IRS Audit Statute of Limitations Your Guide

One of the most common questions I hear is, "How long do I have to worry about the IRS auditing me?" It's a valid concern, and thankfully, there's a clear answer: the IRS audit statute of limitations.

For most people who file their taxes honestly and on time, this crucial window is three years. Think of it as a clock that starts ticking either on the date you file your return or the tax deadline, whichever is later.

Once that clock runs out, the IRS can no longer come knocking to assess more tax for that year. It's a fundamental protection that gives you finality and peace of mind.

What Is the IRS Audit Clock?

Imagine an expiration date on your tax return. Once that date passes, the government's window to challenge it closes. This isn't just a bureaucratic quirk; it's a rule designed to strike a balance.

The IRS needs time to ensure everyone pays their fair share, but taxpayers deserve to move on without the threat of an audit hanging over their heads forever.

The three-year rule is the standard for the vast majority of returns. So, if you filed your 2023 return on April 15, 2024, the IRS generally has until April 15, 2027, to initiate an audit.

You can find more details on how these timelines work for different filers, like those living abroad, at Taxes for Expats.

But it's not always that simple.

When the Audit Clock Can Change

That standard three-year clock isn't set in stone. Certain actions—or inactions—can extend the timeline significantly, or even stop the clock altogether. The two biggest factors are the accuracy of what you reported and whether you filed in the first place.

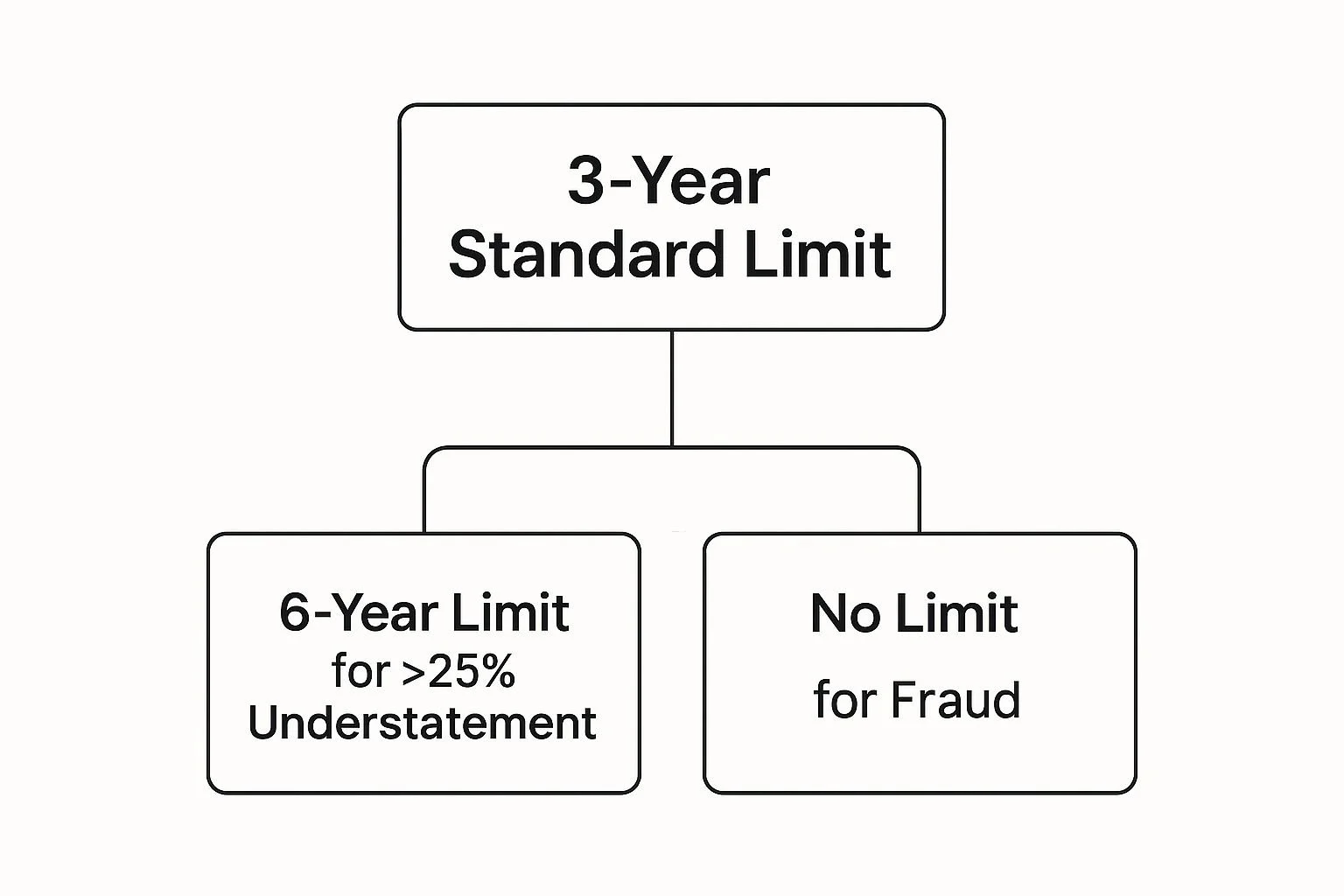

This image breaks down how the standard timeline can shift based on what the IRS finds.

As you can see, a major understatement of your income can double the audit window to six years. And in cases of fraud or failing to file, there's no time limit at all.

IRS Audit Timelines At a Glance

To make this easier to digest, here's a quick summary of the different time windows the IRS has to start an audit, depending on your situation.

| Situation | Statute of Limitations Period | Common Trigger |

|---|---|---|

| Standard Filing | 3 Years | Most returns filed on time with no major errors. |

| Significant Underreporting | 6 Years | Omitting more than 25% of your gross income. |

| Fraud or No Filing | Indefinite (No Limit) | Filing a fraudulent return, willful tax evasion, or not filing at all. |

Ultimately, understanding your potential exposure comes down to knowing which category your return falls into.

The Key Audit Periods to Know

Let's break these down into three simple buckets. Each one is triggered by a different set of circumstances.

The Three-Year Rule: This is your baseline. It applies to returns that are filed on time and are substantially accurate. It covers minor math errors or deductions that might be questionable but aren't glaring red flags.

The Six-Year Rule: This is a big step up. The clock extends to six years if you fail to report more than 25% of your gross income. This isn't for a small, forgotten 1099; we're talking about a substantial amount of unreported income.

The Indefinite Period: This is the most serious scenario. The statute of limitations never runs out. The IRS can come after you at any point in the future if you file a fraudulent return, willfully try to evade taxes, or simply don't file a return at all.

The bottom line is straightforward: The IRS audit statute of limitations is a protection you earn by filing an honest and timely tax return. For most Americans, the three-year rule provides a clear end date to their audit risk for any given year.

Navigating the Standard Three-Year Audit Window

For most people, the three-year audit window is the only one they ever need to worry about. Think of it as the default setting for the IRS audit statute of limitations.

It’s a predictable and, most importantly, finite period. Once that time is up, you can breathe a sigh of relief, knowing you don't have to look over your shoulder forever.

This three-year clock, officially called the Assessment Statute of Limitations (ASL), is a fundamental protection for taxpayers.

It stops the IRS from coming back years and years later to demand more tax for a return you filed honestly.

Understanding how this clock works is the first, biggest step to taking the mystery out of the whole audit process.

When Does the Three-Year Clock Actually Start Ticking?

It's a common mistake to think the clock starts the second you mail your return or click "submit" on your tax software. The truth is a little more specific, and it’s set up to be fair to both you and the IRS.

The three-year countdown actually begins on the later of two possible dates:

The date you actually filed your tax return.

The official tax filing deadline for that year (which is usually April 15th).

This little detail is critical. Filing your taxes early is a great habit, but it will not get you out of the audit window any sooner. The IRS always gets its full three years from the official due date, no matter how early you are.

Let’s see how this works with a couple of real-world examples for a 2023 tax return, which was due on April 15, 2024.

Example 1: The Early Bird You were on top of things and filed your return way back on February 10, 2024. But since the filing deadline (April 15, 2024) is later than your filing date, the audit clock starts on April 15, 2024. For this return, the statute of limitations will expire on April 15, 2027.

Example 2: The Extension Filer You needed more time, so you filed for an extension and submitted your return on October 1, 2024. Because your filing date is later than the original April 15 deadline, the clock starts on October 1, 2024. The statute of limitations for this one will expire on October 1, 2027.

Key Takeaway: Filing early doesn't speed anything up. The IRS audit clock won't start ticking before the original tax deadline, which gives the agency a consistent and fair window to do its job.

What Does It Mean for the Statute to Be "Open"?

While the statute of limitations is "open," the IRS has the legal green light to take a closer look at that specific tax year. This is the period when they can scrutinize your return for accuracy and ask questions.

If the statute is open for a tax year, the IRS can:

Launch an audit, whether by mail, an office visit, or a field examination.

Ask for more documents and records to back up your income, deductions, and credits.

Propose adjustments to what you owe.

Assess additional tax, penalties, and interest if they find mistakes.

But once that three-year window "closes," the IRS generally loses its right to assess more tax for that year. This is what provides the finality taxpayers need and deserve.

Unless a major exception applies—like drastically underreporting your income or outright fraud—you can finally consider that tax year put to bed.

Of course. Here is the rewritten section, crafted to sound completely human-written and natural, while preserving all original information, links, and formatting as requested.

When the Audit Clock Extends to Six Years

While that three-year deadline brings peace of mind to most of us, some situations give the IRS a much longer leash to dig into your finances.

The most common trigger that extends the IRS audit statute of limitations to six years is a substantial understatement of income.

We're not talking about a simple math mistake or a forgotten W-2 here. This is about a significant, game-changing omission.

This longer timeline really drives home the need for careful and complete tax reporting. When the IRS suspects a large chunk of income went missing—whether by accident or on purpose—it grants itself double the usual time to investigate.

If you have complex income streams as a freelancer, business owner, or investor, you absolutely need to understand what pulls this six-year trigger.

What Is a Substantial Understatement of Income?

The IRS doesn’t leave this open to interpretation; it’s a specific mathematical test. A substantial understatement of income happens when you leave off more than 25% of your gross income from your tax return. And pay close attention to that term "gross income." It means all the money you took in before a single deduction or expense is subtracted.

Think of it like this: your total income for the year is a whole pizza. If you only tell the IRS about a portion that's less than three-quarters of that pizza, you've just activated the 25% rule. The IRS now has six years, not three, to come looking for that missing slice.

Here’s a quick, real-world example of how the math plays out:

Your Gross Income: You're a freelance graphic designer who earned a total of $120,000 from various clients.

Your Reported Income: On your tax return, you only report $80,000 of that income.

The Calculation: The omitted income is $40,000 ($120,000 - $80,000). To find the percentage, you divide what you left off by what your correct income was: $40,000 ÷ $120,000 = 33.3%.

Since 33.3% is well over the 25% threshold, you’ve substantially understated your income. Just like that, the IRS audit statute of limitations for that tax year is extended to six years from the day you filed.

Important Note: The IRS bases this calculation on the income you should have reported, not the amount you actually put on the return. This is a clever and crucial detail. It prevents someone from hiding 90% of their income and then arguing the omission was only a small percentage of what they reported.

Other Triggers for the Six-Year Statute

While underreporting income is the most common culprit, a few other issues can also double the audit window. These often revolve around foreign assets and income, an area the IRS watches like a hawk to ensure everyone is complying with international tax law.

The six-year rule can also kick in if you:

Omit Foreign Income: Fail to report more than $5,000 of income generated from foreign financial assets. This could be anything from interest earned in a Swiss bank account to dividends from an investment in a Japanese company.

Miss Foreign Asset Forms: Neglect to file required informational forms for your foreign holdings, like the critical Form 8938 (Statement of Specified Foreign Financial Assets).

Have an Overstatement of Basis: Significantly inflate the original cost (or "basis") of a property you sold. By claiming you paid far more for an asset than you actually did, you artificially lower your taxable gain—something the IRS views as a serious misstatement.

These triggers reveal a clear pattern. The six-year statute of limitations isn't for minor slip-ups; it's reserved for significant errors, omissions, and misstatements.

Whether it’s domestic income, foreign accounts, or property sales, the underlying principle is the same: the bigger the mistake, the longer the IRS has to find it.

Meticulous record-keeping, especially with varied income sources or foreign investments, is your best defense against this extended scrutiny.

When the IRS Has Unlimited Time to Audit

For most people, the three and six-year audit windows offer a welcome sense of finality. But there are a few situations—very serious ones—where the IRS audit statute of limitations simply gets thrown out the window.

In these rare cases, the audit clock never even starts, giving the IRS a permanent green light to come knocking.

This isn’t something you need to worry about if you made an honest mistake or got tripped up on a complicated deduction.

The unlimited audit window is reserved for the most severe forms of non-compliance, where a taxpayer has intentionally tried to break the system.

Filing a Fraudulent Return

The most clear-cut reason for an unlimited audit period is filing a fraudulent return. I'm not talking about a big error or negligence here; this is about intentional, willful deception. To make a civil fraud case stick, the IRS has to prove you knew you owed tax and deliberately tried to evade it.

Think of it this way: accidentally backing your car into a mailbox is a mistake. Hotwiring a car and taking it for a joyride is a willful act. The IRS has a high bar to prove fraud, which is why it's not an accusation they make lightly.

So, what does this look like in the real world?

Keeping two separate sets of financial books—one for you, one for the IRS.

Creating fake receipts or invoices to claim deductions for expenses you never paid.

Claiming nonexistent children or relatives as dependents.

Intentionally hiding assets or income in offshore accounts to avoid detection.

When the IRS proves fraud, the whole idea of a statute of limitations goes away. The government’s logic is that if you intentionally cheat, you forfeit your right to that protection.

Willful Attempt to Evade Tax

This one is a close cousin to fraud and covers a wide range of deliberate actions meant to mislead or conceal information from the IRS, even beyond the return itself. It’s all about a conscious effort to duck a tax bill you know you have.

For instance, a business owner who insists on cash-only transactions specifically to avoid creating a paper trail could be on the hook.

Another classic example is someone who learns they are under audit and immediately starts shredding financial records. These actions scream intent, and that can give the IRS an indefinite amount of time to investigate and assess taxes.

Failing to File a Return

The last trigger for an indefinite audit window is the simplest one of all: failing to file a tax return. The logic here is ironclad.

The statute of limitations clock can't start ticking if there's no return to start it from.

If you were required to file a return for a certain year and just... didn't, that year remains open forever. It doesn't matter if it was five, ten, or even twenty years ago. The IRS can show up anytime, create a Substitute for Return (SFR) for you, and calculate the tax, penalties, and interest they believe you owe.

The good news? Filing that late return, even years down the road, finally gets the clock started. Once a valid return is on the books, the standard three-year (or six-year, if applicable) statute of limitations begins. While getting it done on time is always the goal, it's also smart to know how to avoid an IRS audit in the first place.

How State Audits and Amended Returns Affect the Clock

It's a common trap to think your audit worries are over once the IRS clock runs out. But for most people, the federal return is only half the story.

If you live in a state with an income tax, you're also dealing with a state tax agency—and they have their own rulebook, their own deadlines, and their own auditors.

This means you’re on two separate timelines. The IRS audit statute of limitations has absolutely no bearing on your state tax return. So, even if the three-year federal window has slammed shut, the one for your state might still be wide open.

State vs. Federal Audit Timelines

The timelines can be quite different. Many states mirror the IRS’s three-year rule, but a surprising number give themselves more time to dig into your filings. Some tack on an extra year or more, which is a crucial detail if you're earning income or doing business in multiple states.

Let's look at how a few states stack up against the federal government. You’ll see it’s not a one-size-fits-all situation.

Comparison of State vs. Federal Audit Statutes

Here’s a quick comparison to highlight how different the standard audit statute of limitations can be between the IRS and several key states.

| Jurisdiction | Standard Audit Period | Notes |

|---|---|---|

| IRS (Federal) | 3 Years | This is the federal baseline for income tax returns. |

| California | 4 Years | The Franchise Tax Board (FTB) gives itself an extra year to review your return. |

| New York | 3 Years | New York's standard timeline aligns with the federal rule. |

| Texas | 4 Years | The Texas Comptroller has four years for audits on things like sales and franchise tax. |

As you can see, if you’re a taxpayer in California, you need to hold onto your records and stay on your toes for a full four years. Your federal risk might be gone, but the state can still come knocking.

How Filing an Amended Return Affects the Clock

What if you find a mistake on a past return and file a Form 1040-X to fix it? This is where a lot of people get nervous. The big fear is that filing an amended return throws the door wide open again, resetting the entire three-year audit clock on the whole return.

Thankfully, that’s not what happens.

Filing an amended return does not restart the original three-year statute of limitations. Instead, the IRS gets a much smaller, more specific window to look at what you changed.

The IRS generally gets just 60 days from receiving your amended return to assess more tax, and only on the specific items you amended. This 60-day rule kicks in only if the main three-year statute has already passed or has less than 60 days left on it.

Think of it this way: the main audit window for your original return is closing on its normal schedule. Amending it just props open a tiny side window for a very short time, letting the IRS peek only at the specific things you changed.

For instance, say you amend your 2021 return back in 2024 to claim an education credit you forgot. The IRS can’t use that as an excuse to start questioning your 2021 business mileage.

Their review is strictly limited to that new credit. This is a good thing—it allows taxpayers to do the right thing and correct errors without the fear of inviting a massive, unrelated audit.

What to Do If You Receive an Audit Notice

That thick envelope from the IRS sitting in your mailbox is enough to make anyone’s heart skip a beat. But before you let your mind race, take a deep breath. The single most important thing to do right now is this: do not panic.

An audit notice isn’t an accusation; it's simply a request for more information. And while audit rates have dropped significantly over the past decade—from 0.6% in 2013 down to just 0.2% in 2021—you still need a solid game plan.

Understanding how the IRS audit statute of limitations works is a key piece of that puzzle. For more on how the IRS handles these reviews, especially through correspondence, check out the insights at CRLaw.com.

Your first real step is to read the notice—and I mean really read it. Don't just glance it over. The letter will tell you exactly what the IRS is looking at, which tax year is under the microscope, and what kind of audit you're facing.

Identify the Audit Type and Scope

Knowing what kind of audit you're dealing with is crucial because it dictates your next moves. The IRS will be very clear about which type it is:

Correspondence Audit: This is the most common and least intimidating type of audit. It’s handled entirely through the mail. The IRS might just need you to send over copies of receipts for charitable donations or proof of certain business expenses to clear things up.

Office Audit: This one is a step up. You'll need to go to a local IRS office and meet with an agent. They'll review your records for the specific items they flagged in the notice. It’s more targeted than a full-blown field audit.

Field Audit: This is the most serious and in-depth audit. An IRS agent will actually come to your home, business, or accountant's office to do a comprehensive review of your books and records.

Once you’ve identified the audit type, gather only the documents the IRS has asked for and only for the year they specified. It’s tempting to over-explain or send extra information to be "helpful," but that can backfire. Stick to the script and give them exactly what they requested, nothing more.

Decide on Your Next Steps

With the notice understood and your documents in hand, you’ve reached a fork in the road. Do you handle this yourself, or do you call in a professional?

For a simple correspondence audit with a clear-cut issue, you might be perfectly fine managing it on your own.

However, if you're facing an office or field audit, or if the subject matter feels over your head, getting professional help is almost always the right call. A seasoned tax attorney or CPA knows how to speak the IRS's language. They'll handle the communication, protect your rights, and make sure you don't accidentally say or provide something that turns a small problem into a big one.

If the audit concludes and you end up with a tax bill you can't afford to pay, don't despair. You still have options. Sometimes, it’s possible to negotiate a settlement. It might be worth reading our guide on how to qualify for an Offer in Compromise, as this can be a lifeline for resolving overwhelming tax debt.

Frequently Asked Questions

Even after you get a handle on the rules, it's the specific, real-world questions that often pop up. Let's tackle some of the most common points of confusion I hear from clients to make sure these concepts are crystal clear.

Does the Audit Statute Apply to Tax Debt Collection?

No, it doesn't. This is one of the most important distinctions a taxpayer needs to understand.

The audit statute of limitations is strictly about the IRS's window to assess a new tax—basically, their time limit to look at your return and decide you owe more. Once that tax is officially on the books, a completely different clock starts for collections. The IRS generally has 10 years from the date of assessment to actually collect the debt. These are two separate timelines for two very different IRS actions.

Should I Agree to Extend the Statute of Limitations?

This is a classic audit scenario. The IRS agent is running out of time on a complex audit and asks you to sign a form (like Form 872) to voluntarily extend the deadline. This gives them more time to finish their work without being forced to slap you with a preliminary assessment.

You can absolutely say no. But refusing often forces the agent's hand, prompting them to issue an immediate bill based only on the information they have so far—which is rarely in your favor. It is always a smart move to talk to a tax professional before you even think about signing an extension.

Expert Insight: It might sound counterintuitive, but agreeing to an extension can be a smart strategic play. It can give you and your representative more time to negotiate and head off a rushed, inflated tax bill. But this is a decision that requires careful, professional guidance.

What if the IRS Audits Me After the Statute Expires?

If the IRS tries to hit you with an additional tax assessment after the legal deadline for that tax year has passed, that assessment is generally invalid. This is a fundamental taxpayer right and your strongest defense against an audit that's out of bounds.

Of course, it's not automatic. You or your tax pro have to formally challenge the assessment by proving the statute of limitations had, in fact, expired. This means being certain none of the exceptions we discussed—like the six-year rule for a substantial understatement or any hint of fraud—apply to your case. If you're in this spot, looking into an IRS audit reconsideration could be the critical next step to setting things right.

If you're facing an audit or dealing with tax debt, you don't have to navigate it alone. At the law office of Attorney Stephen A Weisberg, we start with a free, no-obligation tax analysis to determine the best path forward for your unique situation. Contact us today to get the clear answers and expert help you deserve.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034