Currently Non Collectible Status IRS Explained | How to Qualify

When you're staring down a mountain of tax debt, hearing the phrase "Currently Not Collectible status" from the IRS can feel like finding an oasis in a desert. This status, often just called CNC, is basically the IRS hitting a temporary pause button on their collection efforts.

It’s an official recognition that, right now, you simply can't afford to pay your tax bill without it preventing you from covering your basic living expenses. For people facing real financial hardship, it provides some much-needed breathing room from the constant stress of collections.

What Currently Non Collectible Status Really Means

Think of your monthly income as a pitcher of water. You have to pour that water into several essential glasses first—rent, food, utilities, healthcare. These are your non-negotiables.

If your pitcher is just barely big enough to fill those essential glasses, there’s nothing left over. When the IRS sees this, they can grant CNC status. They’re agreeing not to try and take any water from your pitcher because they recognize that doing so would leave one of your essential glasses empty, causing you significant hardship.

This means an immediate stop to some of the most stressful and damaging collection methods.

Hitting the Pause Button on IRS Collections

Once the IRS places your account in CNC status, it’s like a ceasefire. The most aggressive collection tactics are put on hold, giving you instant relief from the pressure.

Here’s what stops:

Wage Garnishments: They won't take money directly from your paycheck anymore.

Bank Levies: They’ll stop seizing the funds in your bank accounts.

Asset Seizures: Any plans to take your physical property are halted.

Aggressive Notices: That relentless stream of threatening letters will finally dry up.

This isn’t just the IRS being nice; it’s a procedure rooted in their own regulations to protect taxpayers from going under.

The IRS Internal Revenue Manual actually directs agents to place accounts in "Currently Not Collectible" when they verify that a taxpayer can't pay their debt without it interfering with their ability to cover basic needs. This legal framework is what forces the release of levies and provides a critical safety net.

What CNC Status Is Not

Now, here’s the critical part: CNC is not tax forgiveness. Not even close. Think of it as hitting snooze on an alarm clock, not turning it off completely. While the collection calls and letters stop, the underlying tax debt is still there, and it's still growing.

Important Takeaway: Even while you're in Currently Non Collectible status, your tax debt continues to rack up interest and penalties. The total amount you owe will keep climbing until the debt is either paid off or the collection statute runs out.

Understanding this distinction is absolutely vital. The relief is temporary and is only meant to last as long as your financial hardship does. The IRS won't forget about you; they will periodically review your financial situation—usually every one to two years—to see if your ability to pay has changed.

You can learn more about what this status involves in our detailed guide on the Currently Not Collectible IRS program. Now that we've covered the basics, let's dive into how the IRS actually decides if you qualify.

How the IRS Decides If You're In Financial Hardship

You can't just call the IRS and tell them you're broke. To qualify for currently non collectible status, you have to prove it with cold, hard numbers. The IRS needs to see, in black and white, that paying your tax debt would leave you unable to cover basic living expenses like rent, food, and utilities.

It all boils down to a pretty simple formula. The IRS takes your total monthly income and subtracts your allowable monthly expenses. If you're left with zero—or a negative number—you've likely demonstrated the kind of financial hardship that gets you into CNC status.

To get to that number, you’ll have to give them a complete look under the hood of your finances.

The Collection Information Statement: Your Financial X-Ray

The main tool the IRS uses to get this complete financial picture is the Collection Information Statement. For most individuals, this is Form 433-F. If you're self-employed, you'll likely use Form 433-A, and businesses use Form 433-B.

Think of this form as a financial x-ray. It gives the IRS a detailed view of your economic health, leaving no stone unturned.

You'll have to lay all your cards on the table, including:

Income Sources: Every penny, from your paycheck and side hustles to Social Security and retirement money.

Cash on Hand: Balances for all your checking, savings, and other bank accounts.

Assets: This means your house, cars, investment accounts, and anything else of significant value.

Monthly Expenses: A complete list of your necessary living costs, from your mortgage payment down to your grocery bill.

Be prepared to back it all up with documents like recent pay stubs and several months of bank statements. Honesty is non-negotiable here. If you try to hide assets or income, your request will be dead on arrival.

What Does the IRS Consider an "Allowable" Expense?

This is where things get tricky, and where a lot of people get tripped up. The IRS doesn't just take your word for what your expenses are. Instead, they measure your spending against a set of their own guidelines, known as the IRS Collection Financial Standards.

These standards are basically the IRS's definition of what it costs to live a modest life in your part of the country. They're broken down into a couple of key categories:

National Standards: These cover day-to-day items like food, clothing, personal care products, and housekeeping supplies. The allowed amount is the same for everyone across the country and is based only on your income and the number of people in your household.

Local Standards: These account for costs that vary wildly depending on where you live. This is mainly housing and utilities (what's reasonable for rent or a mortgage in your county) and transportation (the cost of owning a car or using public transit in your area).

What if your actual rent or car payment is higher than the standard? You'll need a very good reason—and solid proof—that the extra cost is absolutely necessary for your family's health, well-being, or your ability to earn a living.

Crucial Insight: The IRS is not judging your lifestyle. They are making a purely mathematical calculation to determine the absolute minimum you need to survive. Things like private school, fancy dinners, or expensive hobbies will not be considered "necessary" and won't be included in their calculation.

Let's Look at a Real-World Example

Imagine a taxpayer named Sarah. She's a single mom with two kids, living in a regular American city, and she owes the IRS $15,000.

Her Monthly Income: After taxes, Sarah brings home $3,500.

Her Allowable Expenses: After she carefully fills out her Form 433-F, the IRS applies the national and local standards for her area and family size. Her total allowable expenses come out to $3,650.

The IRS does the math: $3,500 (Income) - $3,650 (Allowable Expenses) = -$150.

The result is a negative $150. This shows the IRS that Sarah is already falling short each month just covering the basics. Demanding a tax payment would put her even further behind on essentials like rent or groceries.

This is a textbook case of financial hardship. Based on this simple calculation, the IRS would almost certainly approve her for currently non collectible status and pause all collection efforts while she gets back on her feet.

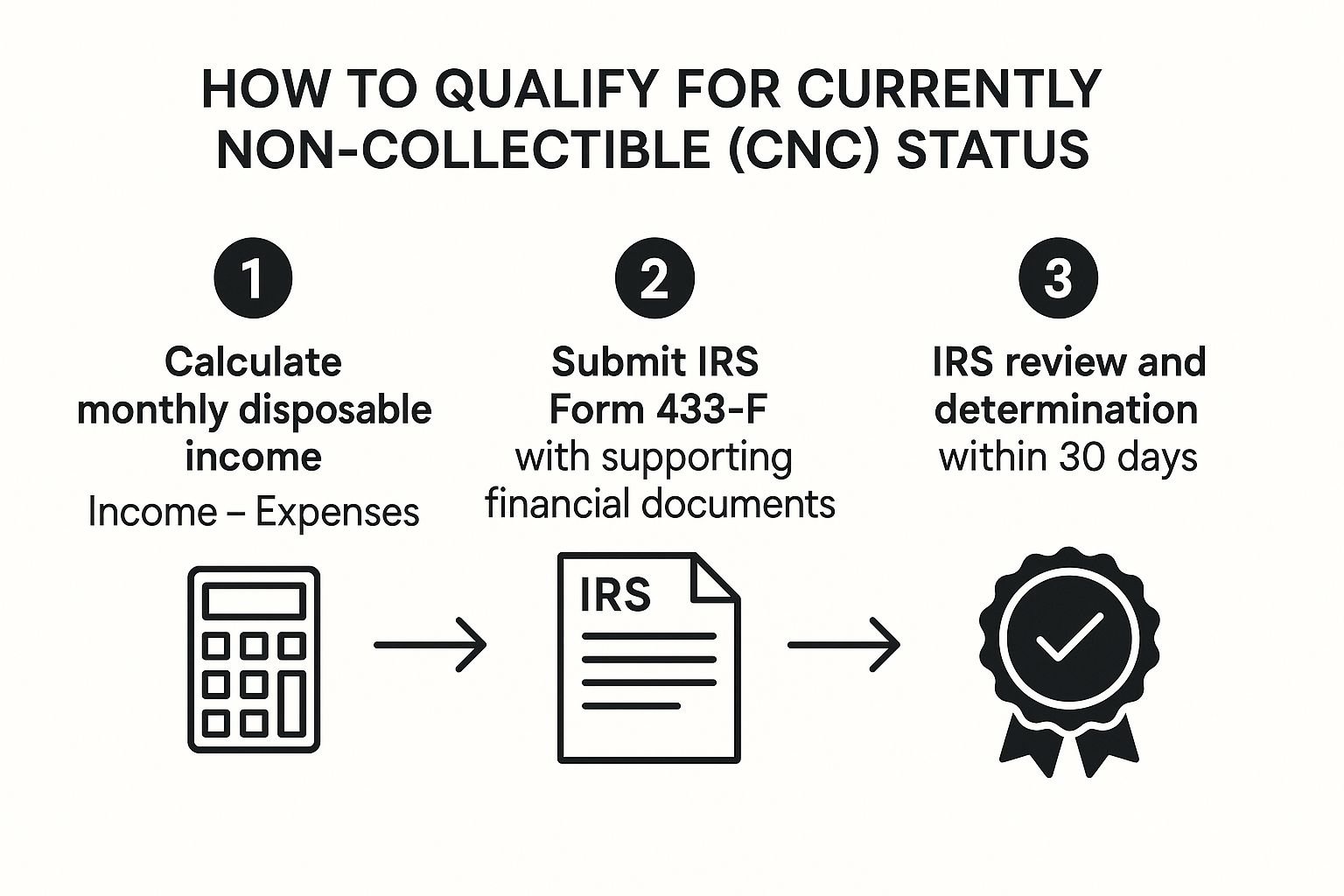

Your Step-by-Step Guide to Requesting CNC Status

Securing Currently Non-Collectible status isn't about just asking the IRS for a break; it's about methodically proving you're in a financial corner. You have to build a solid case for yourself, backed by clear, undeniable evidence of hardship.

The journey usually kicks off when a collection notice lands in your mailbox. Your first instinct might be to ignore it, but the best move is to respond. This is your chance to open a line of communication and let them know you simply can’t pay what they're asking for. The immediate goal is to get the IRS to send you the right financial forms to make it official.

Assembling Your Financial Statement

The heart of your request is the Collection Information Statement. For most people getting an automated collection notice, this will be Form 433-F. If your situation is more complex, or if you're self-employed, you'll likely need the more detailed Form 433-A. Businesses have their own version, Form 433-B.

Think of this form as a complete financial physical. Filling it out with 100% accuracy is the single most important thing you'll do.

Here’s a quick look at what you’ll need to lay out:

Income Details: Every penny coming in each month. This includes your paycheck, any side-gig income, social security, and anything else you receive.

Asset Disclosure: A full list of what you own. We're talking cash in the bank, your home, cars, and any retirement or investment accounts.

Monthly Expenses: A breakdown of your necessary living costs—things like your mortgage or rent, utilities, groceries, car payments, and medical bills.

I can't stress this enough: be brutally honest on this form. Trying to hide an asset or lowball your income is a fast track to getting denied, and it could even lead to penalties.

Gathering Your Supporting Documents

Once you’ve filled out Form 433-F, it's time to back it all up with paperwork. The IRS operates on a "trust, but verify" model, and they need documentation for everything. Put yourself in their shoes: if you were an auditor, what would you need to see to believe the numbers on the page?

Start pulling together these key documents:

Proof of Income: Your last three months of pay stubs are standard.

Bank Records: The last three months of statements for every single one of your bank accounts.

Major Expense Verification: Copies of mortgage statements, rent receipts, utility bills, and car loan statements.

Other Financial Records: Any statements for investments, 401(k)s, or other significant assets.

Get everything organized and attach it to your Form 433-F. A clean, well-organized package makes the IRS agent's job easier, and that can only help your case move along smoothly.

This visual gives a good overview of how the pieces fit together.

As you can see, it's a logical flow: you figure out your real financial situation, gather the proof, and submit it for the IRS to review.

What to Expect After You Submit Your Request

After you've mailed your package, the waiting game begins. An IRS agent will be assigned to review everything you sent. It's pretty common for them to call you with a few follow-up questions or to ask for another document or two.

Pro Tip: Be ready for that call. Keep a copy of everything you submitted nearby so you can answer their questions confidently and accurately. Being cooperative and quick to respond can make a real difference in how they see your case.

The review can take anywhere from a few weeks to several months. It really just depends on how complex your finances are and how busy the IRS is at the moment.

If your request for Currently Non-Collectible status is approved, you'll get a letter in the mail confirming it. This is the official notice that they're pausing collection efforts. If you're denied, the letter will explain why, and you'll have the right to appeal. By tackling this process with honesty and diligence, you give yourself the best possible shot at getting the breathing room you need.

The Reality of Living with CNC Status

Getting that currently non collectible status irs approval can feel like a massive weight has been lifted from your shoulders. It's a genuine moment of calm after a long storm, giving you the breathing room you desperately need when facing real financial hardship.

The most immediate change? The silence. The endless, aggressive letters stop. The stressful phone calls from IRS agents go away. That peace of mind alone is invaluable, letting you focus on getting your finances back on track without the constant threat of collections hanging over your head.

CNC Status What Stops vs What Continues

It’s crucial to understand that CNC status is a pause button, not a stop button. While it halts the most aggressive collection actions, other things keep moving forward. Here's a quick breakdown of what changes and what stays the same.

| Action | Status Under CNC |

|---|---|

| Wage Garnishments | Stops. The IRS will no longer take money from your paycheck. |

| Bank Levies | Stops. Your bank accounts are safe from direct seizure. |

| Asset Seizures | Stops. The IRS suspends actions to take your property. |

| Debt Growth | Continues. Interest and penalties keep accumulating daily. |

| Future Refunds | Continues. The IRS will seize any future tax refunds to pay your debt. |

| Tax Liens | Continues. The IRS can still file a Federal Tax Lien against your property. |

This table highlights the dual nature of CNC status. It provides immediate relief from severe collection tactics, but the underlying tax problem doesn't just disappear.

What Stops Immediately

The main job of CNC status is to put a hard stop to the IRS's most powerful collection tools. Once you're approved, the agency immediately ceases:

Wage Garnishments: They can no longer take a slice of your paycheck before you even see it.

Bank Levies: They must stop seizing funds directly out of your bank accounts.

Asset Seizures: Any plans to confiscate your property, like your car or home, are put on hold.

This protection is a lifeline. It means the money you earn can actually go toward your rent, groceries, and other essentials instead of being intercepted by the government. But this is only half the story.

What Continues Despite CNC Status

While the active hounding stops, your tax debt is still very much alive and growing. Think of CNC as a deferment, not a forgiveness. The IRS still has its hooks in, just less aggressively.

Key Insight: CNC status does not freeze your tax liability. Your total balance will get bigger every single day as interest and penalties continue to pile up.

This is the part people often miss. The relief is temporary, but the debt's growth is relentless. On top of that, the IRS keeps a few powerful collection tools in its back pocket:

Future Tax Refunds Are Gone: Don't expect a tax refund anytime soon. If you're due one while in CNC status, the IRS will automatically grab it and apply it to your old tax bill.

A Federal Tax Lien is Still a Threat: The IRS can, and often does, file a Notice of Federal Tax Lien. This public notice secures the government's claim to your assets, making it nearly impossible to sell your house or get a loan until the tax debt is cleared.

The IRS collected over $120.2 billion in unpaid taxes in a recent year, and they didn’t do it by simply forgetting about debts. Tools like liens and refund offsets are standard procedure, even for taxpayers in hardship status. For a closer look at these activities, you can review the latest collection statistics on the IRS.gov website.

CNC provides a vital safety net, but it isn't a permanent fix. For some, watching the debt grow larger might make other solutions more appealing. If you’re looking to put this debt behind you for good, it might be time to read our complete guide on the IRS Offer in Compromise program.

How and When CNC Status Ends

Getting the IRS to place your account in Currently Non-Collectible (CNC) status brings a huge wave of relief. But it's absolutely critical to understand that this is a temporary pause, not a permanent solution. The IRS hasn't forgiven your debt; they've just agreed to stop trying to collect it for now.

Think of it as the IRS putting your file in a "pending" tray. They fully intend to come back to it later to see if anything has changed.

The IRS Will Be Checking In

The IRS won't just forget about you. Every one to two years, they'll conduct a review to see if your financial situation has improved. You can expect a letter in the mail asking for an updated financial statement—much like the one you filled out to get CNC status in the first place.

They're looking for one thing: a meaningful, positive change in your finances. This is their way of making sure the program is only used by people who genuinely can't afford to pay.

It's also worth noting that the IRS has its own operational challenges. The Taxpayer Advocate Service website has highlighted major processing backlogs, which can sometimes affect how quickly they get around to these reviews.

What Triggers the End of CNC Status?

So, what kind of changes will put you back on the IRS's collection radar? A few specific events will almost certainly trigger a revocation of your CNC status.

Here are the most common reasons:

You Start Making More Money: This is the big one. Landing a much better job, getting a huge promotion, or even a successful side hustle can increase your income enough to end CNC status.

You Receive a Financial Windfall: Did you get an inheritance from a relative? Win a settlement from a lawsuit or even hit a lucky number on a lottery ticket? The IRS considers this a change in your ability to pay.

You Stop Filing Your Taxes: This is a deal-breaker for the IRS. To keep your CNC status, you must file all your future tax returns on time, every time. Failing to do so is a massive red flag that will get your hardship status yanked immediately.

If any of these happen, the IRS will look at your new numbers. If they see you now have money left over after covering your basic living expenses, they'll pull you out of CNC and restart collection activities.

Important Takeaway: Staying compliant is your job. Filing all future tax returns on time is non-negotiable if you want to maintain your CNC status.

The Ultimate Deadline: The CSED

While your finances can change, there's another, more final deadline working in the background: the Collection Statute Expiration Date (CSED). This is the master clock ticking on every tax debt.

From the day your tax is assessed, the IRS generally has just 10 years to collect it. After that 10-year window closes, they legally can't touch you for that debt anymore.

Here's the best part: being in Currently Non-Collectible status does not stop the CSED clock. It keeps ticking away while the IRS has agreed to leave you alone.

This creates the most powerful outcome for someone with long-term financial hardship. If your inability to pay lasts long enough for that 10-year statute of limitations to expire, the tax debt is gone. For good. It's effectively wiped out simply because time ran out.

Exploring Your Tax Relief Alternatives

While getting into currently non collectible status IRS provides a much-needed breathing room, it's not a finish line. Think of it as hitting the pause button on collections; it stops the immediate pressure, but it doesn't resolve the underlying tax debt. For a permanent fix, you’ll need to explore other tools in the IRS’s toolbox.

Luckily, the IRS has several different programs designed to help taxpayers get back on their feet. Each one is built for a specific financial situation, so understanding your options is the first step toward finally putting your tax troubles behind you for good.

Offer in Compromise: A Fresh Start

An Offer in Compromise (OIC) is a powerful tool for taxpayers who genuinely can’t afford to pay their full tax liability before the collection statute runs out. It’s an agreement with the IRS to settle your debt for less than the total amount you owe.

This isn’t just a simple negotiation, though. The IRS has very strict standards. They will only accept an OIC if the amount you offer is the absolute most they could ever hope to collect from your assets and future income.

Who It's For: People or businesses buried under significant tax debt with limited income and assets, who can prove that paying in full is simply not possible.

Pros: It offers a true fresh start, permanently wiping the slate clean for just a fraction of the original debt.

Cons: The application is notoriously complex, demands exhaustive financial documentation, and faces a high rejection rate if not prepared perfectly.

If you feel your financial situation makes full repayment an impossible mountain to climb, it's definitely worth exploring.

Installment Agreement: Predictable Payments

If you have the means to pay your tax debt, just not all at once, an Installment Agreement (IA) is often the most straightforward path forward. This is a formal payment plan that lets you make manageable monthly payments until the debt is cleared.

An Installment Agreement provides certainty. As long as you stick to the plan, it halts aggressive collection actions like levies and gives you a clear, predictable roadmap to becoming debt-free.

Who It's For: Taxpayers who can't pay their entire balance today but have a steady income that allows them to pay it off over time.

Pros: It’s relatively simple to set up, stops the most serious collection threats, and gives you a structured repayment schedule.

Cons: The clock on interest and penalties keeps ticking until the debt is fully paid, which can add a substantial amount to your total bill.

Penalty Abatement: Forgiving the Extras

Sometimes, the original tax bill isn't the biggest problem—it's the mountain of penalties the IRS has tacked on for filing or paying late. Penalty Abatement is a formal request asking the IRS to remove those penalties.

To qualify, you typically need to prove you had a "reasonable cause" for the delay. This could be anything from a serious illness or natural disaster to relying on bad advice from a tax professional.

While it won't erase the core tax you owe, getting thousands of dollars in penalties removed can make the remaining balance far easier to manage. Your financial situation is a complete picture, and sometimes other factors play a role.

Frequently Asked Questions About CNC Status

Even after getting a handle on the basics, people always have specific, practical questions about what currently non collectible status irs really means for them. Let's tackle some of the most common ones head-on.

Does CNC Status Hurt My Credit Score?

This is a classic "yes and no" situation. The IRS itself doesn't report your CNC status directly to credit bureaus like Experian or TransUnion. So, in that sense, no, the status itself won't show up on your report.

Here’s the catch: the IRS can still file a Notice of Federal Tax Lien against you even while you’re in CNC status. That lien is a public record, and credit reporting agencies absolutely pick up on those. A federal tax lien can do serious damage to your credit score.

How Long Does Currently Non Collectible Status Last?

There’s no set timeline. CNC status isn't like a timer that runs out; it's a reflection of your current financial reality. It stays in place for as long as you genuinely can't afford to pay your tax debt without creating a severe economic hardship for yourself.

The IRS won't just forget about you, though. They’ll periodically review your situation, usually every one to two years, to see if your income has improved. If they see you're back on your feet, they can remove the status and start collections again. The only hard stop is the ten-year Collection Statute Expiration Date (CSED)—if the clock runs out on that, the debt is gone for good.

Does Federal CNC Status Apply to State Tax Debt?

Absolutely not. This is a critical point that trips many people up. The IRS is a federal agency, and their decisions—including granting CNC status—have zero impact on what you owe your state's tax department.

Every state has its own set of rules, its own department of revenue, and its own hardship programs. You have to deal with them completely separately.

If you owe state taxes, you must contact your state's tax agency directly to inquire about their specific relief options. An approval for federal CNC status will not automatically pause state-level collections.

At Attorney Stephen A Weisberg, we believe in clarity and direct answers. Instead of guesswork, start with a complimentary tax debt analysis to understand your options and find the best path forward. Contact us today to get the help you need.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034