Responding to IRS Letter: Your Essential Guide

That official-looking envelope from the IRS in your mailbox is enough to make anyone’s heart skip a beat. But before you let your mind race, take a breath. The first and most important step is simple: don't panic.

Just open the letter calmly and look for the notice number, which is usually in the top-right corner. This little code is the key to understanding exactly what the IRS is asking for.

Why Did the IRS Send Me a Letter?

An IRS notice isn't automatically a sign that you're in trouble. Honestly, it's usually just a routine, computer-generated communication. Think about it—the IRS processed over 266.6 million tax documents in a recent fiscal year. Automated checks are the only way to manage that kind of volume.

Most of the time, a letter simply means:

You might have a balance due.

Your refund is going to be larger or smaller than you expected.

The IRS has a question about something on your tax return.

They need to verify it’s really you.

They need a bit more information to process your return.

The IRS made a change to your return.

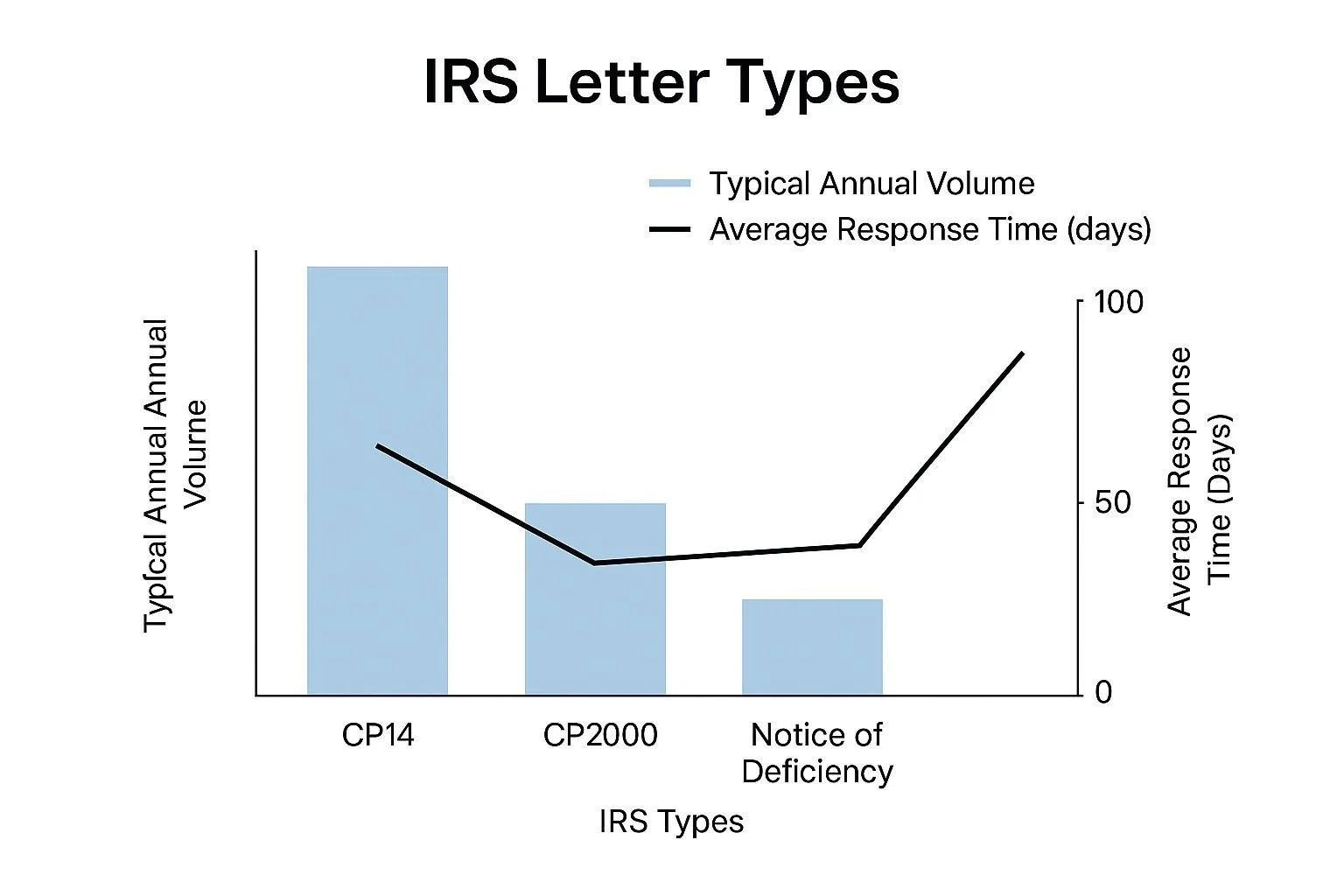

That notice number is your Rosetta Stone. For instance, a CP2000 notice suggests changes to your return because the information they received from a third party, like your employer or bank, doesn't quite match what you filed.

On the other hand, a CP14 is more straightforward—it’s a notice telling you that you owe money on unpaid taxes.

To help you quickly figure out what your letter is about, I've put together a quick reference table.

Common IRS Notices and What They Mean

| Letter/Notice Code | Common Reason | What You Should Do Next |

|---|---|---|

| CP14 | You owe taxes. | Pay the balance by the due date or set up a payment plan. |

| CP2000 | Discrepancy between your return and third-party info (e.g., W-2, 1099). | Review the proposed changes. Agree or provide documentation to dispute them. |

| LTR 3219N | Notice of Deficiency; the IRS plans to assess more tax. | You have 90 days to petition the U.S. Tax Court. This is a critical deadline. |

| CP504 | Intent to Levy; a final warning before the IRS seizes assets. | Contact the IRS immediately to arrange payment or dispute the debt. |

| CP05 | Your refund is under review and has been delayed. | Wait for the review to complete or for a request for more information. Do not refile. |

This table covers some of the most frequent notices, but remember to read your specific letter carefully for details and deadlines.

Understanding Urgency and Timelines

Not all notices carry the same weight. Some are simple requests for information, while others have strict, unmovable deadlines.

As you can see, a Notice of Deficiency is far less common, but it comes with a non-negotiable 90-day deadline for you to take action in Tax Court. This highlights its serious nature. Ignoring any of these communications is a terrible strategy that will only make things worse.

A common mistake I see is people disregarding a notice, hoping it’s just an error that will fix itself. But in my experience, inaction only escalates the issue, sometimes leading to serious collection actions like liens or levies. If things have already gotten to that point, understanding how to remove a tax lien becomes your top priority.

Gathering the Right Documents for Your Response

Once you know why the IRS is contacting you, it's time to build your case. Think of it like a puzzle. You need to find the exact document that fits the specific hole the IRS has pointed out. This isn't the time to dump a shoebox of receipts on their desk.

For example, if the notice is questioning your reported income, you can’t just send a generic "proof of income" letter. You need to pull the specific forms that address the discrepancy.

This could mean providing:

A copy of your Form W-2 from your employer.

The Form 1099-NEC or 1099-K you received for freelance or gig work.

Bank statements that clearly show direct deposits matching the income you claimed.

The same logic applies if the IRS is challenging a deduction. Vague claims get denied. Concrete proof is what gets issues resolved.

Matching Evidence to the IRS Inquiry

Let's say the IRS is asking about your business mileage deduction. Just telling them you drove for work is a non-starter. You need to provide a detailed mileage log.

I'm talking about a log showing the date, where you started, where you went, the business reason for the trip, and the total miles. The more organized you are, the easier you make it for the agent to sign off on your deduction.

Here's a pro tip from years of experience: create a simple cover sheet. List every document you're including and write a brief sentence explaining how it proves a specific point from the IRS notice. This single step makes the reviewer's job infinitely easier and immediately shows you’re organized and serious.

Having good record-keeping habits year-round makes this whole process much less painful. You might want to look into effective knowledge management strategies to keep your financial life in order for the future. And remember: never send originals. Always send copies and keep the originals safely in your files.

If you’re a taxpayer living abroad, I know communication can feel daunting. The good news is the IRS has dedicated international call centers and mailing addresses to help.

Keep in mind that mail response times can be around 10 to 12 working days, so you’ll need to factor that into your planning. This preparation is a critical part of getting your IRS letter handled correctly.

How to Write a Clear and Effective Response Letter

When you sit down to write your response, remember that this letter becomes your official statement. Clarity and professionalism are your best friends here.

It's tempting to get emotional, but I've seen it backfire time and again. Stick to the facts. The agent reading your letter isn't looking for a dramatic story; they just need a straightforward explanation.

Start your letter by getting right to the point. Skip the long-winded intro and immediately identify yourself and the specific issue.

At the very top of your letter, make sure you include this crucial header information:

Your full name and current address

Your Social Security Number (SSN) or Individual Taxpayer Identification Number (ITIN)

The tax year or period in question (e.g., Tax Year 2023)

The notice number (like CP2000) and the date from the letter you received

Getting this right from the start helps the IRS pull your file quickly and saves everyone a headache.

Structuring Your Response

The best way to structure your letter is to address each point from the IRS notice one by one. For every single item the IRS has questioned, you need to state clearly whether you agree, disagree, or partially agree. Right after that, provide a brief, factual explanation.

For example, let's say the notice claims you have unreported income from a Form 1099-K. A good response would be something like: "I disagree with the proposed change regarding unreported income.

The amount shown on the Form 1099-K includes non-taxable transactions, and I have enclosed a reconciliation statement and bank records to support this."

The goal is to make it incredibly easy for the IRS agent to follow your logic. You want to present your explanation and point to your supporting documents in a way that guides them directly to the conclusion you want them to reach.

Now, if you realize you do owe money and can't pay it all at once, you have options. It’s worth learning how to negotiate IRS debt to find a path forward. In these situations, your ability to communicate clearly is paramount. Brushing up on general effective communication strategies can be a huge help.

Finally, wrap it up with a simple, professional closing. Sign it, and you're ready to get it in the mail.

Submitting Your Response and Confirming Receipt

You’ve put in the hard work to draft a solid response and gather your documents. Now comes the final, crucial step: getting it into the hands of the IRS. How you send your package is just as important as what’s inside—do it right, and you prevent your efforts from disappearing into a bureaucratic black hole.

First things first, check the mailing address printed directly on your IRS notice. Don't just glance at it; double-check it. The IRS is a massive organization with different departments handling different issues. Sending your response to the wrong one is a surefire way to cause major delays.

The Certified Mail Rule: This Is Non-Negotiable

I tell every client this: always, always send your response package using USPS Certified Mail with a return receipt. This isn't just a suggestion; it's a critical part of protecting yourself.

This service gives you a tracking number and, more importantly, a legal record proving the exact date the IRS received your correspondence. That little green postcard you get back in the mail is your golden ticket—irrefutable proof of delivery. File it away with your other tax records. If the IRS ever claims they never got your response, this receipt is your defense.

After you’ve sent your response, the waiting game begins. The IRS can take 60 to 90 days or even longer to reply. This is normal. Having your certified mail receipt gives you peace of mind during this period, knowing you’ve fulfilled your obligation.

Following Up and Checking Your Status

While patience is a virtue when dealing with the IRS, you don't have to wait in complete silence forever. If a few months go by with no word, it's reasonable to follow up.

Thankfully, the dreaded phone call to the IRS has gotten a lot better. Recent improvements have slashed wait times on their main phone lines from an average of 28 minutes down to just 3 minutes.

This makes checking on your case's status a much more manageable task. You can read more about these IRS customer service improvements on treasury.gov.

And if the IRS eventually comes back with a decision that isn't in your favor? Don't panic. You still have options. The next step is to understand how to appeal an IRS decision.

When You Should Call a Tax Professional

Look, a lot of IRS letters are straightforward. You might get one asking for a missing form or pointing out a simple math mistake. Those are usually things you can handle on your own without too much stress.

But some envelopes from the IRS carry a lot more weight. These are the ones that signal it’s time to stop what you're doing and call in a professional—someone like an Enrolled Agent (EA) or a CPA who deals with this stuff day in and day out. It's about knowing when the stakes are just too high to go it alone.

So, where’s that line? It’s when the complexity of the issue or the potential financial hit feels bigger than you're comfortable managing.

Situations That Demand Professional Help

Let's be clear: certain IRS notices aren't just letters; they're serious procedural or legal moves. Trying to navigate them without experience is like walking into a courtroom without a lawyer.

You should get an expert involved immediately in these scenarios:

You get a formal audit notice. This isn't a simple document check; it's a deep dive into your entire financial life.

The amount of money at stake is significant. If the tax, penalties, and interest could genuinely hurt you financially, you need professional backup.

The IRS accuses you of negligence or fraud. These are incredibly serious allegations with severe penalties. You need an advocate who understands your rights inside and out.

You're completely overwhelmed. Honestly, if the letter is confusing or the stress is just too much, a pro can lift that burden and bring immediate clarity.

A good tax professional does more than just fill out paperwork. They speak the IRS's language and know the unwritten rules of the game. Having them on your side sends a clear message to the IRS: you're taking this seriously and you have competent representation.

If your tax debt feels insurmountable, a professional can also guide you through complex relief options. For example, they can help you figure out how to qualify for an Offer in Compromise, a settlement process that’s notoriously tough to navigate solo.

Think of hiring an expert as an investment in protecting your financial future.

Burning Questions About IRS Notices

Even with a solid game plan, it's natural for a few "what ifs" to pop into your head when dealing with the IRS. Let's tackle some of the most common questions I hear from clients to help you feel more confident about your next steps.

What Happens If I Ignore an IRS Letter?

I can't stress this enough: doing nothing is the absolute worst move you can make. Ignoring an IRS notice won't make the problem vanish—it guarantees it will snowball.

At first, the IRS might just file a "substitute return" on your behalf, which almost never includes the deductions and credits you deserve.

From there, things can escalate quickly to aggressive collection actions like putting a federal tax lien on your home, garnishing your wages, or levying your bank account. Always, always respond, even if it's just to ask for more time.

How Long Do I Have to Respond?

Most IRS notices give you a 30-day window, but don't assume that's always the case. The specific deadline will be printed right on the letter, usually on the first page.

Pro Tip: The second you open that envelope, find the due date and immediately put it in your calendar. Set a few reminders for yourself. If you legitimately need more time to pull documents together, you can often call the number on the notice to request a brief extension.

Can I Just Handle This by Phone or Online?

It really depends on what the notice is about. For simpler issues, like a request to verify your identity to prevent fraud, a quick phone call or online confirmation can often resolve it.

However, for anything more substantial—especially if you disagree with their findings or need to send over detailed financial records—a formal written response sent via certified mail is your best bet. It creates a paper trail, which is crucial for protecting yourself.

What If I Agree but Cannot Pay?

This is a very common situation, so don't panic. If you agree with the notice that you owe the tax but simply don't have the cash to pay it all at once, you still must respond by the deadline.

The IRS has several payment options, from short-term plans to more involved solutions like an Offer in Compromise. The first step is contacting them to discuss what's available. Ignoring the bill only piles on more penalties and interest, digging a deeper hole.

If you're feeling overwhelmed by a complex IRS issue, Attorney Stephen A Weisberg is ready to help. I offer a FREE Tax Debt Analysis to map out the best strategy for your specific situation before you ever pay a fee. Get the expert guidance you need by visiting https://weisberg.tax today.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034