Can the IRS Take Your Car? Know Your Rights & Protections

Think of it as the end of a very long road. It's not something that happens out of the blue. By the time an IRS agent shows up to take your vehicle, you will have received a mountain of notices and had plenty of opportunities to get things right. It is never a surprise event.

Understanding IRS Asset Seizure

The idea of the government seizing your property is downright scary, but it's crucial to understand the process. The IRS doesn't just decide to take your car on a whim. This power, known as a levy, is the legal seizure of your property to satisfy a tax debt. It’s their final, most aggressive collection tool.

And they're using it less and less. While the authority exists, the actual practice is rare. The IRS conducted only 89 seizures in fiscal year 2022.

That’s a staggering 79% drop from the 426 seizures they carried out back in fiscal year 2015. So, while it's possible, it's highly improbable for the average taxpayer.

Distinguishing a Lien from a Levy

People often mix up "lien" and "levy," but they are two completely different things in the IRS's toolbox. Knowing the difference is critical.

An IRS Lien is a legal claim. It’s the government publicly saying, "This person owes us money, and we have an interest in their property." It's like a cloud on your title. The lien secures the debt and alerts other creditors, but you still own and possess the property.

An IRS Levy is the actual seizure. This is when the IRS physically takes your property to sell it. A lien is a claim; a levy is the enforcement of that claim.

Let’s break it down to make it crystal clear.

IRS Lien vs IRS Levy At a Glance

Here’s a simple table to help you keep these two actions straight.

| Action | What It Is | Impact on Your Property |

|---|---|---|

| IRS Lien | A legal claim against your property to secure a tax debt. | You keep your property, but the lien attaches to it, affecting your ability to sell or borrow against it. |

| IRS Levy | The actual, physical seizure and sale of your property. | The IRS takes possession of your property to sell it and pay off your tax bill. You lose ownership. |

Ultimately, a lien is a warning shot, while a levy is the direct hit.

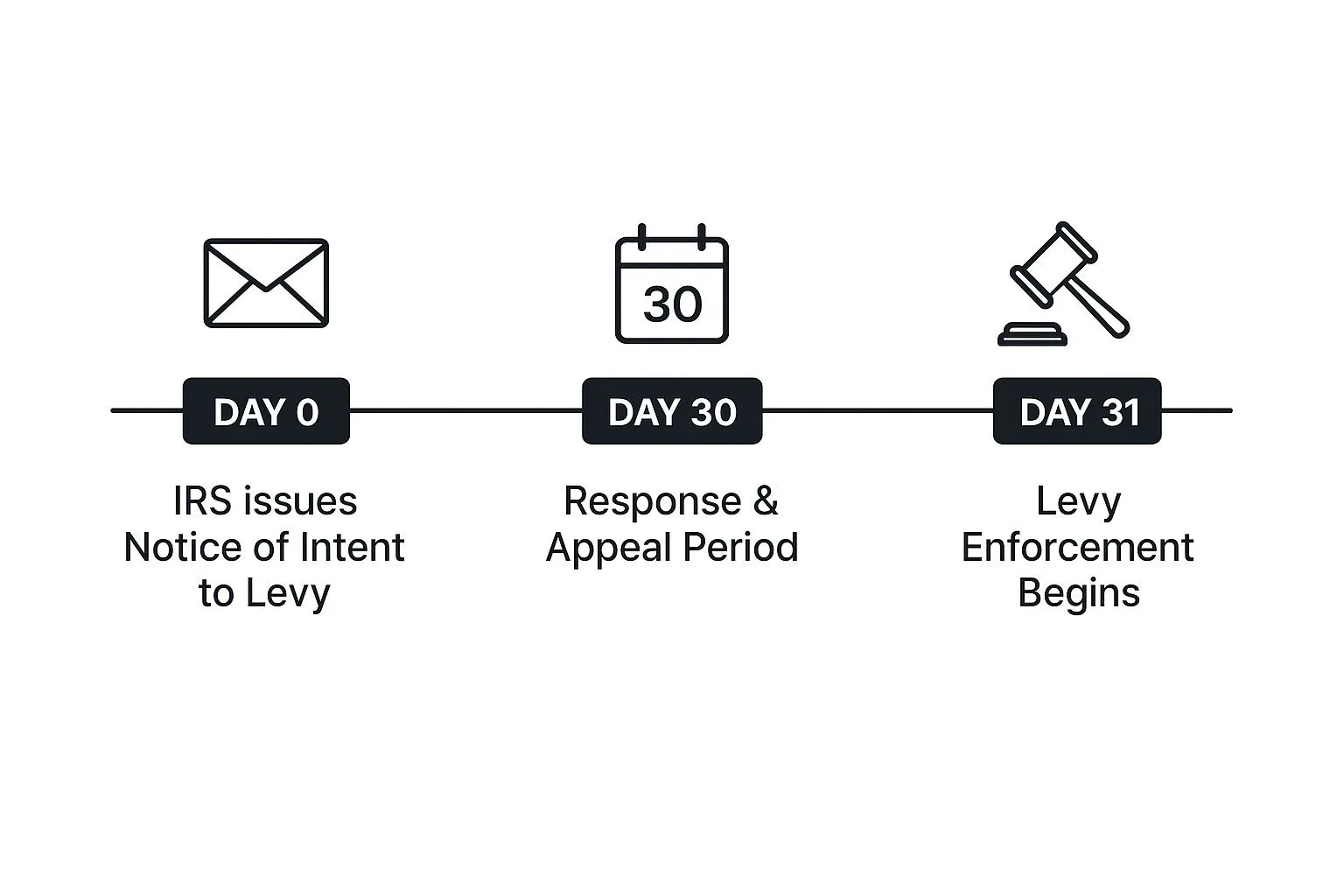

Before the IRS can move forward with a levy on your car, they are required by law to send you a "Final Notice of Intent to Levy and Notice of Your Right to a Hearing." This is your final warning, and it gives you 30 days to respond. This notice is your chance to stop the process cold by requesting an IRS Collection Due Process hearing and fighting back.

The Path to an IRS Vehicle Seizure

Let's be clear: the IRS doesn't just show up one morning and tow your car out of the blue. A vehicle seizure is the last resort, the final stop on a long road paved with official warnings and multiple off-ramps for you to resolve the issue.

Think of it like the warning lights on your car’s dashboard. The first light flickers on when a tax debt is assessed and goes unpaid. That’s just the system acknowledging a problem exists. If you ignore it, more lights start flashing.

The Paper Trail of Warning Notices

Before they can touch your property, the IRS is legally required to follow a very specific, escalating communication process. They can’t just send a tow truck; they have to send a series of letters first, each one getting progressively more serious.

You’ll likely get a few initial reminders, like a CP501 (Notice of Tax Due) or a CP503 (Second Reminder). But things get real when a CP504 Notice of Intent to Levy arrives.

This isn't just a friendly reminder; it's a statutory notice that the IRS is now officially preparing to seize assets if you don’t pay up or make other arrangements.

The one you absolutely cannot ignore is the Letter 1058 or LT11, formally titled "Final Notice of Intent to Levy and Notice of Your Right to a Hearing."

This is it—the final, official warning. It explicitly states the IRS intends to seize your property (including your vehicle) and, crucially, it starts a 30-day countdown for you to appeal the action.

Ignoring this final notice is the single biggest misstep that leads directly to a seizure. It’s your most important and powerful chance to hit the brakes.

That Critical 30-Day Window

Once that Final Notice lands in your mailbox, a clock starts ticking. You have exactly 30 days to request what's called a Collection Due Process (CDP) hearing. This is a powerful legal right that puts an immediate freeze on most collection actions—including seizing your car—while your case is reviewed.

This simple timeline shows just how critical that window is.

As you can see, your action within those first 30 days is the firewall standing between the IRS and your vehicle.

A CDP hearing is your formal opportunity to negotiate. You can propose alternatives like an installment agreement or an offer in compromise.

But if you let that 30-day deadline pass without requesting a hearing, you've essentially given the IRS the green light to move forward. Knowing this timeline is the key to navigating away from the cliff's edge.

When the IRS Decides to Seize a Car

Just because you owe the IRS doesn't mean they'll show up with a tow truck tomorrow. Seizing your car isn't personal; it’s a business decision.

Think of the IRS like a collection agency with a budget. Before they take an asset, they have to ask themselves one simple question: Is it worth the hassle?

Seizing a car is a surprisingly expensive and time-consuming process for the government. They have to pay for towing, storage, all the administrative paperwork, and the costs of running a public auction. It all adds up.

The IRS will only move forward if they believe the sale of your car will bring in enough cash to cover all those expenses and put a real dent in your tax bill.

This all comes down to one critical word: equity. Equity is just the gap between what your car is worth on the open market and what you still owe on your auto loan. If there's little or no equity, your car is essentially worthless as a seizure target.

The Financial Logic Behind a Seizure

To figure out if your car is at risk, you have to learn to think like an IRS Revenue Officer. They're looking for the low-hanging fruit—assets that are easy to liquidate and will bring in a decent return.

Let’s walk through a couple of scenarios to see this in action:

Scenario A (High Risk): You have a $50,000 tax debt and own a pickup truck, free and clear, that's worth $30,000. This vehicle is a prime target. It’s loaded with equity, there's no car loan to pay off first, and selling it would knock down your tax debt substantially.

Scenario B (Low Risk): You owe $5,000 in taxes and drive a sedan worth $15,000, but you still have a $14,000 loan on it. Your equity is a mere $1,000. By the time the IRS pays the auction house and the tow truck driver, there'd be pocket change left to put toward your tax bill. This seizure simply makes no financial sense for them.

The core takeaway is that the IRS isn't interested in seizing assets just for show. A vehicle seizure is a collection tool. If it won't effectively collect a meaningful amount of money, they'll usually move on to other methods, like a wage garnishment.

The IRS even has its own internal rules for this. Generally, they won't target a vehicle unless the tax debt is over $5,000. They overwhelmingly focus on cars that are paid off because lenders always get their cut first from any sale.

If you find yourself in a high-risk spot like Scenario A, it's absolutely critical to act fast. You may be able to protect your assets by negotiating a settlement before things escalate. One of the most powerful tools for this is an Offer in Compromise to settle your tax debt, which could resolve the issue for good.

Are Some Vehicles Safe From IRS Seizure?

Even with its far-reaching powers, the IRS doesn't have a blank check to seize any vehicle it wants. There are specific legal shields you can use, but the key is that you have to be the one to raise them. These protections aren't automatic; you must proactively make your case to the IRS.

The whole point behind these exemptions is to stop a seizure from turning a bad financial situation into a full-blown disaster for your family. The law gets that taking away someone's only way to earn a living or manage basic needs doesn't help anyone—it just digs a deeper hole.

The "Tools of a Trade" Exemption

One of the strongest arguments you can make is the "tools of a trade" exemption. If your vehicle is truly essential for you to do your job—not just for getting to the office, but as a direct instrument of your business—it might be off-limits.

Imagine a self-employed electrician whose van is packed with specialized equipment, or a freelance caterer who needs their specific truck for deliveries. In situations like that, the vehicle is fundamental to earning a living.

But there's a catch. This protection has a dollar limit. For 2024, the exempt amount is just $4,860. If the equity in your work vehicle is worth more than that, the IRS can still seize it, sell it, and hand you back the exempt portion.

Arguing Economic Hardship

Another powerful defense is claiming the seizure would create a significant economic hardship. This argument is all about showing that losing your car would make it impossible for you to cover basic, necessary living expenses for yourself and your family.

To win this argument, you need to bring solid proof to the table. This is about necessity, not just convenience.

Medical Needs: Is the vehicle absolutely essential for getting a family member to dialysis or other critical medical treatments?

Lack of Alternatives: Can you show there's no public transportation available that would let you get to work or the grocery store?

Childcare Duties: Is the car the only way to get your kids to school or daycare so you can work?

You have to paint a clear picture for the IRS, demonstrating that taking your car would do more than just make your life harder—it would actively prevent you from maintaining a basic standard of living. It takes detailed financial proof and a compelling story, but it's a legitimate and often successful argument against seizure.

How to Proactively Stop the IRS From Taking Your Car

When it comes to the IRS, the best defense is a good offense. Don't wait for threatening notices to pile up. Taking proactive steps is the single most effective way to keep control of the situation and protect your property.

Here's the thing—the IRS would much rather work with you than against you. They see taxpayers who communicate and show a real willingness to sort out their debt in a completely different light. Ignoring the problem is a surefire way to make things worse.

By engaging with the IRS directly, you can stop the collection process in its tracks. Remember, seizing your car is a last resort for them, not their opening move.

Open a Line of Communication

The absolute first thing you should do—the moment you realize you can't pay your tax bill—is to contact the IRS. It’s that simple. This one action changes their entire perception of you, from someone who is delinquent to someone who is cooperative.

Once you’ve opened that door, you have several established options to propose a solution. These aren't secret loopholes; they are standard IRS programs designed to help people like you get back on solid ground.

Installment Agreement (IA): This is the most common path. You simply agree to pay off your tax debt over time with a series of manageable monthly payments. As long as you stick to the plan, the IRS won’t pursue a levy.

Offer in Compromise (OIC): If there’s no realistic way you can pay the full amount, an OIC lets you settle the debt for less. Getting one approved requires a deep dive into your income, expenses, assets, and overall ability to pay.

Currently Not Collectible (CNC) Status: If you're facing a true financial crisis, like a job loss or overwhelming medical bills, the IRS might agree to pause all collection efforts. They’ll place your account in CNC status and check in periodically to see if your situation has improved.

Taking Action and Finding a Solution

Which option is right for you? It all comes down to your personal financial picture. An Installment Agreement works well for people who have the cash flow for monthly payments. An OIC, on the other hand, can be a lifeline for those with crippling debt and very limited resources.

An Offer in Compromise is a powerful tool, but the IRS is picky. They’re looking for cases where your offer is realistically the most they could ever hope to collect. Successfullyhow to negotiate irs debt requires meticulous preparation and a clear understanding of what they're looking for.

Tax Debt Resolution Options Compared

To avoid a levy, you need to find the right resolution strategy. This table breaks down the most common paths forward.

| Resolution Method | Best For... | Key Requirement |

|---|---|---|

| Installment Agreement | Taxpayers who can afford consistent monthly payments to clear their debt over time. | A steady source of income to meet the agreed-upon payment schedule. |

| Offer in Compromise | Individuals with overwhelming debt and limited assets who cannot pay the full amount. | Proving that the offer amount is the most the IRS can reasonably expect to collect. |

| Currently Not Collectible | People facing severe, temporary financial hardship, such as unemployment or illness. | Demonstrating that paying the tax debt would prevent you from meeting basic living expenses. |

Ultimately, choosing the right option is the key to preventing asset seizure and getting back on track.

It’s also important to understand the full scope of the agency's power. While most people deal with civil enforcement, IRS Criminal Investigation (CI) is a formidable arm of the agency.

In the 2022 fiscal year alone, CI seized approximately $7 billion in assets. These cases usually involve criminal activity like tax fraud, but they highlight the IRS's broad authority to take property, including vehicles.

Thinking bigger, protecting your car from the IRS is just one piece of the puzzle. It’s wise to implement strong wealth preservation strategies to safeguard your assets from all types of claims.

At the end of the day, it all boils down to two things: communication and action. Don’t wait for that Final Notice of Intent to Levy to land in your mailbox. By reaching out early and working toward a resolution, you can build a protective wall around your assets and start the journey back to financial peace of mind.

What to Do if the IRS Has Seized Your Vehicle

Seeing your car get towed away by the IRS is a gut-wrenching experience. It’s easy to panic, but what you do in the next few hours and days is absolutely critical. The clock is officially ticking.

Once the IRS has your vehicle, it's slated for a public auction to cover your tax debt. You do have options, but they're extremely limited and time-sensitive.

The first thing you need to do is get your hands on the seizure notice, IRS Publication 594. Read it from top to bottom—it will spell out why they took the car and the total amount you owe, which now includes the costs for towing and storage.

Your Immediate Action Plan

Your one and only goal right now is to stop that auction. Forget negotiating a payment plan; that ship has sailed. At this stage, the IRS wants its money, and you have two potential paths to get your car back.

Redeem the Property: You have the right to get your vehicle back anytime before the sale by paying the full tax debt. This includes all the original taxes, penalties, interest, and every single expense the IRS incurred during the seizure. This isn't a negotiation—you'll need certified funds for the entire amount.

Purchase at Auction: If coming up with the full amount isn't possible, your last-ditch effort is to try and buy your own car back at the public auction. This is a huge gamble. You’ll be bidding against other buyers who might see your car as a great deal, and there's no guarantee you'll win.

It's crucial to understand that after the IRS seizes your vehicle, partial payment plans are no longer on the table for getting it back. The agency's position is that the time for negotiation has passed; now, only full payment will stop the sale.

Filing an Appeal After the Seizure

Even after the tow truck is gone, you still have the right to fight back. The Collection Appeal Program (CAP) is your formal avenue to challenge the seizure itself.

Through a CAP appeal, you can argue that the revenue officer didn't follow the proper legal procedures. You can also make a case that the levy creates a severe economic hardship, preventing you from meeting basic living expenses.

Filing a CAP request correctly under this kind of pressure is tough. This is where the notices you received earlier, like the IRS Final Notice of Intent to Levy, become incredibly important. Any procedural mistakes the IRS made will be documented in those papers and can form the basis of your appeal.

A successful appeal isn't a sure thing, but it’s one of the only official channels left to try and reclaim your vehicle before it’s gone for good.

Your Top Questions About IRS Car Seizures, Answered

Let's cut right to the chase. Here are the answers to the most common—and stressful—questions people have when the IRS is threatening to take their car.

How Much Warning Will I Get Before They Take My Car?

Let me be clear: the IRS will not just show up one day and tow your car away out of the blue. A seizure is the end result of a long, documented process.

You will get a whole series of letters and notices in the mail. The most critical one to watch for is the "Final Notice of Intent to Levy and Notice of Your Right to a Hearing." Once that lands in your mailbox, the clock starts ticking. It gives you a crucial 30-day window to file an appeal and officially challenge the seizure before it can happen.

Ignoring those letters is the worst thing you can do. It's like giving the IRS a green light to move forward.

What If I Own the Car With Someone Else?

Yes, the IRS can still seize a jointly-owned vehicle. Even if your name is on the title with a spouse, family member, or business partner, the car is still on the table to settle your tax debt.

But the other owner isn't left completely high and dry. They have legal rights. After the IRS seizes and sells the car, they are legally required to give the innocent co-owner their share of the money from the sale.

This is where things can get messy. The non-liable owner has to prove their ownership stake and what the car was actually worth. It often becomes a complex legal headache. Digging into related topics like understanding auto insurance can sometimes shed light on how vehicle ownership and value are documented, which is a key part of this process.

It's easy to feel cornered when you're up against the IRS. Before you make any decisions, you need a clear strategy tailored to your specific situation. Attorney Stephen A Weisberg offers a FREE, no-strings-attached Tax Debt Analysis to map out your options. Protect what's yours—visit weisberg.tax to schedule your confidential analysis today.

Yes, the IRS can take your car. But let's be very clear: this is an absolute last resort, reserved for taxpayers with significant, long-overdue tax debts.

Want to understand your options before you call anyone?

Download my free book — Freedom From Tax Debt — a plain-language guide to how the IRS collections process actually works and what resolution really looks like.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034