Responding to IRS Letters: Your Guide to Confidently Handle Notices

When an IRS letter shows up in your mailbox, the single best thing you can do is read it carefully and respond by the deadline. Ignoring it is a surefire way to rack up penalties and let a small issue snowball into a much bigger one. A prompt, organized response is always your best move.

What to Do After Getting an IRS Letter

Seeing that IRS logo on an envelope can make anyone's heart skip a beat. I get it. But the most critical thing to do in those first 24 hours is to stay calm and be methodical. Panicking leads to mistakes. A measured approach puts you back in the driver's seat.

Believe me, the absolute worst thing you can do is toss that letter on the counter and pretend it doesn't exist.

Start by breaking down the letter itself. You'll find the most important details right in the top right-hand corner.

Key Information to Find Immediately

As soon as you open the envelope, zero in on these specifics:

The Notice or Letter Number: This is a code, like CP2000 or LTR 5071C, that tells you exactly what the IRS is communicating. This number is the key to understanding the letter's purpose and how seriously you need to take it.

The Response Deadline: The IRS gives you a specific date they need to hear from you. Miss this, and you could find yourself automatically agreeing with their proposed changes and facing extra penalties. Circle this date on your calendar immediately.

The Tax Year in Question: The notice will state which tax year it's about (e.g., 2022, 2023). This instantly tells you which of your records you'll need to dig up.

Expert Tip: Never just assume the IRS is correct. Their systems are powerful, but they aren't perfect. A notice is usually a proposal based on the information they have, not a final bill set in stone. Your response is your chance to provide your side of the story and the documents to back it up.

Figuring out these initial details takes the letter from a source of anxiety and turns it into a manageable task. If you want to be truly prepared for any potential scrutiny, having a comprehensive audit readiness checklist is an invaluable tool.

Once you’ve noted the deadline and identified the issue, you’ve laid the groundwork for a clear, effective, and timely response. That’s the best way to keep a small tax matter from escalating.

How to Decode Common IRS Notices

That envelope from the IRS in your mailbox is enough to make anyone’s heart skip a beat. But before you panic, take a deep breath. Getting a letter doesn't automatically mean you’re in hot water. Often, it's just a routine request for more information or a notification about a minor adjustment.

The first step is figuring out what the IRS is actually trying to say. Think of it as cracking a code.

You're not alone in getting one of these. The IRS mails out a mind-boggling 170 million notices to individual taxpayers every single year.

The agency even realized its own letters were confusing, so it launched a Simple Notice Initiative to make them easier to read.

A pilot program for the identity verification Notice 5071C, for example, led to a 16% drop in calls and a 6% increase in people successfully using the online resolution tool. It just goes to show that clarity helps everyone.

Different Kinds of IRS Letters

To get a quick handle on what you're dealing with, I find it helps to sort the notice into one of three main buckets. This initial read will tell you how urgently you need to act.

Requests for Information: These are the most common and least scary. The IRS might just need you to verify your identity (like with an LTR 5071C) or send documents to back up a deduction you claimed. No big deal, as long as you respond.

Proposed Tax Changes: A CP2000 notice is a perfect example. This is not a bill. It’s a proposal. The IRS is saying, "Hey, we think your tax should be different based on info we got from your employer or bank. What do you think?" You have every right to disagree and send proof.

Immediate Action Needed: These are the ones to take seriously. A notice of intent to levy or a final bill means you need to act now to avoid bigger problems. If the amount is overwhelming, you might need to look at all your options. Our guide on how to qualify for an Offer in Compromise can be a great place to start exploring how to handle significant tax debt.

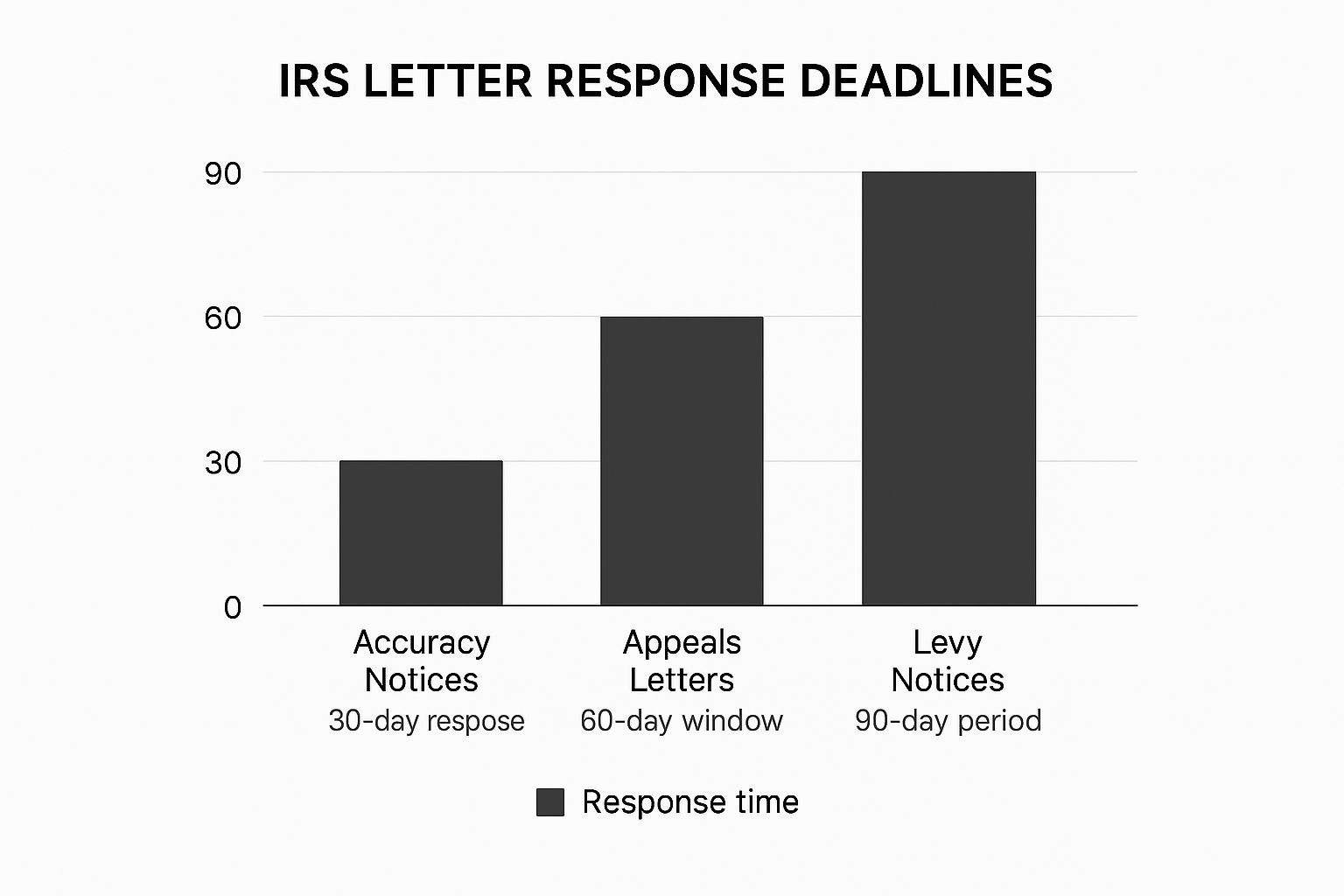

This chart shows just how much the response deadlines can vary, which is why identifying your letter right away is so important.

As you can see, you could have as few as 30 days or as many as 90 to respond. Time is of the essence.

A Quick Guide to Common IRS Notices

To help you quickly figure out what you're holding and what to do next, I've put together this quick-reference table. It covers some of the most common notices taxpayers receive.

| Notice Number | Common Reason for Notice | Immediate Action Required |

|---|---|---|

| CP2000 | IRS proposes changes to your tax return based on third-party info (e.g., from your employer). | Review the proposed changes carefully. Respond by the deadline with agreement or provide documents to dispute it. This is not a bill. |

| CP14 | You have a balance due on your taxes. | Pay the amount by the due date to avoid further penalties and interest. If you can't pay, explore payment options. |

| LTR 5071C | The IRS needs to verify your identity to process your tax return. | Use the online IRS identity verification service or call the number provided. Have a copy of the letter and your prior/current tax returns handy. |

| CP2501 | The IRS has questions about your income, credits, or deductions and needs more information. | Gather the requested documents (receipts, statements, etc.) and mail or fax your response by the deadline. |

| LTR 105C | Your claim for a refund (like the Employee Retention Credit) has been disallowed. | Read the explanation for the disallowance. If you disagree, you have the right to appeal the decision. |

This table isn't exhaustive, of course, but it covers many of the letters that land in mailboxes most often.

Identifying the specific notice is the foundational first step. A CP14 (Balance Due) is a straightforward bill, while a LTR 105C (Claim Disallowance) means a refund you were hoping for has been denied. Each one requires a completely different game plan.

One of the biggest points of confusion I see with clients is the CP2000, Notice of Proposed Adjustment for Underpayment. So many people mistake it for a bill and panic. Remember, it's your chance to set the record straight before the IRS makes a final decision. Your response here is absolutely critical.

Gathering Your Documents to Build a Strong Case

A powerful response to an IRS letter isn’t built on arguments or explanations alone. It's built on solid proof.

Before you even think about drafting a reply, your first job is to play detective and gather all the evidence that supports your position.

Think of it this way: the IRS already has a file on you, and their letter is based on whatever information is in it.

Your mission is to present your own records to either confirm what they're saying or—more likely—show them where they've gone wrong.

I always tell my clients to start by creating a dedicated folder for this specific issue, either physically or digitally.

A digital folder is usually best since it makes sending copies much easier later on. This keeps everything organized and prevents you from mixing up documents for different tax years or issues.

Your Document Collection Checklist

The exact documents you'll need really depend on the specific problem the IRS notice raises. But for most situations, you'll want to start by rounding up these usual suspects:

A copy of the tax return for the year in question.

All your income documents, like W-2s from your jobs and any 1099s you received (1099-NEC, 1099-MISC, 1099-K, etc.).

Bank and credit card statements that can back up your expenses or show the source of deposits.

Receipts and invoices for any deductions or credits the IRS is questioning, such as business expenses, charitable donations, or medical bills.

Any other letters or notices you've already received from the IRS about this specific tax year.

Crucial Tip: Whatever you do, never send original documents to the IRS. Always, always send copies. I've seen it happen too many times—the chances of you ever seeing those originals again are slim to none. Keep your originals safe at home.

Pinpoint the Exact Discrepancy

Once you have all your paperwork in one place, it's time for a side-by-side comparison. Lay the IRS notice out next to your tax return and the supporting documents you just gathered.

For example, if you got a CP2000 notice proposing changes because of underreported income, you need to compare the income sources the IRS lists with the W-2s and 1099s you actually have.

Let's imagine the notice claims you have $5,000 in unreported income from a 1099-NEC. Your next step is to pull out your copy of that specific form. Does the amount on the form match what the IRS is claiming?

Did you accidentally leave it off your return? Or maybe the company that paid you issued a corrected 1099, but the IRS only has the old, incorrect one on file.

This investigative step is the most important part of the whole process. It turns a vague, stressful feeling of "the IRS says I owe more money" into a specific, manageable point of disagreement.

By finding that exact point of friction, you can craft a focused and effective response that gets right to the heart of the matter. You’re no longer just defending yourself; you’re presenting clear, targeted evidence to set the record straight.

How to Write a Clear and Effective Response Letter

When you write to the IRS, you're doing more than just sending a letter. You're creating an official record for your case.

This is your chance to state your position clearly and professionally, so it’s crucial to get it right. The entire goal is to make it as easy as possible for the IRS agent handling your case to understand your side of the story and agree with it.

Get straight to the point. Your very first sentence should identify why you're writing. Reference the notice number (like CP2000) and the tax year in question right at the top. This simple step saves the agent time and immediately sets the context for your response.

Crafting a Professional Tone

I get it. Getting an IRS notice can be frustrating, even infuriating. But letting those emotions spill into your letter is a surefire way to hurt your case. Stick to the facts. The tone should always be respectful, neutral, and business-like.

Clarity is your best friend here. Use simple, direct language instead of trying to sound like a lawyer with complex jargon. Following some essential tips for clear writing can make a world of difference. You want the agent to grasp your points on the first read, without any ambiguity.

A Note on Tone: Remember, the person on the other end is just an employee doing their job. A hostile or emotional letter starts things off on the wrong foot. A respectful, fact-based response, on the other hand, encourages cooperation and makes a smooth resolution much more likely.

Structuring Your Response

A well-organized letter is a persuasive letter. Don't just throw all your points into one long paragraph. Instead, mirror the structure of the IRS notice itself. Address each issue one by one, in the same order they presented them. This creates a logical path for the agent to follow along with their own documents.

For each point, you need to clearly state your position. Do you:

Agree with the proposed change?

Disagree and have evidence to prove your point?

Have additional information that they didn't consider?

Let’s imagine the IRS notice questions a $2,500 deduction for business supplies. Your response for that item could be as simple as: "Regarding the disallowance of the $2,500 deduction for business supplies, I disagree with this change. Enclosed are copies of receipts and bank statements documenting these expenses." It’s direct, professional, and points them right to your proof.

If you find yourself disagreeing on several items and the total amount is getting large, it might be a good time to look at the bigger picture. Understanding how to negotiate IRS debt can give you insight into what’s possible when the stakes are higher.

Essential Components of Your Letter

To make sure your response gets processed correctly and isn't kicked back, there’s some basic information that absolutely must be on every letter you send. I recommend putting this right at the top of the page.

| Information to Include | Why It's Important |

|---|---|

| Your Full Name and Address | To correctly identify you and your account. |

| Your Social Security Number or TIN | This is the main number they use to look up your file. |

| The Notice Number (e.g., CP2000) | Gets your letter to the right department and agent. |

| The Tax Year in Question | Prevents confusion with other tax years. |

| Your Contact Phone Number | Allows the agent to call you for quick clarifications. |

Finally, and this is critical: sign and date your letter. An unsigned letter is not a valid response in the eyes of the IRS. If you forget to sign it, you could miss your deadline even if the letter arrived on time. Your signature is what makes it official. Don't forget it.

Submitting Your Response And What To Expect Next

You’ve done the hard work of gathering your documents and drafting a solid response. Now comes the final, crucial step: getting it into the IRS's hands correctly.

How you send your response is just as important as what's in it, because you need to create an official record that you’ve done your part.

First things first, find the right address. It’s printed directly on the IRS notice you received.

Don't guess or use a generic IRS address you find online—that’s a surefire way to have your response get lost in the shuffle, causing major delays.

When you mail your letter and its attachments, you absolutely must use USPS Certified Mail with a return receipt. This isn't just a friendly suggestion; I consider it a non-negotiable rule when dealing with the IRS.

That little green and white receipt that comes back to you in the mail is your legally binding proof that the IRS received your package and, just as importantly, when they received it.

Expert Insight: Think of certified mail as your insurance policy. For a few extra dollars, you get an undeniable paper trail that proves you met your deadline. I've seen that simple receipt save countless clients from penalties and headaches when the IRS claimed a response was never received.

And remember, you're sending sensitive financial data. It's always smart to review best practices for the secure sharing of documents to protect your information.

The Waiting Game And How To Follow Up

Once your response is in the mail, the hardest part often begins: the wait. You have to manage your expectations here.

The IRS is a massive bureaucracy, and it simply doesn’t move fast. It can easily take 60 to 90 days, sometimes even longer, for the agency to process your correspondence and send a reply.

A long silence doesn’t mean something is wrong. In fact, it's completely normal. Resist the urge to call them every week or send follow-up letters.

Doing so can just clog up the system and potentially confuse the agent handling your case. Your certified mail receipt is your proof—trust the process.

To put it in perspective, IRS customer service reps answered about 20 million live phone calls in a recent fiscal year.

That’s just a tiny fraction of the total communications they handle. This is exactly why a well-documented written response, backed by proof of delivery, is one of the most powerful tools you have.

When Your Response Is Ignored

So, what happens if the clock keeps ticking? If you've passed the 90-day mark without a word, it’s now reasonable to follow up.

Before you pick up the phone, get your ducks in a row. Have your copy of the response letter and your certified mail receipt right in front of you. Then, call the number listed on your original IRS notice. Be prepared for a long wait on hold—it’s just part of the experience.

If the IRS ignores your timely response and jumps straight to collection actions like garnishing your wages, that’s a major red flag.

It often means your response got stuck somewhere in their internal system, and you may need to escalate the issue.

Answering Your Top Questions About IRS Letters

When that official-looking envelope from the IRS lands in your mailbox, it's natural for a million questions to start racing through your mind.

Over the years, I've found that most people have the same core concerns. Getting clear, straightforward answers is the first step to taking control of the situation.

Let's tackle some of the most common questions I hear from clients.

What Happens If I Miss The IRS Deadline?

First, don't panic. Missing an IRS deadline is a serious misstep, but it’s rarely a catastrophic one if you address it quickly. What happens next really depends on the type of notice you received.

If it was a straightforward bill, like a CP14 notice, the immediate consequence is that you’ll start racking up more penalties and interest on whatever you owe.

If the deadline was for responding to a proposed change, like in a CP2000 notice, the IRS will simply assume you agree with their proposed adjustment. They'll then formally assess the tax and send you a bill for the new amount.

The absolute worst thing you can do is ignore it. The problem will not go away. The key is to communicate as soon as you realize you've missed the date—it shows good faith and can prevent things from escalating.

Is It Better To Call The IRS Or Write A Letter?

While picking up the phone feels like the fastest way to get an answer, a written response is almost always the superior strategy. I tell every client this. A formal letter creates an official paper trail, and that documented record is your single best defense if a dispute ever arises about your response.

Let's be honest: calling the IRS can be an exercise in extreme frustration. The agency's phone lines are notoriously overwhelmed.

In a recent fiscal year, the IRS fielded a staggering 281.7 million calls but only managed to answer about 32 million of them.

And for the lucky few who got through? The average wait time was around 23 minutes. You can dig into more of this data yourself in the National Taxpayer Advocate’s annual report.

A quick phone call might be fine for a very simple, clarifying question. But for any substantive disagreement, detailed explanation, or formal response, you absolutely must put it in writing. Always send it via certified mail with a return receipt. This is a non-negotiable step to protect yourself.

When Should I Hire A Tax Professional?

This is the big one. Knowing when to call for backup is a critical judgment call. Based on my experience, you should strongly consider hiring a tax professional, like a seasoned tax attorney, in a few key situations.

The stakes are high. If the total tax, penalties, and interest the IRS is demanding would cause you significant financial hardship, it's time for an expert.

You disagree with the IRS's facts. You might have all the right documents, but presenting a complex or nuanced argument is a skill. A professional knows how to frame it effectively.

You've received a "scary" notice. Any letter that mentions an audit, lien, levy, or wage garnishment is a clear signal to stop and get professional help immediately.

You're simply overwhelmed. There's no shame in admitting that this is too stressful or confusing. Bringing in a pro gives you peace of mind and ensures the job is done right.

A good tax professional does more than just write letters. They take over all communication with the IRS, making sure every response is strategic.

They can also explore solutions you might not even know exist. For example, if you're facing a large tax bill, an expert can determine if you qualify for one of the IRS debt forgiveness programs.

Ultimately, bringing in a professional is about leveling the playing field. They live and breathe this stuff, and they can advocate for the best possible outcome on your behalf.

If you're facing a tax problem and aren't sure what to do next, don't go it alone. Attorney Stephen A. Weisberg offers a FREE Tax Debt Analysis to assess your situation and find the best path forward before you ever pay a fee. Contact us today to get the expert help you deserve.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034