What Are Delinquent Taxes? Key Facts & Solutions

That feeling when you’re staring at a tax bill with a due date that’s already in the rearview mirror? It’s not a good one. So, what exactly are delinquent taxes? Simply put, they are any taxes you owe—whether for property, income, or your business—that haven't been paid by the official deadline.

Understanding Delinquent Taxes

Think of it like a library book. Once you pass the due date, you start racking up late fees. The book isn't just overdue; it's officially late. In the same way, once a tax payment is missed, it enters what’s called delinquent status. This is the trigger that starts a whole series of actions from the government.

Don't let the official-sounding terms scare you off. We're going to break down what happens next into clear, simple steps. The consequences can be serious, there's no sugarcoating that, but there is always a way to move forward. Getting a handle on how this all works is the first, most important step to getting back in control.

The Different Types of Unpaid Taxes

It's a common mistake to think all tax debt is created equal. The truth is, where the debt comes from matters—a lot. Knowing which type of tax you owe is the first step in figuring out how to get back on track.

Most delinquent taxes fall into one of these buckets:

Property Taxes: This one hits close to home—literally. If you fall behind on your property taxes, the local government can slap a tax lien on your house. This is more than just a piece of paper; it’s a legal claim against your property that, if left unresolved, could lead to foreclosure.

Income Taxes: This is probably the most common type of tax debt we see. It can happen to anyone, from freelancers who misjudged their quarterly payments to employees who didn't withhold enough from their paychecks. The scale of this is staggering; the IRS collected $120.2 billion just from unpaid assessments in fiscal year 2024.

Business Taxes: For business owners, this is a whole different level of stress. We're talking about things like payroll and sales taxes. When these go unpaid, the consequences can be severe, potentially threatening the very survival of your company.

Common Reasons Taxes Become Delinquent

Let's be honest—nobody plans to fall behind on their taxes. It’s almost never a deliberate choice. In my experience, it's usually life getting in the way that throws even the most organized person off track.

A sudden job loss, a staggering medical bill, or a small business hitting a rough patch can completely upend your finances, making it impossible to pay the IRS on time. This isn't an isolated problem. You can see this wider trend in the recent spike in 90-day credit card delinquencies, which signals a serious affordability crisis hitting families everywhere.

Of course, sometimes the reason is less dramatic. It could be an honest mistake—a missed deadline, a simple math error on a return, or just plain forgetting. If you realize you haven’t filed for a previous year, our guide on how to file back taxes can walk you through the process.

These kinds of oversights often come to light during other financial checks, which is why knowing how to prepare for an audit without stress is a skill every taxpayer should have in their back pocket.

The Escalating Consequences of Ignoring Tax Debt

Think of tax debt like a snowball rolling downhill. It starts small, but it picks up speed and size the longer you let it go. Ignoring it won't make it disappear—it just makes the problem much, much bigger.

The first thing that happens is purely financial. The moment your taxes are late, penalties and interest start piling on. This isn't a slow trickle; it's a constant accumulation that can make your original debt swell to a shocking amount before you know it.

If the debt continues to go unpaid, the tax authorities will start taking more serious steps. Next up is often a tax lien, which is a public, legal claim against your property. This is a big red flag for lenders and will absolutely tank your credit score, making it difficult to get a loan for a car or a house.

From there, things can escalate to a tax levy. This is where the government stops asking and starts taking. They can garnish your wages, seize money directly from your bank accounts, or even take physical property like your car.

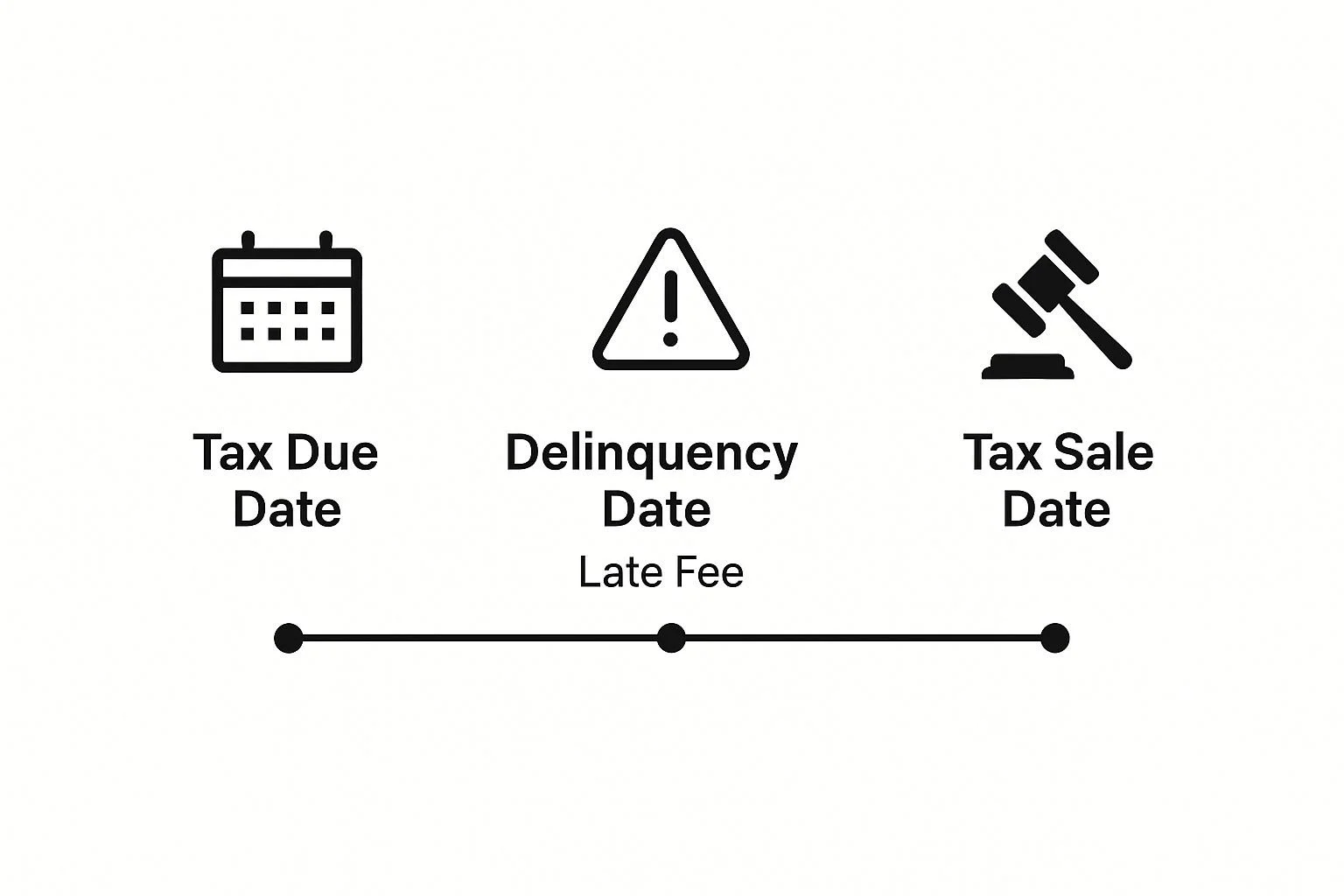

The infographic below shows just how this process can play out with property taxes, moving from a missed due date all the way to a potential tax sale.

To help you visualize how quickly things can intensify with the IRS or state tax agencies, here's a general timeline of what to expect.

Timeline of Consequences for Delinquent Taxes

| Stage | Typical Action Taken by Tax Authority | Impact on the Taxpayer |

|---|---|---|

| Initial Delinquency (First 1–3 months) | Automated notices (letters) are sent. | Initial penalties and interest begin to accrue. Minor credit score impact may start. |

| Continued Non-Payment (3–6 months) | More aggressive letters, including a "Notice of Intent to Levy." | Debt grows significantly. Stress and anxiety increase. |

| Serious Delinquency (6–12 months) | Filing of a Federal Tax Lien. | Severe damage to credit score. Difficulty securing loans or credit. Public record of debt. |

| Aggressive Collection (12+ months) | Issuance of a tax levy. | Garnishment of wages, seizure of bank funds, or repossession of assets (vehicles, property). |

This progression shows why it's so critical to address tax issues as soon as they arise. While there are limits, such as the IRS collection statute expiration date, you never want to let things get to the levy stage.

How to Resolve Delinquent Tax Debt

Staring down a tax bill you can't pay is a heavy weight, but it’s not a dead end. The good news is that tax agencies would much rather work with you than against you. You have options, and simply knowing what they are is the first step to getting back on solid ground.

Common Resolution Paths

One of the most straightforward routes is an Installment Agreement. Think of it like a payment plan that lets you chip away at the debt with manageable monthly payments.

For those in a serious financial bind, an Offer in Compromise (OIC) could be a lifesaver. This allows you to propose settling your tax debt for less than the full amount you owe, but you have to prove you truly can't pay it all.

If you're facing extreme hardship—like unemployment or a medical crisis—you might qualify for Currently Not Collectible status. This temporarily puts a hold on collections until your financial situation improves. Of course, each of these paths has its own set of rules and eligibility requirements.

It’s crucial to get a handle on these issues, especially when you see trends like the national property tax delinquency rate climbing to 5.1%. You can dig deeper into these tax debt solutions to figure out which approach makes the most sense for you.

A Few Common Questions About Delinquent Taxes

When you're dealing with delinquent taxes, a lot of questions pop up, and they're usually pretty urgent. Getting straight answers is the first step toward figuring out your options and moving forward.

Lien vs. Levy: What's the Difference?

It’s incredibly common to mix these two up, but they are worlds apart in the collection process.

Think of a tax lien as the government putting a legal "dibs" on your property. It’s a public notice that you owe them money, and it secures their claim against your assets—your house, your car, you name it. They haven't taken anything yet, but they've staked their claim.

A tax levy is the next step. This is when the government actively seizes your property to pay off the debt. A levy is the real deal—they can take money straight from your bank account, garnish your wages, or even take physical property. A lien is the warning shot; a levy is them collecting.

How Badly Will a Tax Lien Hurt My Credit?

A tax lien can do some serious damage to your credit score. Even after you’ve settled the debt, a paid tax lien can linger on your credit report for up to seven years.

The good news? You can fight back. After paying off the debt, you can request a "withdrawal" of the lien. If the IRS grants it, the lien is removed from your credit report completely, which can help your score bounce back much, much faster.

Can the IRS Really Send Me to Jail?

This is a huge fear for a lot of people, but for the vast majority of taxpayers, it's not a realistic outcome. The IRS reserves jail time for clear-cut criminal cases—we're talking about deliberate, willful tax evasion or fraud.

If you're just an average person who fell behind and is willing to work with them to fix it, prison is not on the table. The IRS is a collection agency at its core; their main goal is simply to get the money you owe.

Facing down tax problems is a heavy burden, but you don’t have to carry it by yourself. As an attorney, I start with a FREE Tax Debt Analysis to map out the best path forward for your unique situation. Find out how I can help you resolve your IRS problems by visiting weisberg.tax.

That feeling when you’re staring at a tax bill with a due date that’s already in the rearview mirror? It’s not a good one. So, what exactly are delinquent taxes? Simply put, they are any taxes you owe—whether for property, income, or your business—that haven't been paid by the official deadline.

Want to understand your options before you call anyone?

Download my free book — Freedom From Tax Debt — a plain-language guide to how the IRS collections process actually works and what resolution really looks like.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034