What Is State Tax Levy? How to Stop It Quickly

When you get a notice about a state tax levy, it's not another bill or a simple warning. It’s the final, serious step where the state legally seizes your property to cover an unpaid tax debt. This is the moment the state stops asking and starts taking—whether it's money from your bank account, a chunk of your paycheck, or other valuable assets.

Understanding What a State Tax Levy Really Means

So many people hear "lien" and "levy" and think they're the same thing. They absolutely are not. Getting this distinction right is the first, most critical step to getting back on solid financial ground.

The Critical Difference Between a Lien and a Levy

Let’s break it down simply. A tax lien is a public claim. The state is essentially putting a legal "dibs" on your property, telling the world you owe them money. It’s a passive move that secures their interest in your assets and can tank your credit, but you still get to keep your stuff.

A state tax levy is when the gloves come off. This is the enforcement of that claim. The state moves past simply claiming your property and actively starts the process of seizing it.

Think of it like this: a lien is a foreclosure notice taped to your front door. A levy is the sheriff showing up to change the locks. The first is a warning; the second is the action.

Tax Lien vs Tax Levy At a Glance

To make this crystal clear, here’s a quick side-by-side comparison.

| Feature | State Tax Lien | State Tax Levy |

|---|---|---|

| What It Is | A legal claim against your property | The actual seizure of your property |

| Primary Purpose | To secure the government's interest in your assets | To collect the money owed by taking assets |

| Impact on You | You keep your property, but your credit is damaged | The state takes your property (bank funds, wages, etc.) |

| Nature | A passive "hold" or public notice | An active, forceful collection action |

Knowing the difference helps you understand exactly where you stand in the collections process.

How a Levy Becomes Reality

A levy isn't a surprise attack. It's the end of a long road that starts after you’ve received several notices about your tax debt and haven't resolved it. The state gives you multiple opportunities to pay or make arrangements before resorting to something this drastic.

State tax agencies have the authority to garnish wages, clean out bank accounts, and even take physical property after sending all the required legal notices. While each state has its own nuances, many base their procedures on federal standards.

You can learn more about the IRS definition of a levy to get a feel for the general framework most states follow. Once you truly grasp what a levy is, you’ll start seeing those official-looking envelopes from the state tax agency for what they are: a countdown clock. And you’ll know it’s time to act before it’s too late.

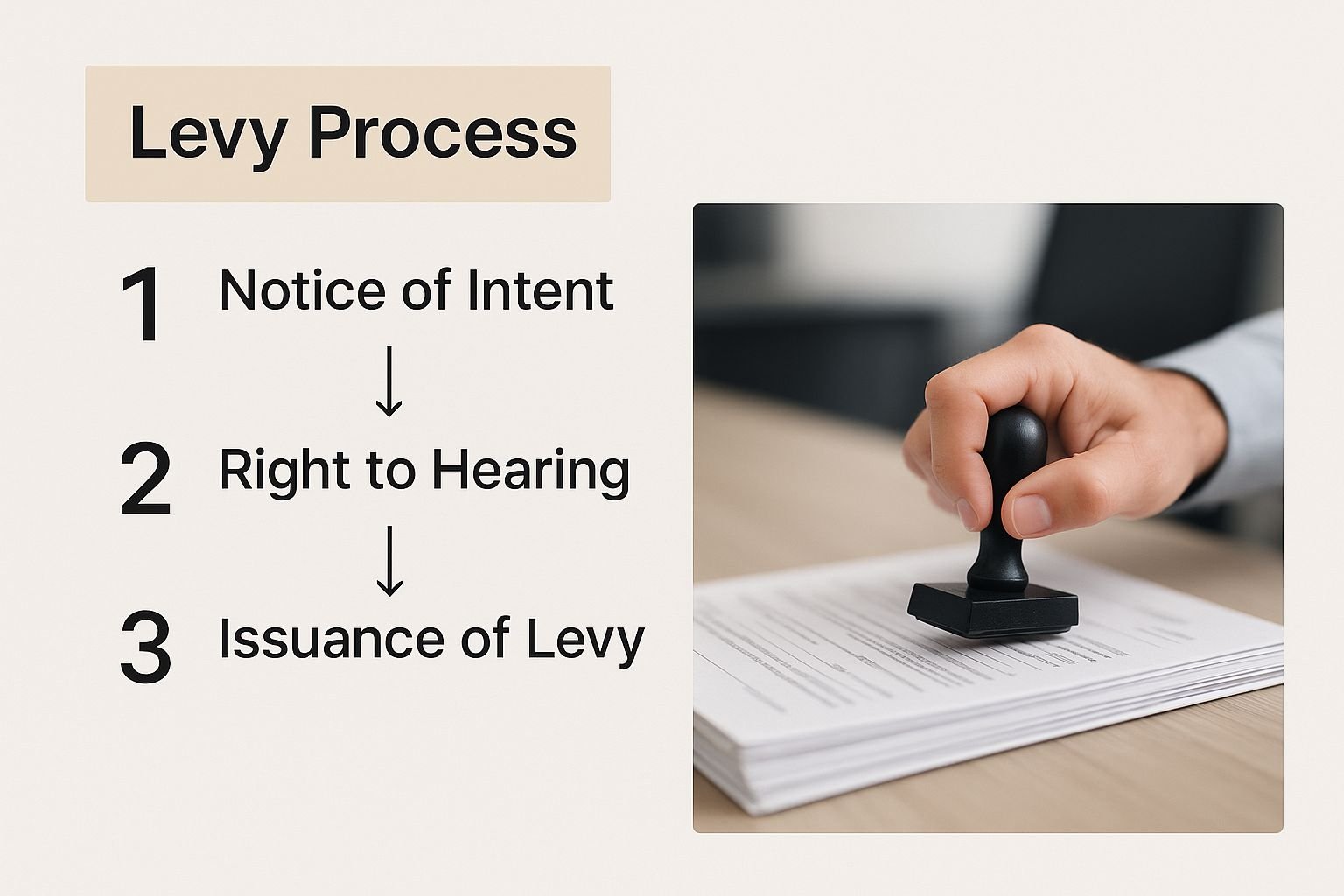

The Path From Unpaid Taxes to a Levy Notice

A state tax levy doesn’t just happen out of the blue. It’s the final, predictable outcome of a long process that starts with a single unpaid tax bill. The journey from a simple tax debt to having your assets seized unfolds in stages, and it only gets serious when you ignore the warning signs.

This process often kicks off with missed filing deadlines, which can lead to hefty penalties for late tax returns that cause the initial debt to snowball. But at every step, the state sends official letters giving you a chance to get things sorted out.

Knowing how this works is key. It takes the mystery out of the process and shows you just how many opportunities you have to step in and prevent the state from taking your property. The only way it escalates is if you ignore those letters.

This infographic breaks down the typical timeline, from the first bill to the final, serious enforcement action.

As you can see, it's a clear, escalating series of steps. The state gives you plenty of notice before they actually seize anything.

The Initial Tax Bill and First Notices

Everything starts with a normal tax bill. If you don't pay it, the state will mail you a Notice and Demand for Payment. Think of this as the first official red flag. The notice will clearly state what you owe—including any interest and penalties that have started piling up—and give you a firm deadline to pay.

If you don’t respond, more letters will arrive, each one a bit more insistent than the last. These notices aren’t just junk mail; they are your road map to fixing the problem, explaining your rights and the options you have to settle the debt.

It's a huge mistake to think these early notices are just routine paperwork. They are legally required warnings that start a countdown. Every letter you ignore brings you one step closer to a levy.

Escalation to the Final Notice

After sending several notices without a response, the state will play its final card: the Final Notice of Intent to Levy. This is not a drill. This letter is the state's way of telling you they now have the legal right to seize your assets and will do so if you don't act within a specific timeframe—usually 30 days.

This final notice is also your last formal chance to fight back. It will detail your right to a hearing or an appeal if you believe the tax amount is wrong or have another legitimate dispute.

Once that 30-day window slams shut, the state has the green light. They can legally contact your bank to freeze your accounts, order your employer to garnish your wages, or seize other property. And they can do it without giving you another warning.

What Assets Can a State Tax Levy Seize?

When that final notice from the state arrives, the first question that probably pops into your head is: what can they actually take? It's a scary thought. A state tax levy gives the government some serious power to seize your assets, but it’s not a blank check.

Knowing what’s vulnerable versus what’s protected is the key to understanding where you truly stand. The state isn't looking to make things complicated.

Their goal is to collect the debt as efficiently as possible, so they go after assets that are easy to access and turn into cash. This is a critical enforcement tool for recovering unpaid property, income, and sales taxes—the very money that keeps state and local governments running.

It’s a serious business, especially when you consider that the lowest-income 20% of Americans can pay an average effective state and local tax rate of about 11.4%, according to the Institute on Taxation and Economic Policy.

Common Targets for Seizure

State tax agencies usually have a predictable playbook. They start with the most liquid assets and only move on to more complex property if the debt isn't settled.

Financial Accounts: This is almost always the first place they look. Your checking accounts, savings accounts, and even certain investment or retirement funds are on the table. The state simply sends a notice to your bank, which is then legally obligated to freeze your funds (up to the amount you owe) and hand them over.

Wages and Income: You might know this as wage garnishment, and it’s a continuous levy. The state orders your employer to slice off a portion of your paycheck and send it directly to them. This doesn't stop until the entire tax debt is paid in full.

Physical Property: This is less common because it’s a bigger headache for the state, but it’s not off-limits. They can seize and sell physical assets like cars, boats, and even real estate. Because of the complicated legal process involved, this is typically a last-resort measure.

What Is Legally Protected From a Levy?

Thankfully, it's not a free-for-all. Both state and federal laws put a hard stop on what tax authorities can take. The point of a levy is to collect a debt, not to push you into total financial ruin. Certain assets and income sources are specifically exempt to make sure you can still cover basic living expenses.

A levy is a powerful tool, but it's not unlimited. Knowing your protections is just as important as knowing your risks. The law provides a safety net to prevent a tax debt from causing complete financial ruin.

These protections aren't always automatic—you might have to step up and prove you’re eligible—but they are your legal right. It’s also crucial to remember that a levy is different from a lien. While a levy seizes your property now, a tax lien is a public claim against your property that messes with your credit and ability to sell.

Key Exemptions to Be Aware Of

While the specific rules and dollar amounts can vary from state to state, some protections are pretty standard across the board:

A Portion of Your Wages: The state can't take your whole paycheck. Laws set a maximum percentage they can garnish, ensuring you’re left with enough money to live on.

Certain Federal Benefits: Money from sources like Social Security, Supplemental Security Income (SSI), and veterans’ benefits is generally shielded from state tax levies by federal law.

Specific Personal Items: Your essential personal belongings—think basic furniture, clothing, and your kids' schoolbooks—are typically exempt up to a certain value.

Tools of the Trade: If you need specific equipment for your job or business, those items are often protected up to a certain value. The state doesn't want to take away your ability to earn a living.

Knowing Your Rights When Facing a Levy

Getting a letter about a state tax levy is enough to make anyone’s stomach drop. It’s stressful, intimidating, and it can feel like you’re powerless against a massive government agency. But I’m here to tell you that’s not the case. You have rights—a specific set of protections designed to ensure you’re treated fairly.

Knowing these rights is your first line of defense. They aren’t just suggestions; they’re legal requirements the state must follow. The system is actually built to give you plenty of chances to sort things out long before they can touch your assets.

Your Right to Proper Notification

First things first: a state can’t just swoop in and seize your property out of the blue. The most basic right you have is the right to be properly informed. Think of it as a mandatory heads-up.

Before they can take any action, you have to receive a series of written warnings, which all lead up to one critical document: a Final Notice of Intent to Levy. This letter officially starts the clock, usually giving you 30 days to respond before the levy kicks in. It has to clearly spell out how much you owe, what they plan to do, and what your options are.

Your Right to Appeal the Levy

Just because the state is threatening a levy doesn't mean it's a done deal. You have the right to challenge their collection action. This is typically done by requesting a formal hearing, often called a Collection Due Process (CDP) hearing or something similar, depending on your state.

This hearing is your chance to make your case in front of an impartial officer. During the appeal, you can:

Dispute the tax bill: Argue that the amount they claim you owe is wrong.

Propose another solution: Suggest a different way to pay, like an installment agreement.

Claim financial hardship: Show that seizing your assets would cause a severe and immediate economic crisis for you and your family.

The best part? Filing an appeal puts an immediate freeze on all collection activity. The state can't touch anything while your case is being reviewed, buying you precious time to work toward a resolution.

Your Right to Professional Representation

You absolutely do not have to go through this alone. You have the right to hire a qualified tax professional—like a tax attorney or an Enrolled Agent—to step in and represent you. When you’re feeling overwhelmed, this can be a total game-changer.

A good representative lives and breathes state tax law. They can handle all the back-and-forth with the tax agency, file the appeal paperwork correctly, and negotiate a deal that actually fits your financial reality.

They often know about solutions you might not even be aware of. For instance, sometimes it’s possible to settle a tax debt for much less than what you originally owed.

Proven Strategies to Resolve a State Tax Levy

Getting hit with a state tax levy feels like a punch to the gut, but it's not a knockout. Think of it as a serious warning, not a final verdict. You have several powerful ways to stop the state from seizing your assets and get back on solid ground.

The absolute worst thing you can do is ignore it. The problem will only escalate. By taking a deep breath and exploring your options, you can find a clear path forward that protects your property and helps you settle your debt for good.

Negotiate an Installment Agreement

For many people, the most direct route to relief is an Installment Agreement. It’s exactly what it sounds like: a structured payment plan. You and the state agree on a manageable monthly payment that you make consistently until the debt is cleared.

This is the perfect option if you just don't have the cash to pay the full balance right now but can handle smaller, regular payments. Once the state approves the agreement, they’ll call off the dogs—releasing active levies like wage garnishments, so long as you keep up your end of the bargain.

Tax debt is a global issue, and governments everywhere rely on being able to collect what’s owed. As a recent OECD report points out, Personal Income Tax can make up as much as 44.0% of total revenue in the U.S., which is why they take enforcement so seriously.

Submit an Offer in Compromise

What if you truly can't afford to pay the full amount, even over time? That's where an Offer in Compromise (OIC) comes in. An OIC lets you formally ask the state to settle your tax debt for less than the total you owe.

This isn't just a casual negotiation. It’s a rigorous application process where the burden is on you to prove that paying the full amount is simply impossible, both now and for the foreseeable future. You'll have to open your books and provide detailed financial records—income, expenses, assets, the whole nine yards.

States typically only consider an OIC in a couple of situations:

Doubt as to Collectibility: You can clearly show that your income and assets aren't enough to cover the debt.

Doubt as to Liability: You have solid evidence proving the amount the state says you owe is actually wrong.

An Offer in Compromise can be a financial lifeline, but don't think it's an easy win. The state scrutinizes every detail. A successful OIC depends entirely on a meticulously prepared application that leaves no doubt about your financial hardship.

Prove an Economic Hardship

Sometimes a levy creates an immediate crisis. If the state’s action is preventing you from covering your family's basic needs, you can request that they release the levy due to economic hardship. This means proving the seizure of your money or property is making it impossible to pay for essentials.

This usually comes down to showing you can't cover critical living expenses like:

Rent or mortgage payments

Utility bills

Groceries

Essential medical treatments

Proving hardship usually gets you temporary relief. It stops the levy, giving you some much-needed breathing room to work out a permanent fix, like an Installment Agreement. Learning about managing tax debt effectively is a great first step toward preventing these situations altogether. And if you’re dealing with a federal issue, our guide on how to stop IRS wage garnishment and protect your income has you covered.

Your Top Questions About State Tax Levies, Answered

When you’re staring down a state tax levy, your mind is probably racing with urgent questions. The stress is real, but getting clear answers is the first step to taking back control. Let's cut through the noise and tackle the most common concerns head-on.

How Quickly Can a State Actually Seize My Bank Account?

Terrifyingly fast. Once that final 30-day notice period is up, the state can act with astonishing speed. A bank levy is an electronic process, meaning they can freeze your funds almost instantly—often on the very same day your bank gets the order.

Once frozen, the bank is legally required to hold your money for a set period, which is typically around 21 days, before they hand it over to the state. This is your do-or-die window. It’s the last chance you have to reach out, negotiate a deal like an installment agreement, and get that levy released before your money is gone for good.

A state tax levy can do a number on your financial health, and that includes your credit. If you're looking for more general info on why your credit score might be dropping, this guide offers some solid insights.

Can They Take My Social Security or Disability Checks?

This is a huge source of anxiety for many, but the short answer is generally no. Federal law throws up a powerful shield around benefits like Social Security, Supplemental Security Income (SSI), and veterans' benefits, protecting them from being snatched by state tax agencies.

If these benefits are direct-deposited, banks are required to automatically identify and protect up to two months' worth of them from any levy.

The process can get messy, though, if you mix these protected benefits with other income in the same account (a practice called "co-mingling"). It’s always smart to double-check your specific state’s laws, as the rules can have slight variations.

How Is a State Levy Different From an IRS Levy?

While they feel the same, the key difference is simply who is coming after the money.

An IRS levy is for unpaid federal taxes (like your federal income tax).

A state tax levy is for unpaid state taxes (like state income, sales, or property tax).

The playbook is pretty similar for both: they send notices, issue demands, and give a final warning. But the specifics—the timelines, appeal rights, and exact amounts of property exempt from seizure—are governed by two totally separate sets of laws. It's also entirely possible to be hit with levies from both the IRS and the state at the same time for different tax debts.

Does Filing for Bankruptcy Stop a State Tax Levy?

Yes, it almost always does. The moment you file for bankruptcy, the court issues something called an "automatic stay." Think of it as a legal stop sign that immediately halts most collection actions against you, including any active or pending state tax levies.

This provides immediate breathing room, stopping wage garnishments and bank freezes right in their tracks. But make no mistake, bankruptcy is a massive financial decision with lasting consequences.

It might not even wipe out the tax debt itself, especially if it's recent. Always talk to a qualified bankruptcy attorney first to figure out if it's truly the right move for your situation.

At Attorney Stephen A Weisberg, we know how crushing tax problems can be. We skip the high-pressure sales pitches and start with a FREE Tax Debt Analysis to see exactly how we can help. If you're dealing with a state tax levy, get the expert guidance you need to find your best path forward.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034