What Happens If You Never File Taxes? Find Out Now

When you don't file your tax return, you kick off a series of escalating problems with the IRS. It starts with a failure-to-file penalty and daily compounding interest, but it can quickly spiral into serious legal action against your property and finances.

The Immediate Consequences of Not Filing Taxes

Think of not filing your taxes like putting off fixing a small drip under your sink. At first, it’s just a minor annoyance. But if you ignore it long enough, you come home to a flooded kitchen.

It's the same with the IRS; the moment you miss that tax deadline, a process begins that quietly—and then not-so-quietly—erodes your financial stability.

The IRS doesn't just sit around and wait for you to act. Its automated systems are built to flag non-filers right away. One of the first things the agency might do is file what’s called a Substitute for Return (SFR) on your behalf. Don't be fooled by the name; this is rarely a good thing for you.

An SFR is the IRS’s best guess at what you owe, but it's a one-sided calculation. They use the income data they have on hand from W-2s and 1099s, but they leave out all the things that could lower your tax bill—like deductions for mortgage interest, credits for dependents, or write-offs for business expenses. The result? A tax bill that’s almost certainly much higher than what you actually owe.

The Financial Domino Effect

Ignoring your filing obligation creates a financial storm that only gets worse over time. You're not just dealing with the original tax amount; you're facing a compounding problem of penalties and interest that can grow exponentially.

Believe it or not, the scale of this problem is staggering. For every six dollars in federal taxes owed in the U.S., one dollar goes unpaid each year. That's a massive hole in the country's budget.

This "tax gap" is exactly why the IRS pursues non-filers so aggressively. You're not just a single person who missed a deadline; you're part of a multi-billion dollar issue the government is determined to solve. The chart from Brookings below gives you a sense of just how big the global tax evasion problem is.

The data makes it crystal clear: with trillions of dollars hidden offshore, tax agencies around the world are highly motivated to track down every cent they're owed. If you want to dive deeper into the numbers, you can explore the full Brookings analysis on tax evasion.

To help you get a clearer picture of what you're up against, here's a quick summary of the key risks.

Summary of Key Consequences

| Consequence | Description |

|---|---|

| Substitute for Return (SFR) | The IRS files a return for you without any of your deductions or credits, resulting in a much higher tax bill. |

| Compounding Penalties & Interest | Your debt grows daily with failure-to-file and failure-to-pay penalties, plus interest charged on the entire balance. |

| Loss of Refunds | If you're actually owed a refund, you typically have only three years to file and claim it. After that, the money is gone for good. |

| Federal Tax Lien | A legal claim against all your property (home, car, bank accounts) to secure the tax debt, damaging your credit. |

| IRS Levy | The actual seizure of your assets—wages, bank accounts, or even physical property—to pay off what you owe. |

As daunting as this all sounds, there is always a way forward. The worst thing you can do is continue to ignore it. The first step toward fixing the problem is simply taking action. You can get started by reading our guide on how to file back taxes and start taking back control of your finances.

How Financial Penalties and Interest Snowball

When you don't file your taxes, the financial fallout isn't just about the tax you originally owed. It's about the relentless pile-on of penalties and interest that the IRS tacks on, turning what might have been a small problem into a serious financial burden.

Think of it like a tiny snowball at the top of a very long hill. It starts small, but with every passing day, it picks up more snow and speed, growing exponentially until it becomes an avalanche of debt. That's exactly how IRS penalties work.

The two big penalties you need to know about are for failure-to-file and failure-to-pay. A lot of people mix these up, but the IRS sees them very differently. In their eyes, not filing your return is a much bigger deal than not being able to pay what you owe. As a result, the penalty for not filing is punishingly high.

The Staggering Cost of Doing Nothing

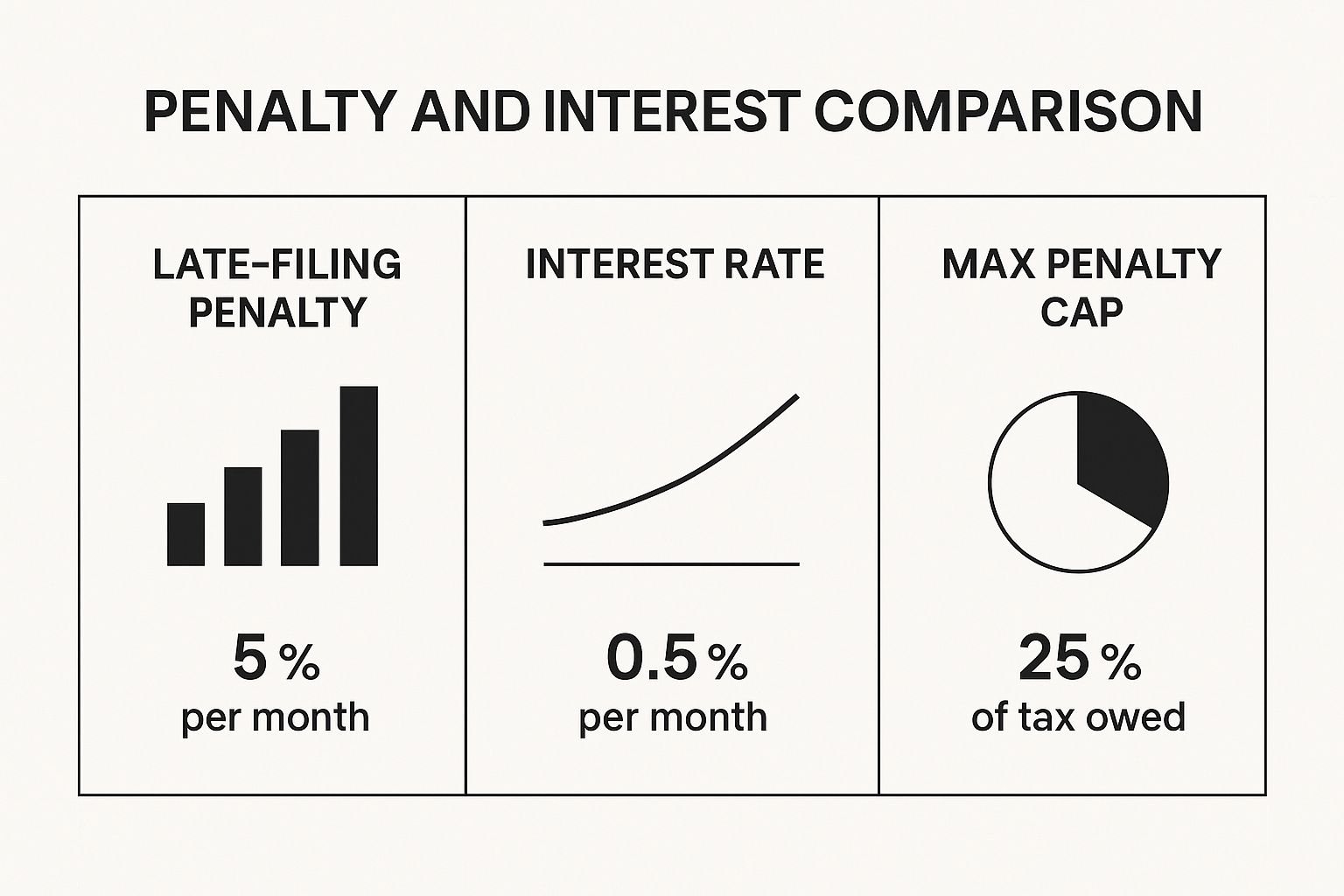

The moment you miss the filing deadline, the clock starts ticking. The failure-to-file penalty is a brutal 5% per month on the unpaid taxes, and it can climb all the way up to 25% of your total tax bill.

Compare that to the failure-to-pay penalty, which is 0.5% per month. That means the penalty for not filing is a staggering ten times worse. The IRS is sending a clear message: even if you can't pay a dime, you absolutely must file your return on time.

This infographic lays out just how quickly these costs can stack up.

As you can see, the failure-to-file charge is the real monster here. It's designed to get your attention and force compliance.

Now, what happens if you don't file and don't pay? The IRS does offer a small break. When both penalties apply in the same month, the failure-to-file penalty is reduced by the failure-to-pay amount. But you're still looking at a combined penalty that can hit 5% per month, a rate that can cause your debt to spiral out of control fast.

Let's put these figures side-by-side to see the real difference.

Penalty and Interest Rate Comparison

This table clearly illustrates the massive difference between the two primary penalties and the interest that accrues on top of it all.

| Penalty Type | Rate Per Month | Maximum Percentage | Annual Interest Rate |

|---|---|---|---|

| Failure-to-File | 5% | 25% | The federal short-term rate plus 3% |

| Failure-to-Pay | 0.5% | 25% | The federal short-term rate plus 3% |

The takeaway is simple: the penalty for not filing is aggressive and immediate. It's the government's way of ensuring that taxpayers don't simply drop off the radar.

Civil Fines vs. Criminal Charges

For most people who fall behind on their taxes, the consequences are purely financial. These civil penalties—the fines and interest we've been discussing—are added to your bill automatically for not following the rules. It's a collections issue, not a criminal one.

But things can get much, much more serious.

If the IRS believes your failure to file was an intentional act of willful tax evasion, the situation changes dramatically. This isn't just about being forgetful or disorganized; it's about deliberately trying to deceive the government or hide your income.

Willful evasion transforms your problem from a simple debt collection matter into a federal crime. This is reserved for the most serious cases, but it's a stark reminder of the legal gravity of ignoring your tax obligations.

When you're buried under an avalanche of penalties and interest, it's easy to feel like there's no way out. But there are structured solutions designed for taxpayers in this exact situation.

Before you give up hope, check out our complete guide to an IRS Offer in Compromise. You might be able to settle your entire tax debt for much less than you currently owe.

When the IRS Can Seize Your Assets

When the official letters and notices from the IRS start piling up unanswered, the situation escalates. This is the point where the problem shifts from simply owing money to facing the government's full collection power. And when it comes to collections, the IRS has two incredibly potent tools: the federal tax lien and the IRS levy.

Think of a tax lien as the IRS planting its flag on everything you own. It's a formal, public claim filed against all your property—your house, your car, even assets you acquire in the future. A lien doesn't immediately take anything away, but it puts a lock on your financial life.

With a lien on your record, your ability to get credit can grind to a halt. Forget getting a new mortgage, car loan, or even a credit card. If you try to sell your home, the IRS gets its money from the sale before you see a dime. It's a serious roadblock.

The Difference Between a Lien and a Levy

So, while a lien is a claim against your property, a levy is the actual act of taking it. If the lien is the warning shot across the bow, the levy is the cannonball hitting the deck. This is what happens if you continue to ignore the debt after the IRS has filed a lien and sent you a Final Notice of Intent to Levy.

A federal tax lien secures the government's interest in your property; a levy takes that property to satisfy the debt. One is a public claim, the other is an active seizure.

The IRS has incredibly broad authority to levy, or seize, all sorts of assets to pay off what you owe. This isn't a suggestion—it's one of the most aggressive collection actions they can take.

Some of the most common targets for an IRS levy include:

Your Wages: The IRS can simply order your employer to divert a chunk of your paycheck directly to them. This is a wage garnishment.

Your Bank Accounts: They have the power to take money right out of your checking or savings accounts, often with no further warning.

Your Property: In more severe situations, the IRS can seize and sell physical property like your vehicle, a boat, or even your home to settle the debt.

Your Social Security Benefits: Through the Federal Payment Levy Program, the IRS can even take a slice of federal payments you're owed, including your Social Security.

This process can move with alarming speed, leaving you with frozen accounts and a much lighter paycheck. To get a much deeper understanding of how this works, our ultimate guide to understanding an IRS Notice of Levy breaks down exactly what taxpayers need to know. The most important thing is to take action before the IRS is forced to.

Understanding the Statute of Limitations

It's a common myth that if you wait long enough, the IRS will just forget about an old tax debt. While there is a statute of limitations that limits how long the IRS can chase you for money, it comes with a massive catch for non-filers: the clock never starts running.

Think of it like a stopwatch in a race. The IRS has a set amount of time to get to the finish line and collect what you owe. But if you never show up to the starting line by filing a return, the race official can't start the watch. Legally, that tax debt can hang over your head forever.

The general rule is pretty clear. Once you file a return and the IRS officially assesses the tax, they get ten years to collect it. This decade-long window is called the Collection Statute Expiration Date, or CSED. But without a filed return, there's no CSED for that tax year.

When the Clock Finally Starts

So, how do you get that ten-year countdown going if you haven't filed? The clock only begins ticking once a tax return is officially on the books. This usually happens in one of two ways:

You File Voluntarily: The moment you prepare and send in that past-due return and the IRS accepts it, the ten-year collection period kicks off.

The IRS Files for You: Ignore the problem for too long, and the IRS might eventually file what's known as a Substitute for Return (SFR) on your behalf. While an SFR often calculates a much higher tax bill than you'd owe otherwise, its assessment date can sometimes get that ten-year clock started.

The most important thing to grasp here is that not filing puts you in a state of financial limbo. With no return filed, that ten-year statute of limitations is effectively paused forever, leaving you exposed to IRS collection actions indefinitely.

Situations With No Time Limit

Now, in some pretty serious cases, the statute of limitations might not apply at all—even if you did file. If the IRS can prove you were involved in willful tax evasion or submitted a fraudulent return, there is no time limit on collections or even criminal charges.

This is exactly why getting back into compliance voluntarily is so crucial. Filing your old returns shows good faith and is a huge part of learning how to avoid an IRS audit or worse.

Hiding from the IRS only digs a deeper hole, as they view deliberate evasion far more severely than simple mistakes. Never filing leaves the door wide open for a lifetime of potential liability.

Your Practical Roadmap Back to Tax Compliance

Falling behind on your taxes can feel overwhelming, like you're stuck in a dense fog with no idea which way to turn. I've seen it countless times. But no matter how long it’s been, there's always a clear path back to solid ground.

The secret is to stop letting the problem paralyze you and start taking small, deliberate steps. Let's walk through that roadmap together.

First things first: you need to gather your records. Don't panic if you can't find old W-2s or 1099s—that’s a common hurdle. The IRS actually makes this part surprisingly easy. You can request a free wage and income transcript for any past year directly from their website.

This document is a lifesaver, as it lists all the income information the government has on file for you, giving you the raw data needed to prepare accurate returns.

Getting Your Back Taxes Prepared and Filed

With your income transcripts in hand, it's time to actually prepare the overdue returns. Here’s a crucial detail: you can't just use the current year's tax forms. If you're filing for 2018, you have to use the 2018 forms and play by 2018's rules.

Once the returns are filled out, you need to physically mail them to the correct IRS service center. Unfortunately, e-filing isn't an option for most back taxes. I always tell my clients to send them via certified mail with a return receipt requested.

That little green card you get back is your definitive proof that the IRS received your filing, a critical piece of evidence that officially starts the clock on getting you back into compliance.

The absolute biggest mistake you can make is to continue doing nothing. By taking proactive steps, no matter how small, you immediately shift from a position of vulnerability to one of control. Filing voluntarily shows the IRS good faith and unlocks resolution options that simply aren't on the table if you wait for them to come after you.

How to Tackle the Tax Bill That Follows

After the IRS processes your returns, you’ll eventually get a formal notice—the bill. It will detail the total amount you owe, which includes the original tax plus all the accrued penalties and interest. If looking at that number makes your stomach drop, take a breath. Paying it all at once is often unrealistic, and the IRS knows this. You have options.

Here are the most common paths forward for managing the debt:

Installment Agreement: Think of this as a payment plan. It allows you to make manageable monthly payments over a set period. For many people with debt under a certain threshold, you can even set this up yourself right on the IRS website.

Offer in Compromise (OIC): An OIC is for those facing true financial hardship. It's an agreement with the IRS to settle your tax liability for less than the full amount you owe. They'll take a hard look at your ability to pay, your income, expenses, and assets to see if you qualify. It’s a high bar to clear, but it can be a lifeline.

Currently Not Collectible (CNC) Status: If you genuinely cannot afford to pay anything toward your tax debt, the IRS might place your account in CNC status. This is a temporary pause on collection actions like liens and levies. While it gives you breathing room, be aware that penalties and interest don't stop growing while you're in CNC status. Collections will resume if your financial situation improves.

Common Questions About Unfiled Taxes

When you're dealing with the stress of unfiled taxes, a lot of questions pop up. It can feel overwhelming, but getting clear, straightforward answers is the first step toward finding a solution. Let's tackle some of the most common concerns I hear from clients.

What if I’m Owed a Refund? Can I Still Get It?

Yes, you can—but you have to act fast. The IRS gives you a strict three-year window from the original tax deadline to file and claim your refund.

Miss that deadline, and the money is gone for good. It officially becomes the property of the U.S. Treasury. It’s a classic case of "use it or lose it," and it's surprising how many people leave their own money on the table simply by waiting too long.

I Don't Have My Old W-2s or 1099s. What Now?

This is probably one of the most frequent roadblocks people encounter, but thankfully, it's also one of the easiest to solve. Forget digging through old files or calling past employers.

The IRS keeps its own records. You can go directly to the IRS website and use their "Get Transcript" tool. In a few clicks, you can request a free wage and income transcript that shows every bit of income reported under your Social Security number for a given year. It has all the numbers you need.

A lot of people worry that filing old returns will automatically put them on the IRS's audit radar. In my experience, the opposite is true. Voluntarily coming forward to get compliant looks much better than waiting for them to track you down. The real risk lies in doing nothing.

Am I Going to Jail for Not Filing?

This is the big one—the fear that keeps people up at night. Let me put your mind at ease: for the average person who simply fell behind, jail time is extremely unlikely.

Criminal charges are reserved for the most serious cases of willful tax evasion. This isn't just forgetting to file; this is about intentionally lying, hiding income, or using fraudulent schemes to deceive the government.

For most, the consequences are purely financial penalties and interest. The best way to ensure this never becomes a remote possibility is to take the first step and file those past-due returns.

If you're facing years of unfiled taxes and don't know where to begin, Attorney Stephen A Weisberg can help. I start with a FREE, no-obligation Tax Debt Analysis to determine the best path forward for your specific situation.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034