A Guide to Form 9465 Instructions

When that letter from the IRS arrives and you see a tax bill you just can't pay, your stomach drops. It's a stressful feeling, but you're not alone in this. The good news is the IRS has systems in place for this exact situation, and one of the most common solutions is setting up a payment plan.

Is an IRS Installment Agreement Really Your Best Move?

Before you jump to conclusions, let's be clear. An installment agreement isn't the only option, and it might not even be the best one for you. It's simply a formal agreement with the IRS to pay your tax debt over time through manageable monthly payments.

The official paperwork for this is Form 9465, Installment Agreement Request. Think of it as your formal application to break down a large, overwhelming tax bill into smaller, predictable chunks. You can see the government's overview of the form on reginfo.gov, but what you really need to know is when to use it.

First, take a breath and look at the whole picture. An installment agreement might seem like the obvious choice, but it’s just one tool in the toolbox.

Your IRS Payment Options at a Glance

Here’s a quick rundown of the most common ways to tackle a tax bill you can't pay right away. This can help you see where an installment agreement fits in.

| Payment Option | Best For | Key Consideration |

|---|---|---|

| Short-Term Extension | You can pay in full soon, just not by the deadline (within 180 days). | Fewer fees and less interest accrue compared to a long-term plan. |

| Installment Agreement | You need more than six months to pay off the full amount. | Interest and penalties continue to accrue. There's a setup fee. |

| Offer in Compromise (OIC) | You genuinely cannot pay your full tax debt due to financial hardship. | Much harder to qualify for; requires extensive financial disclosure. |

As you can see, the right choice depends entirely on your specific financial situation.

The Reality of an Installment Agreement

So, who is this for? Before you even think about the form 9465 instructions, you need to see if you're a likely candidate. The IRS isn't just going to hand out payment plans to everyone.

Generally, you have a good shot at approval if:

You're up-to-date on your tax filings. This is non-negotiable. The IRS won't even consider a payment plan if you have unfiled returns from previous years.

Your total debt is under a certain limit. For a streamlined agreement, this is often $50,000 (including tax, penalties, and interest).

You can realistically pay it off. The IRS needs to see that you can clear the debt before the Collection Statute Expiration Date (CSED) expires, which is usually 10 years from when the tax was assessed.

Expert Tip: An installment agreement doesn't make your debt smaller. It's a tool to stop aggressive collection actions—like a bank levy or wage garnishment—while you pay what you owe. But be warned: interest and penalties don't stop. They keep adding up until your balance is zero.

Weighing the Good Against the Bad

Let's break down the trade-offs here. On the one hand, getting an installment agreement approved gives you immediate breathing room. The threatening letters stop, you get a predictable monthly payment, and you can sleep a little better knowing you have a plan.

The downside? It's going to cost you more in the long run. The failure-to-pay penalty and interest charges will continue to grow your balance.

There’s also a setup fee just to get the plan started (though it can be lowered or waived if you qualify as a low-income taxpayer). This is why it’s so critical to pay off the debt as fast as you can, not just make the minimum payment.

Gathering Your Documents Before You Start

Before you even think about filling out Form 9465, we need to talk about prep work. I've seen it time and time again: people dive in without the right info, and it’s a recipe for delays or outright rejection from the IRS.

Think of it like cooking. You wouldn't start a complicated recipe without getting all your ingredients on the counter first. Doing the same here will save you a world of frustration and prevent simple mistakes that can send you back to square one.

The Must-Have Information

Alright, let's get down to brass tacks. You absolutely cannot proceed without these key pieces of information. This is your non-negotiable list.

Your Taxpayer ID Numbers: This means your Social Security Number (SSN). If you filed a joint return, you'll need your spouse's SSN, too.

The Exact Tax Debt: No guesstimates. You need the precise dollar-and-cents amount you owe.

The Tax Year and Form: Be specific. Is this for the 2023 tax year? Is the debt tied to your Form 1040?

Every single one of these details has to match what the IRS has on file for you. Any mismatch, and you're looking at an automatic processing snag.

Finding the Right Numbers

So, where do you find this stuff? The IRS sends a lot of mail, and your best starting point is usually the most recent notice they've sent you.

Look for an official IRS notice, like a CP14. These letters spell out exactly how much you owe and for which tax period. If you can't find a recent notice, the next best thing is to pull out the copy of the tax return you filed for that year.

Pro Tip: Honestly, the easiest and most reliable way to get this info is by logging into your IRS online account. It’s a direct line to the source, showing your current balance, payment history, and all the specifics for each tax year. No guessing required.

Having these documents ready to go transforms a potentially painful task into a manageable one. It also helps to know what you’re getting into. For a closer look at your options, you can explore the various IRS payment plans and their nuances in our newsletter.

A Line-by-Line Walkthrough of Form 9465

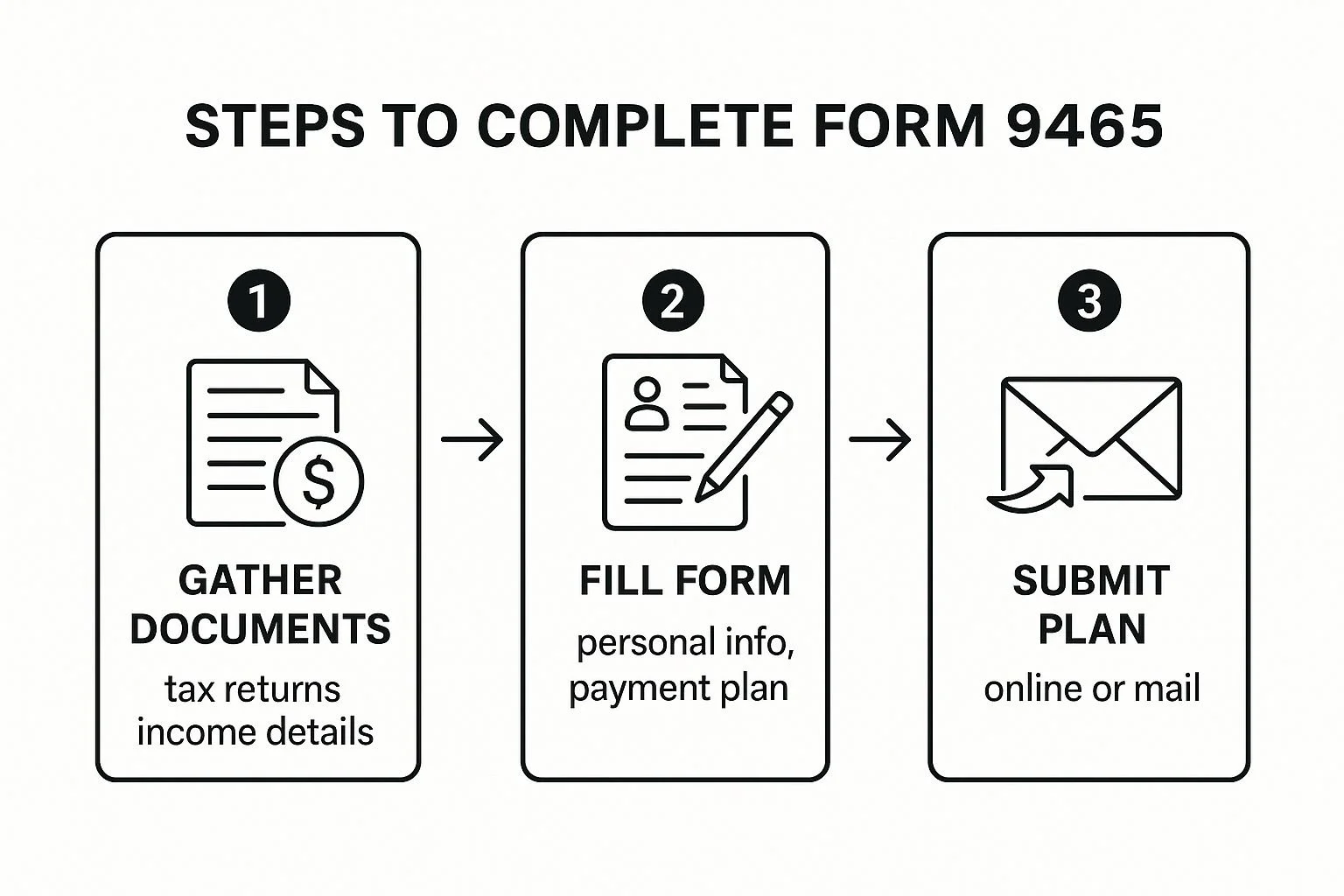

Alright, let's get down to brass tacks. You've got your documents ready, so it's time to tackle Form 9465. Don't let it intimidate you. We’re going to walk through this form together, line by line, so you can fill it out accurately and with confidence.

I always tell my clients that preparation is more than half the battle. This simple flowchart breaks down the process into three manageable stages: gathering your info, filling out the form, and getting it submitted.

As you can see, getting everything in order before you start writing is the key to a smooth process. Now, let’s dig into the form itself.

Part I: Your Basic Information

First up is the easy part, but it demands your full attention. Simple mistakes here are the number one reason for processing delays. Be meticulous.

Lines 1-4 Name and Address: Enter your name—and your spouse's, if you filed a joint return—exactly as it appears on your tax return. The same rule applies to your address. If you've moved since your last filing, use your current address.

Lines 5-6 Identifying Numbers: This is where your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN) goes. Read it, check it, and then check it again. This is how the IRS computer system finds you.

Line 7 Your Phone Numbers: Give them your home and work numbers. If an IRS agent needs to clarify something, being reachable can make the difference between a quick approval and weeks of waiting.

Lines 8a & 8b Employer Information: List your employer's name, address, and phone number. If you're your own boss, just write "Self-employed." Simple as that.

Part II: The Payment Proposal

This section is where the strategy comes in. It's your official offer to the IRS, outlining what you owe and, most importantly, what you plan to pay them each month.

Line 9 Tax Return Details: Specify the tax form number (usually Form 1040) and the tax year or years you owe for. It's very common to have debt spanning multiple years, and the good news is you can list them all on a single Form 9465.

Line 10 Total Tax Owed: Find the total amount you owe on your tax return or the most recent notice the IRS sent you. Don't guess—be precise.

Line 11 Proposed Monthly Payment: This is the most critical line on the entire form. You need to propose a monthly payment amount. The key here is to be realistic but fair. The IRS needs to see you're offering the largest payment you can reasonably afford.

A Word of Experience: Proposing a token amount, like $25 a month on a $20,000 debt, is a huge red flag for the IRS. It suggests you aren't serious about clearing the debt. They expect your proposed payment to be enough to pay off the full balance within the 10-year Collection Statute Expiration Date (CSED).

Line 12 Desired Payment Day: You get to pick a day of the month for your payment, anywhere from the 1st to the 28th. I strongly advise clients to pick a date that's a day or two after their regular payday. This ensures the funds will always be there, preventing a costly default.

Navigating Payment Methods and Fees

The form will then ask how you plan to pay. Your answer here will directly affect the setup fees you're charged.

Line 13 Direct Debit This is the IRS's preferred method, and for good reason. You authorize them to automatically pull the payment from your bank account each month. It's the most convenient option and also comes with a lower setup fee. If you choose this, you'll need to provide your bank's routing and account numbers and sign the authorization right there on the form.

Line 14 Check, Money Order, or Other If you'd rather have control and mail a payment yourself each month, this is your option. Just be aware that the IRS charges a higher setup fee for this manual method.

To get the full picture, you can always review the complete form 9465 instructions directly from the IRS. They provide the official breakdown of every field and calculation.

Finally, you’ll sign and date the form. By signing, you're swearing under penalty of perjury that everything you've entered is true. If you filed a joint tax return, both you and your spouse must sign the form for it to be valid.

How to Calculate a Realistic Monthly Payment

This is where the rubber meets the road. Deciding on the monthly payment amount to propose on Form 9465 is easily the most critical part of this whole process. It's a bit of a tightrope walk.

If you offer a payment that’s too low, the IRS might just say no, sending you right back to square one. But if you propose a number that's too high, you could find yourself unable to keep up when an unexpected expense pops up. A defaulted agreement is often worse than having no agreement at all.

The real goal here is to find that perfect middle ground—a payment you can comfortably afford that the IRS will also find acceptable. This isn't a time for guesswork; it's about taking a quick but honest look at your real financial situation.

Finding Your True Disposable Income

Before you can even think about filling in Line 11 on the form, you need to know what you can actually afford to pay each month. This means getting a handle on your true disposable income.

It doesn’t have to be complicated. Just grab a notepad or open a spreadsheet and jot down two columns:

Total Monthly Income: This is all the money coming in after taxes. Include your regular paycheck, any side gig income, and anything else you receive consistently.

Essential Monthly Expenses: Be brutally honest with yourself. This isn't just rent and a car payment. It's groceries, utilities, insurance, gas, and the minimum payments on your credit cards or other loans.

Now, subtract your essential expenses from your income. That number you're left with? That's your disposable income. It's the maximum amount you could theoretically send to the IRS.

Crucial Takeaway: Whatever you do, don't propose your entire disposable income as your payment. Life happens. Cars need repairs, kids get sick. Always build in a buffer for those surprises. A good rule of thumb is to offer between 50% and 75% of that final number.

The IRS's Unspoken Rule: The CSED Clock

Here's something the IRS doesn't advertise on the front page of its website: they are working against a clock. It's called the Collection Statute Expiration Date (CSED), and it's a 10-year countdown that starts the day your tax is officially assessed.

From the IRS’s perspective, any payment plan you propose must be large enough to clear your entire debt—including all the interest and penalties that will continue to pile up—before that 10-year window slams shut.

So, if you owe $24,000, an offer of $100 a month is likely dead on arrival. Why? Because it would take 20 years to pay off, long past the CSED. You can get a much better feel for how different payment amounts will play out by running the numbers through an IRS installment agreement calculator.

Guaranteed Acceptance for Smaller Debts

Now for some good news. There’s a major exception that makes this whole calculation much simpler for a lot of people. The IRS offers a streamlined, almost guaranteed approval path for taxpayers who owe a relatively small amount.

This is a massive advantage. It removes nearly all the stress and guesswork from the process.

Statistically, millions of Americans rely on these plans. In fact, about 11 million taxpayers currently have active agreements to manage $65 billion in tax debt.

To handle that volume, the IRS has simplified things. If your total balance is $10,000 or less, you’ve filed all your tax returns for the past five years, and you can commit to paying off the debt within three years, your request will almost certainly be approved without a deep dive into your finances.

You can see more facts and figures regarding IRS payment plans on TurboTax's blog. This is a key provision in the Form 9465 instructions that can get you a quick "yes."

Submitting Your Form and What to Expect Next

You’ve done the hard part and filled out Form 9465. Now, you need to get it in front of the right people at the IRS. How you submit it is just as crucial as filling it out correctly, and you basically have two paths: the fast-track online route or the traditional paper-and-mail method.

For most people, I strongly recommend using the IRS Online Payment Agreement (OPA) tool. It’s the quickest, most straightforward way to get this done.

The biggest advantage? You often get an immediate decision on your request, which saves you from weeks of stressful waiting. But if you’re more comfortable with paper or have a more complicated tax situation, mailing the form is still a solid option.

Mailing Your Form 9465

If you're filing Form 9465 with your current year's tax return, it’s simple. Just attach the form to the front of your Form 1040 and mail everything to the address listed in your tax return instructions.

However, if you're sending it in separately to deal with an old tax bill, where you mail it depends entirely on where you live. For example, if you're in New York or Massachusetts, your form goes to Holtsville, NY. But if you're a taxpayer in California or Arizona, you'll be sending it to Ogden, UT. Double-check you have the right address—sending it to the wrong facility will definitely slow things down.

Key Takeaway: If you mail your Form 9465, expect the IRS to take 30 to 60 days to respond. Try not to worry during this time. No news is usually just a sign that your request is in the queue and being processed.

After You've Sent It In

Once the IRS reviews your application, you’ll receive a letter in the mail. This official notice will either approve your installment agreement or explain why it was rejected. If you’re approved, the letter will lay out all the terms—your monthly payment amount, the due date, and any setup fees you might owe.

As soon as you're approved, the ball is in your court.

Make Your First Payment: Don't wait for the first official due date on your statement. Go ahead and send your first payment as soon as you get the approval notice.

Stay Compliant: This is the most important rule. You absolutely must file all your future tax returns on time and pay any new taxes you owe in full. If you fall behind on new tax obligations, the IRS can, and likely will, default your agreement.

Remember, an installment agreement is just one tool in the toolbox. If you’re facing a serious financial struggle, you might want to see how to qualify for an Offer in Compromise, which can sometimes settle your debt for much less than you owe. For now, staying on top of your approved payment plan is the key to finally resolving your tax debt and avoiding more aggressive collection actions.

Common Questions About Form 9465

Even with the instructions right in front of you, stepping into a payment plan with the IRS can feel like walking into a maze. It’s completely normal to have a long list of "what-if" questions pop up. Let's walk through some of the most common concerns I hear from clients so you can get this done with confidence.

What Happens If I Can't Make a Monthly Payment?

Life happens. The IRS gets that, at least to a point. If you see a missed payment on the horizon, the absolute best thing you can do is call the IRS right away. Don't wait.

Ignoring the problem is the fast track to defaulting on your agreement. A default can unwind all your hard work, potentially leading to the very things you were trying to stop, like wage garnishments or a levy on your bank account. If your financial picture has genuinely changed for the worse, you might be able to work out new terms. Being proactive shows the IRS you’re trying to do the right thing.

Can I Get a Plan if I Haven't Filed All My Taxes?

This is a hard "no." The IRS will not even consider an installment agreement until you are fully caught up on all your past tax filings. It’s a non-starter.

If you have unfiled returns from prior years, your first job is to get those prepared and sent in. This is a must-do, even if you know you can't pay the balance on those returns. The IRS simply won't negotiate a payment plan for one tax year while others are still missing in action.

Key Insight: To the IRS, "compliant" means all required returns have been filed and you're up to date on your current estimated tax payments. This is a fundamental rule of the game.

Do Interest and Penalties Stop After Approval?

This is a huge misconception, and it's a costly one. No, interest and penalties do not stop accruing.

Getting your plan approved can cut the failure-to-pay penalty rate (often in half), but it doesn't make it disappear. More importantly, interest keeps piling up on your entire unpaid balance every single day until it's paid off. This is why you should always try to pay more than the minimum whenever possible. Every extra dollar you send shrinks the principal, which in turn reduces the total interest you'll pay over the life of the debt. For those with a much larger liability, learning how to settle IRS debt might reveal more suitable options.

Is the Online IRS Tool Better Than Mailing the Form?

For most people, yes, without a doubt. The IRS's Online Payment Agreement (OPA) tool is way faster and you'll often get an answer instantly. If you mail in a paper Form 9465, you could be waiting 30 to 60 days just for them to process it.

The setup fees are also much lower when you apply online. The one catch is that the online tool has its limits. If you owe more than $50,000 or have a more complex financial situation, you'll likely have to stick with the paper Form 9465 and provide a full financial disclosure.

Facing tax debt can be overwhelming, but you don't have to handle it alone. At Attorney Stephen A Weisberg, I start with a FREE Tax Debt Analysis to determine the best path forward for your specific situation.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034