What to Do If You Owe Taxes: Expert Tips to Resolve Your Debt

If you owe the IRS, let me be blunt: the single most important thing you can do is file your tax return on time. It doesn't matter if you can't pay the full amount right away.

Filing is paramount. Ignoring that tax bill is the fastest way to rack up crippling penalties and trigger aggressive collection actions from the government.

Taking control of the situation starts now. Let's walk through what to do.

Your First Moves When You Owe the IRS

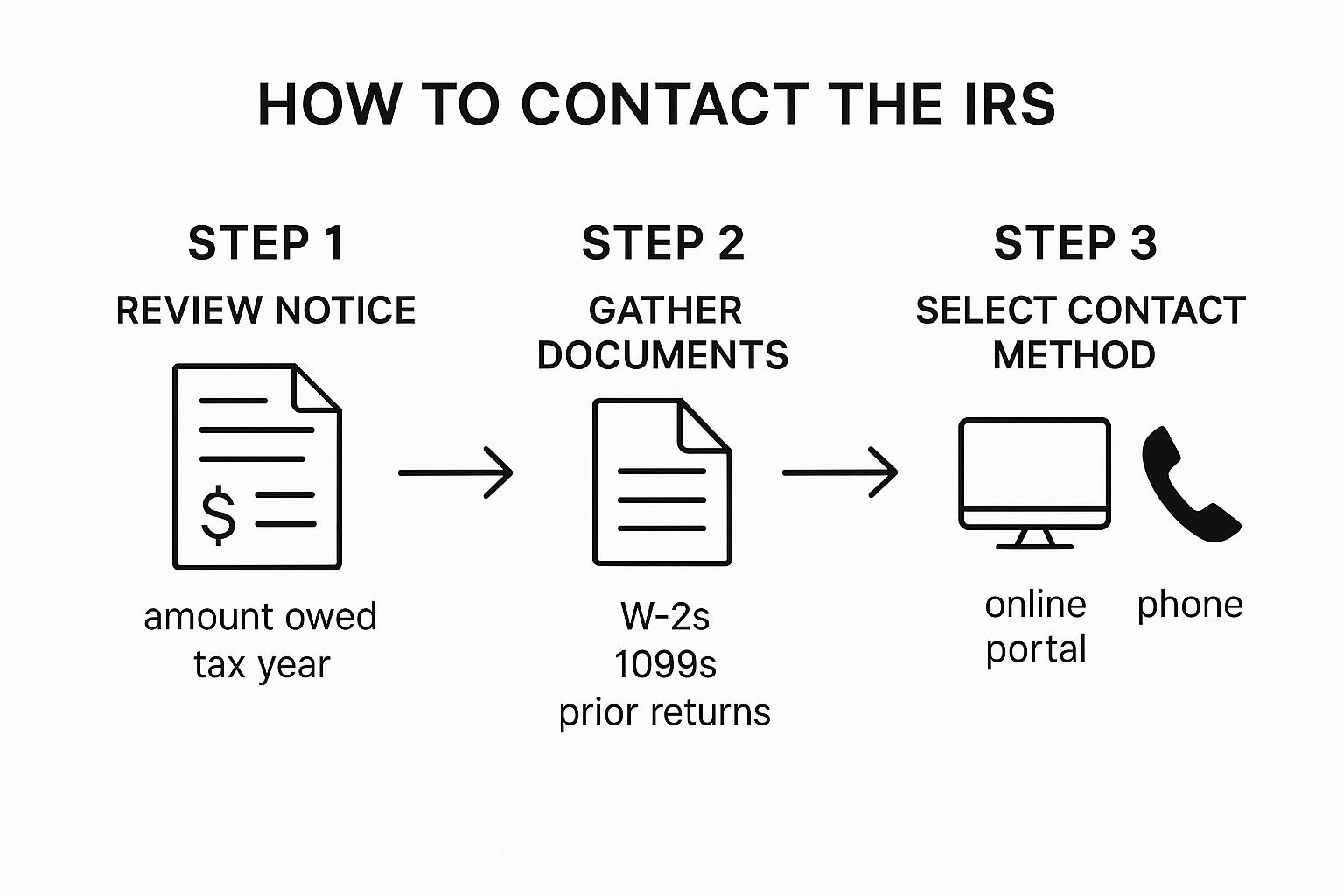

Getting that official-looking envelope from the IRS can make your stomach drop. I've seen it countless times with clients. But paralysis is your worst enemy.

After pausing automated collection notices during the pandemic, the IRS is back to its regular schedule, so you can't afford to sit on that letter.

First things first, make sure the notice is actually from the IRS. Scams are everywhere. The real IRS initiates contact about a tax debt through U.S. Mail, not with an out-of-the-blue phone call or threatening email.

You can instantly confirm what you owe by creating an online account at IRS.gov. It gives you a direct look at your balance and payment history—no guessing required.

File Your Return, No Matter What

I can't stress this enough. So many people believe they should wait to file until they have the cash to pay. That's a huge, expensive mistake.

Why? It comes down to two different penalties. The "failure-to-file" penalty is a brutal 5% of the unpaid taxes for each month your return is late (capped at 25%). In sharp contrast, the "failure-to-pay" penalty is only 0.5% per month.

Just by getting your return in on time, you sidestep that much larger penalty. It's a massive saving and, just as importantly, it signals to the IRS that you aren't trying to hide. It's the essential first step toward getting things sorted.

Busting the Myth of the Inflexible IRS

Many taxpayers picture the IRS as a monolithic, unbending agency that doesn't negotiate. From my experience, that couldn't be further from the truth.

The agency actually has several well-established programs specifically designed to help people who are struggling to pay. The whole system is built on communication.

Facing tax debt can feel isolating, but it's a challenge shared on a massive scale. Globally, public debt is projected to rise above 95% of gross domestic product, a clear sign that both governments and individuals are wrestling with financial obligations.

This widespread fiscal pressure highlights a universal truth, whether you're a country or an individual: you have to get your financial house in order.

The International Monetary Fund (IMF) advises nations to embrace transparency and proactive planning, and the same logic applies to you. You can read more about these global economic trends on the IMF's blog.

Your situation is part of a larger story, and the path to resolution—planning, communicating, and finding a manageable arrangement—is a well-trodden one.

Here’s a quick rundown of the main avenues the IRS offers to help you get back on track.

IRS Tax Debt Options at a Glance

This table gives you a quick summary of the primary ways to handle federal tax debt, helping you identify which path might be best for your situation.

| Option | Best For | Key Feature |

|---|---|---|

| Short-Term Payment Plan | Those who can pay in full within 180 days. | Provides extra time to pay without a formal agreement. |

| Offer in Compromise (OIC) | Individuals with significant financial hardship who can't pay the full amount. | Allows you to settle your tax debt for less than you originally owed. |

| Installment Agreement | People who need more than 180 days to pay the full amount owed. | Sets up a structured, long-term monthly payment plan. |

| Currently Not Collectible | Taxpayers with no ability to pay due to unemployment or low income. | Temporarily pauses collection activity until your financial situation improves. |

Understanding these options is the first step toward finding the right solution. Each one is designed for a different financial reality.

Create Your Immediate Action Plan

Once you've filed your return and confirmed the debt, you can trade that anxiety for a clear-headed plan. Here’s what to do next:

Read every notice carefully. Check the deadlines, the tax years involved, and the specific amounts.

Get your financials in order. Pull together recent pay stubs, bank statements, and a list of your monthly expenses. You'll need this.

Explore your payment options. Head to the IRS website and start digging into the details of short-term plans, installment agreements, and other programs.

Taking these steps transforms you from a victim into the person solving the problem. You're showing the IRS you're ready to work with them, and that cooperation is the key to resolving any tax debt successfully.

Navigating IRS Payment Plan Options

When you’re staring down a tax bill you can’t pay all at once, an IRS payment plan is often the most straightforward path forward.

Think of it as a formal, structured agreement to pay off your debt over time. It’s what keeps the IRS from moving on to more serious collection actions, like slapping a lien on your property or levying your bank account.

The trick, of course, is picking the right plan for your specific financial situation. The IRS gives you two main roads to take: a Short-Term Payment Plan or a Long-Term Installment Agreement. Knowing the ins and outs of each is absolutely critical to making a smart decision.

The Short-Term Payment Plan

Got a hunch you can clear your entire tax debt within the next six months? The Short-Term Payment Plan is probably your best bet. The IRS essentially gives you an extension of up to 180 days to get your bill paid in full.

This option is so appealing because it’s simpler and, frankly, cheaper. You won't have to pay any setup fees, which is a major win compared to the long-term alternative.

But let's be clear: this isn't a free pass. Interest and penalties will keep piling up on your unpaid balance until every last dollar is paid. It's a grace period, not a "get out of jail free" card.

To get this extension automatically through the IRS website, you generally need to owe a combined total of less than $100,000 in tax, penalties, and interest. If your debt is higher, you might still get an extension, but you’ll probably have to get on the phone with the IRS to make your case.

No matter which plan you're considering, preparation is everything. Before you ever pick up the phone or log on to the IRS site, you need to have your ducks in a row.

This just hammers home the point: understand your notice, pull together your financial documents, and then decide how you want to reach out.

The Long-Term Installment Agreement

What if 180 days just isn't realistic? That's where the Long-Term Installment Agreement (IA) comes in. This is the go-to solution for breaking your total tax debt into manageable monthly payments over a much longer period—up to 72 months, in fact.

This is the right move for people who have a steady income but just can't come up with a lump sum to knock out the debt quickly. It gives you predictability and, most importantly, puts a stop to more aggressive collection tactics as long as you stick to the payment schedule.

A Word of Caution: An Installment Agreement is a formal contract. As long as you uphold your end of the bargain, the IRS will generally back off. But if you start missing payments, they can—and will—terminate the agreement, putting you right back in their crosshairs.

If you want to apply online, your total debt needs to be under $50,000 (this includes individual income tax, penalties, and interest). For businesses, that threshold is lower, at $25,000.

If you owe more than these amounts, you’ll need to do it the old-fashioned way by submitting Form 9465, Installment Agreement Request, or by calling the IRS directly.

Understanding The True Cost

Unlike the short-term option, Long-Term Installment Agreements have setup fees. And these fees can vary quite a bit depending on how you apply and how you set up your payments.

Here’s the breakdown:

Online Application with Direct Debit:$31

Online Application with Other Payment Methods:$130

Phone/Mail Application with Direct Debit:$107

Phone/Mail Application with Other Payment Methods:$225

The IRS does waive these fees for qualifying low-income taxpayers. But no matter what you pay to set it up, remember that interest and penalties continue to compound on your remaining balance for the entire life of the agreement.

A good debt repayment calculator can be a real eye-opener, helping you see just how much interest adds to your total cost over time.

Figuring out these future costs can get complicated.

To get a much clearer picture of what your monthly payments and total payback amount might look like, I highly recommend checking out our detailed guide on using an IRS payment plan calculator.

It will help you run the numbers so you can make a truly informed choice before locking yourself into a plan.

When to Pursue Tax Relief and Forgiveness

So you've looked at an IRS installment plan, and the numbers just don't work. The monthly payment is still completely out of reach. What now?

This is the point where you need to look past standard payment arrangements and explore serious relief programs.

When you're facing genuine financial hardship, the IRS has specific lifelines designed for people who truly cannot pay their full tax bill.

These aren't loopholes to get out of paying taxes; they are last-resort options for those in dire straits.

Programs like an Offer in Compromise or Currently Not Collectible status require you to essentially open up your entire financial life to the IRS.

They want to see everything. These are reserved for situations where your income and assets make paying the debt in full an impossible burden.

The Offer in Compromise: A Fresh Start

An Offer in Compromise (OIC) is exactly what it sounds like: an agreement where the IRS lets you settle your tax debt for less than you originally owed. It's often seen as the holy grail of tax resolution, but let me be clear—it's incredibly tough to get. The IRS will only accept an OIC if they believe the amount you’re offering is the absolute most they could ever hope to collect from you.

The agency scrutinizes your entire financial picture, focusing on four key areas:

Ability to Pay: Your income minus what the IRS considers allowable living expenses.

Income: Your current and potential future earnings.

Expenses: The reasonable costs for you and your family to live.

Asset Equity: The value of everything you own—real estate, cars, retirement accounts, you name it.

The IRS plugs these numbers into a rigid formula to determine your "reasonable collection potential." If your offer doesn't meet or beat that calculated amount, it's a non-starter. To get a better sense of the strict criteria, you can review our guide on how to qualify for an Offer in Compromise.

When Is an OIC the Right Move?

Imagine a client who lost a high-paying executive job. They burned through their savings trying to stay afloat and now work a job that barely covers the mortgage and groceries.

They’re staring down a $60,000 tax debt from their better-earning years, and there’s simply no path to paying it back. This is a classic OIC candidate. Their current financial reality makes the old debt an impossible anchor.

The application process itself is a marathon. You'll need to submit Form 656 and either Form 433-A (for individuals) or 433-B (for businesses), backed by a mountain of financial proof. Absolute honesty and meticulous detail are non-negotiable.

Currently Not Collectible: A Temporary Pause

But what if your situation is so severe you can't pay anything? This is where Currently Not Collectible (CNC) status can provide a crucial pause. CNC isn't forgiveness; it's a temporary halt. The IRS agrees to stop active collections—meaning no more wage garnishments or bank levies—while you're in this status.

Don't mistake this for the debt vanishing. Your tax bill is still there, and penalties and interest keep piling up. The IRS will also check back in on your finances periodically, usually every year or two, to see if your ability to pay has improved.

I once worked with a self-employed carpenter who suffered a bad fall, leaving him unable to work for the foreseeable future. With zero income and medical bills piling up, he had nothing to send the IRS. CNC status gave him the breathing room he desperately needed to focus on his recovery without the constant stress of collection notices.

This individual struggle mirrors a much larger economic issue. As interest rates climb, the cost of carrying debt has exploded.

In fact, major governments like the U.S. now spend more on debt interest than on national defense. With global public debt soaring to around $100 trillion, both governments and individuals are feeling the pressure.

This trend, detailed by the World Economic Forum, underscores a harsh reality: delaying tax payments is more costly than ever as interest compounds at an alarming rate.

Whether you're aiming for an OIC or need the temporary relief of CNC status, remember that the burden of proof is entirely on you. Your success hinges on providing clear, undeniable evidence that you simply cannot resolve your tax debt through a normal payment plan.

How to Tackle State Tax Debt

If you're staring down a tax bill from the IRS, there's a good chance you have another one from your state's department of revenue waiting in the wings. It’s a classic one-two punch, and you can’t afford to ignore either opponent.

While owing the government money feels the same no matter who sends the bill, the rules of engagement are wildly different.

The IRS sets a certain standard, but each state has its own unique playbook for collecting what it's owed. This creates a confusing patchwork of regulations where what works in one state might completely fail in another.

State Rules Are a Different Ballgame

The differences between state and federal tax resolution can be staggering. Many states offer their own version of an Offer in Compromise (OIC), but the qualifications can be a far cry from the IRS's requirements.

Let's look at a couple of real-world examples I see all the time:

California: The Franchise Tax Board (FTB) offers installment agreements, which sound similar to the IRS. But their OIC program is a separate beast, requiring its own application (Form FTB 4905) and a very strict review of your financial situation.

New York: The New York State Department of Taxation and Finance also has payment plans and an OIC. The real kicker? They have collection tools the IRS doesn't, like the power to suspend your driver’s license over a significant tax debt. That gets people’s attention fast.

These examples highlight a critical point: you have to treat your state tax debt as its own unique and serious problem. Never, ever assume that a strategy that works with the IRS will fly with your state.

Finding the Right Information for Your State

Your first move should be heading straight to your state's official department of revenue or taxation website. This is the only place to get accurate forms, payment plan details, and legitimate contact information. A word of caution: make sure the site ends in .gov. There are plenty of look-alike sites out there that will charge you for things you can do for free.

Tackling federal and state tax debts at the same time is non-negotiable. If you focus only on the IRS, you might come home to find a state tax lien slapped on your property. That lien is a public record that can absolutely crater your credit score.

Once you’re on the official site, look for links like "Payments," "Collections," or "Help with Tax Debt." This is where you’ll find the guidance and forms to get started.

A major hurdle for many is the Notice of State Tax Lien, which is the state's legal claim against your property. While it's similar to a federal lien, the process to get it removed is dictated entirely by state law. Understanding this process is vital, and you can learn more in our guide on how to remove a tax lien.

Why You Have to Fight on Two Fronts

It’s tempting to pour all your energy into the bigger federal debt and let the state bill slide. That’s a huge mistake. State collection actions can be just as aggressive—and sometimes move even faster—than the IRS.

Here’s your game plan:

Get the Full Picture: First, figure out exactly what you owe to both the IRS and your state. No estimates.

Know the Rules: Research the specific payment plans and relief options available from both agencies.

Build a Unified Budget: Create a single, realistic budget that accounts for payments to both the feds and the state. If you're trying for an OIC, you'll likely need to prepare and submit two separate, tailored offers.

By confronting both tax debts head-on, you stop one problem from blowing up while you’re busy with the other. A coordinated strategy is the only way to truly get back on solid financial ground and leave these tax headaches behind for good.

Deciding When to Hire a Tax Professional

It’s tempting to try and tackle tax debt on your own, and frankly, sometimes you can. The IRS has made its online tools pretty decent for setting up a straightforward payment plan. But there’s a clear tipping point where going it alone stops being brave and starts being reckless.

Knowing when to wave the white flag and call in an expert is one of the most important decisions you'll make. It often boils down to two things: complexity and stakes.

If you're just looking to get on an installment plan for a few thousand dollars, you can probably manage it. Once the numbers get bigger or the situation gets messy, the value of a pro isn't just a convenience—it's a necessity.

Red Flags That Scream "Hire a Pro"

Some situations are more than just a nudge to get help; they're giant, flashing neon signs. These are the moments when the financial and legal risks of a DIY approach become far too great to manage by yourself.

Here are the tell-tale signs that you need an expert in your corner, and fast:

Your total tax debt tops $50,000. This is a magic number for the IRS. Cross this line, and you’re often out of the running for their simple online agreements. The scrutiny you’ll face gets a whole lot more intense.

You're sitting on multiple years of unfiled tax returns. This is no longer just a debt problem—it’s a full-blown compliance crisis. A professional knows how to get you caught up the right way, mitigating the penalties and managing the inevitable fallout.

You're facing a complex IRS audit. An audit isn't a friendly chat. It's a formal, in-depth examination of your finances, and having a representative who speaks their language is your best defense against a devastating outcome.

You want to pursue an Offer in Compromise (OIC). We’ve talked about this before; OIC applications are notoriously complex and have a sky-high rejection rate. An experienced pro knows exactly what it takes to build a case the IRS will actually consider.

You think the IRS is wrong about what you owe. If you believe the tax assessment is incorrect, you can’t just say so. You have to formally challenge it, a process that requires a deep command of tax law and IRS procedure.

Trying to handle these issues alone is like trying to fix your own transmission with a butter knife. You might have a vague idea of what needs to happen, but the odds of making a costly, irreversible mistake are incredibly high.

Key Insight: This strategic thinking isn’t just for individuals. Big corporations grapple with debt all the time, and their playbooks offer useful lessons. The core principle is always about balancing today’s needs against the long-term consequences of that debt—a truth that holds whether you're a Fortune 500 company or a single taxpayer.

Choosing the Right Kind of Expert

Not all "tax pros" are created equal. The expert you need is determined entirely by the problem you have. Hiring the wrong type of professional is a surefire way to waste both time and money.

Here’s a quick rundown of the three main types of tax professionals you’ll encounter:

Enrolled Agent (EA): These pros are licensed directly by the IRS. They are true tax specialists who can handle everything from preparing returns to representing you in front of the IRS.

Certified Public Accountant (CPA): While many CPAs are focused on general accounting, those who specialize in tax resolution bring expert advice and a broader financial perspective to the table.

Tax Attorney: This is your go-to when a tax problem crosses into legal territory. A tax attorney is non-negotiable for navigating Tax Court, dealing with criminal tax investigations, or any situation where you need the protection of attorney-client privilege.

For most tax debt problems, an Enrolled Agent or a CPA specializing in tax resolution is a fantastic choice. Their expertise is perfectly matched for negotiating with the IRS.

But for high-stakes situations with serious legal risk, a tax attorney is indispensable. To see how these experts work in practice, take a look at our guide on how to settle IRS debt with a smart strategy.

The entire financial world, from giant corporations to individuals, is in a constant dance with debt. For instance, shifts in corporate tax rates directly impact how much debt a company is willing to take on.

The U.S. federal corporate rate fell to 21% in 2017, but with state taxes, the effective rate is closer to 25%. As data updates from financial experts show, these policies are always in flux. It's a powerful reminder that understanding the real cost of debt is vital, especially when the laws themselves keep changing.

Common Questions About Owing Taxes

Once you start digging into payment plans and relief programs, a lot of practical questions pop up. These are the "what if" scenarios that keep people up at night. Let's tackle some of the most common ones I hear from clients so you can move forward with confidence.

What Happens If I Ignore an IRS Tax Bill?

Ignoring the IRS is a terrible idea. I’ve seen it play out time and time again, and it never ends well. Think of it like a small leak; ignore it, and you’ll eventually have a flood on your hands. The IRS has a very predictable and aggressive collection process.

After a few letters, they'll stop asking nicely. The first major step is often a federal tax lien. This is a public legal claim against all your assets—your house, your car, everything. It wrecks your credit and makes it nearly impossible to sell property or get a loan.

If that doesn't get your attention, they'll move to a levy, which means they actively start taking your stuff. This isn't a threat; it's a reality. A levy allows them to:

Garnish your wages right from your paycheck.

Clean out your bank accounts and even dip into retirement funds.

Seize physical property, including your vehicle or home.

All this time, penalties and interest are piling up daily, making the original debt grow exponentially. The only way to stop this domino effect is to open a line of communication.

Can I Get Tax Penalties Removed?

Yes, absolutely. The IRS can and does remove penalties through a process called penalty abatement. It isn't a given, but if you have a solid reason, you have a good shot at it.

The most straightforward path is the First-Time Abatement (FTA). If you’ve been a model taxpayer for the previous three years—meaning you filed and paid on time—you can often get a pass on penalties for one bad year. You just have to ask.

You can also argue for abatement based on "Reasonable Cause." This applies when life gets in the way. Think serious illness, a death in the family, a natural disaster, or even getting bad advice from a tax pro.

To prove Reasonable Cause, you need to write a clear, detailed explanation and provide documentation to back up your story. One critical thing to remember: even if the IRS forgives the penalties, you will almost always still owe the interest that accrued on the underlying tax debt.

Does Tax Debt Ever Expire?

Technically, yes. The IRS generally has a ten-year statute of limitations to collect a tax debt. This countdown is called the Collection Statute Expiration Date (CSED), and it starts on the day your tax was officially assessed.

But—and this is a huge but—it's not a simple 10-year wait. Many of the actions you might take to resolve your debt actually pause the clock. Filing for bankruptcy, submitting an Offer in Compromise, or even asking for an installment plan can "toll" the statute, stopping the countdown.

Trying to wait out the IRS is a high-risk, low-reward strategy. The clock can be extended for years beyond the initial decade, and the agency is incredibly persistent. It's far better to face the debt head-on than to hope it just fades away.

Should I Use a Credit Card to Pay My Taxes?

You can, but you need to be very careful. You can't just pay the IRS directly with a credit card. You have to go through an approved third-party processor, and they’ll charge you a convenience fee—usually around 2% of your payment.

The upside is speed. Paying the IRS off immediately stops their failure-to-pay penalties and interest from growing. If you have a rewards card with a big sign-up bonus and you know you can pay the card off in a month or two, it might make sense.

The danger is the interest rate. Your credit card’s APR is almost guaranteed to be much higher than the rate on an IRS payment plan.

If you let that tax debt sit on your credit card for months, you’ll end up paying far more in interest to the credit card company than you ever would have to the IRS. This move only works if you have a surefire way to pay off the credit card balance almost immediately.

Navigating the complexities of IRS and state tax debt requires expertise and a strategic approach. If you're facing a significant tax bill or a complex situation, you don't have to handle it alone. At Attorney Stephen A Weisberg, we start with a free, no-obligation tax debt analysis to determine the best path forward for you.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034