What Is State Tax Levy? Learn How It Affects Your Finances

When the state government talks about taking your property to cover an unpaid tax bill, they're talking about a state tax levy. It's one of the most serious collection tools they have.

While a tax lien is simply a legal claim against your property, a tax levy is the state actively seizing it. It’s how the government forcibly collects what it's owed, and it can happen directly from your bank accounts, paychecks, or other valuable assets.

Decoding the State Tax Levy

Think of a tax lien as a public warning sign the state places on your property. It tells potential creditors that you have a tax debt, securing the government's place in line if you sell. It's a serious black mark on your credit, but at that moment, you don't lose anything.

A state tax levy, on the other hand, is when the hammer comes down. It’s the consequence. If the lien was the warning shot, the levy is the state exercising its legal authority to take what you own to settle the score.

This isn't an action that comes out of the blue; it's usually the final step after a series of notices and payment demands have gone unanswered.

The Critical Difference Between a Lien and a Levy

Getting this distinction straight is absolutely vital if you're facing a tax debt. People mix them up all the time, but they are worlds apart in terms of immediate impact. A lien is a claim. A levy is a seizure.

A tax lien secures the government's interest in your property when you have a tax debt. A tax levy actually takes the property to satisfy the tax debt. Think of it this way: a lien is a claim, while a levy is an enforcement action.

To make this crystal clear, let’s break down the key differences between these two powerful state collection tools.

State Tax Levy vs State Tax Lien at a Glance

| Aspect | State Tax Lien | State Tax Levy |

|---|---|---|

| What it is | A legal claim against your property. | The actual seizure of your property. |

| Impact on Property | Secures the state's interest; you still own it. | The state takes possession of the asset. |

| Purpose | To act as a public notice of debt. | To satisfy the tax debt by taking assets. |

| Analogy | A "warning sign" on your property. | The "hammer coming down." |

| Timing | Typically the first step in collections. | A later, more aggressive enforcement step. |

Hopefully, this table helps you see just how different these actions are. A lien clouds your title and credit, but a levy can empty your bank account overnight.

What Can a State Actually Seize?

State tax agencies have incredibly broad powers to levy assets. The specific rules and what's exempt can vary from state to state, but their reach is extensive. Don't underestimate it.

Here are the most common targets:

Wages and Salary: This is a big one. The state can order your employer to send a chunk of your paycheck directly to them before you ever see it. Most people know this as wage garnishment.

Bank Accounts: They can hit your checking and savings accounts, often freezing everything and taking the balance up to the amount of your debt. It's a sudden and jarring experience.

Personal Property: Your car, boat, or other valuable items aren't safe. The state can seize and sell them.

Real Estate: Yes, they can even take your home or other properties you own, though this is often a last resort.

The sheer power of a levy is why you can never afford to ignore a state tax debt. It can throw your entire financial life into chaos without warning, which makes understanding the process and your rights absolutely essential.

The Road to a State Tax Levy

Let’s be clear: a state tax levy doesn’t just happen overnight. It’s the final, and most serious, move in a long game of collection efforts by the state. Think of it less like a surprise attack and more like the inevitable end of a well-telegraphed journey.

Knowing the stops along the way is your best defense because each one is a chance to get off the train before it crashes. It all starts innocently enough with a tax bill. Maybe you underpaid, made a mistake on your return, or just didn't file one at all. If you don't pay that first bill, the state’s collection machine kicks into a higher gear.

That’s when the letters start arriving. The first one might feel like a simple reminder, but don't be fooled. Each subsequent notice gets more intense, with the language shifting from a polite request to an iron-clad demand for payment. They’ll spell out exactly what you owe in taxes, plus all the penalties and interest that are piling up.

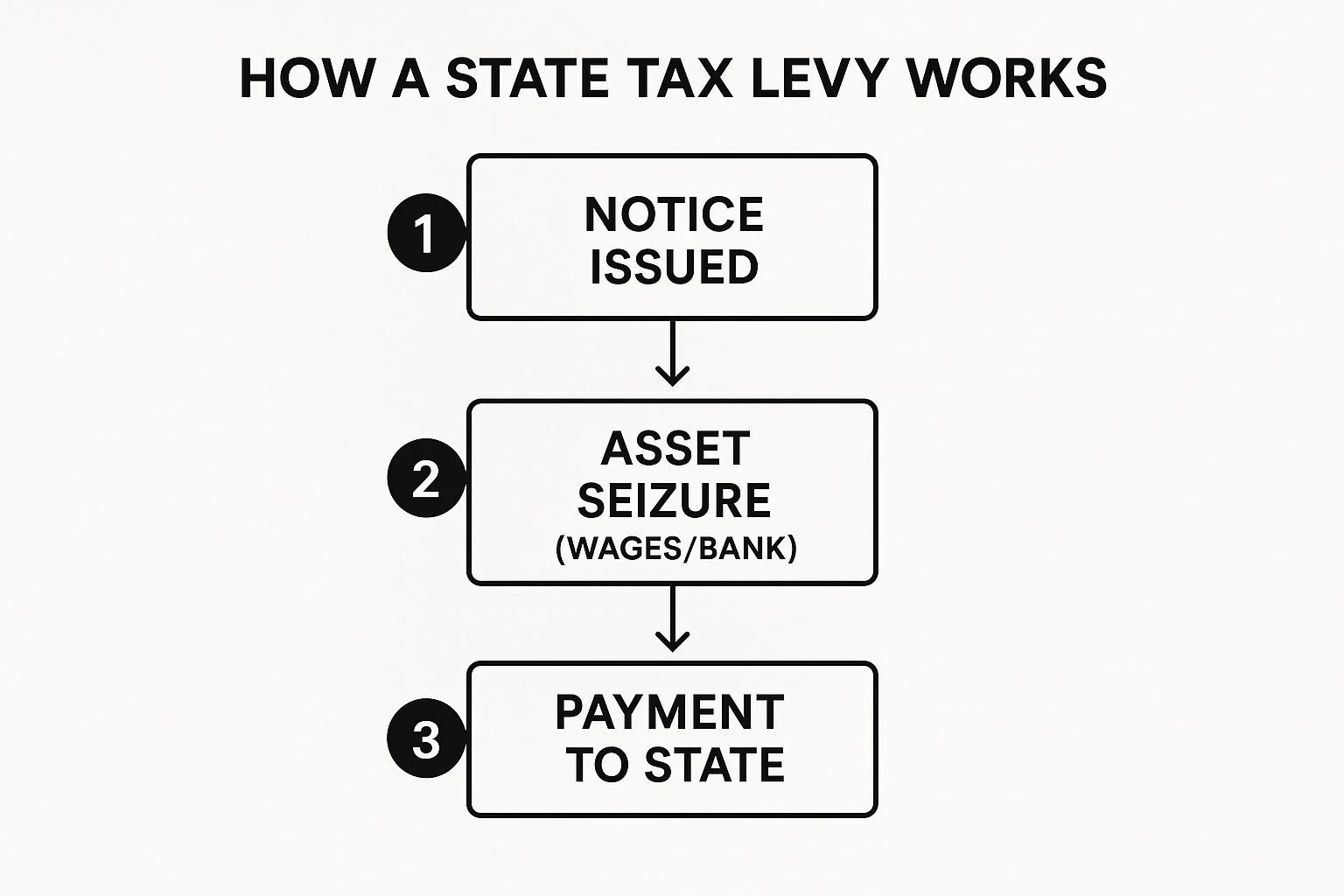

The Final Warning: Notice of Intent to Levy

Out of all the mail you'll get, one letter stands above the rest in importance: the Notice of Intent to Levy. This is the state's final warning shot across the bow. It’s an official, legally binding document that says, "We have the right to seize your property, and we will if you don't pay up or contact us to make other arrangements."

You typically have 30 days to act from the moment you receive this notice.

Ignoring it is the single biggest mistake you can make. Once that 30-day window slams shut without you taking action, the state has the green light. They are now legally free to go directly to your employer, your bank, or anyone else holding your assets and start taking what they're owed.

This flow chart breaks down the simple, powerful mechanics of what happens when that final notice is ignored.

As you can see, once the state has sent the required legal notices, the path leads straight to them seizing your assets to settle the debt.

How Do People End Up Here?

No one plans to fall behind on their taxes. More often than not, it's life that gets in the way. People from all walks of life find themselves in this situation, and it's important to remember that state tax agencies have seen it all before. They often have programs in place to help people dealing with genuine hardship.

Some of the most common reasons we see include:

Sudden Financial Hardship: A job loss, a serious medical diagnosis, or a divorce can blow a hole in anyone's finances, making it impossible to cover a tax bill.

Business Cash Flow Issues: If you're a small business owner or freelancer, you know the drill. A client pays late, or a slow season hits, and suddenly the money set aside for taxes has to go to payroll or rent.

Disputes Over the Tax Bill: Sometimes, you might genuinely believe the state got the numbers wrong. The critical thing to remember is that you can't just ignore the bill; you have to formally dispute the assessment through the proper channels.

A levy is almost always the result of a breakdown in communication. By the time a bank account is frozen or wages are garnished, there have been multiple letters and multiple chances to fix the problem. The very first step back is to open the lines of communication.

Knowing these warning signs and understanding the path to a levy gives you power. The key is to never, ever ignore the notices—especially that Final Notice of Intent to Levy. Acting on it is your last best chance to resolve the issue before the state takes control.

Protecting Your Assets and Knowing Your Rights

That official-looking levy notice from the state can feel like a knockout punch. It’s designed to get your attention, and it definitely does. But it’s not the end of the story. You have rights, and state laws provide a crucial window to defend yourself and protect your most essential assets from being seized.

The single most important right you have is the right to appeal. When you get a "Notice of Intent to Levy," the clock starts ticking. You usually have a strict deadline, often just 30 days, to request a hearing. This isn't just a bureaucratic step; it’s your chance to get in front of someone, argue your case, and find a resolution before they start taking your property.

What Assets Are Exempt from a State Tax Levy

While the state has broad powers to collect, they can't leave you with nothing. The law recognizes that taking every last penny would be counterproductive and create extreme hardship. Because of this, certain assets and income streams are legally off-limits.

Here’s a general idea of what’s usually protected:

A Portion of Your Wages: The state can’t take your whole paycheck. A legally protected amount, which often depends on your filing status and how many dependents you have, is yours to keep for basic living costs.

Certain Government Benefits: Money from Social Security, unemployment, disability, and some veterans' benefits is typically shielded from state tax levies.

Essential Personal Property: States won't take the shirt off your back. They generally exempt necessary items like essential clothing, school books, and a certain value in furniture and household goods.

Workers' Compensation: If you're receiving payments for a workplace injury, that money is usually safe from seizure.

It's vital to remember that a state tax levy is a powerful fiscal tool used to enforce compliance. State tax levies are a key part of how states collect revenue, a system that varies widely in its impact across different income levels. Learn more about how state tax systems affect taxpayers from the Institute on Taxation and Economic Policy.

Taking The Right Steps to Protect Yourself

Knowing your rights is one thing; using them is what truly matters. The best defense is a good offense, and that means ensuring your taxes are filed accurately and on time to begin with. Getting help from professional tax preparation services can prevent these headaches before they even start.

It's also critical to understand that a levy is not the same as a lien. They are two different enforcement actions that require completely different strategies.

Actionable Strategies to Resolve a State Tax Levy

Staring down a state tax levy is a heavy burden, no doubt about it. But it’s a situation you can absolutely work your way out of. After the initial shock wears off, it's time to shift your energy from worrying about the problem to actively finding the solution.

The good news is that state tax agencies have established paths to help you get back on track.

The absolute worst thing you can do is nothing. Ignoring the problem won't make it disappear; it just invites more aggressive collection actions. The single most important first step is to open a line of communication with the tax agency. By getting in front of it, you can start exploring options that work for both you and the state.

Negotiate a Payment Plan

For a lot of folks, the clearest path forward is setting up an Installment Agreement. Think of it as a formal payment plan where you agree to chip away at your tax debt with consistent, manageable monthly payments.

Who It's For: This is perfect for taxpayers who can't pay the full bill right now but have enough income to make steady payments over an extended period.

How It Works: You'll need to open up your books and provide financial details to the state. They need to see what you can realistically afford. Based on that, they'll set a payment amount and schedule.

Outcome: Once it's in place, the levy gets lifted. As long as you stick to the plan and make your payments on time, the state will halt all other collection efforts.

The state won’t even consider a payment plan unless all your past-due tax returns are filed. They need a complete picture of what you owe before they can make a deal.

Getting compliant is non-negotiable. If you have unfiled returns hanging over your head, check out our guide on how to file back taxes to get that critical first step squared away.

Settle Your Tax Debt for Less

What if a payment plan is still out of reach? If your financial hardship is severe, you might be a candidate for an Offer in Compromise (OIC). An OIC is a powerful tool that allows you to settle your tax debt for less—sometimes much less—than the full amount you owe.

This isn't a get-out-of-jail-free card, though. States are very particular about who qualifies. They'll only accept an OIC if they're convinced there's little to no chance they could ever collect the full debt. You'll have to prove you're in a tough spot financially.

Request Currently Not Collectible Status

In the most extreme cases—think sudden unemployment, a serious medical crisis, or other debilitating circumstances—you can ask to be placed in Currently Not Collectible (CNC) status.

If approved, the state puts a temporary freeze on all collection activities, including levies. It’s important to understand this isn't a permanent fix. The debt is still there. The state will check in on your financial situation periodically, and if things improve, collections will start back up.

To help you see how these options stack up, here’s a quick comparison.

Comparing Tax Debt Resolution Options

| Resolution Method | Best For... | Key Requirement | Potential Outcome |

|---|---|---|---|

| Installment Agreement | Taxpayers with steady income who need time to pay off their debt. | Proving you can afford consistent monthly payments. | Levy is lifted; you pay off the full debt over time. |

| Offer in Compromise (OIC) | Taxpayers facing severe financial hardship with no foreseeable way to pay the full debt. | Demonstrating significant financial distress and inability to pay. | The state accepts a lower amount as full payment of your tax liability. |

| Currently Not Collectible (CNC) | Individuals with extreme financial hardship (e.g., unemployment, illness). | Proving your current income doesn't cover basic living expenses. | Collection activities are paused temporarily until your financial situation improves. |

Each path has its own set of requirements and outcomes, but the common thread is taking action. By understanding what’s available, you can find the right strategy to put this tax problem behind you for good.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034