What Are Bank Levies? A Clear & Simple Explanation

Understanding What Are Bank Levies: The Financial Tool That Changed Banking

When you hear the word "levy," your mind probably jumps to a government action to seize assets for unpaid taxes—a stressful situation for anyone.

If you've received a notice from the IRS, it's important to know your next steps, and you can find a breakdown of the process in our ultimate guide to understanding a notice of levy. But in the world of high finance, a bank levy means something entirely different. It's not about taking money from a taxpayer's account; it's a specific tax placed directly on banks.

Think of it like car insurance companies offering discounts to safe drivers. Those discounts encourage responsible behavior on the road. A bank levy operates on a similar principle.

It’s a specialized financial tool meant to encourage banks to run their operations more safely by influencing how they get their funding. Instead of relying on high-risk, short-term borrowing, bank levies push institutions to use more dependable funding sources, such as customer deposits and their own capital.

This makes a bank levy fundamentally different from the standard corporate income tax, which is simply a tax on profits. A bank levy is designed to shape behavior for a more stable financial system.

Why Did Bank Levies Emerge?

The story behind the modern bank levy starts with the 2008 global financial crisis. The spectacular failure of major financial institutions highlighted a critical weakness: many banks were dangerously over-leveraged, meaning they had borrowed far more money than they had in their own capital.

When the market soured, they couldn't pay their debts, which triggered a domino effect of failures and led to taxpayer-funded bailouts costing billions.

In the aftermath, governments needed a way to prevent this from happening again. They introduced bank levies as a proactive measure to make the banking system stronger.

The central idea was to make risky borrowing more expensive for banks, nudging them toward safer, more sustainable ways of doing business. This marked a major shift in financial regulation, moving from merely reacting to crises to actively trying to prevent them.

Key Components of a Bank Levy System

A bank levy isn't a simple, one-size-fits-all tax. It's carefully designed to target specific parts of a bank's balance sheet. The key components usually include:

The Tax Base: This is what gets taxed. It often includes a bank's liabilities, like wholesale debt and other types of borrowing. More stable funding sources, such as insured customer deposits and shareholder equity, are typically exempt.

The Tax Rate: This is the percentage charged. It can be a single flat rate or a tiered system where riskier borrowing is taxed at a higher rate. This structure directly incentivizes safer financial choices.

This method has become a popular regulatory tool, especially in Europe. Its main goal is to reduce a bank's leverage—the ratio of its debt to its assets. By discouraging reliance on wholesale debt, these levies encourage banks to hold more retail deposits and equity, which are considered much more stable. A major study of nearly 3,000 banks across 27 EU countries confirmed that these levies work, effectively influencing leverage ratios. You can dive into the research and learn more about how European bank levies reduce leverage.

From Financial Crisis to Policy Solution: The Story Behind Bank Levies

Bank levies weren't created in a vacuum; they were born from the chaos of one of the most severe financial disasters of our time. The 2008 global financial crisis revealed a major weakness in the world's banking system.

Many of the largest banks were heavily reliant on borrowed money and held incredibly risky assets. When the housing market buckled, these institutions faced devastating losses they simply couldn't absorb, setting off a domino effect that nearly collapsed the global economy and led to massive, taxpayer-funded bailouts.

After the dust settled, policymakers were left with a pressing question: how can we stop this from happening again? The solution was to change how banks behave by adjusting the financial incentives. Think of it like a restaurant that keeps using risky, cheap ingredients that might make people sick.

A bank levy acts as a special tax on those specific ingredients, making it more expensive to cut corners and encouraging the use of safer, better supplies. For banks, this meant making their riskiest types of funding more costly.

Crafting a New Form of Accountability

This new way of thinking led to the bank levy as a policy tool. Governments needed a mechanism to make sure banks contributed to the stability of the very system they profited from and to hold them responsible for the risks they introduce. The goal was to build a protective financial cushion before another crisis could hit.

This represented a major change from reacting to disasters to proactively managing financial health. It's a different concept entirely from an individual's tax troubles, where mechanisms like an Offer in Compromise can provide a path to tax debt settlement.

The First Bank Levies Take Shape

The United Kingdom was a frontrunner in this movement, introducing its own policy to manage these system-wide risks. The UK bank levy first appeared in 2011, creating an annual charge on certain liabilities and equity shown on the balance sheets of banks and building societies.

This tax was specifically designed to target items like outstanding loans and specific kinds of debt these institutions held, and it applied to all banks operating in the UK. You can explore the specifics of the UK's bank levy framework to get a more detailed look at its structure.

How a Bank Levy Actually Works: Decoding the Financial Mechanics

To get what a bank levy is, you have to look under the hood at its moving parts. Think of it like a car insurance premium; it’s not a random number but a figure calculated based on specifics like your driving record and car model.

In the same way, a bank levy isn't a simple, flat tax. It's a carefully designed financial tool meant to steer a bank's behavior by targeting its funding.

The whole thing kicks off when a creditor, often a government tax agency like the IRS, wins a legal judgment against you for an unpaid debt. This judgment grants the creditor the right to go after your assets, including any money you have in a bank account. Once that legal authority is set, the creditor can start the levy process.

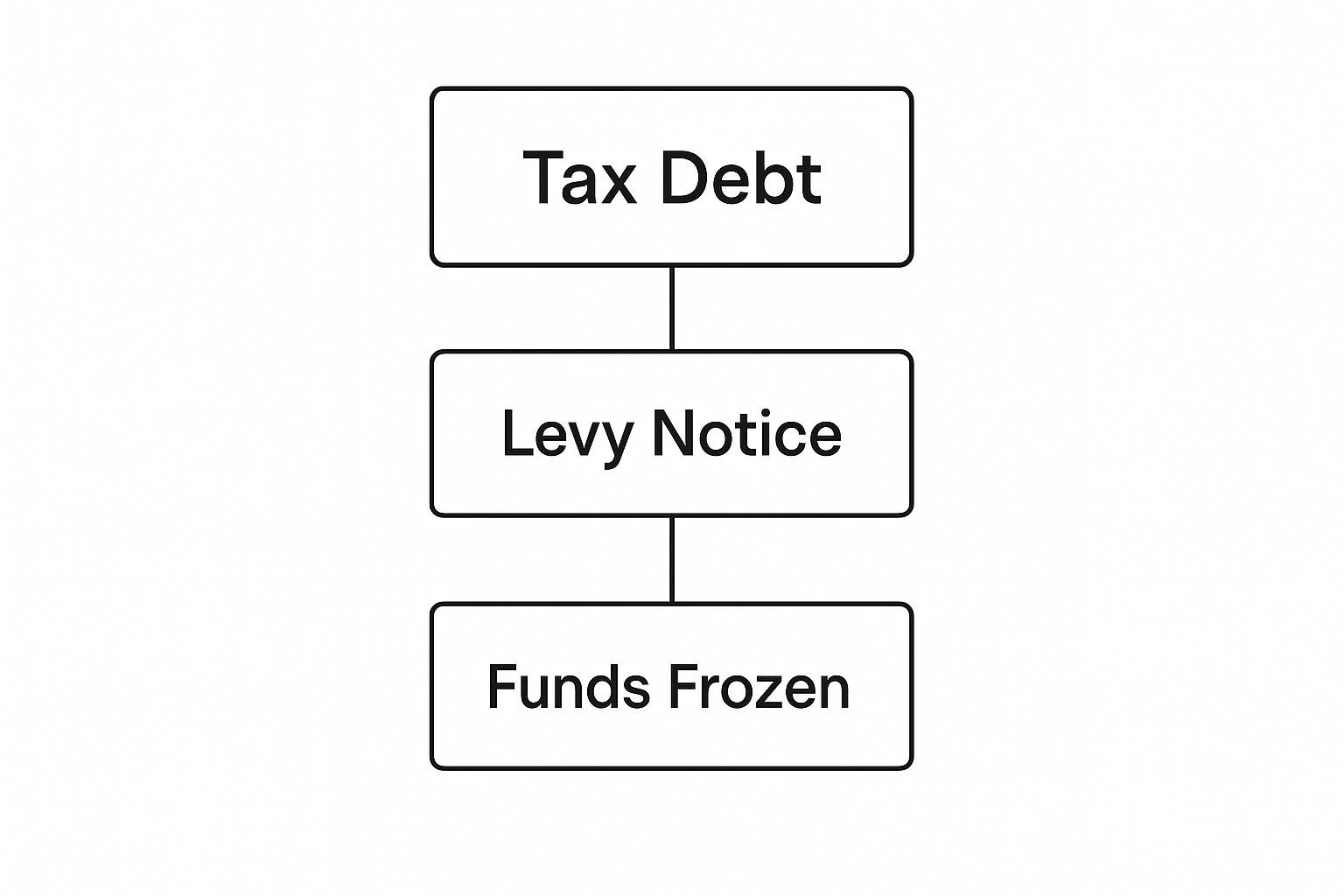

This infographic lays out the direct sequence of events once an unpaid tax debt triggers collection actions.

As the visual shows, an initial tax debt can lead straight to your bank funds being frozen once a levy notice is issued.

The Mechanics of Seizure

Once a creditor decides to make a move, the mechanics are surprisingly direct and potent. The process generally plays out in a few distinct stages:

Issuing the Notice of Levy: The creditor sends a formal legal document, the Notice of Levy, to the bank where you have an account. This notice isn't a polite request; it's a legal order that forces the bank to act. The IRS recently resumed sending these automated notices, highlighting their role in the collection process.

Freezing the Account: As soon as the bank gets the notice, it's legally required to freeze your account. This freeze is immediate. The bank identifies the available funds at that precise moment, up to the amount specified in the levy, and locks them down. For instance, if you owe $5,000 and have $6,500 in your account, the bank will freeze $5,000 of it.

The 21-Day Hold Period: After your funds are frozen, the bank must hold onto them for a mandatory 21-day period. This isn't just a bank policy but a legal requirement. It acts as a critical window for you to take action—either by paying the debt in full, negotiating a resolution, or proving the levy was a mistake. This holding period is your last chance to fix the problem before the money is gone for good.

Transferring the Funds: If you don't resolve the debt within those 21 days, the bank is legally required to send the frozen funds directly to the creditor. At this stage, the levy is complete, and your money has been officially seized to satisfy the debt.

Global Approaches: How Different Countries Tackle Banking Taxation

While the idea of a bank levy is straightforward, how it's applied varies greatly from one country to another. Imagine it like a set of local traffic laws. Every town needs rules for driving, but the specific speed limits, parking rules, and one-way streets are designed for that town's unique road system.

In the same way, each nation customizes its banking tax rules to fit its economic goals, the structure of its financial system, and its top priorities. This creates a fascinating patchwork of systems, all providing a different answer to the question of what are bank levies in the real world.

The United Kingdom, an early adopter of this policy, offers a great case study. Its bank levy is based on a bank's total liabilities, but the government has tweaked the formula over the years. The goal is to find a balance between raising revenue and ensuring London remains a competitive global financial hub.

The UK's journey shows that these tax policies aren't set in stone; they are active documents that evolve based on economic performance and changing market conditions.

Different Systems, Different Targets

A look at different national strategies reveals the strategic thinking behind them. A crucial choice is what, exactly, to tax—the tax base. Some countries cast a wide net, while others perform more like a surgeon, targeting very specific activities.

For example, Germany focuses its levy on off-balance-sheet derivatives while completely exempting customer deposits. This sends a clear message: the government wants to discourage complex, risky financial products without punishing the everyday banking services funded by stable public savings.

This is a stark contrast to other European approaches. Since 2009, over 15 European Union countries have introduced bank levies, each with its own unique design. Most systems protect financial stability by exempting core equity and insured deposits, but their primary targets differ.

Hungary: Applies its levy to a bank's total assets.

France: Bases its calculation on a bank's minimum regulatory capital.

This diversity demonstrates that there isn't one "correct" way to implement a levy; the structure reflects each country's specific economic philosophy. You can discover more about the diverse designs of European bank levies to see how these systems are constructed.

Rate Structures and Revenue Goals

Another key point of difference is the tax rate. Some countries choose a simple flat rate, applying the same percentage to all financial institutions above a certain size. This method is easy to administer but doesn't necessarily account for the different levels of risk taken by each bank.

In contrast, other nations have set up progressive or tiered rate structures. In these systems, the tax rate climbs based on the perceived riskiness of a bank's funding sources.

For instance, a bank that relies heavily on short-term, less stable wholesale funding might face a higher levy than one funded mainly by long-term deposits from customers.

This approach directly nudges banks toward safer choices by making riskier behavior more expensive, effectively using the tax code as a regulatory tool to promote financial stability.

Real-World Impact: What Bank Levies Mean for Everyone

Think about what happens when a new toll is placed on a busy highway. It’s not just the drivers paying the fee who feel the change. Side streets get more congested, delivery routes for local businesses change, and it can even affect where people decide to buy a home.

A bank levy works in a similar way, creating ripples that spread far beyond a bank’s balance sheet. It touches businesses, consumers, and the entire competitive landscape. Knowing what are bank levies in theory is important, but seeing their practical consequences shows the full story.

The immediate fear was that banks would simply pass the cost of the levy on to customers through higher account fees or steeper interest rates on loans.

The reality, however, turned out to be more nuanced. While some costs were certainly passed along, many banks also changed their internal strategies to soften the levy’s impact. This has sparked a clear shift in how they fund their day-to-day operations.

Many institutions now focus on attracting more stable funding sources, like deposits from individuals and businesses, which are often exempt from the levy calculation. This strategic move, directly driven by the levy's design, has arguably made the banking system more resilient.

The Ripple Effect on Lending and Services

This change in funding has real-world consequences for the economy. By prioritizing stable deposits, banks might become more careful with their lending. On the one hand, this helps create the safer financial system that policymakers intended. On the other hand, it could make it more challenging for small businesses and startups to get the credit they need, as they are often seen as higher-risk borrowers.

The levy has also changed the competitive dynamics among banks. Institutions that already relied heavily on customer deposits found themselves with a natural advantage, while those dependent on wholesale funding had to quickly adapt their models.

Some unintended consequences also surfaced. For instance, initial rules sometimes placed an unfair burden on smaller community banks, which led to revised regulations and targeted exemptions.

Ultimately, these policies are a delicate balancing act. The goal is to make banking safer and ensure that financial institutions contribute to the stable system they benefit from.

At the same time, regulators must keep a close watch on how these policies affect credit availability and consumer costs to keep the system both secure and accessible.

While a bank levy is a tool for systemic financial health, individuals facing personal tax debt have different tools available. To understand these options better, you can explore our smart guide on how to settle IRS debt for actionable insights.

The Data Behind the Impact

Looking at the numbers helps paint a clearer picture of how these policies have played out. The following table highlights the revenue generated by bank levies in several countries and provides a snapshot of their economic significance.

Bank Levy Revenue and Economic Impact Statistics: Key financial data showing revenue generated by bank levies and their economic significance across different countries

| Country | Annual Revenue (Billions) | % of Total Tax Revenue | Per Household Impact | Implementation Year |

|---|---|---|---|---|

| United Kingdom | Approx. £2.5 | ~0.3% | ~£90 | 2011 |

| Germany | Approx. €1.2 | ~0.15% | ~€30 | 2011 |

| France | Approx. €0.7 | ~0.06% | ~€24 | 2011 |

| Sweden | Approx. SEK 6 | ~0.25% | ~SEK 1200 | 2018 |

This data shows that while bank levies generate substantial revenue, their direct percentage of total tax income remains relatively small. However, the per-household impact demonstrates how these national policies translate into tangible economic figures for everyday citizens.

Measuring Success: Do Bank Levies Actually Deliver Results?

Bank levies have been a key part of financial regulation for over a decade, giving us enough time to step back and ask a simple question: did they work? Think of it like a city installing a new traffic light at a dangerous intersection.

A year later, you’d check the accident reports to see if the change made the crossing safer. In the same way, we can now look at studies and real-world results to see if these taxes successfully lowered banking risks and strengthened the financial system.

The central question is whether these levies actually changed how banks operate. The evidence suggests they did, though the story has some important complexities.

The main objective was to discourage banks from relying on risky, short-term debt and instead push them toward more stable funding sources, such as customer deposits and their own capital.

Data reveals a clear shift in this direction. Banks in jurisdictions with levies have, on average, adjusted their funding models, which marks a significant win for the policy.

Analyzing Leverage Ratios and Funding Shifts

One of the most important yardsticks for success is a bank's leverage ratio, which is a simple comparison of its debt to its equity. Generally, a lower ratio signals a safer, more stable institution. A body of research consistently shows that bank levies have a direct effect on these ratios.

The chart below, from a study on European banks, highlights the statistical link between bank levies and leverage, demonstrating a tangible impact.

This data confirms that levies serve as a counterbalance to tax rules that might otherwise encourage taking on more debt. They effectively nudge banks to hold more of their own capital, which is a vital part of building a more durable financial system.

However, gauging success isn't always so clear-cut. It’s challenging to separate the effects of the levy from other post-crisis regulations, like increased capital requirements. These policies often work in tandem, making it difficult to give credit for improved stability to just one measure.

Additionally, some banks have found clever accounting methods to reduce their levy payments without truly changing their risk-taking behavior, exposing a weakness in the current systems.

While these financial tools focus on institutional stability, individuals facing their own tax challenges have different options. You can explore a personal tax debt solution to understand the paths available for handling individual tax liabilities.

Ultimately, the most effective bank levies seem to be those integrated into a wider regulatory strategy. They aren't a magic fix, but they have proven to be a useful tool for promoting safer banking practices and encouraging lasting behavioral change.

The data shows they have an effect, but they work best when combined with thorough financial oversight.

The Future of Banking Taxation: What's Coming Next

The world of finance is in constant motion, and the regulations that govern it must adapt to keep pace. Understanding what are bank levies today is only half the story; the real question is how they will evolve to meet future challenges.

Think of it like city planners constantly updating traffic laws to manage new forms of transportation, from electric bikes to autonomous vehicles. In the same way, financial regulators are actively shaping the future of banking taxation to address a changing financial system.

A major force behind this evolution is the growth of digital banking and fintech. These new market entrants are changing how we move and manage money, introducing both new possibilities and potential risks that weren't on the radar when the first bank levies were created.

This has sparked a crucial debate among policymakers: should these levies be extended to cover new kinds of financial companies, and if so, how?

Proposed Reforms and Emerging Trends

International cooperation is becoming more important than ever. As finance becomes increasingly global, mismatched tax rules between countries can create loopholes and unfair advantages. Efforts are now focused on developing more consistent approaches to prevent banks from shifting their riskiest operations to countries with more relaxed regulations.

At the same time, governments are tweaking the systems they already have. For instance, recent UK law allows regulators to recapitalize a failing small bank by imposing special levies on the rest of the industry. This is a direct lesson from past financial crises, aimed at protecting the system without needing a public bailout. The key areas of discussion include:

Expanding the Tax Base: Debates are ongoing about whether to apply levies to new financial products or non-bank institutions that perform bank-like functions.

Refining Rate Structures: Policymakers are looking into more dynamic rate systems that can adjust based on a bank's real-time risk profile, rather than a static snapshot.

Enhancing Resolution Tools: New rules are being developed to ensure that when a bank fails, the financial industry, not the taxpayers, bears the cost.

With over a decade of data to draw from, a clearer picture of what works is emerging. We've learned that levies are most effective when they are combined with strong capital requirements and watchful oversight. The future of banking taxation isn't about finding a single silver bullet, but about the steady, intelligent refinement of the tools we already have.

Managing complex financial rules is tough, whether you're a multinational bank or a small business owner dealing with the IRS. If you're struggling with tax debt, you don't have to figure it out alone. I offer a FREE Tax Debt Analysis to assess your situation and identify the best way forward before you make any commitment.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034