Understanding IRS Non Collectible Status

When you're staring down a mountain of IRS debt, it can feel like the walls are closing in. But the IRS actually has a provision for people going through genuine financial turmoil. It’s called IRS non collectible status, or more formally, Currently Not Collectible (CNC).

Think of it as the IRS hitting a temporary "pause button" on their collection machine. If you truly can't afford to pay your tax debt without sacrificing basic living expenses—like rent, food, and utilities—the IRS can agree to back off for a while. This immediately stops scary actions like wage garnishments and bank levies, giving you some much-needed breathing room.

Decoding IRS Non Collectible Status

This status isn't a get-out-of-jail-free card. It's a formal acknowledgment by the IRS that, right now, you simply don't have the means to pay. They recognize that trying to squeeze money out of you would cause an "economic hardship," a term they take quite seriously.

The core idea is to provide a safety net. It allows you to stabilize your financial situation without the constant threat of having your paycheck seized or your bank account wiped out.

Currently Not Collectible Status At a Glance

To quickly grasp what CNC status does and doesn't do, here’s a simple breakdown.

| Feature | Description |

|---|---|

| What It Is | A temporary suspension of IRS collection activities like levies and wage garnishments. |

| Primary Purpose | To provide relief for taxpayers experiencing significant financial hardship. |

| Debt Status | The tax debt remains and continues to grow due to penalties and interest. |

| Duration | It's not permanent. The IRS will periodically review your financial situation to see if you can pay again. |

| Eligibility | Based on a detailed analysis of your income, assets, and essential living expenses. |

| Key Takeaway | It's a "pause button," not a "delete button" for your tax liability. |

This table highlights that CNC is a temporary measure, a bridge to get you through a tough time, not a final solution to your tax problem.

The Pause Button vs. The Delete Button

It's absolutely critical to understand that CNC status pauses collection, it doesn't erase the debt. This is the single biggest point of confusion for many taxpayers.

While you're in CNC status, the IRS collection notices will stop. But behind the scenes, your tax bill is still growing. Penalties and interest continue to pile up, which means the total amount you owe will be larger when the IRS determines you can afford to pay again.

This makes CNC fundamentally different from an Offer in Compromise (OIC), where the IRS agrees to settle your tax debt for a lower amount than you originally owed.

The IRS Framework for Hardship

The IRS doesn't hand out CNC status easily. You have to prove that paying them would leave you unable to cover your necessary living expenses. They will put your finances under a microscope, looking at your income, assets, and monthly bills to confirm that you are facing a legitimate hardship.

This isn't just an informal agreement; it's an official designation. The IRS follows specific internal guidelines when evaluating these cases, as outlined in their procedures for IRS hardship evaluations on their website.

By placing an account in CNC status, the IRS recognizes that pursuing collection at that moment is not feasible. This action provides taxpayers with the space needed to address their financial challenges without the immediate threat of enforced collection.

Ultimately, CNC is a lifeline for those who truly cannot pay. It’s a temporary hold, a stepping stone toward getting back on your feet and figuring out a long-term plan to resolve your tax debt for good.

How to Qualify for IRS Hardship Status

Qualifying for IRS non collectible status isn't just a matter of having a low income. It's about demonstrating, with hard numbers, that paying your tax bill would make it impossible to cover your basic, necessary living expenses. The IRS has a very specific, data-driven method for figuring out if you're truly facing financial hardship.

Think of your monthly budget as a bucket. Your income is the water coming in, while your essential expenses are holes in the bottom where water has to go out. The IRS grants hardship status when there’s simply no water left in the bucket for them after your necessary costs are met.

The IRS Financial Analysis Formula

To figure this out, the IRS puts your finances under a microscope. They take your total monthly income and weigh it against a set of standardized allowable living expenses. It’s a formulaic approach designed to see if you have any "disposable income" left over once you’ve paid for necessities.

The IRS doesn't just pull these numbers out of thin air. They use a combination of national and local standards to determine what’s considered a reasonable expense. This is their way of being fair, acknowledging that the cost of living in downtown Los Angeles is a world away from rural Kansas.

These standards cover the absolute basics:

Food, Clothing, and Miscellaneous: This is a national standard that changes based on your income and the number of people in your household.

Housing and Utilities: A local standard based on the county where you live. It covers things like rent or mortgage payments, property taxes, insurance, and utilities.

Transportation: These are also local standards that account for either vehicle ownership costs or what you'd spend on public transit in your specific area.

If your actual expenses are legitimately higher than these official standards, you’ll need to provide solid proof to justify them.

Scrutinizing Your Entire Financial Picture

The IRS is going to want a complete, warts-and-all look at your financial life. You'll provide this by filling out Form 433-F, the Collection Information Statement. Be ready to document everything with painstaking accuracy.

They zero in on three key areas:

Total Income: This means all of it—wages, self-employment earnings, Social Security, rental income, and any other money coming in the door.

Monthly Expenses: You'll have to list out all of your necessary living costs, from rent and car payments to groceries and health insurance premiums.

Asset Valuation: The IRS will examine the equity you have in assets like your home, vehicles, and bank accounts to determine if you could liquidate them to pay your debt.

The IRS's entire goal here is to confirm that you genuinely cannot pay. Any inaccuracies or things you leave off your financial statement can get your request for hardship status denied on the spot.

This is why giving them complete and honest information is absolutely critical. It’s the entire foundation for proving you need IRS non collectible status.

Real-World Scenarios That Lead to Hardship

Financial hardship often isn't a slow burn; it’s frequently triggered by a sudden, life-altering event that completely upends your financial stability. These situations throw the income-versus-expense equation so far out of whack that paying taxes becomes an impossibility.

Think about these common situations:

Sudden Job Loss: A taxpayer gets laid off from a job they've had for years. Their income vanishes overnight, but the mortgage and car payments don't, creating an instant financial crisis.

Unexpected Medical Crisis: A serious diagnosis brings a mountain of medical bills and an inability to work. Suddenly, income plummets just as expenses are skyrocketing.

Long-Term Disability: A life-changing accident leads to a permanent disability, forcing someone onto a fixed, reduced income that barely covers the cost of living.

In every case, the ability to pay the IRS is wiped out by circumstances far beyond the taxpayer's control. It's crucial to remember that CNC status is a temporary fix for these situations. If you think you might be able to pay a smaller, settled amount, it might be worth exploring how to qualify for an Offer in Compromise as another option for resolving your tax debt for good.

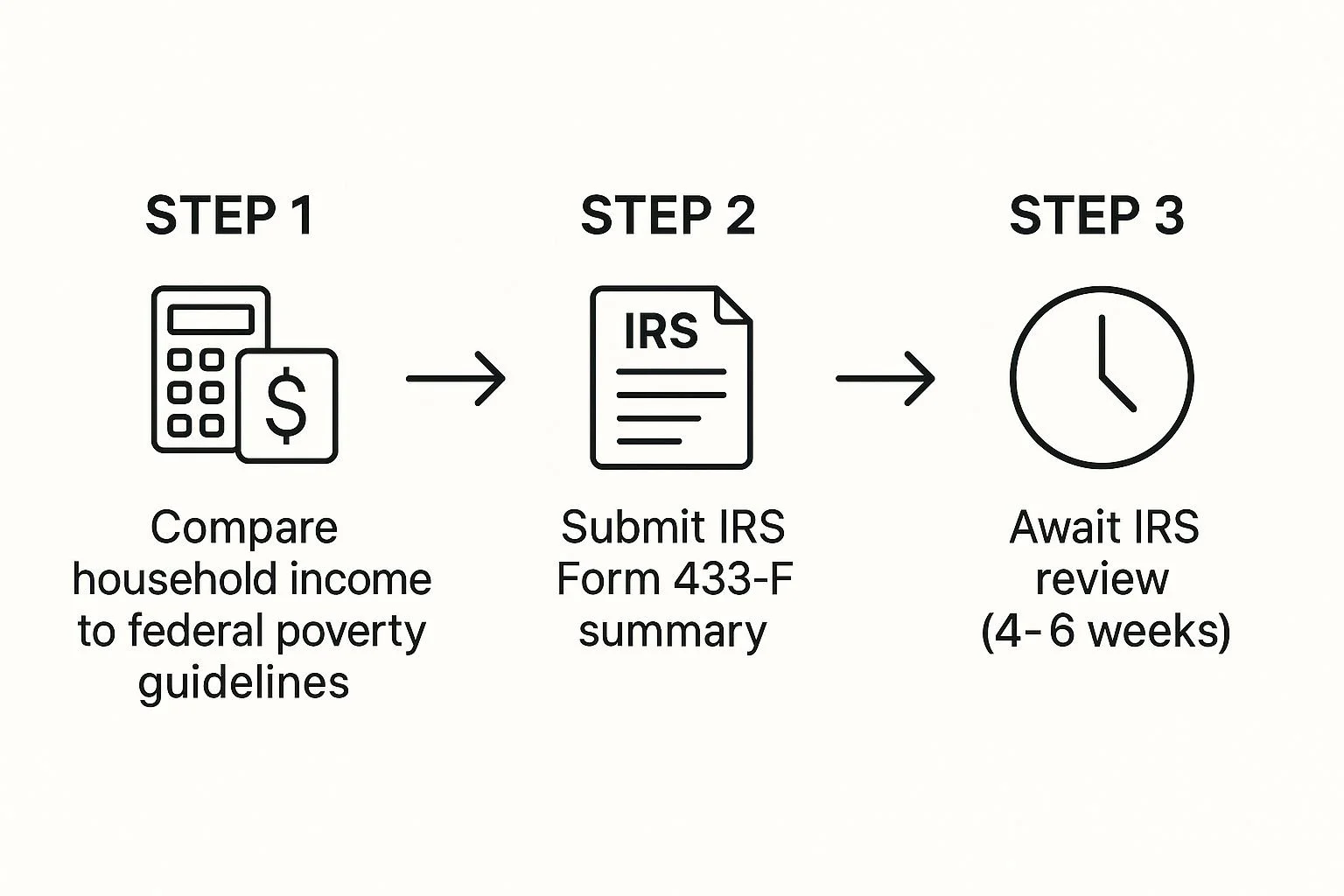

Your Step-by-Step Guide to Requesting CNC Status

So, how do you actually get the IRS to grant you non collectible status? It might feel like an impossible mountain to climb, but there's a clear path forward. It all starts with being proactive and having an honest conversation with the IRS, backed by solid proof.

The very first move is picking up the phone. Find the number on your most recent IRS collection notice and call them. When you get an agent on the line, you’ll need to clearly state that you’re requesting to be placed in Currently Not Collectible (CNC) status because of financial hardship.

This phone call isn't just a formality—it’s where you start laying the groundwork. You don't need to tell your whole life story, but be ready to give a quick, honest summary of why you can't pay. Maybe you lost your job, or maybe you’re buried in medical bills. The agent will then point you to the next step, which almost always involves one critical piece of paperwork.

The Cornerstone of Your Request: Form 433-F

Everything—and I mean everything—rides on Form 433-F, the Collection Information Statement. This is the document where you lay all your financial cards on the table for the IRS. It gives them a detailed snapshot of your life: what you earn, what you spend just to live, and what you own. It’s the single most important tool they use to decide if you genuinely can’t afford to pay.

Think of it this way: Form 433-F is the foundation of your entire case. If that foundation is shaky or has holes, the whole thing comes crashing down.

Here’s a simple visual of how the process flows.

As you can see, it's a straightforward path: you assess your financial reality, submit the form to prove it, and then await the IRS's decision.

Gathering Your Financial Documentation

To fill out Form 433-F with the level of detail the IRS demands, you’ll need to gather a stack of documents. This isn’t the time for guesswork; you need to prove every number you write down. The agent might give you a specific list, but getting a head start on collecting these will make everything go much smoother:

Proof of Income: Your last 3-6 months of pay stubs are a must. Also, grab any Social Security statements or records of other income sources.

Bank Statements: You'll need the last 3-6 months of statements for every single bank account you have, both checking and savings.

Housing Expenses: Get your mortgage or rent statements, recent property tax bills, and your homeowners' insurance policy.

Utility Bills: Pull together your most recent bills for gas, electricity, water, and phone service.

Transportation Costs: Find your car payment or lease statements, insurance cards, and be ready to estimate your monthly fuel and maintenance costs.

Other Essential Expenses: This includes things like health insurance premiums, significant medical bills, or any court-ordered payments you make, like alimony or child support.

Having all this paperwork organized and ready to go does two things. First, it makes filling out the form a whole lot easier. Second, it signals to the IRS that you’re taking this seriously. A well-documented, organized case always has a better shot at approval.

Completing and Submitting the Form

When you sit down with Form 433-F, be meticulous. Go slow. Double-check every single number you enter. Even a small, innocent mistake or a forgotten expense can cause major delays or even get your request for IRS non collectible status flat-out denied.

Once you’re confident the form is perfect, you’ll send it to the IRS agent handling your case along with copies of all your supporting documents. Don’t be surprised if the agent comes back with a few follow-up questions—that’s a normal part of their review process.

What to Expect During the IRS Interview

The final piece of the puzzle is usually a detailed phone call with the IRS agent or revenue officer. They will walk through your Form 433-F with you, line by line, asking you to confirm the information and explain anything that looks unusual.

The agent's goal is simple: they want to be absolutely sure your financial picture is accurate and that you truly don't have the means to pay your tax debt. Throughout this conversation, your job is to be honest, consistent, and patient. Just answer the questions directly.

After the interview, the agent will make their decision. If they approve your request, you’ll get an official letter in the mail confirming you’ve been placed in CNC status. It's a huge relief, but remember, it’s often a temporary fix. For a more permanent resolution, it's worth exploring all your options.

Weighing the Pros and Cons of Non Collectible Status

Getting the IRS to agree to non collectible status feels like a huge weight has been lifted. It's a critical step with some very real benefits, but it’s definitely not a "get out of jail free" card. Think of it less like a magic wand that erases your tax debt and more like hitting the pause button on a very stressful situation.

Before you jump in, it’s crucial to understand the full picture—what you gain, what you give up, and what it means for you down the road. This isn’t just about stopping the scary letters; it’s about weighing immediate relief against future financial realities. Let's break down both sides of the coin.

The Powerful Advantages of CNC Status

The single biggest, most immediate benefit of Currently Not Collectible (CNC) status is the cessation of aggressive IRS collection actions. That constant knot in your stomach from threatening letters, non-stop phone calls, and the very real fear of seeing your bank account emptied overnight? It stops.

This gives you invaluable breathing room. The most significant benefits include:

An End to Levies and Garnishments: The IRS will immediately stop taking money from your bank accounts or paychecks. This means your income can go toward essentials like rent and groceries without you fearing it will disappear.

Protection of Your Assets: With collections on hold, your property and other assets are temporarily safe from being seized to pay your tax bill.

A Chance to Regain Stability: This break from the pressure gives you time to figure things out. You can focus on finding a new job, dealing with a family crisis, or simply getting your finances in order without the IRS breathing down your neck.

For so many people I've worked with, the mental and emotional relief is just as important as the financial side. Stopping the collection machine lifts an incredible burden, allowing you to finally focus on rebuilding.

The Significant Downsides and Realities

While the relief is very real, the drawbacks of IRS non collectible status are just as serious and need to be understood. The most common mistake people make is thinking the problem is solved. It isn't—it's just on hold.

Here's the first hard truth: your tax debt is still growing. Even though the IRS isn't actively collecting, interest and penalties keep piling up on your unpaid balance. That $50,000 you owe could easily balloon to $60,000 or more while you're in CNC status, digging you into an even deeper hole.

On top of that, you can say goodbye to any tax refunds. The IRS will automatically snatch any future refunds you’re entitled to and apply them to your debt. This is called a refund offset, and you won't see a dime of that money until the tax bill is paid in full.

Evaluating the Benefits and Drawbacks of CNC Status

Seeing the trade-offs side-by-side can make the decision much clearer. CNC status is a temporary fix, and its short-term benefits come with some heavy long-term costs.

| Pros of CNC Status | Cons of CNC Status |

|---|---|

| Immediately stops wage garnishments and bank levies. | Tax debt continues to grow with interest and penalties. |

| Halts stressful and aggressive IRS collection calls. | The IRS will seize all future tax refunds. |

| Provides time to stabilize your financial situation. | The status is temporary and subject to periodic review. |

| Protects assets from immediate seizure by the IRS. | The IRS can still file a Notice of Federal Tax Lien. |

| Offers critical peace of mind and reduces stress. | Does not stop the 10-year collection statute from running. |

Finally, and this is a big one, CNC status is not permanent. The IRS will check up on you, usually every one to two years. If your income has gone up, they’ll pull you out of the program and expect you to start paying again. It's a temporary hold, not a permanent solution.

Life After the IRS Grants Non Collectible Status

Getting that letter in the mail confirming your IRS non collectible status is a huge weight off your shoulders. The constant, aggressive collection calls stop. The scary-looking notices disappear from your mailbox. For the first time in a long time, you can actually breathe.

But this isn't the finish line. Think of it more like a ceasefire. The active battle is on hold, but the underlying issue—your tax debt—is still there. This is your chance to regroup, and you need to use this time wisely. If you don't, you could find yourself right back in the IRS's crosshairs.

Understanding the Ten Year Clock

One of the most important concepts you need to know about is the Collection Statute Expiration Date (CSED). It’s basically the IRS's deadline. By law, they typically get 10 years from the date your tax was assessed to collect what you owe.

Here's the good news: being in non-collectible status doesn't pause this clock. It keeps ticking. Every single day you're in CNC is another day closer to that 10-year limit. If the CSED arrives before the IRS has collected the debt, it's legally gone forever.

While some people have their tax debt expire while they're in CNC status, you shouldn't bank on it as your main strategy. Your real focus should be on getting your finances back in order for a more permanent solution.

The IRS Review Process

Currently Not Collectible status is temporary, not a "set it and forget it" deal. The IRS will be checking in on you periodically to see if your financial picture has improved. This review usually happens every 18 to 24 months.

Most of the time, this is an automated process. The IRS computer system flags your account for review, often triggered by the income you report on your latest tax return. If it sees your income has jumped up, you can bet they'll be in touch to see if you can start paying again. This is exactly why you must keep up with your tax filings.

Triggers That Can Revoke Your CNC Status

A few different things can knock you out of non-collectible status and put you right back on the collections list. You need to know what these triggers are so you can stay protected for as long as you genuinely need to be.

Here are the main ones:

A Big Jump in Income: This is the most common trigger by far. Landing a new job, getting a fat raise, or receiving a large bonus tells the IRS you might have enough money to start a payment plan.

Forgetting to File Future Tax Returns: This is a non-starter. You absolutely must file all your federal tax returns on time, every single year. It doesn't matter if you can't afford to pay what you owe on that new return—you still have to file it.

Getting a Major Asset: Suddenly coming into a large inheritance, hitting the lottery, or making a big profit from selling a house will definitely get the IRS's attention and likely lead to them revoking your CNC status.

This "grace period" is your opportunity to do more than just lie low. It's time to create a solid budget, cut back on unnecessary spending, and maybe even start stashing away a small emergency fund. If you can build better financial habits now, you'll be in a much stronger position to negotiate a final solution, like an installment agreement, once your income recovers.

Common Questions About IRS Non Collectible Status

When you're trying to navigate IRS non collectible status, a lot of questions pop up. It’s only natural. Getting the details straight is crucial for managing your expectations and making this temporary relief work for you. Let's walk through some of the most common questions I hear from taxpayers.

How Long Does This Status Last?

This is usually the first thing people ask. The simple answer is: there's no set expiration date. It's not like a program that runs for a specific number of months or years and then just stops.

Instead, the status holds as long as your financial hardship does. The IRS will check in on you periodically—usually every 1 to 2 years—to see if your income has improved enough to start making payments again. If it has, they'll move to take you out of the program.

Does Non Collectible Status Erase Tax Debt?

This is a big one, and a very common misunderstanding. Let me be clear: CNC status does not make your tax debt disappear. It only hits the pause button on active collection efforts from the IRS.

Think of it as the IRS calling a timeout, not forfeiting the game.

Your original tax bill is still there, and worse, it keeps growing. Interest and penalties continue to pile up the entire time you're in CNC status.

That means the total amount you owe will actually be higher when you eventually come out of the program. For a better look at long-term fixes, you can explore other tax debt solutions that may be available to you.

Can the IRS Still File a Tax Lien?

Yes, they absolutely can. This catches a lot of people by surprise. Even though the IRS agrees to stop aggressive collection tactics like garnishing your wages or levying your bank account, they reserve the right to file a Notice of Federal Tax Lien against your property.

A tax lien is a public claim against your assets that secures the government's interest in what you owe. It can wreck your credit score and make it incredibly difficult to sell property or get a loan, even while you're technically in IRS non collectible status.

This is exactly why CNC should be seen as a temporary bridge to a more permanent fix, like an Offer in Compromise. Just to give you an idea, in fiscal year 2024, the IRS accepted about 21% of these offers, settling $163.4 million in debt. This shows how different relief options work together. You can dig into the numbers on IRS collection activities and statistics on their website.

Dealing with the IRS is complex, and getting your account placed in non-collectible status requires careful documentation and negotiation. At Attorney Stephen A Weisberg, I start with a FREE Tax Debt Analysis to determine the best path forward for your specific situation.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034