How to Avoid an IRS Audit A Practical Guide

Want to know the secret to avoiding an IRS audit? It’s surprisingly simple: file a tax return that’s complete, accurate, and backed by meticulous records.

It’s all about being honest, organized, and proactive. When you adopt that mindset, tax season stops being a source of stress and becomes just another part of your financial routine.

Understanding Your Audit Risk in Today's Tax Climate

Just the thought of getting a notice from the IRS is enough to make anyone’s stomach drop. But the first step to preventing an audit is understanding what the IRS is actually looking for right now. The landscape has definitely shifted.

A huge part of this change comes down to money. Thanks to a recent funding boost, the IRS has been hiring more agents and, more importantly, upgrading its technology.

They’re now using sophisticated AI and data analytics to automatically cross-reference information and flag returns that look fishy or deviate too far from the norm.

Who Is Under the Microscope?

While anyone can technically be audited, the IRS focuses its energy where it’s most likely to find errors or unreported income. Knowing if you fit into a higher-risk category is crucial.

Right now, enforcement is ramping up, especially for:

High-Income Earners: If you're reporting substantial income—especially over $400,000—you're statistically more likely to attract attention.

The Self-Employed and Gig Workers: Anyone filing a Schedule C has more opportunities to make mistakes when reporting income and expenses, which the IRS knows all too well.

Investors with Complex Assets: If your return includes cryptocurrency transactions, large capital gains, or rental property income, the complexity alone increases the chances of a second look.

The truth is, most audits aren't random. They are triggered by specific items on your return that an IRS computer or agent has flagged as needing a closer look. Being aware of these triggers is your first line of defense.

To give you a clearer picture, I've put together a table of common red flags. Understanding these triggers is one of the best ways to build a return that flies under the radar.

Top IRS Audit Red Flags and Proactive Tips

| Red Flag | Why It Attracts Scrutiny | Proactive Tip |

|---|---|---|

| Claiming Large, Unsubstantiated Deductions | Taking unusually high deductions compared to your income (e.g., claiming 100% business use of a vehicle) is a classic trigger. | Keep flawless records. Use a mileage log app for vehicle expenses and keep every single receipt for business purchases. |

| Errors on Your Return | Simple math mistakes, transposed numbers, or mismatched information (like your name or SSN) can get your return flagged by automated systems. | Double-check everything before you file. If you use a tax preparer, review the return yourself before it's submitted. |

| High Income | Taxpayers earning over $400,000 are a known priority for the IRS, as the potential for recovering unpaid tax is much higher. | Work with a tax professional who has experience with high-net-worth individuals to ensure every detail is correct and defensible. |

| Significant Rental Real Estate Losses | Claiming large losses from rental properties can be a red flag, especially if you have high W-2 income. | Understand the passive activity loss rules. Document your "material participation" to justify your ability to deduct losses. |

This isn't an exhaustive list, but it covers the big ones. The common thread is always documentation and consistency.

Proactive Steps for Prevention

Just knowing the risks isn’t enough—you have to act. The key to audit-proofing your return is creating a financial story that’s clear, logical, and fully supported by documentation. This is where preparation becomes prevention. For a deeper dive, I highly recommend learning more about IRS audit and what really happens behind the curtain.

To really get ahead of the game, I suggest using an ultimate audit readiness checklist to guide your preparation. This shifts tax filing from a reactive chore to a strategic move that protects your finances.

By understanding who the IRS is targeting and why, you can assess your personal risk and build a return that’s not just compliant, but audit-resilient.

Building an Audit-Proof Record-Keeping System

Think of your financial records as your first line of defense. If the IRS ever comes knocking, impeccable documentation is the single most powerful tool you have.

This isn’t about just cramming receipts into a shoebox and hoping for the best. It's about building a clear, logical story that proves every single number on your tax return.

A solid system does more than just prepare you for a potential audit; it turns the annual tax-filing scramble into a predictable routine.

More importantly, it creates a transparent financial trail that leaves little room for an auditor to question your integrity. This kind of proactive bookkeeping is a cornerstone of staying off the IRS's radar.

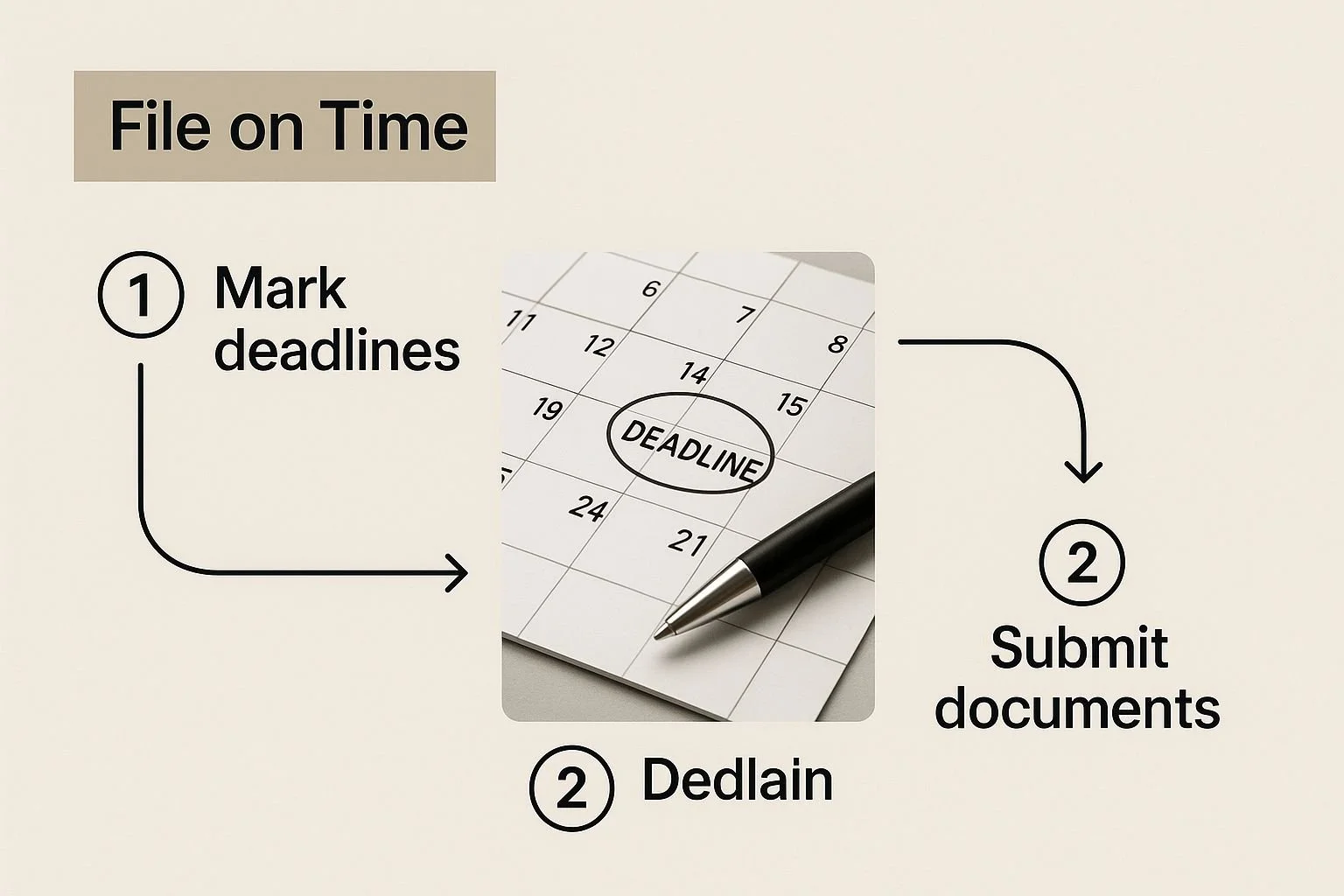

The infographic below highlights a simple, yet critical, first step in any record-keeping strategy—just being on time.

Filing on time is foundational. It helps you avoid late-filing penalties, which are an easy way to attract unwanted attention from the IRS.

Ditch the Shoebox and Go Digital

Let's be honest, the days of wrestling with stacks of paper are over. A digital system isn't just a matter of convenience; it’s more secure, searchable, and far more efficient. The trick is to find a method that you'll actually use and stick with it consistently.

You could use dedicated accounting software or even a well-organized set of folders on a cloud drive. Consistency is everything. When an email receipt lands in your inbox, save it immediately to the right folder.

Get a paper receipt? Use a scanning app on your phone to snap a picture right then and there. This simple habit solves the age-old problems of faded ink and lost slips of paper.

For a great deep dive into how to store important documents, check out this resource. It offers excellent strategies for both physical and digital preservation.

Separate Your Business and Personal Finances

This one is absolutely non-negotiable, especially if you're self-employed, a freelancer, or run a small business. Mixing your finances—using a personal credit card for business supplies or paying a personal bill from your business account—is one of the fastest ways to invite IRS scrutiny. It makes proving what’s a legitimate business expense a nightmare.

Do yourself a favor: open a separate checking account and get a dedicated credit card just for your business. Period. All business income goes in, and all business expenses go out.

This simple move creates a clean, easy-to-follow financial trail. An auditor can see your business’s financial life without wading through your personal grocery receipts and Netflix subscriptions. It instantly adds a layer of credibility to your tax return.

What to Keep and For How Long

Knowing what to save is just as critical as how you save it. Your goal is to be able to back up every piece of income, every deduction, and every credit you claim on your return.

Here’s a checklist of the essentials:

Proof of Income: This means all your W-2s, 1099 forms (like MISC, NEC, K, DIV, INT), and if you're a business, complete records of all payments you've received.

Expense Records: Hold onto receipts, invoices, canceled checks, and bank or credit card statements that detail your business spending. For big-ticket items, keep the proof of payment, too.

Home Office Deduction Records: Claiming this? You'll need utility bills, rent or mortgage statements, insurance records, and repair invoices, plus the math showing how you calculated the percentage of your home used for business.

Charitable Donations: For cash gifts, you need a bank record or a written note from the charity. For any non-cash donations over $250, you must have a formal written acknowledgment from the organization.

Investment Transactions: Keep all your brokerage statements (like Form 1099-B) that show purchases, sales, and the cost basis for stocks, bonds, and especially any cryptocurrency trades.

So, how long do you need to hang onto all this? As a general rule, keep your tax records for at least three years from the date you filed. But that window stretches to six years if you happen to underreport your gross income by more than 25%.

Personally, I advise clients to keep records for a conservative seven years just to be safe. This documentation is also crucial if you ever need to get caught up; our guide on how to file back taxes explains what you'll need.

Navigating High-Risk Areas on Your Tax Return

Certain parts of a tax return just beg for a second look from the IRS. If you know what these high-scrutiny zones are, you can prepare a return that sails through the system without raising any eyebrows.

It’s all about anticipating what an auditor might question and building a rock-solid case for every number you report from the get-go.

Put yourself in the IRS's shoes for a moment. Their job is to make sure everyone's playing by the rules, so they naturally focus their resources on areas where mistakes—or let's be honest, intentional misrepresentations—are most common.

This usually means big or unusual deductions, self-employment income, and any kind of complex financial activity.

Mastering Self-Employment and Business Deductions

Filing a Schedule C for your business or side hustle automatically puts you in a higher statistical risk pool for an audit.

Don't take it personally. It’s just that this form is loaded with deduction opportunities that are incredibly easy to get wrong or overstate.

The home office deduction is a classic example. Claiming it isn't the problem; claiming it incorrectly is what gets you into hot water. You've got two ways to calculate it, and each has its own documentation requirements.

Home Office Calculation Methods:

The Simplified Method: This is the no-fuss approach. You can deduct $5 per square foot of the part of your home used for business, but only up to 300 square feet. That caps your deduction at a clean $1,500. You'll need proof of the square footage, but not every single utility bill.

The Actual Expense Method: This one takes more effort but can lead to a much bigger deduction. You have to figure out the percentage of your home used "regularly and exclusively" for business and then apply that percentage to your actual home expenses—things like mortgage interest, insurance, utilities, and repairs. For this, meticulous records aren't just a good idea; they're mandatory.

Beyond the home office, watch out for business meals and entertainment. You can typically deduct 50% of the cost of business-related meals.

To make that deduction stick, you need to be able to show the date, location, amount, the specific business purpose, and who was there. A vague receipt note like "business lunch" just won't cut it during an audit.

Handling Charitable Donations and Large Deductions

The IRS absolutely wants to encourage charitable giving with tax deductions, but they also want to be sure those claims are legit. Small cash donations are one thing, but as soon as you start talking about larger contributions, especially non-cash items, the burden of proof is on you.

If you donate more than $500 in property (think clothes, furniture, or even a vehicle), you must file Form 8283. For any donation valued over $5,000, you’ll almost certainly need to get a qualified appraisal. The golden rule is to get a formal acknowledgment letter from the charity for any single donation of $250 or more.

A common trip-up I see is people trying to claim a deduction for the "value" of their volunteer time. You can deduct your out-of-pocket costs while volunteering, like mileage, but you can't deduct the value of your labor. That's a critical distinction.

The Growing Scrutiny on Investments and High Income

Heads up: the IRS is sharpening its focus on complex investments and high-income taxpayers, and they've got the technology and funding to back it up.

Returns showing significant capital gains from stocks, rental property income, or cryptocurrency trades are getting a much closer look these days.

This isn't a passing trend. Audit rates for the wealthiest taxpayers and big corporations are set to climb significantly.

Individuals earning over $10 million could see their audit rate jump from 11% to 16.5% by 2026, while large corporations might see their rate leap from 8.8% to a staggering 22.6%. You can learn more about these IRS audit targets and how they might affect high earners.

For investors, this means documenting your cost basis—what you paid for an asset in the first place—is more critical than ever.

When you sell a stock or crypto, your taxable gain is the sale price minus your cost basis. If you can't prove your basis, the IRS might just assume it's zero, sticking you with a much, much higher tax bill.

Staying on top of these areas takes diligence. But if you understand the rules and keep the right paperwork, you can confidently claim what you're entitled to and drastically lower your odds of a stressful and expensive IRS audit.

Why Filing a Flawless Return Is Non-Negotiable

After all the hard work of organizing your records and identifying your audit risk areas, we arrive at the final—and most important—step: filing a completely error-free return.

Think of it this way: you can study for weeks, but if you make a simple mistake on the final exam, your grade still suffers. With taxes, that "bad grade" often comes in the form of an IRS notice.

Accuracy isn't just a nice-to-have; it's your primary defense against an audit. The IRS runs on powerful automated systems designed specifically to sniff out inconsistencies.

Even a tiny, honest mistake can create a mismatch that gets your return kicked out of the automated pile and onto a human reviewer's desk. That's why getting it perfect is non-negotiable.

The High Cost of Simple Mistakes

In my experience, it's almost always the small, silly oversights that snowball into the biggest problems. I’ve seen a single transposed digit in a Social Security number completely derail a dependent claim.

I’ve seen simple math errors on a list of deductions trigger a scary-looking letter from the IRS.

These aren't red flags for fraud, but they are signals to the IRS that something about your return isn't quite right, which is all the invitation they need to dig deeper.

One of the most common and easily avoidable triggers is mismatched income. Here's a critical fact: the IRS already has your W-2s and 1099s.

Its computers automatically cross-reference the income you report with the figures they received from your employers and clients. If those numbers don't line up to the dollar, you are all but guaranteeing yourself a CP2000 notice, or worse, a full-blown audit.

The goal is to file a return so clean and straightforward that it gives the IRS no reason to even pause. When every number matches, every name is spelled correctly, and all the math adds up, your return just sails right through the system.

A Final Review Checklist

Before you or your tax pro hits that "submit" button, you need to do one last, careful review. Treat it like you're proofreading the most important document of your year, because that's exactly what it is.

Here's a quick rundown of the common—and costly—errors I see all the time:

Social Security Numbers: Double-check your own SSN and the numbers for your spouse and any dependents. A typo here is a classic reason for a rejected return and flagged claims.

Math Check: Seriously, re-check the math. From adding up your itemized deductions to calculating your final tax owed, it's easy for a number to get fumbled.

Income Verification: Pull out your W-2s and 1099s and put them right next to your tax form. Make sure every single dollar has been accounted for. Don't round up or guesstimate.

Filing Status: Are you sure you chose the right filing status (Single, Married Filing Jointly, Head of Household, etc.)? Picking the wrong one can drastically change your tax liability and immediately attract attention.

Using E-Filing and Timelines to Your Advantage

This is one area where modern technology is a huge help. E-filing your return, either through software or a professional, is one of the best ways to avoid an IRS audit.

The software itself acts as a first line of defense, automatically checking for math errors and flagging empty fields before the return can even be sent.

It’s also crucial to understand how time plays into this. Generally, the IRS has three years from the date you file to audit you.

But a major mistake can throw that timeline out the window. If you understate your gross income by more than 25%, that statute of limitations stretches to six long years.

If the IRS suspects fraud, there is no time limit at all. You can explore the full details of these timelines to see just what’s at stake.

Getting your return right the first time isn't just about avoiding an immediate headache. It’s about closing the book on that tax year for good. A flawless return is a quiet return, and when you're dealing with the IRS, "quiet" is a beautiful thing.

When You Should Hire a Tax Professional

Look, I get it. DIY tax software is incredibly powerful these days. But let’s be honest—knowing when to call in a professional is the mark of a truly savvy taxpayer.

Certain life events and financial situations crank up the complexity so much that getting expert guidance isn't just a nice-to-have.

It’s absolutely essential for staying on the right side of the IRS and making sure you're not leaving money on the table.

This isn’t about throwing in the towel on your finances. It's about acknowledging that the U.S. tax code is an absolute beast. A good tax professional does so much more than just plug numbers into a form.

They bring strategy, foresight, and a critical line of defense to the table, making their fee one of the best investments you can make in your own peace of mind.

Signals That You Need Expert Help

Some financial moves are like bright, flashing neon signs telling you it's time to upgrade from that software subscription. If any of these sound familiar, the cost of hiring a pro is almost always a fraction of what a mistake could cost you down the line.

You've Started a Business: The second you hang your shingle—whether you're a sole proprietor, have an LLC, or formed an S Corp—your tax world gets infinitely more complicated. Suddenly, you're juggling self-employment taxes, figuring out quarterly estimated payments, and navigating a dizzying array of business deductions, each with its own rulebook.

You Manage Rental Properties: Owning rental real estate throws a ton of jargon your way. Think depreciation schedules, passive activity loss rules, and correctly classifying every expense as either a repair or an improvement. An expert ensures you’re legally maximizing your deductions while keeping the rock-solid records you'll need if the IRS ever comes knocking.

You've Received an Inheritance or Large Gift: Coming into a chunk of money or property isn't as simple as a bank deposit. It can trigger all sorts of complex tax issues, not just for you but for the estate that gave it to you. A pro can walk you through things like basis adjustments and any future tax headaches you need to be aware of.

You're Trading Cryptocurrency: The IRS is laser-focused on digital assets right now. I’ve seen countless people get tripped up trying to track cost basis, report gains and losses correctly, and handle funky situations like airdrops or staking rewards. Getting this wrong is an easy way to attract unwanted attention.

Think of a tax professional as an experienced guide for your financial journey. You can probably handle the familiar trails in your local park just fine on your own. But when you decide to scale a mountain, you hire a guide who knows the terrain, the weather, and exactly where the hidden crevasses are.

Understanding the Different Kinds of Tax Pros

Not all tax experts wear the same hat. The right choice really hinges on your specific needs, whether you're just filing a complex return or staring down a serious issue with the IRS. Knowing who does what helps you find the right person for the job.

Comparing Tax Professionals

| Professional Title | Primary Role and Expertise | Best For... |

|---|---|---|

| Enrolled Agent (EA) | EAs are licensed directly by the IRS. They are pure tax specialists who can represent taxpayers in any matter before the IRS. Their world is 100% tax—preparation, planning, and representation. | Individuals and small businesses with complex tax returns, those needing audit representation, and anyone looking for ongoing strategic tax planning. |

| Certified Public Accountant (CPA) | CPAs are state-licensed and have a broader background in general accounting, auditing, and business consulting on top of tax services. | Business owners who need a full suite of financial services, like bookkeeping, creating financial statements, and strategic business advice alongside their tax work. |

| Tax Attorney | A lawyer who specializes in tax law. They are the only ones who can represent you in U.S. Tax Court and are equipped to handle serious legal battles with the IRS, including criminal tax investigations. | Taxpayers facing massive tax debt, scary audits, accusations of tax evasion, or other high-stakes legal tax disputes. |

For most people, a top-notch EA or CPA is the perfect partner for getting their annual taxes filed correctly and planning for the year ahead. Their expertise is gold for minimizing what you owe while making your return as bulletproof as possible.

But if you find yourself in a really tough spot—like owing a significant tax debt you simply can't pay—a tax attorney can open up doors to solutions you might not even know exist.

For instance, if you're buried under a large tax bill, it's worth learning from a qualified professional how to qualify for an Offer in Compromise.

Ultimately, bringing a professional onto your team is a strategic investment in your financial well-being. Their guidance doesn't just help you sidestep an audit; it empowers you to make smarter financial decisions, year after year.

Common Questions About IRS Audits

Even when you've done everything right, a few nagging questions about IRS audits can still cause a lot of anxiety.

Let's tackle these common concerns head-on. Clearing up the gray areas gives you the confidence to manage your tax life without letting myths or fear call the shots.

Understanding the reality behind these scenarios is a huge part of building a smart, proactive tax strategy.

What Are My Real Chances of Being Audited?

This is the question everyone wants an answer to, and the truth is: it depends entirely on your situation. The often-quoted statistic is that the audit rate for individual tax returns is less than 1%. But that number can be seriously misleading.

Your personal risk isn't a random lottery. It’s heavily influenced by your income, the complexity of your return, and whether you run a business.

Think of it this way: someone with a single W-2 job and the standard deduction has an almost zero chance of being audited.

On the other hand, a high-earning consultant with a Schedule C packed with business expenses is playing in a different league.

The IRS puts its resources where it expects to find money, so your specific financial profile is what really determines your odds.

Does Filing an Extension Increase My Audit Risk?

This is one of the most stubborn myths in the tax world, and I'm happy to bust it. The answer is a clear and simple no. Filing for an extension does not make you a target. In fact, most tax professionals I know agree it can do the opposite.

Put yourself in the IRS's shoes for a second. An extension means you're taking extra time to get your documents in order and ensure your return is accurate. A return slapped together in a panic on April 15th is far more likely to have mistakes than a carefully prepared one filed in October. The IRS wants accurate returns, not just fast ones.

Filing an extension shows you’re taking your tax obligations seriously and prioritizing accuracy. It’s the mark of a diligent taxpayer, not a suspicious one.

Is It Risky to Amend a Tax Return?

Amending a return with Form 1040-X isn't inherently risky, as long as you're doing it for the right reasons—like correcting an honest mistake or claiming a credit you overlooked. The why behind the amendment is what matters.

For instance, if you forgot to report $50 in interest from a savings account and file an amended return to correct it, the IRS will almost certainly just process it and move on. No big deal.

However, if you amend a return to make a huge, aggressive change—like suddenly claiming a massive home office deduction you've never taken before—that could definitely raise a red flag.

The best move is always to file an amended return as soon as you find a significant error. Being upfront is always better than hoping the IRS doesn't notice.

What Should I Do If I Get an IRS Notice?

First thing's first: don't panic. The overwhelming majority of letters from the IRS are not audit notices. They're usually simple, automated letters asking for more information, pointing out a math error, or flagging a mismatch between what you reported and a 1099 form they received.

Here’s your game plan:

Read the notice from top to bottom. Understand exactly what the IRS is asking for and, most importantly, the deadline for your response.

Pull your records. Gather the specific documents that support the item in question on your tax return.

Respond in writing before the deadline. Never, ever ignore an IRS notice. A clear, professional response with copies of your supporting documents is often all it takes to close the matter.

If the notice seems complicated or you feel in over your head, that's the time to call a tax professional. Sometimes, that notice can even be the first step toward a better outcome. For those with a large tax bill, there are relief options available, and it's worth exploring the details of the IRS tax forgiveness program with an expert to see if you might qualify.

At Attorney Stephen A Weisberg, we understand that dealing with the IRS can be intimidating. With over a decade of experience, our team helps individuals and businesses navigate complex tax issues, from audits to debt resolution, ensuring you get the best possible outcome. Start with a free, no-obligation tax debt analysis to understand your options.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034