How Far Back Can You Amend Taxes? Your Complete Guide

Think of it like a store's return policy. You bought something, got home, and realized it wasn't right. Most stores give you a window to bring it back for a refund. The IRS operates on a similar principle when you've overpaid your taxes.

Generally, you have three years to go back, amend a tax return, and claim a refund you're owed. This is the single most important deadline to burn into your memory.

Understanding The IRS Three-Year Window For Amendments

While everyone calls it the "three-year rule," the IRS officially knows it as the statute of limitations for a credit or refund. This rule is the foundation of the whole amendment process, defining exactly how far back you can reach to fix a mistake and get your money.

So, when does this three-year clock actually start ticking? The IRS has a very specific "later of" rule to make sure the timeline is fair.

The statute of limitations clock starts on the date that is later:

Three years from the date you filed your original tax return.

Two years from the date you actually paid the tax for that year.

This little detail is a big deal. It’s designed to give you the maximum amount of time possible. For example, let's say you filed your 2021 tax return on April 15, 2022, but couldn't pay what you owed until June 1, 2023. That two-year clock from your payment date would give you a much longer window to amend than the standard three-year rule would.

Key Deadlines at a Glance

For most people, that three-year timeline from the filing date is the one that matters. Here in the United States, taxpayers usually have three years from the date they filed—or the tax due date, if they filed early—to submit an amended return and claim an additional refund.

To make it simple, here’s a quick summary of the standard deadlines for claiming a refund.

Standard IRS Deadlines for Amending a Tax Return

| Scenario | Deadline for Amending |

|---|---|

| Claiming a Refund | Whichever is LATER: 3 years from filing date OR 2 years from tax payment date. |

| Filing Early | The 3-year clock starts on the official tax deadline (e.g., April 15), not your early filing date. |

| Filing on Extension | The 3-year clock starts from the date you actually file the return, not the extension deadline. |

Getting a handle on these timelines is your first and most critical step. And when you're dealing with a government agency like the IRS, hearing from people who've been on the inside can be incredibly helpful. You can find some valuable insights from an IRS professional that shed light on how things work from their perspective.

Why Tax Amendment Deadlines Even Exist

It’s easy to think the deadlines for amending a tax return are just arbitrary rules. In reality, they're the product of more than a century of experience, designed to strike a crucial balance in our tax system. These rules, formally known as statutes of limitations, are all about fairness and finality.

On one side, they give you a fair shot to go back and fix a genuine mistake or claim a refund you missed. On the other, they give the government a point where it can finally close the books on a tax year.

Think of it this way: without a cut-off date, the financial records for both taxpayers and the government would be open-ended forever. A simple clerical error from decades ago could pop up at any time, creating an impossible mess of disputes and uncertainty.

A Century of Fine-Tuning

The whole concept of a federal income tax as we know it kicked off with the 16th Amendment back in 1913. Fun fact: the original tax deadline wasn't April 15th. It started as March 1, then got pushed to March 15 in 1918. It wasn't until 1954 that April 15 became the familiar deadline we have today.

This history lesson isn't just trivia; it shows how the system has been tweaked over time to become more efficient while still trying to accommodate taxpayers' needs. This evolution is what led to the clear, predictable windows for amendments that we have now.

Ultimately, all these deadlines—from the standard three-year rule to all its exceptions—are governed by specific provisions of tax law. Understanding this isn't just about knowing the rules. It's about appreciating that there's a structure in place designed to prevent a never-ending cycle of revisions for both you and the IRS, making the entire process manageable.

Important Exceptions That Extend Your Amendment Deadline

While the three-year rule is the gold standard, it's definitely not the final word. The tax code is surprisingly flexible in certain situations, offering special passes that can dramatically extend how far back you can go to amend your taxes.

Knowing these exceptions is a game-changer. They can unlock refunds you might have assumed were lost to time. Let's dig into the most common scenarios that give you more time to file that Form 1040-X.

Bad Debts and Worthless Securities

Ever invested in a stock that completely tanked? Or maybe you loaned money to a business that went under? If so, the IRS gives you some extra breathing room to handle the financial fallout from these specific kinds of losses.

Instead of the usual three-year window, you get a much more generous seven-year period to amend your return for:

Worthless Securities: This applies when a stock, bond, or another security you own becomes completely and utterly worthless. The loss is treated as if it happened on the very last day of that tax year.

Bad Debts: This is for when you can prove a legitimate loan you made (not a gift) has become uncollectible.

Why the extra time? Because figuring out the exact moment a stock officially becomes worthless or a debt is truly uncollectible can be a messy, drawn-out process. This seven-year window gives you the runway you need to get your documentation in order and properly claim the deduction you're entitled to.

Foreign Tax Credits

If you've paid income taxes to another country, you can often claim a credit for it on your U.S. return to avoid double taxation. For this, the timeline is even longer. The IRS allows a ten-year window to file an amended return and claim a foreign tax credit. This is one of the longest extensions you’ll find.

The ten-year rule is a practical acknowledgment that dealing with international tax laws can be complicated. Delays in getting final tax documents from foreign governments are common, and this extension provides the necessary leeway.

Real-World Example: Let's say you worked in Germany back in 2017 and paid German income taxes. It's now 2024, and you just realized you never claimed a credit for those taxes on your 2017 U.S. return. Thanks to the ten-year rule, you still have until 2028 to file a Form 1040-X and get that credit.

Significant Underreporting of Income

Now for an exception that works in the IRS's favor. If you substantially understate your income—we're talking by more than 25% of the gross income you reported on your original return—the IRS gets more time to act.

In this scenario, the statute of limitations for the IRS to come back and assess more tax is extended from three years to a full six years. While this isn't an extension for you to claim a refund, it’s a critical piece of the puzzle.

Knowing this underscores just how far back your tax life can be examined. Of course, not filing at all creates even bigger problems, which is why tackling unfiled returns head-on is so crucial.

To help visualize how these deadlines stack up, here's a quick comparison of the standard amendment deadline against some of the major exceptions.

Extended Deadlines for Amending a Return

| Reason for Amendment | Time Limit to File | Example Scenario |

|---|---|---|

| Standard Amendment | 3 years from the date you filed your original return, or 2 years from the date you paid the tax (whichever is later). | You filed your 2021 tax return in April 2022 and later discovered a missed deduction. You have until April 2025 to amend. |

| Bad Debt or Worthless Security | 7 years from the due date of the return for the year the loss occurred. | A stock you owned became worthless in 2019. You have until 2027 to amend your 2019 return to claim the loss. |

| Foreign Tax Credit | 10 years from the due date of the return for the year the foreign taxes were paid or accrued. | You paid taxes to the UK in 2018 but forgot to claim the credit. You have until 2029 to amend and claim it. |

| IRS Assessment (Substantial Understatement) | 6 years for the IRS to assess additional tax if you underreported income by more than 25%. | You filed your 2020 return but omitted a large consulting gig. The IRS has until 2027 to audit and assess the tax. |

As you can see, the reason for the amendment makes all the difference. It's not a one-size-fits-all timeline.

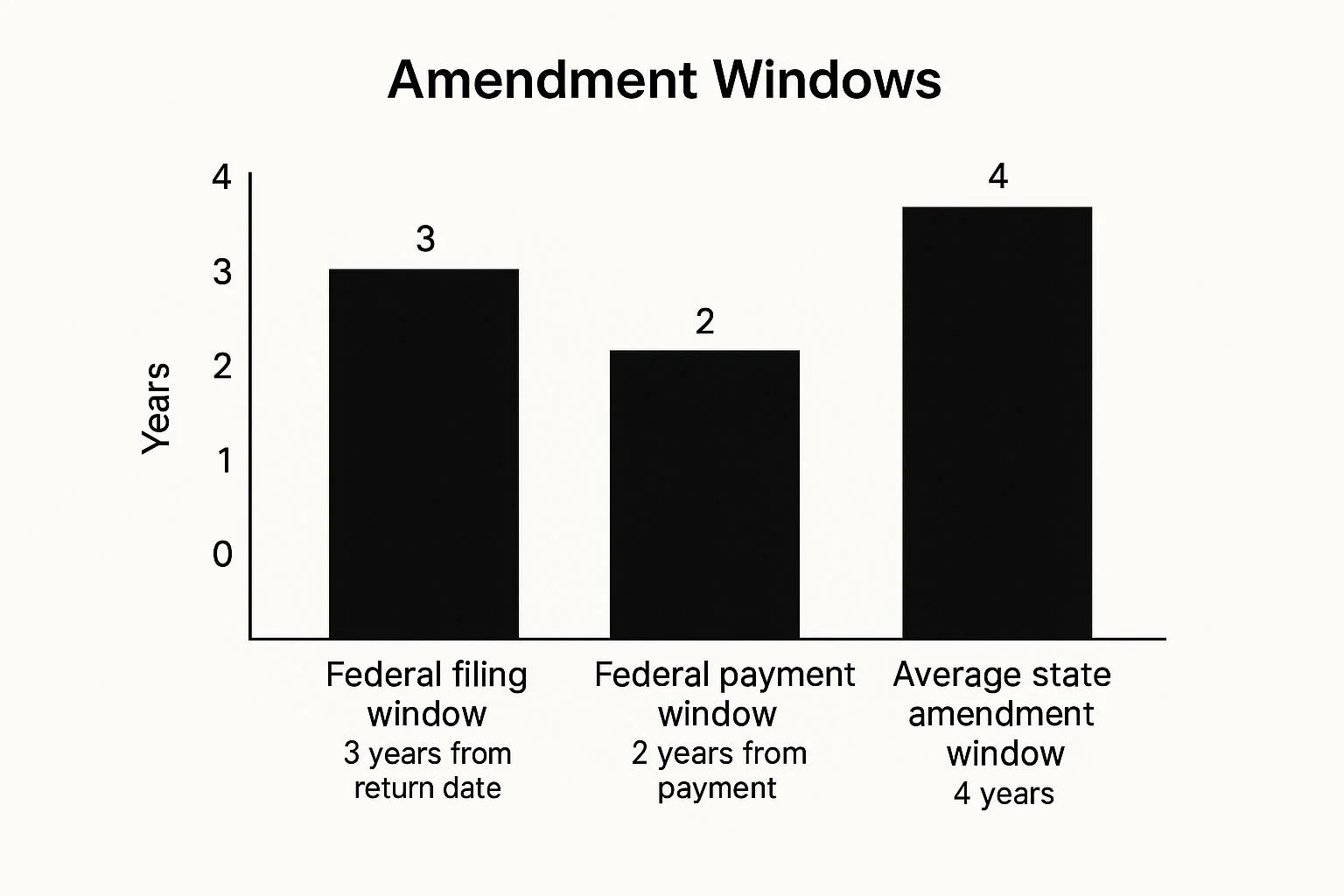

The infographic below shows how the federal windows compare to the average state timeline, adding another layer to consider.

As the chart highlights, the federal timelines for filing for a refund and for the IRS to assess tax are distinct, and your state’s rules can introduce a whole different set of deadlines.

When the Amendment Clock Never Stops Ticking

While most tax deadlines have a clear finish line, a few serious situations completely erase it. In these specific cases, the statute of limitations clock doesn't just get a little more time—it never even starts. This gives the IRS an unlimited window to assess taxes, penalties, and interest.

Think of the usual three-year rule as a timer the IRS sets the moment you file. But for a couple of major no-nos, that timer is effectively broken. It stays stuck at zero, leaving your tax year open to review forever. This permanent lookback period kicks in for two scenarios the IRS takes very seriously.

The statute of limitations never expires if a taxpayer:

Fails to file a tax return at all.

Files a fraudulent tax return.

If you fall into either of these categories, the question of "how far back can you amend?" becomes moot. The IRS can go back as far as it needs to because there's simply no expiration date on its authority.

The Consequences of a Frozen Clock

When the clock is frozen, the financial fallout can be devastating. The IRS can come after back taxes for any number of years, tacking on hefty penalties for failure to file, failure to pay, and accuracy or fraud.

And all the while, interest is compounding daily on that growing balance, quickly turning what might have been a small tax issue into an insurmountable one.

This isn't a problem you can ignore, hoping it will just fade away. It won't. It will only get bigger and more tangled over time. That indefinite timeline means the IRS could launch an audit or start collection actions five, ten, or even twenty years down the road.

Finding a Path Back to Compliance

If you're in this boat, whether from years of unfiled returns or past mistakes you regret, the key is to be proactive. The longer you wait, the worse the financial damage becomes. Thankfully, the IRS has established ways for people to get back on the right side of the law.

One of the best options is the IRS Voluntary Disclosure Practice. This program is a lifeline for taxpayers who know they willfully broke the rules. It allows you to come forward, get compliant, and potentially sidestep criminal prosecution. It creates a clear path to:

File all of your old, missing tax returns.

Pay the back taxes and interest you owe.

Work toward a resolution for the civil penalties.

Trust me, coming forward on your own terms is always seen more favorably than getting caught. It shows you're making a good-faith effort to fix things, which can dramatically reduce the severe financial and legal pain that comes with fraud or long-term non-filing.

Tackling these issues head-on, ideally with professional help, is the only way to get that clock ticking again and finally put the matter to rest.

Navigating State Tax Amendment Rules

Getting your federal return corrected is a big step, but don't pop the champagne just yet. It's often only half the battle. A common mistake I see taxpayers make is filing their federal Form 1040-X and thinking they're completely in the clear. The reality is, your state’s tax agency has its own rulebook, and they definitely want to hear about any changes you’ve made.

Think of it this way: your federal and state returns are two sides of the same coin. A change to one almost always affects the other. If you ignore the state side, you're setting yourself up for a nasty surprise down the road in the form of unexpected notices, penalties, and interest charges.

Here’s the single most important thing to remember: state amendment rules are not universal. Every state plays by its own rules, and it’s a huge mistake to assume their deadlines mirror the IRS’s three-year window.

State Timelines Can Vary Significantly

While some states do happen to follow the federal three-year rule, many don't. I've worked with clients in states that give you four years or even longer to file an amended return. This can be a lifesaver if you've discovered a mistake but the federal deadline has already passed—you might still be able to get a refund from your state.

On the flip side, some state deadlines are much shorter, demanding quicker action. This is especially true when your federal amendment means you owe more tax. States often require you to notify them of a federal change within a surprisingly tight window, sometimes just 60 to 90 days.

If the changes on your federal return affect your state tax bill, filing a state amendment isn't optional. The clock on state penalties and interest starts ticking from the original due date of the return, not from the day you got around to fixing your federal paperwork.

Where to Find Your State’s Rules

So, how do you find out the exact rules for your state? Your first and best stop should always be the official website for your state's department of revenue or taxation.

Once you’re on the site, head to the section for individual income tax and look for keywords like:

"Amended return"

"Statute of limitations"

"Claim for refund"

These pages will tell you everything you need to know, including which specific forms to use (it's almost never the federal 1040-X) and the deadlines you have to meet. Never, ever assume the federal rules apply. Taking a few minutes to verify your state’s specific requirements is the only way to keep your tax record clean and claim every dollar you're rightfully owed.

A Step-by-Step Guide to Filing Your Amended Return

Alright, so you understand the deadlines and why they're so important. Now for the practical part: actually filing the amendment. It sounds daunting, but it really isn't. The whole process revolves around a single, crucial document: Form 1040-X, Amended U.S. Individual Income Tax Return.

Think of it like correcting an exam you already turned in. You got your grade back (your original tax return), but then realized you missed a question or answered something incorrectly (a missed deduction or an extra W-2). Form 1040-X is how you submit your corrections to get the right final score.

Gathering Your Essential Documents

Before you even glance at the form, get organized. Trust me, having all your paperwork lined up from the start makes everything go much smoother. You'll avoid the frustration of stopping and starting to hunt down a missing document.

Here's what you need to pull together:

Your Original Tax Return: You can't fix what you can't see. Have a copy of the exact return you're amending right in front of you.

New or Corrected Documents: This is the new information triggering the amendment. It could be a corrected W-2, a 1099 that came in late, or any other form that changes your numbers.

Proof for New Deductions or Credits: Claiming a new deduction? Make sure you have the receipts, bank statements, or other records that prove you're entitled to it.

Once you have these items gathered, you're in a great position to tackle the form itself. If you're ready to jump in, you can find a detailed guide on how to amend a tax return with comprehensive, step-by-step instructions.

Completing and Submitting Form 1040-X

Form 1040-X is pretty straightforward. It’s set up with three main columns: Column A is for the figures from your original return, Column C is for your new, corrected figures, and Column B simply shows the difference between the two. The form guides you through the math to figure out if you're due a refund or now owe more tax.

The most critical section, however, is Part III: the "Explanation of Changes." This is where you talk directly to the IRS.

Don't be vague here. Be clear and specific. Instead of saying "forgot a deduction," write something like: "Adding a $500 deduction for charitable contributions. A copy of the receipt from XYZ Charity is attached."

After filling out the form, you must attach copies of any new or revised documents that back up your changes—like that corrected W-2 or the charity receipt. Here’s a pro tip: if you need to amend returns for multiple years, you have to file a separate Form 1040-X for each tax year. Never try to bundle them together. You can learn more about the nuances of this process in our deep dive on how to amend a tax return.

Finally, once you've mailed or e-filed your amended return, you can keep tabs on it with the IRS’s "Where's My Amended Return?" tool online. Just be prepared to wait—it can take up to 20 weeks for the IRS to process it, so patience is a must.

Frequently Asked Questions About Amending Taxes

Even after laying out the rules, I know specific questions always come up. Let's tackle some of the most common things taxpayers wonder about when they realize they might need to amend a return.

Can I E-File an Amended Return?

Yes, you can—for most recent years, anyway. For tax years 2019 and later, you can now e-file your Form 1040-X through most approved tax software. This is a huge improvement over the old days of having to mail everything in.

E-filing is much faster, you get an instant confirmation that the IRS received it, and you can track its status online. For older returns, though, you’re still stuck with the old-school method: print and mail.

What if My Amendment Shows I Owe More Tax?

This is a big one. If your amended return shows you owe more tax, you need to pay that balance as soon as you file your Form 1040-X. Don't wait.

The IRS calculates interest on what you owe from the original tax deadline, not from the date you amend. Paying right away is the only way to stop that interest clock and avoid potential penalties. If the new tax bill is more than you can handle, it might be time to look into professional tax debt solutions to get things under control.

Key Takeaway: Amending a return does not automatically trigger an audit. However, it does guarantee that an IRS employee will review that specific tax year again.

A simple, straightforward change—like adding a W-2 you forgot—is very unlikely to cause a stir. But if you’re making complex changes or claiming a huge, unexpected refund, you can bet it will get a closer look. The best way to keep things smooth is to make sure every change is clearly explained and you have all the paperwork to back it up.

At Attorney Stephen A Weisberg, we understand that navigating IRS rules can be overwhelming. If you're facing tax debt or complex compliance issues, we can help you find the best possible outcome. Contact us today for a free, no-obligation tax debt analysis to understand your options.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034