Form 668-W, the official wage levy notice, your employer stops being a bystander and becomes a legally mandated participant. They don't have a choice in the matter; they are required by law to comply with the order.

Their job is to take the calculation tables provided by the IRS, figure out how much of your paycheck is not exempt, and start withholding that amount immediately. They will send those funds directly to the IRS from every single paycheck until they get an official release. That release comes in the form of Form 668-D, Release of Levy.

How Long Does an IRS Wage Garnishment Last?

This is a crucial point: an IRS wage garnishment isn’t a one-and-done deal. It’s a continuous levy that latches onto your income and stays there indefinitely. It won't just stop after a few paychecks or a certain dollar amount is met.

The garnishment only ends when one of three things happens:

The entire tax debt, including all the painful penalties and interest, is paid in full.

You work out an alternative resolution with the IRS (like an Installment Agreement), and they formally issue a levy release.

The ten-year statute of limitations for collecting the debt expires, which is a very rare outcome and not something to bank on.

The bottom line is you have to take action to make it stop. The IRS has several programs available, and our guide to tax debt solutions can help you start exploring which one might be right for you.

Will I Lose My Job if the IRS Garnishes My Wages?

Absolutely not. Federal law provides a critical protection here. The Consumer Credit Protection Act (CCPA) makes it illegal for an employer to fire you because of a single wage garnishment.

An IRS levy is something most competent HR and payroll departments have seen before. They know how to handle it professionally and confidentially. It really shouldn't put your job in jeopardy. One small caveat: this protection specifically covers a single garnishment. If you have multiple, separate garnishments from different creditors, the situation can get more complicated.

Key Takeaway: An IRS wage garnishment is a serious financial problem, but it is not grounds for termination. Federal law protects your job from a single levy, giving you the stability you need to tackle the tax issue itself.

Can the IRS Garnish My Social Security or Disability Income?

Yes, unfortunately, the IRS has the power to take a portion of certain federal payments. Through a system called the Federal Payment Levy Program (FPLP), they can directly levy Social Security retirement and disability benefits.

However, there are important limits. The IRS can generally take up to 15% of your monthly Social Security benefits. But, and this is a big one, they are legally forbidden from touching Supplemental Security Income (SSI) payments at all. Knowing which income is vulnerable and which is protected is a vital part of planning your defense.

If you're facing a potential wage garnishment, you don't have to navigate the complex IRS system alone. At Attorney Stephen A Weisberg, we start with a free, no-obligation tax debt analysis to determine the best path forward for your specific situation.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034