What to Do If You Haven't Filed Taxes in 3 Years

That sinking feeling in your stomach when you realize you haven't filed taxes in 3 years is something I've seen countless times. It’s easy to feel paralyzed, but here’s the good news: the absolute best thing you can do is start tackling it right now.

Believe it or not, the IRS actually prefers when taxpayers come forward voluntarily. Taking that first step can head off much bigger problems down the road. And here's a crucial point most people miss: you might even be owed a refund, but that opportunity disappears if you wait too long.

Your First Move When You Haven't Filed Taxes in 3 Years

It’s human nature to avoid something this stressful, but letting it fester only compounds the penalties and interest. Procrastination is your worst enemy here.

The key is to take back control with a clear, manageable plan. Remember, the IRS isn’t on a witch hunt; their main objective is to get taxpayers back into the system and compliant. Coming to them first puts you in a much stronger position.

When you're facing multiple unfiled returns, knowing where to begin is half the battle. This quick checklist breaks down your immediate priorities.

Immediate Action Checklist for Unfiled Returns

| Action Item | Why It's Important | Where to Start |

|---|---|---|

| Stop Procrastinating | Penalties and interest grow daily. The sooner you act, the less you'll potentially owe. | Set a specific, non-negotiable time this week to start gathering info. |

| Check the Refund Clock | You only have 3 years from the original due date to claim a refund. Don't let your money disappear. | Identify the oldest unfiled year. If it's approaching the 3-year mark, prioritize it. |

| Gather Your Documents | Accurate returns start with the right paperwork. This prevents errors and future IRS notices. | Request an IRS Wage and Income Transcript online. It's the fastest way to get your W-2s and 1099s. |

| Don't Assume You Owe | Many non-filers are actually due a refund from withholding but never claim it. | Look at your W-2s. If your federal withholding is high, you might be getting money back. |

This checklist isn't about solving everything at once; it's about building momentum. Taking these small, concrete steps will demystify the process and put you back in the driver's seat.

Why Acting Now Is Critical

Time is absolutely your enemy, especially when it comes to potential refunds. The IRS has a strict three-year statute of limitations for claiming any money you're owed. If you let that deadline pass, the refund is gone forever.

This rule makes your oldest unfiled return the most urgent one. If that three-year window closes, you forfeit that money directly to the U.S. Treasury—even if you still owe taxes for other years.

The most common mistake people make is assuming they owe money without checking. Millions of dollars in refunds go unclaimed every year simply because people fail to file. Don't let that be you.

Gather Your Essential Documents

Okay, time for the first concrete step: collecting your financial documents for each of the three years. This is the bedrock of filing accurate returns. Even if your records are a mess, don't panic. Most of what you need can be retrieved.

You'll need to round up things like:

W-2 Forms: From every single employer during those years.

1099 Forms: For any freelance work, contract gigs, or other miscellaneous income (look for forms like the 1099-NEC or 1099-MISC).

Other Income Records: This includes things like investment statements (1099-INT, 1099-DIV) or any other relevant financial data.

If you’re staring at that list and thinking, "I have no idea where those are," there's a simple solution. You can request an IRS Wage and Income Transcript directly from the IRS website.

It's a free report that shows all the income information that was reported to the IRS under your Social Security number for a given year. Forgetting to file can happen for all sorts of reasons.

Gathering Your Financial Documents for Past Years

Alright, let's get into the nitty-gritty. To file an accurate return, you need the right documents. I know that after three years, your records might be a complete mess or even nonexistent. Don't panic. The IRS actually gives you the perfect place to start.

Your first move should be to head over to the IRS website and request a Wage and Income Transcript for each year you didn't file. Seriously, this thing is a lifesaver. It lists all the income information the IRS already has on you—W-2s from old jobs, 1099s from freelance gigs, you name it.

Finding What the IRS Doesn't Know

Now, those IRS transcripts are fantastic for income, but they don't tell the whole story. They won't show you any of the deductions or credits that could slash your tax bill. For that, you’ll have to do a bit of digging.

This is where your own financial records come into play. Your bank statements are a goldmine. If you don't have them handy, it’s worth taking a moment to figure out how to download bank statements from your online banking portal.

Once you have those statements, you can start hunting for clues about all the expenses that could lower what you owe.

Look for these common deductions:

Business Expenses: If you were self-employed, scan for any supply purchases, software you paid for, home office costs, or even mileage if you have logs.

Charitable Donations: Did you give to any qualified charities? Your bank or credit card statements can back this up.

Medical Expenses: Track down records of any significant medical bills. They might be deductible if they add up to more than a certain percentage of your income.

Educational Costs: Look for tuition payments or student loan interest statements (Form 1098-E), as these can open the door to some valuable credits.

Think of yourself as a financial detective. Every receipt, bank transaction, or old email confirmation is a potential clue that can help you piece together an accurate financial history and ensure you don’t pay a dollar more in taxes than necessary.

This is why a detailed approach is so important. When you haven't filed taxes in 3 years, reconstructing these records is your best shot at maximizing a potential refund or minimizing the amount you owe. Even if you can't find every single receipt, your bank statements create a solid foundation. Trust me, the time you spend here will pay off.

Understanding the Consequences of Not Filing Taxes

It’s easy to let tax filing slide. In the short term, ignoring it feels simpler. But that feeling is temporary, and the financial consequences are very real and designed to get worse over time.

The first step to fixing this is to understand what you're actually up against. It's not as scary or mysterious as you might think. The IRS isn't some boogeyman; it's a bureaucracy following a script to collect what's owed.

When you haven't filed taxes in 3 years, the problem isn't just the tax you originally owed. It's the penalties and interest that have been piling up, turning a small problem into a much bigger one.

The Two Big Penalties Explained

The IRS hits you with two main penalties when you don’t file and pay. You absolutely need to know the difference, because one is way more painful than the other.

Failure to File Penalty: This is the one that really stings. It’s 5% of what you owe for every month (or even part of a month) that your return is late. This penalty doesn't grow forever, but it can hit a maximum of 25% of your total unpaid tax bill.

Failure to Pay Penalty: This one is much gentler. It’s only 0.5% of your unpaid taxes each month. Like the other penalty, it also maxes out at 25%.

Look at those numbers again. The penalty for not filing is 10 times higher than the penalty for not paying. This is the single most important thing to understand. It’s why any tax pro will tell you to file your return on time, even if you can't send a single dollar with it. Just getting the return in stops that nasty Failure to File penalty dead in its tracks.

How Interest Makes Everything Worse

As if the penalties weren't enough, the IRS also charges interest on the whole mess—the original tax, the Failure to File penalty, and the Failure to Pay penalty. And this isn't simple interest; it compounds daily. You are literally paying interest on your interest. The rate changes, but it's climbed as high as 8% recently.

This combination of stacking penalties and compounding interest is exactly how a manageable tax debt from three years ago can snowball into something that feels completely overwhelming today.

"I see this all the time. Someone thinks, 'I can't pay, so I won't file.' That's the worst possible move. Filing the return immediately halts the most aggressive penalty and is the first concrete step toward getting right with the IRS."

Let's put some real numbers to this. Say you owed $3,000 for a return due three years ago and you just never filed it.

Here’s a rough breakdown of what happens:

The Failure to File penalty would have hit its 25% max pretty quickly, tacking on $750.

The Failure to Pay penalty would have been ticking along for 36 months, adding another $540 (0.5% x 36 months x $3,000).

All the while, interest would have been compounding daily on the original tax and the growing penalty balance for three straight years.

Your original $3,000 problem is suddenly a lot closer to a $5,000 debt. This is why you can't afford to wait. When you haven't filed taxes in 3 years, the consequences are predictable and expensive. But the good news is, the solution starts with one simple action: getting those old returns prepared and filed. That act alone can save you a surprising amount of money.

How to Prepare and File Your Overdue Returns

With all your documents finally in one place, it's time to actually file. I know this is the part that feels the most daunting, especially if you haven't filed taxes in 3 years. But honestly, it boils down to picking the right approach for your situation. You're basically choosing between tax software, hiring a pro, or going old school and mailing the forms yourself.

Each path makes sense for different people. If your finances are simple—say, you just have W-2 income and you're taking the standard deduction—prior-year tax software can work just fine. But if your situation is more tangled with multiple income streams, investments, or business expenses, calling in a tax professional is almost always a wise move.

Finding the Correct Tax Forms

Here's a rookie mistake I see all the time: using the current year's tax forms to file for a past year. The IRS tweaks its forms every single year, and sending in the wrong one is a surefire way to get it rejected.

You have to use the specific Form 1040 that corresponds to the exact year you're filing.

The good news is the IRS keeps an archive. You can find all the prior-year forms and instructions you need right on their website. Just search for "Form 1040" and the year (like "Form 1040 2021"), and you'll find the right PDFs. It's a bit of a pain, but it's absolutely critical to get this right.

Pro Tip: Always, always file your back taxes in chronological order. Start with the oldest year first and work your way forward. Tax years are connected—things like a capital loss carryover or a change in your adjusted gross income from one year directly affect the next. Filing out of order creates a domino effect of errors that you'll have to fix with amended returns down the line.

Choosing Your Filing Method

Okay, so how should you actually submit these returns? Your choice here really depends on how complex your taxes are and how confident you feel tackling them. To help you decide, let's look at the options side-by-side.

Filing Options for Back Taxes

| Filing Method | Best For | Pros | Cons |

|---|---|---|---|

| Tax Software | Simple returns (W-2 income, standard deductions). | Cost-effective and guides you through the process. | Cannot e-file older returns; limited support for complex issues. |

| Tax Professional | Complex situations, significant tax debt, or high anxiety. | Expert guidance, maximizes deductions, handles IRS communication. | The most expensive option upfront. |

| DIY Mail-In | Straightforward returns for detail-oriented individuals. | The lowest direct cost. | High risk of errors; no professional support; you handle all IRS correspondence. |

Choosing the right method from the start can save you a world of headaches later on.

Tax Software: Some services offer access to software for previous years. It's a good, affordable option for simple returns, but remember this key detail: you almost always have to print and mail returns that are more than a year or two old. E-filing is usually off the table.

Tax Professional: Bringing in a CPA or Enrolled Agent who specializes in back taxes can be the best money you'll ever spend. They live and breathe this stuff. They'll find deductions you didn't know existed and will take over all communication with the IRS, which is a huge weight off your shoulders.

DIY Mail-In: You can always print the forms, fill them out by hand, and mail them in. This gives you total control but also total responsibility. If you go this route, you need to be meticulous. And please, send everything via certified mail with a return receipt. You need that proof of filing.

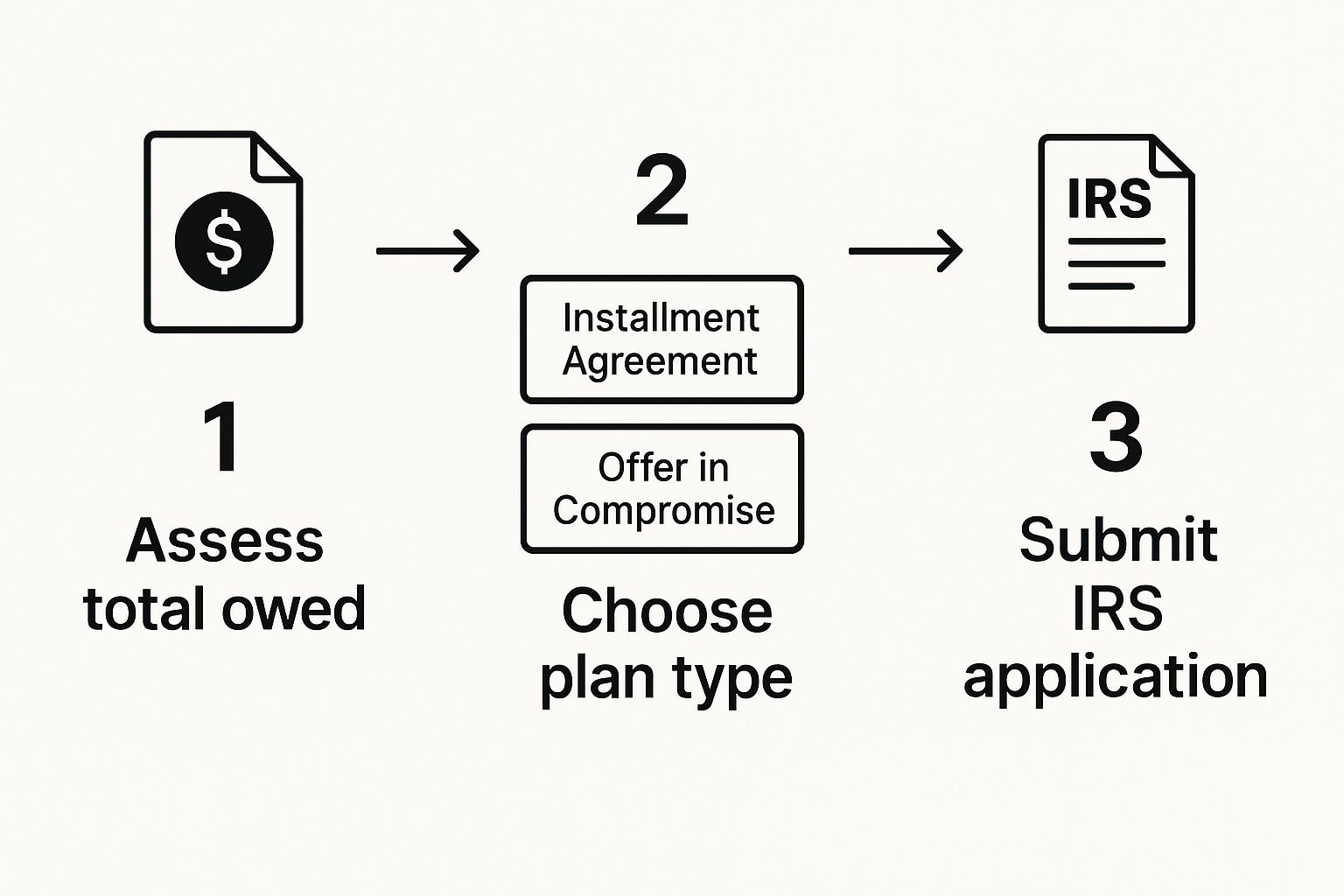

This chart gives you a visual of what happens after you've filed and figured out what you owe.

As you can see, once you know the total amount due, you aren't just left hanging. The IRS has structured programs like an Installment Agreement or an Offer in Compromise to help you manage the debt.

Whichever path you take, the mission is the same: get accurate and complete returns filed for every single missing year. For a deeper dive into the nitty-gritty, check out our complete guide on how to file back taxes. Getting this done correctly is your first real step out of tax trouble and toward peace of mind.

Navigating Your Options if You Owe the IRS

Okay, you’ve ripped off the Band-Aid and filed those overdue returns. Now comes the hard part: staring at the total amount you owe. That number can feel like a punch to the gut, but I promise you, it's not a dead end.

The IRS has several structured programs designed for people in your exact situation. They aren't looking to ruin you. In fact, the agency would much rather work with you to find a manageable solution than push you into a corner. The key is knowing what’s available.

IRS Payment Plans and Agreements

For most people who haven't filed taxes in 3 years and are now facing a bill, an IRS payment plan is the most common and direct path forward. These are bread-and-butter solutions for the IRS, and they're relatively simple to set up once your returns are officially filed.

Here are the two main flavors:

Short-Term Payment Plan: Think you can knock out the debt within 180 days? This is your best bet. A short-term extension usually involves less red tape and fewer fees than a long-term plan.

Installment Agreement: This is the go-to for larger balances. It’s a formal plan that lets you make monthly payments for up to 72 months (that's six years). It’s designed for anyone who needs more breathing room to get their debt handled.

Simply getting one of these plans in place sends a clear signal to the IRS: you're taking this seriously. That alone can keep more aggressive collection actions, like liens or bank levies, off the table.

Solutions for Significant Financial Hardship

But what if even a monthly payment feels out of reach? If you're facing real financial distress, the IRS has other relief options, though the bar for qualifying is much higher.

An Offer in Compromise (OIC) is a big one. This allows certain taxpayers to settle their tax liability for less than the full amount owed. It's not a get-out-of-jail-free card, though. The IRS scrutinizes your ability to pay, income, expenses, and asset equity. An OIC is a complex process reserved for those in genuinely tough financial spots.

Another route is being placed in Currently Not Collectible (CNC) status. This is essentially the IRS hitting the pause button on collections because they can see you can't afford to pay your basic living expenses, let alone your tax bill. Just know that while they stop actively collecting, your debt doesn't disappear—penalties and interest will keep piling up.

A Lifeline for Penalties: First-Time Abatement

Here’s a powerful tool that many people—and even some tax pros—overlook: First-Time Penalty Abatement. If you had a clean track record with the IRS before this period of non-filing, the agency might agree to waive the Failure to File and Failure to Pay penalties for the first year you missed.

This can be huge. To qualify, you must have all your returns filed and either pay the tax due or get on a payment plan. When you haven't filed taxes in 3 years, this could wipe out the penalties for one of those years, making a serious dent in your total balance.

There are many ways to tackle a tax bill, from payment plans to personal loans. And if you’re considering other financing, it’s worth asking, Can Personal Loans Be Used to Pay Off Taxes?.

Answering Your Top Questions About Filing Back Taxes

The moment you realize you haven't filed taxes in 3 years, a wave of questions—and a good bit of anxiety—usually follows. It’s completely normal. Let’s cut through the noise and tackle the most common worries I hear from clients every day.

Am I Going to Jail for Not Filing My Taxes for 3 Years?

Let’s get the biggest fear out of the way first. The short answer is: almost certainly not.

While tax evasion is a crime, the IRS reserves its criminal investigations for the most egregious cases—think deliberate, large-scale fraud. Their main goal isn't to put people in jail; it's to collect the tax that's owed and get you back on track with your filing obligations.

When you come forward voluntarily to file your old returns, you're showing the IRS you want to comply. For the vast majority of people in this situation, the issue will be handled with civil penalties and interest, not handcuffs.

What if the IRS Has Already Filed a Return for Me?

If you haven't filed, the IRS may eventually create something called a Substitute for Return (SFR) for you. Don't be fooled by the name; an SFR is rarely a good thing for the taxpayer.

The IRS builds this return using only the income data they have on file from W-2s and 1099s. Crucially, they don't include any of the deductions or credits you're entitled to. This means the tax bill they calculate is almost always much higher than what you actually owe.

The good news? You have the right to file your own, correct tax return to replace their version. By filing your own return, you can claim all your rightful deductions and credits, which can drastically reduce or even wipe out the balance the IRS calculated.

The Substitute for Return is the IRS's best guess, and it's always a guess that favors them. Filing your own accurate return is your right and your best defense against an inflated tax bill.

I Know I Owe Money, So Should I Even Bother Filing?

Yes. Absolutely. Filing is always the right move, even if you can’t pay immediately.

First off, filing is a legal requirement. More practically, not filing opens you up to a nasty Failure to File penalty. This penalty can be up to 10 times higher than the Failure to Pay penalty. Simply getting the return filed stops that aggressive penalty in its tracks.

You might even be wrong about owing. It's not uncommon for people to be due a refund for one or more of those unfiled years. But you'll lose that refund forever if you don’t file within three years of the original due date. Beyond that, having unfiled returns can be a major roadblock for getting a mortgage or other loans, and you won't get Social Security credit for those years of work.

At Attorney Stephen A Weisberg, we understand the stress of facing the IRS. Instead of demanding a large retainer upfront, we start with a FREE Tax Debt Analysis to determine exactly how we can help.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034