Can You File Bankruptcy on Tax Debt? A Complete Guide

Yes, you absolutely can file bankruptcy on tax debt. But it’s not as simple as checking a box. Think of it less as a get-out-of-jail-free card and more like a very specific key that only fits certain locks. Getting it right depends entirely on the type of tax, its age, and which chapter of bankruptcy you file under.

Understanding Your Options for Tax Debt in Bankruptcy

It’s one of the biggest myths out there: that tax debt follows you forever, no matter what. The truth is, the U.S. Bankruptcy Code was specifically designed to provide a legal path to discharge—or completely wipe out—certain income tax liabilities. But success hinges on meeting a handful of very strict, non-negotiable requirements.

Whether you can eliminate your tax bill depends on a few key factors, most importantly whether you file for Chapter 7 (liquidation) or Chapter 13 (reorganization). Each chapter handles tax debt in its own way, and the best fit for you comes down to your unique financial picture and the specifics of your tax problems.

Core Conditions for Discharging Tax Debt

To get that fresh start, your tax debt has to clear several time-sensitive hurdles. These rules exist for a good reason: they're designed to stop someone from racking up a huge tax bill on purpose and then immediately filing for bankruptcy to dodge it.

The government wants to see that your tax issues stem from genuine financial hardship over a period of time, not a last-ditch scheme to avoid paying what you owe.

To even be considered, your income tax debt must meet all of the main timing rules. Missing one by even a single day can derail the entire process.

| Condition | What This Means | Potential for Discharge |

|---|---|---|

| The Three-Year Rule | The tax return's original due date must be at least 3 years before your bankruptcy filing. | Your debt is old enough to be considered for discharge. |

| The Two-Year Rule | You must have actually filed the tax return at least 2 years before filing for bankruptcy. | Filing late but still meeting this rule can work. |

| The 240-Day Rule | The IRS must have assessed the tax at least 240 days before you file your bankruptcy case. | This gives the IRS time to process before you seek discharge. |

| No Fraud | You can't have committed tax fraud or willful evasion. | Any hint of fraud makes the debt non-dischargeable. |

These are the absolute fundamentals for getting IRS income tax debt wiped out in either a Chapter 7 or Chapter 13. It's also critical to remember this only applies to income taxes. Other types, like payroll taxes or the trust fund recovery penalty, are almost never dischargeable.

The bottom line is that not all tax debt is created equal in the eyes of a bankruptcy court. Only older, properly filed income tax debts that are free of any fraud have a shot at being discharged completely.

Why Professional Guidance Is Essential

Trying to navigate these complex timing rules on your own is incredibly risky. One mistake in calculating the look-back periods could mean you go through the entire bankruptcy process, only to find out you still owe the IRS every penny.

Before you commit to this path, it’s smart to look at all your options for relief. We cover some of these in our guide to IRS debt forgiveness options.

Ultimately, working with an experienced tax attorney isn't just a good idea—it's essential. They can pull your official IRS transcripts and do a detailed analysis to confirm if your debts are even eligible for discharge, helping you make a truly informed decision before you take such a significant step.

Choosing Your Path: Chapter 7 vs. Chapter 13

When you realize bankruptcy might be the answer to your tax problems, you’ll find yourself at a critical crossroads. The two main paths are Chapter 7 and Chapter 13 bankruptcy, and they work in fundamentally different ways.

The right choice for you isn't a one-size-fits-all answer; it hinges entirely on your income, the assets you own, and exactly what kind of tax debt you’re facing.

Think of Chapter 7 as a financial reset button. It’s often called a "liquidation bankruptcy" because its main goal is to wipe out your eligible debts quickly, often in just three to six months. If your tax debts are old enough to meet the very specific timing rules, Chapter 7 can eliminate them completely.

Chapter 13, on the other hand, is less of a sprint and more of a structured marathon. Known as a "reorganization bankruptcy," this process involves creating a manageable repayment plan that spans three to five years. It's designed for people who have a steady income and can afford to pay back at least a portion of what they owe over time.

The Power of Chapter 7 Liquidation

There’s a reason Chapter 7 is the most common type of consumer bankruptcy—for those who qualify, it’s incredibly fast and effective. Its biggest advantage is the power to discharge unsecured debts like credit card balances, medical bills, and, crucially, certain income tax debts.

To get in the door, you first have to pass a "means test." This test basically compares your household income to your state's median income. If your income falls below that line, you generally qualify for Chapter 7.

This path is often the best fit if:

You're dealing with a lot of other unsecured debt on top of your taxes.

Your income tax debt is old enough to meet all the strict timing requirements.

You don't have many valuable assets that you'd risk losing.

One of the most powerful features of filing is the "automatic stay." The moment your case is filed, a court order stops all collection efforts dead in their tracks. That means no more IRS wage garnishments or bank levies, giving you immediate breathing room.

The Strategic Advantage of Chapter 13 Reorganization

So what happens if your tax debt is too new to be wiped out in a Chapter 7? Or what if you make too much money to pass the means test? This is exactly where Chapter 13 shines as a strategic tool. It gives you a way to handle tax debts that can't simply be erased.

Even if your tax debt is non-dischargeable, Chapter 13 forces the IRS to accept a manageable repayment plan. It stops penalties and interest from piling up and lets you pay the debt back on your terms—not theirs—over the life of the plan.

Chapter 13 is particularly effective for dealing with:

Recent tax debts that don't meet the timing rules for discharge.

Tax liens, because you can structure a plan to pay off the secured portion of the debt.

"Trust fund" taxes like payroll taxes, which are never dischargeable.

By rolling your debts into one predictable monthly payment, Chapter 13 gives you a clear and protected runway to resolve your tax issues without the constant threat of aggressive IRS collections.

Comparing Chapter 7 and Chapter 13 for Tax Debt

Choosing the right bankruptcy chapter is the most important decision you'll make when tackling tax debt this way. This quick comparison table can help you see how each one approaches the problem differently.

| Feature | Chapter 7 (Liquidation) | Chapter 13 (Reorganization) |

|---|---|---|

| Primary Goal | Wipes out eligible debts quickly. | Creates a 3-5 year repayment plan. |

| Tax Debt Treatment | Discharges old, eligible income tax debt. | Manages all tax debts, even recent or priority ones. |

| Timeline | Typically 3-6 months. | 3 to 5 years. |

| Who It's For | Lower-income filers with few assets. | Filers with regular income who can afford payments. |

| Key Benefit | Total elimination of qualifying tax debt. | Stops collections and manages non-dischargeable taxes. |

Ultimately, this is a strategic decision that requires a close look at the details. An experienced bankruptcy attorney can review your tax records, income, and overall financial picture to help you choose the chapter that will deliver the best possible outcome for your unique situation.

The Critical Timing Rules You Must Meet

When people ask, "can you file bankruptcy on tax debt?" the answer almost always comes down to timing. It's less about what you want to do and more about what the calendar says you can do. The court uses a strict set of "look-back" periods to figure out if your tax debt is old enough to qualify.

I like to think of it as a combination lock on a vault. To open that vault and get your financial freedom, you have to get every number right, in the perfect sequence. Miss just one, and that vault door stays shut, leaving you right where you started with the IRS. These rules are completely non-negotiable and require some careful calculation.

The Three-Year Rule for Tax Return Due Dates

The first number in our combination is the Three-Year Rule. This is the big one, the foundation for everything else. The original due date for the tax return has to be at least three years before you file for bankruptcy. And yes, this includes any extensions you might have filed.

So, let's say we're talking about your 2020 tax return. That was originally due on April 15, 2021. To satisfy this rule, you can't file for bankruptcy until after April 15, 2024.

If you file even one day early, that 2020 tax debt is out. This rule is there to stop people from racking up tax debt on purpose and then immediately running to bankruptcy court for an easy out.

The Two-Year Rule for Filing Your Return

Next up is the Two-Year Rule. This one isn't about when the return was due; it’s about when you actually filed it. You must have physically filed the tax return for the debt in question at least two years before you file your bankruptcy case.

This rule catches people who file their taxes late. Sticking with our example, your 2020 return was due April 15, 2021, but you didn't get around to filing it until June 1, 2022. Even though you pass the Three-Year Rule in April 2024, you now have to wait until after June 1, 2024, to satisfy this second rule. You have to meet both.

Crucial Takeaway: You absolutely cannot get rid of taxes in bankruptcy for a return you never filed. The court views an unfiled return as a willful failure to follow tax law, and it won't reward that by wiping out the debt.

The 240-Day Rule for Tax Assessment

The last number in our combination is the 240-Day Rule. The IRS has to have officially "assessed" the tax—meaning they formally recorded your debt on their books—at least 240 days before you file your bankruptcy petition.

For most people who file on time, this assessment happens pretty quickly. The tricky part is that the 240-day clock can be paused, or "tolled," by certain events.

Things like an IRS audit or a pending Offer in Compromise can stop the clock, making this one of the most complex rules to calculate. This is where getting an expert legal opinion is so important.

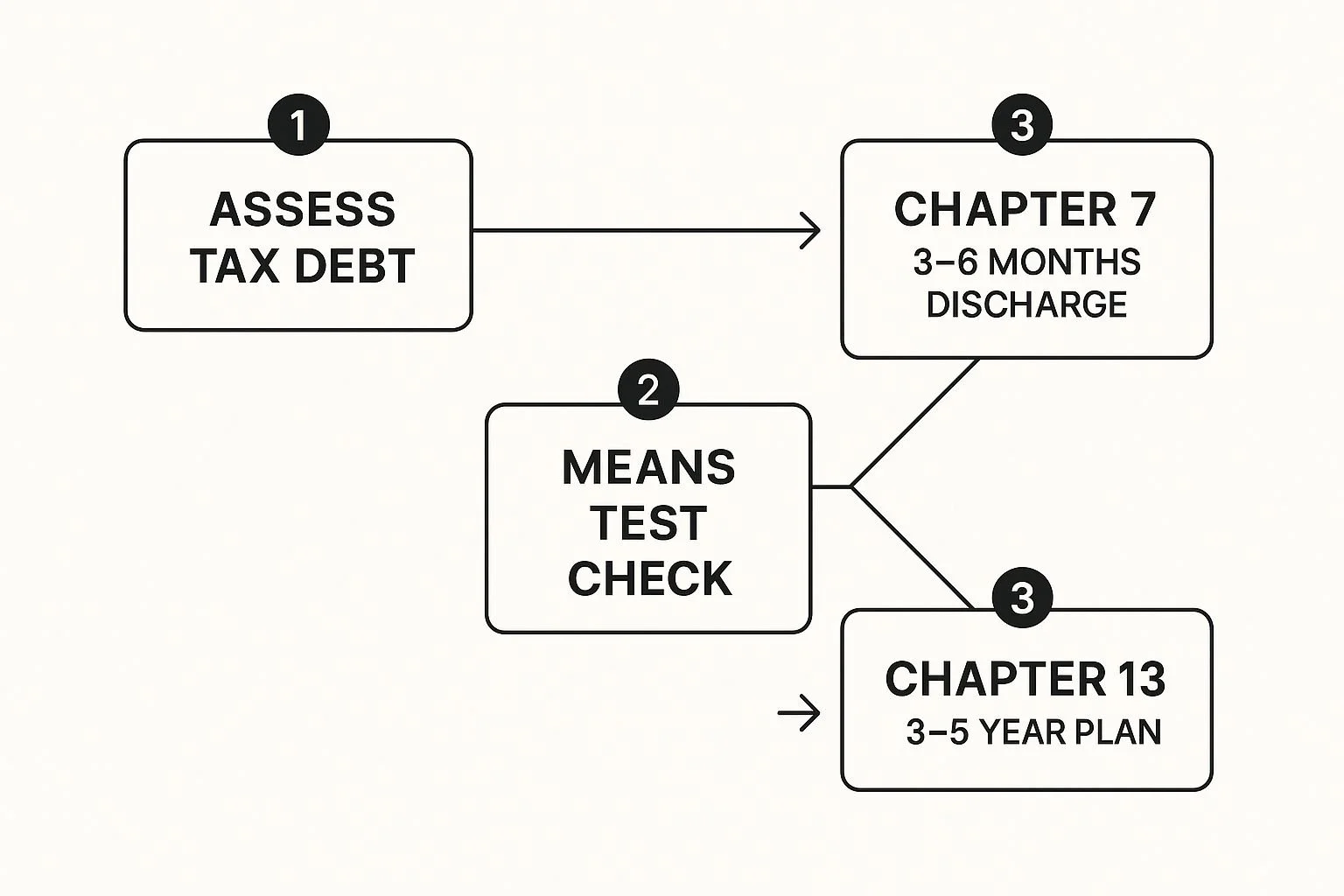

This flowchart gives you a good visual of how everything fits together, from assessing the debt to choosing the right bankruptcy chapter.

As you can see, once you've figured out your debt and passed the means test, your path will generally lead to either a quick discharge with Chapter 7 or a longer-term repayment plan through Chapter 13.

The Non-Fraudulent Return Requirement

Finally, there’s one master rule that can trump all the others: you must have filed a non-fraudulent tax return. If the IRS proves you committed tax fraud or willfully tried to evade your taxes, that specific tax debt can never be discharged in bankruptcy. No amount of time will heal a debt that was created through intentional deceit.

So, to bring it all together, here’s the checklist for wiping out old income tax debt.

The tax return was due at least three years ago.

The tax return was filed at least two years ago.

The tax was assessed at least 240 days ago.

The return was not fraudulent.

You have to hit every single one of these targets for the specific tax year you want to address. As you can imagine, figuring out these dates isn't always simple, and getting it wrong can sink your entire case. The only surefire way to know if you're eligible is to have a tax debt attorney review your official IRS transcripts before you even think about filing.

Tax Debts That Bankruptcy Cannot Erase

While bankruptcy can be a powerful tool for getting out from under old income tax debt, it’s not a magic wand that makes every tax problem vanish. Some tax liabilities are stubbornly "non-dischargeable," meaning they will stick with you even after your bankruptcy case is closed.

Knowing what these exceptions are from the get-go is critical. It helps you set realistic expectations and avoids the nasty surprise of finding out you still owe the IRS or state after the whole process is over.

Think of it this way: bankruptcy can clear a lot of financial debris, but some debts are bolted to the foundation.

Trust Fund Taxes: The Unforgivable Debts

The most common type of tax debt you can't shake in bankruptcy involves trust fund taxes. This is money you collect from other people with the understanding that you're holding it for the government.

The two main examples are:

Payroll Taxes: As an employer, this is the federal income tax, Social Security, and Medicare you withhold from your employees' paychecks.

Sales Taxes: As a business owner, this is the tax you collect from customers when they buy goods or services from you.

The government’s position is firm: that money was never yours. You were simply acting as a temporary caretaker—holding it "in trust"—before you passed it along.

Because of this unique status, these debts are almost impossible to discharge in any form of bankruptcy. If you fail to turn them over, you could be hit with the devastating Trust Fund Recovery Penalty (TFRP), which makes you personally responsible. You can learn more about this in our in-depth guide on the Trust Fund Recovery Penalty.

The government sees you as a collection agent. Failing to pay trust fund taxes isn't just a debt; it's a breach of that trust, and the bankruptcy court will not forgive it.

Taxes Tied to Fraud or Willful Evasion

This one is pretty simple: you can't cheat on your taxes and then ask the court to wipe the slate clean. Any tax debt connected to a fraudulent return or a willful attempt to evade paying taxes is permanently non-dischargeable.

The court and the IRS won't reward dishonesty. That debt will follow you no matter how old it is or which bankruptcy chapter you file under. This really drives home how important it is to have filed honest and accurate tax returns in the first place, as we covered in the timing rules.

The Lingering Problem of Tax Liens

Finally, you have to understand how a federal tax lien changes the game. When the IRS files a Notice of Federal Tax Lien, it slaps a secured claim on your property, like your house or your car.

Here's the tricky part. Even if the actual income tax debt is old enough to be discharged in Chapter 7, the lien itself can survive. This means that while the IRS can no longer come after your wages for that specific debt, the lien remains attached to your property.

If you ever try to sell or refinance, they can take their share from the proceeds. For this reason, a Chapter 13 bankruptcy, which allows you to create a plan to pay off the lien over time, can often be a better strategy for dealing with tax liens.

When to Consider Alternatives to Bankruptcy

Filing for bankruptcy is a huge decision. It's not something you just jump into, as it leaves a long-lasting mark on your credit and financial life.

Before you even think about heading down that road, it’s critical to understand that bankruptcy isn't your only play. The IRS actually has some powerful programs designed to help you resolve tax debt without ever stepping foot in a courtroom.

Think of it this way: bankruptcy is the nuclear option. It might solve the immediate problem, but the fallout can be significant. Exploring these other paths is like looking for a diplomatic solution before declaring war. These alternatives are specifically designed for taxpayers who are genuinely struggling and need a way out.

Offer in Compromise (OIC)

One of the best tools in the taxpayer's arsenal is the Offer in Compromise (OIC). Before even considering bankruptcy, you absolutely must see if you qualify for an IRS Offer in Compromise. This program allows you to settle your tax debt for less—sometimes much less—than the total amount you owe.

The IRS will consider an OIC if they believe they won't be able to collect the full amount you owe before the collection statute expires. They'll look at your "reasonable collection potential," which is just a fancy way of saying they'll analyze your income, essential living expenses, and the value of your assets. If the numbers show you can't pay in full, an OIC could be your golden ticket.

Installment Agreements and CNC Status

What if you don't qualify for an OIC but still can't pay the entire debt at once? An Installment Agreement (IA) is the next logical step. It’s a straightforward payment plan you set up with the IRS, letting you chip away at the debt with manageable monthly payments, often over a period of up to 72 months.

For those in truly dire financial straits, the IRS offers Currently Not Collectible (CNC) status. This is a temporary pause button. If you're approved, the IRS agrees to stop aggressive collection actions like wage garnishments or bank levies because they recognize you simply don't have the ability to pay right now.

Just remember, interest and penalties keep adding up, and the IRS will check in on your financial situation periodically to see if things have improved.

These alternatives are more important than ever as people feel the squeeze of a tough economy. In fact, global bankruptcies recently jumped by 10% over the previous year, which shows just how much financial pressure people are under. This trend really drives home the need to explore every single option before taking the drastic step of bankruptcy.

Key Insight: Working directly with the IRS can often lead to a much better result than bankruptcy, especially if your tax debts aren't dischargeable anyway. These programs keep you out of the court system and are far less damaging to your credit report.

Ultimately, there's no one-size-fits-all answer. The right path depends entirely on your unique financial picture. Taking a serious look at these alternatives is the most important first step you can take. To get a better handle on how to start these conversations, check out our guide on how to negotiate IRS debt.

Why Financial Pressures Lead to Tax Debt

Let's be honest: almost no one chooses to fall behind on their taxes. It’s rarely a single decision made in a vacuum. Instead, it’s usually the last domino to fall after a series of mounting financial pressures that feel like an overwhelming tidal wave.

Understanding this context is key, as it reframes bankruptcy not as a personal failure, but as a practical, strategic response to impossible economic circumstances.

The path to serious tax debt almost always starts with an unexpected life event. Think about a sudden job loss, a frightening medical diagnosis, or a messy divorce.

These shocks can instantly shatter a carefully balanced budget, forcing you to make impossible choices. Pay the IRS, or pay for rent, groceries, and keep the lights on? For most people, the answer is obvious.

The Snowball Effect of Competing Debts

For many families, tax debt doesn't live on an island. It’s usually tangled up in a much larger, more complicated financial web where every dollar is already stretched to its breaking point.

High inflation makes daily life more expensive, while rising interest rates make other debts—like credit cards and car loans—a much heavier burden. This creates a dangerous snowball effect.

This kind of financial strain is incredibly common. By the end of 2024, U.S. credit card balances exploded to a record $1.21 trillion.

At the same time, the number of households falling 90+ days behind on their credit card and auto loan payments shot to a 14-year high.

These aren't just numbers; they're a clear signal of the intense pressure people are under.

When you're juggling a mortgage, car payments, and credit card bills that seem to grow overnight, the IRS often becomes the creditor that gets pushed to the back burner. It feels less immediate than keeping a roof over your head, but the penalties and interest are always there, growing silently and relentlessly.

This pile-up of different debts creates a perfect storm. When cash flow is squeezed this tight, business owners, for example, might start looking into options like business loans without collateral just to get some breathing room and prevent a cascade of defaults.

Ultimately, these compounding pressures can make it impossible to keep up with tax payments. When you find yourself in this position, it’s crucial to remember that you are not alone and that there are structured legal tools designed to provide real relief. If you want to explore your options, our guide on finding a comprehensive tax debt solution is a great place to start.

Frequently Asked Questions

When you’re staring down a mountain of tax debt and thinking about bankruptcy, a lot of questions pop up. It’s only natural. Getting straight answers is the only way to make a smart decision for your future. Let’s tackle some of the most common questions I hear from people in your exact shoes.

Will Filing Bankruptcy Stop an IRS Wage Garnishment?

Yes. The second you file for any chapter of bankruptcy, a powerful legal protection called the automatic stay kicks in. Think of it as an immediate, court-ordered ceasefire.

This order instantly stops almost all creditor collection actions dead in their tracks. That means no more IRS wage garnishments, no more bank levies, and no more harassing collection letters. It gives you critical breathing room.

If your tax debt is ultimately wiped out in a Chapter 7, that garnishment is gone for good. In a Chapter 13, the garnishment also stops, but the debt gets handled through your court-approved repayment plan instead.

What Happens to State Tax Debt in Bankruptcy?

For the most part, state tax debts get the same treatment as federal IRS debts in bankruptcy. If you're hoping to discharge them in a Chapter 7, they have to pass the same set of strict timing tests we've been talking about.

The tax return had to be due at least three years ago.

You must have actually filed the return at least two years ago.

The state must have assessed the tax at least 240 days ago.

If your state income taxes fail to meet these rules, they're considered non-dischargeable. But that doesn't mean you're out of options. You can still wrap them into a Chapter 13 plan. This stops the state's aggressive collection tactics and lets you repay what you owe over a more manageable timeframe.

Do I Need a Lawyer for Tax Debt Bankruptcy?

Technically, you can file for bankruptcy on your own. But when tax debt is involved, I can't stress this enough: it's a very bad idea.

The rules for discharging tax debt are notoriously complicated and littered with traps for the unwary. One tiny mistake—miscalculating a look-back period or misinterpreting the type of tax you owe—can torpedo your entire case, leaving you right back where you started.

You’d have wasted all that time, money, and stress for nothing. Even legal professionals who manage these complex cases rely on tools like legal software to keep everything organized and avoid those kinds of costly mistakes.

Hiring an experienced bankruptcy attorney isn't just a good idea; it's essential. A pro will pull your official tax records, determine exactly which debts can be discharged, and make sure your case is filed perfectly to give you the fresh start you deserve.

Facing overwhelming tax debt can feel isolating, but you don't have to navigate it alone. At Attorney Stephen A Weisberg, we start with a FREE Tax Debt Analysis to determine exactly how we can help before you ever pay a fee.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034