Non Collectible Status IRS: Real Relief for Tax Hardship

Understanding Non Collectible Status: Your Financial Lifeline

Feeling buried under a mountain of tax debt can be incredibly stressful. The constant stream of intimidating letters and the threat of having your wages garnished or bank accounts seized can leave you feeling trapped.

During these tough times, the non collectible status IRS program offers a crucial break. Officially called Currently Not Collectible (CNC), this isn't a secret loophole but a sensible acknowledgment from the IRS that making you pay right now would cause you severe financial distress.

Think of it as the IRS hitting a "pause" button on its collection efforts. It’s a formal recognition that you simply can't afford to pay your tax bill at this moment without sacrificing your basic needs. This pause gives you the essential breathing room to get your finances in order.

What Is Currently Not Collectible Status?

Imagine you're in a boxing match with the IRS, and you’re on the ropes. CNC status is like your corner throwing in the towel for a temporary timeout.

The IRS agrees that your current income and assets aren't enough to cover your essential living expenses and your tax payments. It’s important to understand this is not debt forgiveness—the tax debt doesn't disappear.

Instead, the IRS "Currently Not Collectible" (CNC) status is a designation that temporarily stops aggressive collection actions like wage garnishments, bank levies, or seizing property.

This status is granted when a taxpayer proves they cannot afford to pay their tax debt without experiencing significant economic hardship. You can read more on the official IRS website about how they temporarily delay the collection process.

While interest and penalties will continue to accumulate on your balance, the halt in active collection can be a game-changer, giving you the space to find financial stability.

How Does This Protection Actually Work?

Once the IRS places your account in CNC status, the collection machine comes to a standstill. The menacing letters will stop, the phone calls will end, and the immediate danger of a levy on your bank account or paycheck is lifted.

This protection is granted after a thorough review of your financial life, which you'll document on forms like the IRS Form 433-F, Collection Information Statement.

The guiding principle here is simple: the IRS understands that pushing someone into complete financial ruin is not productive. For example, consider a single parent who recently lost their job and is facing growing medical expenses.

The IRS would look at their income (or lack thereof) compared to necessary living costs—rent, food, healthcare—and see that there is no disposable income left to pay taxes.

This process provides a vital safety net during a crisis, allowing you the time to recover. For those facing this challenging situation, you can get more details in our complete guide on the Currently Not Collectible IRS program.

Who Actually Qualifies: Beyond Financial Stress

Getting approved for the IRS's Currently Not Collectible (CNC) status is about more than just having a tough month financially. The IRS needs to see a clear line between temporary money troubles and a genuine economic hardship that makes paying your tax debt impossible without sacrificing basic needs.

Think of it this way: it’s not about having an empty bank account, but about proving that any payment to the IRS would mean you couldn't afford rent, food, or essential medical care.

To figure this out, an IRS agent essentially becomes a financial investigator. They’ll review your complete financial situation, often using Form 433-F (Collection Information Statement), to determine your reasonable collection potential (RCP).

This isn't a measure of your total debt; it's a snapshot of your ability to pay based on your monthly cash flow and any assets you could liquidate.

The IRS Financial Hardship Calculation

The IRS uses a specific formula to gauge your hardship. They take your total monthly income and subtract a standardized amount for allowable living expenses.

These are figures the IRS has determined are reasonable for costs like housing, food, transportation, and healthcare, based on national and local averages. If your actual expenses are higher than these standards, the burden is on you to prove they are absolutely necessary.

For instance, consider a retiree whose only income is $2,200 a month from Social Security. Their essential living costs—mortgage, utilities, and groceries—add up to $2,100. On top of that, they have $200 in non-negotiable monthly prescription costs.

Their total necessary expenses are $2,300, which means they are already $100 short each month. In a case like this, the IRS would likely determine there's no disposable income to collect, making the retiree a prime candidate for CNC status.

To help you understand what the IRS considers essential, the table below breaks down the types of expenses they review.

| Expense Category | Allowable/Required | IRS Guidelines | Special Considerations |

|---|---|---|---|

| Housing & Utilities | Allowable | Based on local standards for mortgage or rent. Includes electricity, gas, water, etc. | Costs significantly above local averages require strong justification. |

| Food & Clothing | Allowable | Based on national standards, adjusted for family size. | Costs for specialized diets or work uniforms may be considered with proof. |

| Transportation | Allowable | Covers one or two vehicles for work/health. Includes car payments and operating costs. | Luxury car payments are not allowed. Public transport costs are based on actual expenses. |

| Health Care | Allowable | Premiums, out-of-pocket costs (copays, prescriptions), and dental/vision care. | All medical expenses must be documented. Ongoing treatment costs are factored in. |

| Court-Ordered Payments | Required | Child support, alimony, or other legally mandated payments. | These are almost always allowed as they are legally required. |

| Discretionary Spending | Non-Allowable | Vacations, entertainment, private school tuition, expensive dining, savings contributions. | The IRS does not consider these necessary for basic living. |

This table shows the clear distinction the IRS makes: expenses for survival are considered, while costs related to lifestyle choices are not.

Necessary vs. Discretionary Spending

The IRS draws a firm line in the sand between what’s essential and what’s a luxury. They will accept reasonable costs for housing and a basic vehicle, but they won't approve payments that support a high-end lifestyle.

Here’s a quick breakdown:

Allowed expenses typically include your mortgage or rent (as long as it fits local standards), modest car payments, groceries, utilities, health insurance, and any court-ordered payments.

Disallowed expenses are things like expensive car leases, tuition for private schools, contributions to vacation funds, or a habit of dining at pricey restaurants.

Context is also critical. A single parent dealing with a child's sudden medical crisis or a small business owner on the verge of closing up shop has a much more compelling hardship case than someone whose financial strain comes from overspending on non-essentials.

Your success hinges on your ability to document that every dollar you earn is already spoken for by legitimate, necessary living costs.

Navigating The Application Process Like A Pro

Getting approved for non-collectible status with the IRS is less about simply completing a form and more about presenting a clear, honest picture of your financial hardship.

The application is your opportunity to show that paying your tax debt right now is impossible without giving up your basic living essentials. The whole process relies on total transparency and careful documentation.

The main tool you'll use is the IRS Collection Information Statement. While the IRS might sometimes request the shorter Form 433-F, you'll most likely be filling out Form 433-A if you're an individual or Form 433-B for a business.

Don't think of this as a simple questionnaire; it's the foundation of your financial story. Every single number must be supported by proof.

Assembling Your Application Package

Before you write a single thing on the form, gather all your supporting documents. This preparation is the key difference between a successful application and one that gets stuck in a cycle of information requests. A well-prepared package should include:

Proof of Income: Pay stubs, Social Security statements, or profit-and-loss statements from the last three to six months.

Proof of Expenses: Bank statements, canceled checks, utility bills, mortgage or rent statements, and receipts for necessary costs like medical care.

Asset Information: Statements for all bank accounts and retirement funds, plus valuations for any vehicles or real estate you own. If you tried to get a loan to pay your tax bill and were denied, include the rejection letters—they provide strong evidence of your situation.

Your goal is to create a detailed picture that leaves no room for questions. Accuracy is everything; any inconsistencies between your form and your bank statements will raise immediate red flags for the IRS agent reviewing your case.

Choosing Your Communication Channel

How you submit your request can also influence the outcome. You typically have three main choices:

By Phone: For straightforward cases, you might be able to request CNC status over the phone with an IRS agent. This is often the quickest way but offers less opportunity for detailed explanations.

By Mail: Sending a written request allows you to include a cover letter that explains your personal circumstances, along with your Form 433 and all the documents. This method creates a complete and official record of your request.

With a Revenue Officer: If your case is more complicated or the debt is significant, you may be assigned a Revenue Officer. This means you'll have direct meetings to present your case.

After you submit your application, the IRS review can take anywhere from several weeks to a few months. Expect follow-up questions and be ready to respond promptly and professionally.

If your request is denied at first, don't lose hope. You have the right to appeal, and sometimes a different approach is all that's required. To explore all your options, you can learn more about how to negotiate IRS debt and find the best path forward.

Living With CNC Status: The Good And The Reality Check

Getting approval for non collectible status irs brings immediate and palpable relief. Imagine a sudden quiet after a long, loud storm; the threatening letters stop arriving, the fear of a bank account levy or wage garnishment fades, and you finally have the mental space to get your finances in order. This peace of mind is the most significant benefit of CNC status.

However, this is not a permanent "get out of jail free" card. Think of it more like a temporary truce with the IRS, not a final peace treaty. To maintain this status, you have some important ongoing duties.

The Ongoing Responsibilities of CNC

While the IRS has paused collections, they are still monitoring your situation. Here’s what you must do to keep your account in good standing:

File Future Taxes on Time: This is non-negotiable. You are required to file all future tax returns when they are due. A late filing is one of the quickest ways for the IRS to cancel your CNC status and restart collection actions.

Say Goodbye to Tax Refunds: Any future tax refunds you might be owed will be automatically taken by the IRS and put toward your old tax debt. It's a smart move to adjust your payroll withholdings to get closer to a $0 refund, so you aren't overpaying throughout the year just to have it seized.

Expect Financial Check-Ins: The IRS will periodically review your financial health, typically every one to two years. If your income goes up substantially or your essential living expenses go down, they may decide you can now afford to pay. If that happens, they will remove you from the CNC program.

The Statute of Limitations Clock

A crucial factor to understand is the Collection Statute Expiration Date (CSED). This is the 10-year countdown the IRS legally has to collect a tax debt.

One of the most powerful aspects of the non collectible status irs program is that this 10-year clock continues to tick even while your account is on hold.

This means it’s possible for the statute of limitations to run out completely while you are in CNC status. If that happens, the tax debt is essentially erased forever. You can find more details about how this process works on Choice Tax Relief's website.

Ultimately, CNC status is a lifeline that gives you a much-needed break from aggressive collection efforts. The key is to stay compliant with tax laws and be ready for financial reviews to hold onto this important protection.

Choosing Your Best Path: CNC Vs Other Relief Options

Achieving non-collectible status from the IRS is a powerful solution when you genuinely lack the means to pay your tax debt. However, it’s not the only way forward.

Understanding the full landscape of relief options is crucial for making the best decision for your long-term financial stability. Think of CNC status as hitting the "pause" button on collections, while other programs offer structured paths to resolving your debt.

For taxpayers who have some reliable income or assets, other programs might be a more suitable fit. An Offer in Compromise (OIC) lets you settle your tax liability for a lower amount than what you originally owed, while an Installment Agreement (IA) creates a predictable monthly payment plan.

Offer in Compromise (OIC) vs. CNC

An OIC is built for individuals who can pay a portion of their debt, either in a lump sum or over a short period. Its main benefit is finality—once the IRS accepts your offer and you pay it, the debt is gone for good. In sharp contrast, CNC status is for those who cannot afford any payment right now due to severe financial hardship.

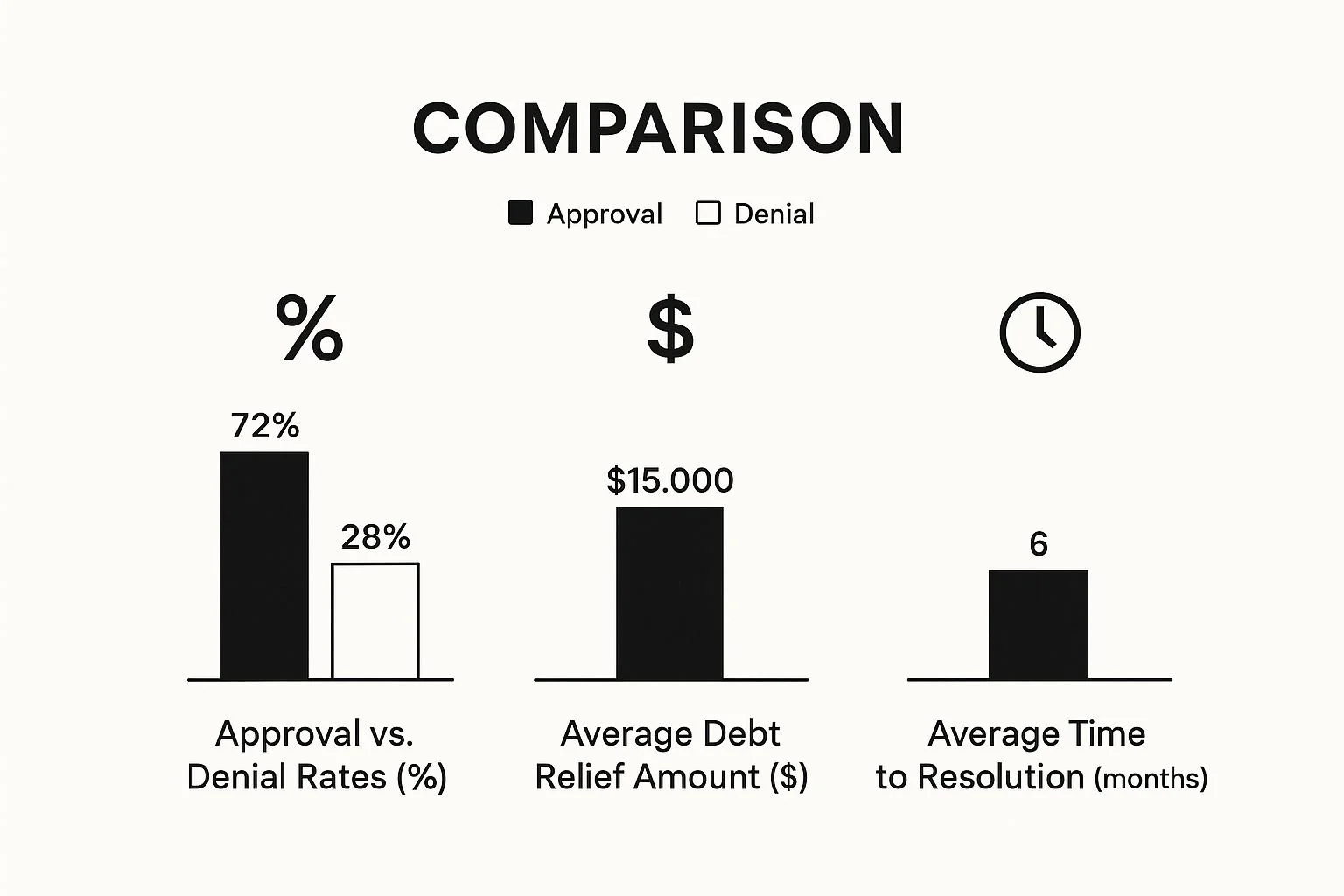

During Fiscal Year 2024, taxpayers submitted 33,591 offers, and the IRS accepted 7,199 of them, settling $163.4 million in tax debt. These numbers, available in the IRS's official collection activity statistics, show that while an OIC isn't guaranteed, it's a viable tool for those in the right circumstances.

Installment Agreements vs. CNC

If you can afford to make consistent monthly payments, an Installment Agreement is often the most direct route. It's an excellent choice for people with a steady income who simply need to spread out their tax payments over time.

The primary advantage here is predictability, which makes budgeting much easier. If your income is too low or unstable to commit to any regular payment, CNC remains the better option.

To help you see how these programs stack up, here's a side-by-side look at the key differences.

| Relief Option | Eligibility Requirements | Application Process | Debt Impact | Best For |

|---|---|---|---|---|

| Currently Not Collectible (CNC) | Severe financial hardship; income is less than or equal to allowable living expenses. No ability to pay. | Submit Form 433-A, 433-B, or 433-F with detailed financial information. | Pauses collection activity. Debt remains and accrues interest/penalties. Status is temporary and reviewed periodically. | Individuals with no disposable income or assets who need immediate relief from collections. |

| Offer in Compromise (OIC) | Doubt as to collectibility (can't pay in full), doubt as to liability, or effective tax administration. | Submit Form 656 and Form 433-A/B. Requires a detailed financial analysis and an offer payment. | Settles the entire tax debt for less than the full amount owed. Provides a permanent resolution. | Taxpayers who can afford a partial payment (lump sum or short-term) to resolve their debt permanently. |

| Installment Agreement (IA) | Must have filed all required returns and owe a combined total of under $50,000. | Can often be set up online, by phone, or by submitting Form 9465. Less intensive than OIC/CNC. | Allows you to pay the full debt over time (up to 72 months). Interest and penalties continue to accrue. | People with a steady income who can afford consistent monthly payments to chip away at their debt. |

As the table shows, each program serves a different purpose. An OIC offers a permanent fresh start, an IA provides a manageable payment structure, and CNC delivers a temporary but essential reprieve.

This infographic breaks down the success rates and resolution times for these key tax relief programs.

The data highlights that while an Offer in Compromise can provide substantial debt relief, the approval process is selective, whereas CNC status focuses purely on immediate financial hardship.

Strategically, sometimes applying for CNC status first can be a smart move. It stops collections and gives you breathing room to stabilize your finances, which might better position you to qualify for an OIC down the road.

Ultimately, the right choice depends entirely on your specific financial situation. To explore these options further, you can find more information in our guide to identifying the ideal tax debt solution.

Avoiding Costly Mistakes That Kill Your Application

Getting approved for non-collectible status from the IRS is a careful procedure where even minor oversights can lead to major setbacks. Taxpayers facing genuine financial struggles can find their applications rejected because of mistakes that could have been avoided. Successfully managing this process involves more than just filling out a form; it requires accuracy, consistency, and a solid grasp of the IRS's expectations.

Incomplete or Inconsistent Financials

The most frequent reason for a denial is submitting financial information that is either incomplete or inconsistent. Treat your application, especially Form 433, like a sworn statement.

Every single number you list must be supported by evidence. If your bank records show consistent payments for a storage unit you forgot to list as an asset or expense, an IRS agent will immediately see that as a problem.

Hiding assets or income is a fatal error. The IRS has powerful data-matching systems and will uncover discrepancies. Honesty and thoroughness are your best approach; full disclosure is key.

Common Misconceptions to Avoid

Many taxpayers make critical errors based on myths about the Currently Not Collectible (CNC) program. It's vital to understand the facts:

CNC is not a permanent solution: The IRS will typically re-evaluate your financial standing every one to two years. If your income goes up, they will remove the status and start collections again.

You must continue filing your taxes: A fundamental condition for keeping CNC status is to file all future tax returns on time and pay any new taxes you owe. If you don't, your status will be canceled immediately.

Don't ignore IRS mail: When the IRS asks for more information, a lack of response is often seen as an attempt to avoid them, which can result in a quick denial. Always reply quickly and make sure the agency has your current contact details.

Poor Documentation and Follow-Up

The strength of your hardship claim depends entirely on your proof. It’s not enough to just say you have high medical bills; you must supply receipts, insurance EOBs, and doctors' statements. If you claim high transportation costs for a long work commute, provide a map and a clear explanation.

Every claim needs detailed documentation. For those looking into different relief options, our guide on the broader IRS tax forgiveness program offers a look at various solutions and what they require.

In the end, a successful application tells a believable and well-documented story of financial hardship. By sidestepping these common errors, you present your case in the best way possible and greatly improve your odds of getting approved.

Building Your Recovery Plan While Protected

Getting the IRS to grant you non collectible status is a huge relief, but what you do next is just as important. Think of this period as a protected workshop for your finances.

Instead of seeing it as a break from your problems, view it as a unique opportunity to rebuild your financial footing without the pressure of active collections. It’s your chance to transform temporary relief into lasting stability.

This rebuilding phase requires a careful touch. Your goal is to strengthen your financial position without making moves that might alarm the IRS and cause them to re-examine your status. The focus should be on creating solid financial habits, not on acquiring new wealth overnight.

Smart Steps for Financial Recovery

While your account is in CNC status, it's best to focus on actions that have a high impact but a low profile. This isn't the right time to make large investments or buy flashy assets. Instead, direct your energy toward these practical steps:

Build a Modest Emergency Fund: Gradually set aside a small amount of money for genuine emergencies, like an unexpected car repair or medical expense. This demonstrates financial responsibility to the IRS, showing you’re planning ahead rather than hiding assets.

Carefully Rebuild Credit: Start making consistent, on-time payments for all your current obligations. You might also consider a secured credit card to begin repairing your credit score, which will be vital for your financial health later on.

Stay Current on New Taxes: This is non-negotiable. You must file all future tax returns on time and pay any new taxes you owe in full. Failing to do so is the quickest way to have your CNC status revoked.

Planning for the Long Term

Your non-collectible status is not permanent; the IRS will typically review your finances every one or two years. A key part of your long-term plan involves the 10-year Collection Statute Expiration Date (CSED).

This is the legal window the IRS has to collect your back taxes. A major advantage of CNC status is that this 10-year clock keeps ticking, and it's possible for the statute to run out, which would wipe out your old tax debt for good.

To stay on track, create a simple budget based on the necessary living expenses allowed by the IRS. If your income goes up, you need to be ready to report it. A small increase, perhaps from a part-time job, might not change anything, but a significant pay raise almost certainly will.

Working with a tax professional can help you understand these financial lines and make choices that support both your immediate recovery and your future financial security.

Managing CNC status while building a plan for the future can feel overwhelming. If you could use professional guidance to map out your recovery, consider a Free Tax Debt Analysis to learn how expert help can protect your financial well-being.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034