Filing Back Taxes Help: Your Complete Recovery Guide

Understanding Your Back Tax Situation

That sinking feeling in your stomach when you realize you have unfiled taxes is a common experience. It's easy to freeze up and avoid the problem altogether.

But the first step toward getting back on track isn't as scary as you think. It's simply about getting a handle on the facts, which takes the power away from the fear and puts it back in your hands.

How Many Years Do You Really Need to File?

So, where do you even begin? Most people's first question is how many years of unfiled returns they actually need to worry about. To be considered "current" with the IRS, you generally need to file returns for the last six years. The goal here is compliance, not punishment.

But there's a huge catch you need to know about. If you're owed a refund for any of those years, you only have three years from the original tax deadline to file and claim it. Miss that window, and your money goes to the U.S. Treasury for good.

Figuring out which years might get you money back versus which ones will result in a tax bill is a great place to start. If you want a deeper dive, you can check out our guide on how to file back taxes.

Assessing the Financial Impact

Putting off your back taxes doesn't make the problem go away—it just makes it more expensive. The IRS has a system of penalties and interest that grows over time. Two big ones to watch out for are:

Failure-to-File Penalty: This is a hefty 5% of what you owe for each month the return is late, maxing out at 25% of your unpaid tax.

Failure-to-Pay Penalty: This is a smaller 0.5% of your unpaid tax each month, but it also caps at 25%.

These penalties stack up fast. To put it in perspective, the IRS processed over 140 million returns during the 2025 tax season, and its systems are very good at spotting who's missing. You can see more filing season trends here. Every day you wait, interest is compounding not just on the tax you owe, but on the penalties, too.

Is This a Civil or Criminal Issue?

Let's tackle the biggest fear right away: going to jail. For almost everyone, failing to file taxes is a civil matter, not a criminal one. The key difference is your intent.

A civil issue means you owe money and need to work out a way to pay it. This is incredibly common and often happens because life throws a curveball—a family emergency, a job loss, or just getting overwhelmed and procrastinating.

A criminal case, on the other hand, involves willful tax evasion. To prove that, the government has to show you deliberately and intentionally tried to cheat the system. Think fake Social Security numbers, hiding offshore accounts, or creating phony invoices. Unless you were doing something like that, your problem is a financial one that has a solution.

Gathering Your Financial Documents And Records

Alright, let's talk about the part that can feel like a bit of a treasure hunt: rounding up all the necessary paperwork. This step can seem daunting, but breaking it down into a methodical search makes it far less stressful. The goal is to know where to look, who to ask, and what to do when you hit a dead end.

Your Primary Paper Trail

Before you start reaching out to others, your first stop should be your own records. Go through those old filing cabinets, desk drawers, and digital folders on your computer or cloud storage. You might be pleasantly surprised by what you’ve already saved.

If you come up empty on key income documents, here’s where to turn next:

W-2s: Get in touch with the HR or payroll departments of your former employers. Most can email you a copy without much fuss. If the company has since closed, don't panic—we have a backup plan for that.

1099s: If you worked as an independent contractor, a polite email to your old clients is the best first step. For investment income, such as a 1099-INT or 1099-DIV, your financial institution is the one to contact.

Bank Records: Your bank can provide statements from previous years, which are invaluable for tracking expenses or verifying income deposits. Keep in mind they might charge a small fee for retrieving older records.

The IRS Is Your Unlikely Ally

Here's a tip that many people miss when they need filing back taxes help: the IRS already has a significant amount of your income information on file. You can request a free Wage and Income Transcript for each unfiled year directly from them. This document is a lifesaver, as it shows the data from most income forms filed under your Social Security Number, including:

W-2s from your jobs

1099-NEC and 1099-MISC forms for freelance or contract work

1099-G for any unemployment benefits you received

1099-R for retirement plan distributions

This transcript won't include information about your deductions or any state taxes paid, but it gives you an excellent and official foundation for rebuilding your income picture.

To help you stay organized, here’s a quick-reference checklist. It breaks down the essential documents you'll need based on how you earned your income.

| Document Type | W-2 Employees | Self-Employed | Investment Income | Where to Obtain |

|---|---|---|---|---|

| W-2 Forms | ✅ | Former Employers, IRS | ||

| 1099-NEC/MISC | ✅ | Clients, IRS | ||

| 1099-INT/DIV/B | ✅ | Banks, Brokerages, IRS | ||

| Bank Statements | ✅ | ✅ | ✅ | Your Bank |

| Expense Receipts | ✅ | Your Records, Bank Stmts | ||

| Mortgage Interest (1098) | ✅ | ✅ | ✅ | Lender, IRS |

As you can see, there's quite a bit of overlap. The most significant difference is that if you're self-employed, the responsibility for tracking business expenses falls entirely on you.

When Records Are Gone For Good

So, what happens if a document seems to be lost to time? This is a common problem, especially for self-employed individuals trying to account for business expenses from several years ago. If you can’t locate receipts, the best approach is to carefully reconstruct your expenses using old bank and credit card statements.

For example, you can comb through a year's worth of statements to identify and add up all your software subscriptions, office supply purchases, and other deductible costs. This process of reconstruction is a cornerstone of effective tax resolution. It’s all about creating a logical and defensible financial summary that the IRS will accept, even without every single piece of original paper.

Navigating IRS Procedures And Requirements

Dealing with the IRS can feel like you're up against a faceless, intimidating giant, but it really operates on a set of predictable rules. Understanding its processes is the key to getting your back taxes filed without all the extra stress. It's less like a high-stakes courtroom drama and more like following a specific, albeit slow, administrative checklist.

The Right Order for Filing Multiple Years

When you're facing a stack of unfiled returns, there's a golden rule: prepare them chronologically, starting with the oldest year first. This isn't just about being neat; it directly impacts your bottom line. Certain tax items, like capital losses or a net operating loss from a business, can be carried forward to lower your taxable income in future years.

For example, if your business took a big loss in 2019, you can't figure out your 2020 taxes correctly until you know how much of that loss you can apply. Filing out of order will cause a domino effect of mistakes, meaning you'll have to go back and amend everything later. Always make sure you're using the official tax forms for each specific year, as they do change over time.

Submitting Your Returns and What to Expect

While you can file your current taxes online in minutes, getting help with filing back taxes often means taking a step back in time. The majority of returns for prior years must be paper-filed by mail. You can find all the old forms and instructions you need on the IRS website, so just be sure to download the correct versions for your specific tax years.

After you mail your returns, you'll need a healthy dose of patience. The IRS handles these manually, and it can take six months or more before you hear anything or receive a bill. Try not to worry if you don't get an immediate response. This snail's pace is a huge contrast to modern filing; while the IRS expects to receive over 86 million e-filed returns in 2025, that speed just doesn't apply to old paper returns. You can see more IRS filing statistics here to get a sense of the scale they operate on.

Communicating with the IRS

If you find you need to contact the IRS directly, go in prepared. Before you even think about dialing, have this information in front of you:

Your Social Security Number (or Individual Taxpayer ID Number)

Your birth date

The tax years in question

A copy of the return you filed, if possible

Be ready for long hold times—calling early in the morning can sometimes help. And what if you mail your return and then realize you made a mistake? Don't pick up the phone. Instead, you'll need to file an amended return using Form 1040-X. This form is specifically for correcting information you've already sent, and the IRS will process it separately.

Exploring Penalty Relief And Payment Options

Once you’ve tackled the stress of filing old returns, the fear of penalties and interest usually kicks in. But here’s some good news: the IRS is more than just a collections agency. It has several programs to help people get back on track, and securing this kind of filing back taxes help can seriously reduce your final bill.

Getting Penalties Wiped Clean

A surprising number of taxpayers are eligible for penalty removal but simply don't know they have to ask for it. The most common route is the First-Time Penalty Abatement (FTA). If you have a clean tax record for the previous three years, you're likely a good candidate. To qualify, you must have filed all your required returns and either paid your tax bill or set up a plan to do so. Think of it as a one-time "free pass" from the IRS for an honest oversight.

Another path is to claim reasonable cause. This option is for situations where you couldn't file or pay because of circumstances completely out of your control. Legitimate reasons might include:

A severe illness or the death of an immediate family member.

The destruction of your home, business, or records in a disaster like a fire or flood.

Following incorrect advice you received from a competent tax professional.

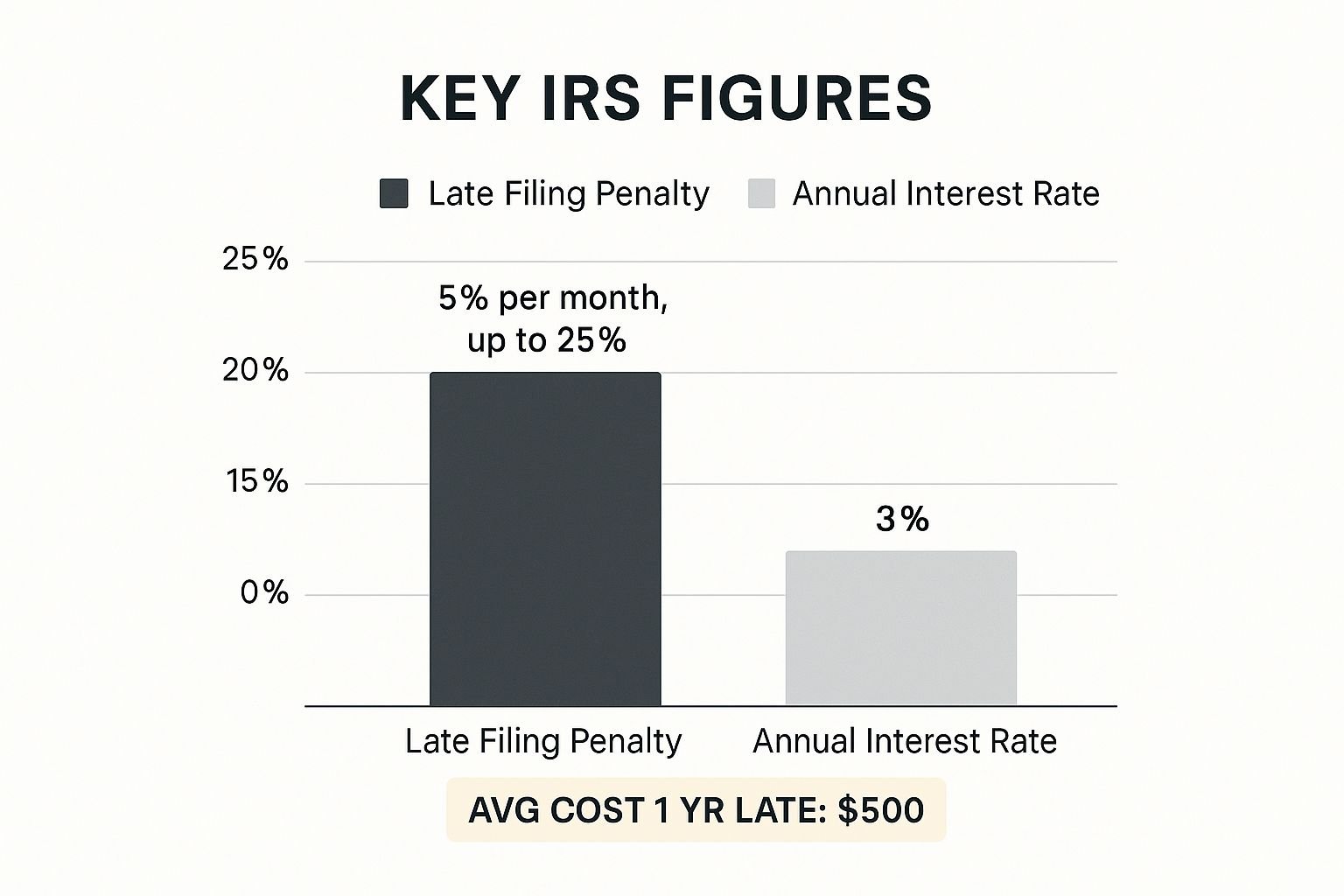

To really grasp why getting penalties removed is so critical, you need to see how fast they grow. This chart shows just how punishing the late-filing penalty is compared to the interest rate.

The takeaway here is that the 5% monthly failure-to-file penalty is the real problem. It can quickly eclipse the original tax you owed, which makes penalty abatement your most important goal. If you're arguing for reasonable cause, your success will depend entirely on having clear, organized documentation to back up your story.

To help you see which path might be right for you, let's compare the main relief options side-by-side.

IRS Penalty Relief Programs Comparison

Overview of available penalty relief options with eligibility requirements and potential savings

| Relief Program | Eligibility | Maximum Relief | Application Process | Success Rate |

|---|---|---|---|---|

| First-Time Abatement | Clean compliance record for the prior 3 years; all returns filed. | Waives failure-to-file and failure-to-pay penalties. | Typically a simple letter or phone call to the IRS. | High, if all criteria are met. |

| Reasonable Cause | Documented, unavoidable circumstances (e.g., illness, disaster, bad professional advice). | Waives penalties related to the specific incident. | Formal written request via Form 843 with supporting evidence. | Varies; depends on the strength and documentation of the case. |

| Offer in Compromise | Proven and significant financial hardship; doubt as to collectibility of the tax. | Settles the entire tax liability (tax, penalties, and interest) for less than the full amount. | Complex application (Form 656) with full financial disclosure (Form 433). | Lower; reserved for severe cases with strict IRS evaluation. |

As you can see, the best option really depends on your specific history and financial situation. First-Time Abatement is often the easiest win, while an Offer in Compromise is a much more involved process reserved for those with serious financial hardship.

Finding a Payment Plan That Works for You

Even after getting penalties removed, you might be left with a tax bill that's too big to pay off in one go. This is where IRS payment plans are a lifesaver. For many, a Short-Term Payment Plan, which gives you up to 180 days to pay, is a simple fix.

If you need more time, a formal Installment Agreement is the next step. This lets you make manageable monthly payments for up to 72 months. The IRS has made the application process for these agreements fairly simple, and you can often set one up directly on their website.

For those facing extreme financial difficulty, there's the Offer in Compromise (OIC). An OIC is a formal agreement that allows you to resolve your entire tax liability with the IRS for a lower amount than you originally owed.

This isn't a simple negotiation; the IRS will scrutinize your ability to pay by examining your income, expenses, and the equity in your assets.

Because an OIC is a complex and detailed process, we've put together a complete guide to tax debt settlement with an Offer in Compromise to walk you through every step.

Choosing the right option can mean the difference between years of crushing debt and a genuine fresh start.

Maximizing Refunds And Unclaimed Money

Most people assume that filing an old tax return automatically means writing a check to the IRS. In reality, you might be pleasantly surprised to find out you were actually owed a refund.

The only problem? The government has a strict deadline for you to claim that money. If you've been dragging your feet, you could be leaving cash on the table, which is why getting caught up is such an important financial move.

The Three-Year Refund Window

The IRS gives you exactly three years from the original due date of a tax return to file it and claim your money. This is called the refund statute of limitations. For example, your 2021 tax return was originally due in April 2022.

That means you have until April 2025 to file it and get your refund. Miss that deadline, and your money is permanently handed over to the U.S. Treasury. This is a huge incentive to stop procrastinating and get your returns filed.

Hunting For Overlooked Credits And Deductions

Tax rules change from year to year, so credits and deductions that were available in the past might not be around anymore. This is a common area where people miss out, because you need to look at each old return based on the specific laws for that year.

For instance, depending on the year, you might have been eligible for:

A much larger Child Tax Credit before it was reduced.

The American Opportunity or Lifetime Learning Credits for tuition you paid.

The Earned Income Tax Credit (EITC), especially if you had a lower-income year.

The IRS has processes designed to return this money. As of late March 2025, the agency had already processed nearly 61.6 million refunds, with the average payment being a hefty $3,170. This proves that there's a real financial benefit to filing, as a significant amount of money is regularly returned to taxpayers. You can see more recent IRS refund statistics here.

Strategic Filing When You Owe And Are Owed

So, what happens if you dig in and discover a mixed bag—you're due a refund for 2021 but owe the IRS for 2022? This happens all the time. When you file both returns, the IRS will automatically apply your 2021 refund to your 2022 tax bill. This is known as an offset.

This actually works in your favor. The offset immediately shrinks the debt that is accumulating penalties and interest. You're effectively using the government's money (your refund) to pay down what you owe.

This is a perfect example of how getting expert filing back taxes help can turn a complicated issue into a smart financial decision, helping you resolve multiple tax years at once while minimizing what you have to pay out of pocket.

When To Seek Professional Help

Look, the DIY spirit is strong, and for a single, straightforward late return, you might be perfectly fine handling it yourself. But how do you know when you've crossed from a simple "oops" into "I need backup" territory? Paying for an expert might seem like an extra cost, but it's often a small price compared to the potential savings in penalties, interest, and sleepless nights.

Warning Signs You Need a Pro

It’s time to put down the calculator and call an expert if you find yourself in one of these situations. These are clear signals that your tax problem has become too complex or high-stakes to manage alone.

Think about reaching out for help if:

You're behind on more than just one or two years of tax returns.

You’ve done a rough calculation and the tax you owe is likely to top $25,000.

The letters from the IRS are getting more serious, using words like "levy" or "lien."

Your finances aren't simple. You might have income from a business, juggle multiple 1099s from freelance work, or manage rental properties.

You think you could qualify for complex relief programs, which are notoriously difficult to navigate successfully without experience.

If any of this sounds familiar, getting professional filing back taxes help is a crucial step in protecting your financial well-being.

Choosing the Right Kind of Help

So you’ve decided to call in a professional—but who? Not all tax pros have the same background or focus. You'll generally run into three types:

Enrolled Agents (EAs): These are federally-licensed tax specialists. Their expertise is entirely focused on tax preparation and representing taxpayers directly before the IRS.

Certified Public Accountants (CPAs): Licensed by the state, CPAs offer a wider range of accounting services, including bookkeeping and financial planning, but they also handle tax problems.

Tax Attorneys: These are lawyers who specialize in tax law. They are your best bet for complex legal fights, potential criminal tax issues, or high-stakes audits where legal interpretation is key.

Even the IRS encourages taxpayers to find qualified representation and provides a directory to help you check a professional's credentials. The agency prefers to work with professionals who understand the system. When you're facing a really tough situation, like trying to settle your tax debt for less than you owe, having an experienced representative on your side is critical.

You can learn more in our article about successful tax relief strategies. The right pro does more than just fill out old forms; they create a strategy to get you the best possible outcome.

Moving Forward And Staying Compliant

Getting your back taxes sorted out brings an incredible sense of relief. Now, the big question is: How do you make sure this is a one-time experience? The best filing back taxes help you can give yourself is creating a few simple routines to prevent tax problems from ever piling up again.

Creating Your Year-Round Tax Strategy

Let's ditch the annual April tax scramble for good. Thinking about your taxes year-round isn't about becoming a financial guru; it's about treating it like any other regular part of your finances. A few minutes each month can save you a world of stress and money later on.

Here are a few game-changing habits you can start right now:

Make Your Phone Your Bookkeeper: Use a receipt-scanning app to snap photos of business expenses the moment you make them. No more shoeboxes full of faded receipts—just an organized digital folder ready to go.

Schedule Quarterly Financial Check-Ins: Put a reminder on your calendar every three months. It’s a quick chance to review your income, check your expenses, and make sure you're on track for any estimated tax payments.

Open a "Tax-Only" Savings Account: Set up an automatic transfer to move a percentage of every single payment you receive into a separate savings account. This "set it and forget it" approach ensures the money is there when the IRS comes calling.

Adjusting for the Future

Life changes, and your tax strategy needs to change with it. If you’re an employee, it’s smart to look at your Form W-4 withholdings every so often, especially after big events like getting married or having a child. A quick adjustment can prevent a surprise tax bill.

For freelancers and business owners, this is even more critical. If your income goes up or down, you absolutely need to recalculate your quarterly estimated payments. This single step can be the difference between a smooth tax season and a massive unexpected debt.

Building these habits is your best defense. But if you do run into another complicated issue, it's reassuring to know there are various tax debt solutions available to help you get back on solid ground without the panic.

If you're facing a tax problem that feels like too much to handle on your own, don't let it fester. Start with a FREE Tax Debt Analysis with an experienced attorney to see your options and map out a clear path forward.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034