How to Settle Tax Debt Your Guide to IRS Relief

That thick envelope from the IRS sitting on your counter can feel paralyzing. But it’s not a final verdict—it’s a starting point. Tackling tax debt is all about understanding exactly what you’re up against, mapping out a strategy, and finding the right tool for the job, whether that’s an Offer in Compromise or a simple Installment Agreement. This is how you take back control.

Facing Your Tax Debt: A Realistic Path Forward

When you get that official notice, your first instinct might be to panic. Don't. Instead, see it as a call to action. Your first move is to get a crystal-clear picture of the situation. You need to find out the exact amount you owe, which includes the original tax bill plus all the penalties and interest that have piled up since.

The easiest way to do this is by creating an online account on IRS.gov or by requesting your official tax transcripts directly from them. This isn't about staring down a scary number; it’s about gathering the intelligence you need to build a solid game plan.

Understanding Your Primary Options

Once you know the total liability, you can start weighing the different relief programs the IRS offers. Each one is built for a specific financial scenario, so picking the right one is absolutely critical to getting it resolved.

To give you a better idea of what’s available, here’s a quick summary of the main programs people use to get back on track with the IRS.

Your Main IRS Debt Relief Options at a Glance

| Relief Program | Best Suited For Taxpayers Who... | Primary Outcome |

|---|---|---|

| Offer in Compromise (OIC) | Are facing severe financial hardship and can't pay the full amount. | Settle the tax debt for less than the total amount owed. |

| Installment Agreement (IA) | Have the ability to pay the full debt but need more time to do so. | Pay off the full tax liability through manageable monthly payments. |

| Currently Not Collectible (CNC) | Cannot afford basic living expenses, let alone a tax payment. | Temporarily pauses IRS collection efforts until your financial situation improves. |

Each of these options serves a different purpose. The key is to honestly assess your financial reality and see which program aligns with what you can realistically handle right now.

The absolute worst thing you can do is ignore the notices. The problem won’t just go away. It will get bigger and more expensive as penalties and interest keep adding up. The only way out is to be proactive and figure out your next move.

You Are Not Alone in This Process

If you’re staring down a tax bill, know that you’re in good company. This is a surprisingly common problem. In fact, by 2020, Americans owed the IRS something in the neighborhood of $128 billion in back taxes.

That number alone shows just how many people find themselves in this exact spot. You can dig into more trends shaping the tax relief world over at UCFS.net.

Trying to figure all this out on your own can feel overwhelming. This is often where experienced professional tax firms come in.

A seasoned pro can help you make sense of your situation, identify the best path forward, and walk you through the entire process. They replace that feeling of dread with a structured, manageable plan. And believe me, with the right help, this situation is absolutely manageable.

Qualifying for an Offer in Compromise

An Offer in Compromise, or OIC, is often seen as the ultimate solution for tax debt. It's the one IRS program that lets you settle your tax bill for less than what you originally owed.

While it sounds incredible, let's be clear: the IRS doesn't just give these away. Qualifying is a tough, detailed process, and frankly, most people who apply don't get approved.

The IRS created the OIC program as a final option for people in genuine financial trouble. Before they'll even look at your offer, you have to convince them that taking a smaller amount now is the best they can hope for. Your entire case must be built on one of three specific grounds.

The Three Paths to an OIC

The IRS lays out three official reasons why they might accept an Offer in Compromise. You have to prove, with hard evidence, that you fit squarely into one of these boxes.

Doubt as to Collectibility: This is the most common reason for an OIC. You’re essentially showing the IRS your full financial picture and proving there's serious doubt you could ever pay the full amount owed. It's an argument based on your inability to pay.

Doubt as to Liability: This path is far less common. Here, the argument isn't about your finances; it's about the tax debt itself. You're claiming the IRS made a mistake, the tax was assessed incorrectly, and you don't actually owe it in the first place.

Effective Tax Administration (ETA): This is a rare, special circumstance. Under ETA, you technically have the assets or income to pay the debt, but doing so would cause an exceptional, unfair, or inequitable economic hardship. Think of someone who would have to sell their home to pay the tax, leaving them and their disabled dependent with nowhere to live.

For the vast majority of people trying to settle tax debt, the conversation starts and ends with Doubt as to Collectibility. This means putting your entire financial life under a microscope.

Calculating Your Reasonable Collection Potential

The entire foundation of a "Doubt as to Collectibility" offer rests on a number the IRS calls your Reasonable Collection Potential (RCP). This figure is the absolute minimum the IRS will accept to settle your debt. It's not a guess; it's a specific calculation based on your assets, income, and allowable expenses.

The formula is pretty direct: (Net Equity in Assets) + (Future Remaining Income) = Your RCP.

Net Equity in Assets: This is the value of your assets (home, cars, bank accounts, retirement funds) minus any loans against them.

Future Remaining Income: This is your gross monthly income minus what the IRS allows for monthly living expenses, which is then multiplied by either 12 or 24 months into the future.

The IRS will comb through every line item on your Form 433-A (for individuals) or 433-B (for businesses). They use strict national and local standards for what you're allowed to spend on housing, food, and transportation. If you claim an expense that's higher than their standard, you better have a rock-solid reason and the documents to back it up.

Key Takeaway: The IRS doesn’t care about your personal budget or desired lifestyle. They work off their own standardized, allowable expenses. Your offer has to be more than your calculated RCP, or it’s dead on arrival.

Building a Winning Case

Submitting an OIC is about more than just filling out forms. It’s about building a compelling, fact-based narrative of your financial hardship.

The main document is Form 656, Offer in Compromise, but the real work is in the detailed financial statements on Form 433 that support it.

Let's look at a real-world example. A self-employed web developer loses her biggest client due to a merger and her income is cut by 70%. She burns through her savings to stay afloat.

She has a small 401(k) and a five-year-old car she’s still making payments on. In this scenario, her RCP is likely very low, making her a potentially strong candidate for an OIC based on Doubt as to Collectibility.

Her application would need to meticulously document the sudden income loss, show the minimal equity in her assets, and present living expenses that fall within IRS guidelines.

This need for effective settlement mechanisms is a global issue. As of 2025, global public debt has soared past 95 percent of gross domestic product (GDP). This fiscal pressure on governments worldwide makes programs like the OIC essential for both collecting revenue and providing a safety valve for citizens in financial distress.

Because of the high stakes and sheer complexity, it's critical to understand the entire OIC landscape before you start. If you're seriously thinking about this route, I recommend reading our complete guide to IRS Offer in Compromise tax debt settlement to get a better handle on every single step.

How to Set Up an IRS Installment Agreement

So, an Offer in Compromise isn't in the cards for your financial situation. That’s perfectly fine. For most people I work with, the most sensible and common way forward is an IRS Installment Agreement (IA). Think of it as a formal payment plan that lets you chip away at your full tax bill over time with monthly payments you can actually handle.

Unlike an OIC, where you have to prove serious economic hardship, an installment agreement is for people who can pay what they owe but need more time to do it without wrecking their budget. It's a structured, straightforward way to get right with the IRS, showing them you’re serious about paying, just on a more realistic schedule.

Different Agreements for Different Situations

The IRS doesn't have a one-size-fits-all payment plan. They offer a few different flavors of Installment Agreements, each designed for specific debt levels and financial circumstances. Knowing which one you’re likely to qualify for from the get-go can save you a lot of headaches.

Here’s a quick rundown:

Guaranteed Installment Agreement: If your total tax bill is $10,000 or less, you’re pretty much a shoo-in for this. The main condition is that you’ve filed and paid on time for the last five years.

Streamlined Installment Agreement: This is the one I see most often. It’s for taxpayers who owe a combined total under $50,000 (that includes the tax, penalties, and interest). The best part? You generally don’t have to submit a mountain of financial paperwork, which makes the approval process much quicker.

Partial Payment Installment Agreement (PPIA): This is a more complex beast. It’s for folks who can afford to make monthly payments but won’t be able to pay off the entire debt before the 10-year collection clock (the CSED) runs out. These are tricky to negotiate and almost always require professional help.

For the vast majority of people, the Streamlined IA is the path of least resistance to resolving their tax debt.

A Word of Caution: As you start this process, your phone might start ringing with calls from "tax debt settlement services." Be very careful. These companies often use high-pressure sales tactics and make promises they can't deliver on. The safest route is always going directly through the IRS website or working with a tax professional you trust.

Applying for Your Payment Plan

Getting an Installment Agreement set up is more accessible than it’s ever been. For many people, you can get the whole thing done online in a few minutes and walk away with immediate peace of mind.

Your first stop should be the IRS's Online Payment Agreement (OPA) tool. If you owe less than $50,000 and qualify for the Streamlined agreement, you can often get instant approval without ever sitting on hold. You’ll just need some basic personal info and details from your last tax return to verify who you are.

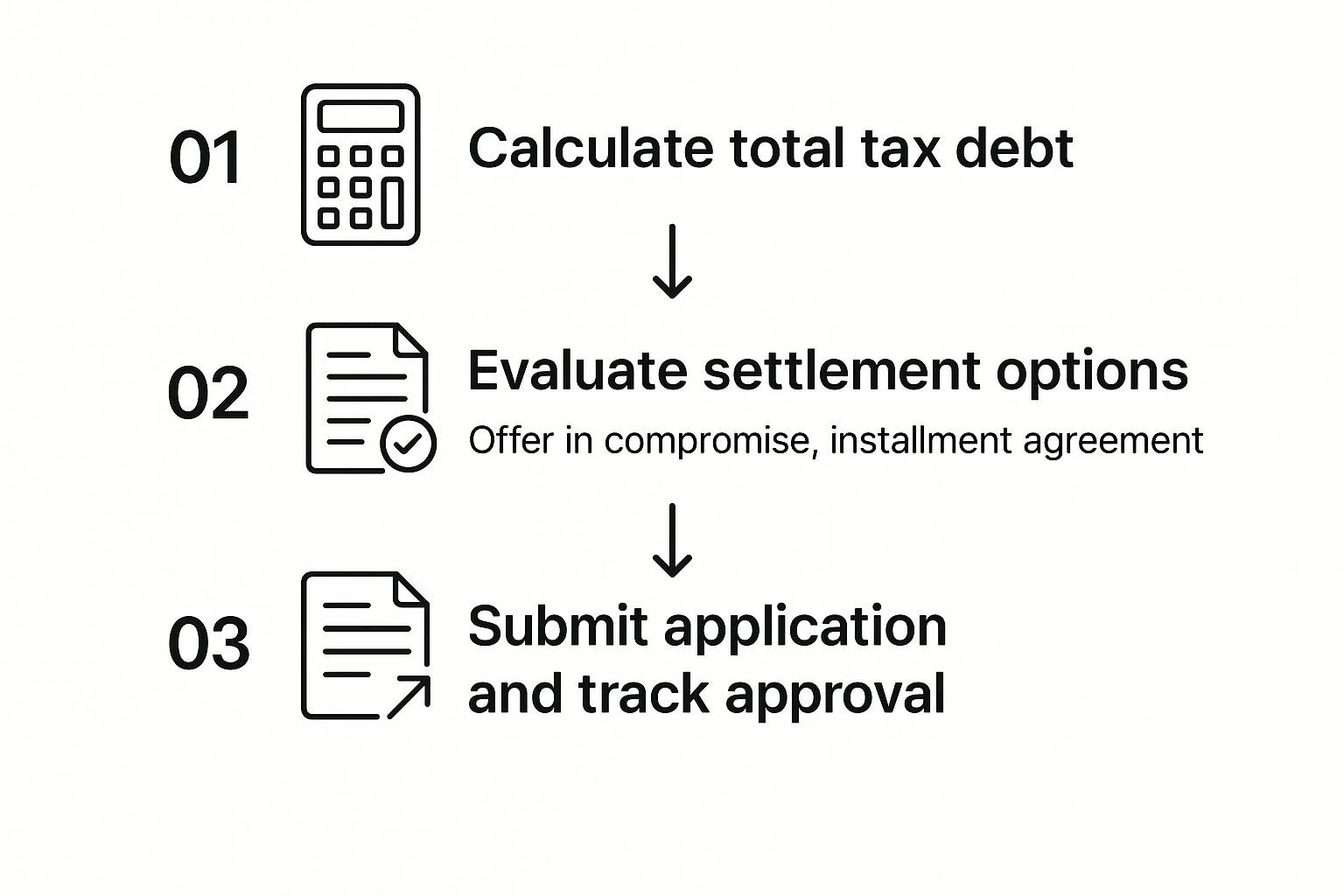

This visual guide shows the general flow for tackling tax debt, from figuring out your options to getting your application in.

As you can see, that middle step—evaluating your options—is crucial. It's where you confirm whether an Installment Agreement is truly the best move for you.

If you’d rather handle things with pen and paper, or if your case is a bit more complicated, you can mail in your request. To formally ask for an installment agreement, you'll need to fill out and send in Form 9465, Installment Agreement Request.

Negotiating a Payment You Can Afford

But what happens if the online tool spits out a monthly payment amount that still makes you break out in a cold sweat? That's when we have to negotiate. If you simply can't afford the IRS's standard calculation (your total balance divided by 72 months), you have to prove it.

This means you’ll need to submit a Collection Information Statement (Form 433-F). This form is essentially a detailed financial snapshot of your monthly income and your allowable living expenses.

The whole point is to show the IRS exactly what you have left over—your disposable income—after you’ve paid for essentials like housing, food, and car payments.

Your proposed payment needs to be grounded in this number. A meticulously prepared Form 433-F is your single best tool for convincing an IRS agent to approve a lower monthly payment that you can actually stick with long-term.

If you want to dive deeper into the nitty-gritty of these negotiations, our guide on how to negotiate IRS debt lays out more specific strategies. Getting a payment plan you can live with is a massive step toward putting this tax debt behind you for good.

Exploring Other Vital Relief Programs

Offers in Compromise and Installment Agreements tend to grab the spotlight, but they're not the only plays in the book for tackling tax debt. Sometimes, a different angle of attack is exactly what you need. Two of the most powerful—and often overlooked—programs are Penalty Abatement and Currently Not Collectible status.

Think of these as specialized tools. They can provide a critical lifeline by targeting specific parts of your tax problem, giving you the breathing room you need to get back on solid financial ground. Knowing how and when to use them is a cornerstone of any good tax resolution strategy.

Wiping Out Penalties with an Abatement

The IRS loves to tack on penalties. Late filing, late payment, accuracy issues... they add up fast. In some cases, penalties can balloon into a huge chunk of your total tax bill. A Penalty Abatement is your formal request to the IRS to wipe those penalties off your account.

But you can't just ask nicely. To get penalties removed, you typically have to show you had "reasonable cause" for failing to file or pay on time. This isn't about having a good excuse; it's about proving a legitimate, often unavoidable, life event got in the way of you exercising what the IRS calls "ordinary business care and prudence."

So, what counts as reasonable cause?

A debilitating illness or the death of someone in your immediate family.

Your home, business, or records being destroyed in a disaster like a fire or flood.

You got bad advice from a competent tax professional and you reasonably relied on it.

Requesting an abatement usually means writing a clear, persuasive letter to the IRS. You need to explain what happened, include specific dates, and back it all up with documentation. For instance, if a medical crisis was the problem, you'd want to include copies of relevant medical records or a letter from your doctor. Your goal is to paint a clear picture of why you couldn't comply.

Expert Tip: Don't forget about the IRS "First-Time Abate" waiver. If you have a clean tax record for the prior three years, you can often get penalties waived without having to prove reasonable cause. All it takes is asking for it, and a simple phone call can literally save you thousands.

Hitting Pause on Collections with CNC Status

What happens when your finances are so tight you can't cover basic living expenses, much less a monthly tax payment? That's where Currently Not Collectible (CNC) status can be a lifesaver. It’s not a permanent fix, but it acts like a temporary pause button on all IRS collection efforts.

If the IRS agrees that you truly cannot afford to pay, they’ll put your account into CNC status. The threatening letters stop. The collection calls cease. They won’t levy your wages or bank accounts. It’s a formal recognition of extreme financial hardship, designed to give you space to recover.

To get there, you have to prove it. This involves submitting a detailed financial statement, like Form 433-F or 433-A, that shows your monthly income is less than or equal to your allowable living expenses based on the IRS's own standards.

But there are two critical things to remember about CNC:

This is not forgiveness. Your tax debt doesn't disappear.

Interest and penalties keep adding up. The total amount you owe will continue to grow while you're in CNC.

The IRS will check in on you periodically to see if your financial situation has improved. Once you're able to make payments again, they'll take you out of CNC status and work with you on a payment arrangement.

These individual financial struggles mirror larger economic trends. On a global scale, emerging economies are staring down a massive debt refinancing crisis, with over $4.5 trillion in bond debt set to mature between 2024 and 2026. This immense pressure on national finances shows just how vital effective debt and tax settlement frameworks are for stability—a principle that holds true for both countries and individuals.

Digging into these programs can help you find the best path forward for your specific situation. For a deeper dive into all your options, take a look at our smart guide to tax relief success for more expert insights.

Critical Mistakes to Avoid When Settling Tax Debt

When it comes to settling tax debt, knowing what not to do is just as important as knowing what to do. The path to resolving your tax issues is full of traps that can easily trip you up, leading to more stress and a bigger bill from the IRS. Trust me, I've seen it happen time and again.

The biggest mistake, hands down, is ignoring the problem. Shoving those official-looking IRS letters in a drawer and hoping they’ll go away is a recipe for disaster. Those notices aren't suggestions; they’re the start of a ticking clock.

Crucial Insight: An ignored IRS notice is a direct trigger for more aggressive collection actions. This is how small tax problems spiral into major financial crises involving liens on your property and levies on your bank accounts or wages.

Ignoring the issue allows penalties and interest to compound daily, making a manageable problem much more expensive. Simply picking up the phone to understand your situation can stop the bleeding and prevent the IRS from escalating things.

Missing Key Deadlines

The IRS runs on a very strict schedule. Every notice they send has a firm deadline, and missing it can slam the door on your best resolution options.

Think about the Collection Due Process (CDP) notice. You typically have just 30 days from the date on that letter to request a hearing to appeal a lien or a proposed levy. If you miss that window, you lose your right to appeal in U.S. Tax Court. It's a hard stop, not a friendly reminder, and it strips you of significant negotiating power.

Submitting Inaccurate or Incomplete Information

When you apply for a resolution like an Offer in Compromise or an Installment Agreement, the financial information you provide on Form 433 must be bulletproof. The IRS will go over it with a fine-tooth comb.

Understating Your Income: Don't even think about it. Hiding income is an express lane to getting your request denied and can easily spark a tax fraud investigation.

Overstating Your Expenses: The IRS has national and local standards for what living expenses should be. Claiming you spend $900 a month on groceries when the standard for your household is $500 will raise immediate red flags unless you have ironclad proof of a special circumstance.

Forgetting Assets: "Forgetting" to list that old savings account or a piece of property isn't an oversight—it's a material omission that will instantly kill your deal.

Your financial disclosure has to be a completely honest snapshot of your life. Any little discrepancy gives the IRS an easy excuse to say no. Remember, these settlement agreements are legal documents. A huge mistake is not carefully reviewing what you're signing; getting familiar with some basics of contract review for non-lawyers can be a real lifesaver here.

Falling for Tax Relief Scams

When you’re under pressure and feeling desperate, a "quick fix" can sound too good to be true. It usually is. The tax relief industry is unfortunately rife with predatory companies looking to take advantage of your situation.

Be very skeptical of anyone who guarantees they can settle your debt for "pennies on the dollar" before they've even seen your financials. These outfits often demand huge upfront fees and then do little to nothing.

A legitimate professional—a CPA, Enrolled Agent, or Tax Attorney—will never make those kinds of promises. They'll start by thoroughly analyzing your situation to see if and how they can help. They provide a realistic assessment and guide you through the established IRS procedures, which is the only real path to resolving your tax debt for good.

Your Questions on Settling Tax Debt Answered

Diving into the world of tax debt brings up a ton of questions. It’s completely normal. The path to getting things squared away is paved with specific rules, timelines, and outcomes that can feel pretty overwhelming at first. Getting clear, honest answers is the first step toward feeling confident and making the right call for your future.

Let’s tackle some of the most common questions that pop up when people are ready to finally face their IRS issues head-on.

How Long Does It Take to Settle Tax Debt?

This is probably the number one question I get, and the honest answer is: it depends entirely on which path you take. There’s no single timeline, because each resolution program moves at its own speed.

Some solutions are surprisingly quick. A straightforward IRS Installment Agreement, for instance, can be set up incredibly fast. If you qualify for a Streamlined Agreement and use the IRS’s online tool, you could have an approved payment plan locked in and ready to go in under 30 minutes.

On the other hand, an Offer in Compromise (OIC) is a marathon, not a sprint. From the moment you mail that application, you should brace yourself for a six to 12-month wait, and sometimes even longer if your financial picture is particularly complicated. The IRS has to meticulously vet every single detail, and that investigation simply takes time.

Similarly, asking for Penalty Abatement usually takes the IRS a few months to review and send back a decision. The most important thing you can do during any of these waiting periods is stay current. Keep filing your new returns and making any required estimated payments.

Can Tax Debt Be Forgiven After 10 Years?

Yes, technically it can be, but it's not as simple as just letting the calendar run out. The IRS generally has a 10-year statute of limitations to collect a tax debt, which includes the tax, penalties, and interest. This deadline is called the Collection Statute Expiration Date (CSED), and it starts from the date the tax was officially assessed. Once that date passes, the IRS is legally barred from collecting.

Here’s the catch: certain actions you take can "toll" or pause that 10-year clock, effectively extending the collection period.

These actions include things like:

Filing an Offer in Compromise

Requesting a Collection Due Process (CDP) Hearing

Filing for bankruptcy

Living outside the U.S. for a significant time

Because these events hit the pause button, it’s actually quite rare for a tax debt to simply expire on its own. Think of it less as a passive waiting game and more as a legal deadline that the IRS actively manages.

What Happens If My Offer in Compromise Is Rejected?

Getting an OIC rejection letter can feel like a punch to the gut, but it is not the end of the road. When the IRS denies your offer, you have 30 days from the date on that letter to file an appeal with the IRS Office of Appeals.

This appeal is your formal chance to argue that the initial decision was wrong. You can bring in new information, clear up any misunderstandings from the first go-around, or better explain why your circumstances truly warrant a settlement. A rejection is a signal to rethink your strategy, not to give up.

If an appeal doesn't work out or isn't the right move, you can immediately pivot to another resolution. This is the perfect time to get an Installment Agreement set up, maybe even a Partial Payment plan, or to see if you now qualify for Currently Not Collectible status.

Should I Hire a Professional to Settle My Tax Debt?

Whether you need a pro really comes down to how complex your situation is. For a simple case—like setting up a Guaranteed Installment Agreement for a small debt—you can probably handle it yourself right on the IRS website. In fact, you can play around with the numbers and see what your payments might be with a good IRS Installment Agreement calculator to get a feel for your options.

However, for the more tangled and serious issues, professional help is invaluable. You should strongly consider hiring an expert if you're:

Dealing with a large tax bill (generally over $50,000)

Burdened with multiple years of unfiled tax returns

Trying to get an Offer in Compromise approved

Fighting against aggressive collection tactics like a wage levy or bank garnishment

A credentialed tax professional—like a Tax Attorney, CPA, or Enrolled Agent—lives and breathes this stuff. They navigate the IRS maze every single day.

They know how to frame your case for the best possible result and can shield you from making expensive mistakes. Just be wary of any company that guarantees a specific outcome or pressures you for huge upfront fees.

At Attorney Stephen A Weisberg, we believe in a transparent and honest approach. Instead of making unrealistic promises, we start with a FREE Tax Debt Analysis to determine exactly how we can help you achieve the best possible outcome with the IRS.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034