Your Guide to IRS Form 433 A OIC

IRS Form 433-A (OIC) isn't just another tax form. Think of it as the complete financial story you’re telling the government—it’s the primary evidence you'll use to prove you simply can’t afford to pay your tax debt in full. It’s the cornerstone of your entire Offer in Compromise.

Why Form 433-A OIC Is So Critical for Your Tax Settlement

Before you even think about filling out a single line, it’s vital to understand what this form represents to the IRS. For most people, an OIC is filed based on "doubt as to collectibility," which is just the IRS's way of saying there’s a real question about whether they could ever collect the full amount you owe. Form 433-A (OIC) is how you prove that.

This document lays out your entire financial picture—every dollar you earn, every necessary expense you have, and every asset you own. The IRS pores over this information to calculate one single, all-important number: your Reasonable Collection Potential (RCP).

Getting this number right is everything.

Key Takeaway: Your RCP is what the IRS determines it could realistically get from you. For your OIC to even be considered, your offer amount must meet or exceed this figure. No exceptions.

The Foundation of Your Offer

Let me be clear: the IRS doesn't just take your word for it. They will verify everything. The numbers you put on Form 433-A (OIC) are cross-referenced with public records and other third-party data. This is why total accuracy and honesty are non-negotiable. One mistake can sink your entire offer.

The stakes are high. In 2020, for example, the IRS accepted about 18,000 OICs out of roughly 54,000 applications—that's a success rate of only 33%. What separates an accepted offer from a rejection letter often comes down to how well this form is prepared.

Ultimately, a well-prepared Form 433-A (OIC) clearly demonstrates two things:

Your current financial situation makes it impossible to pay your full tax liability.

Your offer represents the most the IRS could ever hope to collect from you.

A Quick Look at Key Form 433-A OIC Sections

To give you a better idea of what you're up against, here's a breakdown of the main sections of the form and what the IRS is looking for in each. They're building a complete financial profile, so every piece matters.

| Section Number | Section Title | What You Need to Disclose |

|---|---|---|

| Sections 1-3 | Personal & Business Info | Basic identifying details for you, your spouse, and any dependents. Includes business ownership details. |

| Section 4 | Assets | A full accounting of everything you own: cash, bank accounts, investments, real estate, vehicles, and other property. |

| Section 5 | Income | All sources of monthly income for your entire household, from wages and self-employment to pensions and social security. |

| Section 6 | Monthly Living Expenses | A detailed list of your necessary living costs, like housing, food, transportation, and healthcare. |

Getting these sections right is the first step. The IRS uses this raw data to build its calculation, so accuracy is your best friend here.

Doubt as to Collectibility

When you file an OIC based on "doubt as to collectibility," you're making a specific claim: you don't have the income or assets to pay your tax debt, either now or in the foreseeable future. For individual taxpayers, Form 433-A (OIC) is the only way to prove it.

Every number, from your grocery budget to your car's trade-in value, directly impacts the final RCP calculation.

A sloppy or poorly documented form can easily lead to an inflated RCP. If that happens, you’re looking at an immediate denial or a counteroffer that’s just as unaffordable as the original debt.

For a deeper dive into whether you're a good candidate for this program, you can explore our guide on how to qualify for an Offer in Compromise.

Assembling Your Financial Documents for the IRS

When you're preparing a form 433 a oic, accuracy comes down to one thing: solid documentation. I’ve seen it time and again—people try to fill out this beast of a form from memory, and it almost always leads to mistakes, red flags, and a swift rejection from the IRS.

Don't think of this as just gathering paperwork. You're building a case for yourself. Every document is a piece of evidence that validates your financial picture.

The goal is to paint a clear, consistent, and verifiable story that leaves an IRS examiner with no questions or doubts.

The Core Documentation Checklist

Before you even think about putting pen to paper (or fingers to keyboard), your first job is to get all your financial records in order.

The IRS typically wants to see everything from the last three to six months before you file your OIC.

This gives them a snapshot of your recent financial life and shows that your situation is stable, not just a momentary blip.

Here’s the essential list to get you started:

Proof of Income: This means recent pay stubs for everyone in the house who works, profit and loss statements if you're self-employed, and statements for any other income like Social Security, pensions, or unemployment.

Bank Statements: You'll need the last three to six months of statements for every single checking and savings account you have. Be ready to explain any big deposits or withdrawals that look out of the ordinary.

Investment and Retirement Account Statements: Pull the most recent statements for your 401(k)s, IRAs, brokerage accounts, and anything else you have invested.

Real Estate Information: Grab your latest mortgage statements, property tax bills, and a current market analysis to show what your home is worth and what you still owe.

Vehicle Information: Dig up the loan or lease statements for your cars, trucks, or motorcycles. You’ll also need to figure out their current fair market value—a quick search on a site like Kelley Blue Book usually does the trick.

Expert Tip: Do yourself a huge favor and organize everything into folders—physical or digital—by category and date. This simple bit of prep work will save you a massive headache later and keep you from mixing things up.

Documenting Your Expenses and Valuations

Just saying you spend a certain amount on something isn't good enough for the IRS. You have to prove it. While the IRS has standard allowances for many basic living costs, you’ll need solid proof for any expenses that go above those standards or are unique to your situation.

The level of detail required is similar to any official government filing. For instance, this guide to faxing government forms without errors highlights just how crucial clarity and completeness are.

To make sure your numbers on the form 433 a oic are bulletproof, pay special attention to these areas:

Significant Medical Costs: Collect every bill, receipt, and insurance statement for ongoing medical treatments or prescriptions that aren't fully covered.

Tuition and Education Costs: Have the invoices and payment confirmations for any necessary school expenses for you or your kids.

Childcare or Dependent Care: Get contracts or detailed receipts from your daycare or provider showing the monthly cost.

This isn't just about checking boxes for the IRS; it's about building your credibility. When the numbers on your form line up perfectly with the documents you provide, it signals to the examiner that you're being transparent.

Any discrepancy, no matter how small, can trigger a deeper audit and sink your entire Offer in Compromise. To get a full picture, you can dig into the specifics of IRS Form 433-A and its requirements.

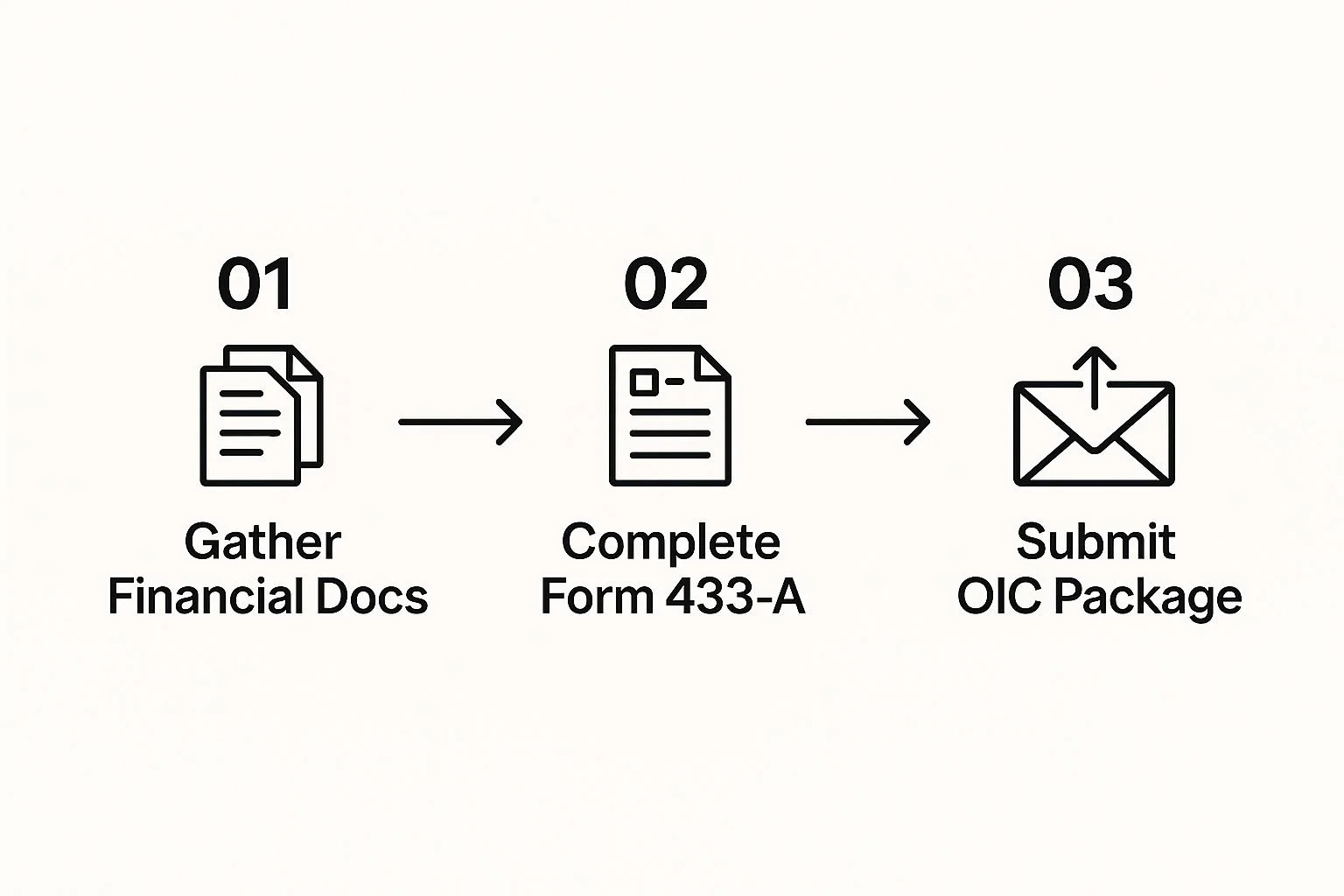

A Practical Walkthrough of Each Form Section

Opening up Form 433-A (OIC) can feel like trying to solve a puzzle in another language. Every section demands incredibly specific details, and how you frame that information can make or break your Offer in Compromise.

Let's walk through it, translating the IRS-speak and flagging the spots where I've seen taxpayers get tripped up time and again.

The goal here is simple: paint a picture of your financial situation with complete transparency and honesty. This builds your credibility with the IRS examiner and gives them a clear, straightforward look at your circumstances—which is precisely what you need.

This visual guide breaks down the core process into three key stages.

As you can see, the path from gathering your documents to the final submission really highlights how completing the form itself is the most intensive part of the entire OIC journey.

Navigating Personal and Business Information

At first glance, Sections 1 through 3 seem easy enough. This is where you put your personal details, dependents, and any business interests. But don't just fly through it. If you’re self-employed or run a sole proprietorship, you need to be meticulous.

Double-check that every piece of information perfectly matches what’s on your most recent tax return. A simple mismatch—like an old address or a slightly different business name—is a small but avoidable red flag that can create needless delays.

Section 4: Unpacking Your Assets

This is it. This is the section of the form that gets the most intense scrutiny. The IRS needs a full accounting of everything you own, down to the last dollar. Misrepresenting or lowballing your assets is one of the quickest tickets to having your OIC flat-out rejected.

Let's look at a real-world scenario: You have an old 401(k) from a job you left years ago. It has a balance of $8,000. It’s easy to forget about or assume it doesn't count. But the IRS already knows it’s there—they get copies of forms 1099-R and 5498.

Instead of leaving it off, you list it accurately. Then, you can attach a separate statement explaining that cashing it out would trigger steep taxes and penalties, which reduces its actual contribution to your ability to pay. This is both honest and strategic.

Remember, your assets go far beyond what's in your checking account. Be ready to detail:

Cash on Hand: Be realistic. Listing $0 looks suspicious because the IRS knows everyone keeps some cash for daily expenses.

Investments: This means all stocks, bonds, and mutual funds. You’ll need to provide their current market value.

Real Estate: You must list the current fair market value, not what you originally paid. Getting a comparative market analysis from a realtor is a great piece of documentation to have.

Vehicles: Use a reliable source like Kelley Blue Book to find the private party sale value. Don't use the trade-in value, which is almost always lower.

Personal Property: For things like furniture, electronics, or jewelry, a reasonable "garage sale" value is what they're looking for. The IRS isn't expecting you to get your couch professionally appraised.

Expert Tip: When listing retirement accounts, always provide the current balance and be ready to show the "quick sale value." This is the net amount you'd actually pocket after paying taxes and penalties if you were forced to liquidate it today. It’s a much more realistic number for calculating your ability to pay.

The whole process of completing Form 433-A (OIC) is a meticulous exercise. You’re providing a sworn statement about your income, assets, and liabilities—covering everything from cash and bank accounts to investments and retirement plans.

The form must be signed under penalties of perjury, which just hammers home how critical total accuracy is. You can find more details in the official IRS instructions.

Section 5: Reporting Your Household Income

Now we get to the money coming in. This section demands a complete snapshot of every dollar that enters your household each month.

If you have a standard W-2 job with a steady paycheck, this part is fairly simple. But for freelancers, gig workers, and small business owners, it gets tricky.

You can't just pick a good month or pull a number out of thin air. The IRS wants to see a realistic monthly average, which usually means you'll need to average your earnings over the last six to twelve months.

Consider this self-employment scenario: A freelance graphic designer’s income goes up and down. One month, she brings in $6,000, but the next, it’s only $2,500.

Wrong Way: Listing $6,000 as her monthly income. This inflates her ability to pay and will be immediately contradicted by her bank statements.

Right Way: She adds up her income from the past six months (let's say it's $24,000 total) and divides by six to get a monthly average of $4,000. She then attaches a simple profit and loss statement showing her math.

This approach is defensible. It proves to the IRS examiner that you're being thorough and giving them an honest look at your financial reality. Don't forget to include income from all sources for everyone in the household—the IRS is evaluating your entire family unit's ability to pay.

Calculating Your Income and Expenses Like an IRS Agent

This is it. The income and expense sections of your Form 433-A OIC are where your entire Offer in Compromise is won or lost. I can't stress this enough.

This isn't just about jotting down a budget; it's a forensic accounting exercise that determines your official "ability to pay." One small mistake here, one misinterpretation, and your offer is dead on arrival.

Your mission is to present these numbers exactly as an IRS agent would see them. That means you have to get out of your own head, stop guessing, and start using the agency’s own rigid logic and standards to build your case.

Decoding Your Total Monthly Income

First up, income. The IRS wants to know your average gross monthly income, which can get complicated fast if you don't have a steady, predictable paycheck.

If you've got fluctuating income from seasonal work, sales commissions, or a side hustle, you absolutely cannot just list your best month's earnings.

That’s an instant red flag that will torpedo your offer by making it look like you can afford to pay way more than you actually can.

What you need is a credible, defensible average. In most cases, that means averaging your income over the last three to six months.

Let's look at a real-world scenario. Imagine a rideshare driver with these earnings over the last three months:

Month 1: $3,200

Month 2: $4,500 (a fantastic, but unusual, month)

Month 3: $2,800

He can't put down $4,500. Instead, he needs to calculate the average: ($3,200 + $4,500 + $2,800) / 3 = $3,500. That $3,500 is the number he reports on the form, and he'll have the bank statements and platform reports to back it up.

The Hard Truth About Allowable Living Expenses

This is the single biggest trap taxpayers fall into. You don’t get to list what you actually spend every month. The IRS couldn't care less about your actual spending habits. They have a strict, non-negotiable set of standardized living expense amounts, known as the National and Local Standards.

These standards put a hard cap on what the IRS will allow for basic necessities across three main categories:

Food, Clothing, and Miscellaneous: A single, nationwide number that depends on your income and the number of people in your household.

Housing and Utilities: This is a local standard that changes by county. It's meant to cover everything from rent or mortgage payments to property taxes, insurance, gas, electric, and basic maintenance.

Transportation: This has two components—a national figure for vehicle ownership costs (car payments, insurance) and a local figure for operating costs (gas, repairs) that varies by metro area.

Key Insight: You have to look up these figures on the IRS website for your specific county and family size. If you list your actual expenses and they're higher than these standards, the IRS will simply ignore your numbers and plug in their own, unless you have an extraordinary, well-documented reason.

Trying to justify expenses above these standards is an uphill battle. It's not enough to say, "My rent is high." You have to prove why that specific expense is absolutely necessary and unavoidable.

For a deeper dive into how these standards fit into the overall calculation, take a look at our complete guide to IRS Offer in Compromise settlements.

Justifying Expenses Above the IRS Standards

Let's say the local housing and utility standard for your county is $2,200 a month, but your mortgage and bills actually come out to $2,600. To have any chance of getting the IRS to allow that higher amount, you need bulletproof documentation.

This might mean showing evidence that a child's medical condition requires them to live in a specific school district where housing costs are higher. Simply wanting to live in a nicer part of town will get you nowhere.

It's a similar story for healthcare. The IRS allows you to claim the actual amount you pay out-of-pocket for things like health insurance premiums or ongoing prescription costs.

But "claim" is the key word—you need ironclad proof. Receipts, insurance statements, and letters from doctors are not optional; they are required.

Calculating Your Disposable Income

After all that work, the final calculation is straightforward but incredibly powerful. To truly understand what the IRS believes you can pay, you have to calculate disposable income using their formula.

Total Monthly Income - Total Allowable Expenses = Monthly Disposable Income

This one number is the bedrock of your Offer in Compromise. The IRS will multiply this figure by either 12 or 24 (depending on the payment terms you propose) to arrive at the minimum offer they'll even consider.

If you have a positive disposable income, that money has to be part of your offer. If the number is zero or negative, you're in a much stronger position to argue that you simply can't afford to pay the tax debt.

Common Mistakes and Tips for a Stronger Application

I've seen far too many Offer in Compromise applications get rejected for simple, avoidable mistakes—not because the taxpayer didn't deserve a break. A single error on your form 433 a OIC can torpedo your entire case before an IRS agent even gives it a serious look.

Think of this section as your final quality check. It's your last chance to spot the red flags an IRS examiner is trained to find. Even if your financial situation clearly justifies an OIC, a sloppy application sends a bad signal.

It suggests you're disorganized, careless, or worse, trying to hide something. Let's walk through the most common pitfalls I see and how to build a case that sails through the review process.

Inconsistency Is the Enemy

If there's one golden rule, it's this: everything must be consistent. The numbers need to tell one clear, cohesive story. The income you list in Section 5 has to perfectly match the deposits on your bank statements.

The value of your car in Section 4 must be a reasonable figure you can back up with a source like Kelley Blue Book.

Any discrepancy, no matter how small, creates doubt. For instance, if your pay stubs show a net monthly income of $4,000, but your bank statements only show $3,500 in deposits, you need a rock-solid explanation.

Maybe $500 is automatically deducted for a loan payment you didn't list elsewhere. If you don't explain that, the IRS examiner is left to assume the worst.

Expert Tip: Before you seal the envelope, lay everything out side-by-side. Compare your bank statements, pay stubs, and the figures on your form 433 a oic. A simple math error can sink you before you even get started.

Miscalculating and Misrepresenting

You'd be surprised how often basic arithmetic errors derail an application. These are completely avoidable. To ensure your figures are accurate, you might find some tips on mastering data integrity through Excel data validation helpful for organizing everything before you even touch the form.

Beyond bad math, certain strategic mistakes are just as damaging. Here are a few I see all the time:

Understating Asset Values: Don't value your car at its "trade-in" price. The IRS uses fair market value, and they have access to the same valuation tools you do.

Forgetting Assets: That old 401(k) from a job you left five years ago? It absolutely counts. The IRS already knows about it from Form 5498 filings, so leaving it out is a major red flag.

Failing to Explain Large Transactions: Did a family member gift you $5,000 three months ago? You have to disclose it and explain what it was for. Otherwise, it just looks like you're hiding income.

These aren't just minor details; they go straight to your credibility.

Transparency and Professionalism

Your entire OIC package needs to look professional. From the form itself to every supporting document, it should be neat, organized, and easy for the examiner to navigate. Please, don't just shove a stack of crumpled receipts into an envelope.

Make the examiner's job easy. Use paper clips to group related documents, like pay stubs with their corresponding bank statements. If your situation is complicated, attach a brief, clearly written letter explaining the key points.

This level of organization does more than just look good—it shows you respect the process and the examiner's time. That can build crucial goodwill right from the start.

Remember, the OIC process can drag on for months, sometimes over a year. A clean, well-organized file helps prevent needless delays.

A rejected OIC puts you right back at square one, and you could be facing aggressive collections again. If you're dealing with immediate threats, you should check out our guide on how to stop IRS wage garnishment while your case is pending.

Ultimately, the strongest applications are always the ones that are transparent and meticulously prepared.

Common Questions (and Crucial Answers) About Form 433-A OIC

Even after you've wrangled all your documents and stared at the Form 433-A OIC for hours, a few tricky questions always seem to pop up. These "what-if" scenarios aren't always spelled out in the official instructions, but getting them wrong can sink your entire offer.

Let's clear up some of the most common points of confusion I see when helping clients with their Offers in Compromise.

What Happens If I Forget to Include an Asset?

Forgetting to list an asset on your OIC is a huge mistake, even if it's an honest one. From the IRS's perspective, it looks like you're trying to hide something, and that’s a fast track to rejection. It can even lead to penalties.

The worst-case scenario? The IRS accepts your offer, and then they discover the forgotten asset down the road. They have the right to completely cancel the deal, putting you right back where you started with the full tax debt.

It's always, always better to over-disclose. If you realize you made a mistake after filing, you need to contact the IRS immediately to amend your form.

Do I Have to Include My Spouse's Finances?

Yes. This is a non-negotiable for most people. The IRS wants to see the full financial picture of your household, not just the person who technically owes the tax. It doesn't matter if your spouse has zero tax debt to their name.

The form is built for this, with columns for both you and your spouse. Their income, assets, and expenses are all part of the calculation the IRS uses to determine your true ability to pay on the Form 433-A OIC.

Important Takeaway: Think of it from the IRS's point of view. They aren't just looking at an individual; they are evaluating an economic unit. Your household's combined finances determine what they believe you can afford to pay.

How Does the IRS Actually Verify My Information?

The IRS absolutely does not just take your word for it. They have a massive system for cross-referencing every number you put on that form.

Third-Party Data: They'll immediately compare your submission to the W-2s, 1099s, and other records they get from employers, banks, and brokerages.

Public Records: Information about property you own, cars you've registered, or business licenses you hold is all public information they can easily pull.

Your Own Documents: The agent assigned to your case will pour over the bank statements, pay stubs, and other proof you submit, hunting for any discrepancies.

A major mismatch between your form and their data is an instant red flag that will derail your application. This is exactly why 100% accuracy isn't just a goal—it's a requirement.

Feeling overwhelmed by your tax situation? At Attorney Stephen A Weisberg, I provide a FREE Tax Debt Analysis to determine exactly how I can help before you commit to anything.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034