What Is Offer in Compromise? Save on IRS Debt Today

When a tax bill spirals out of control, it can feel like you’re trapped with no way out. The sheer size of the debt seems impossible to tackle. This is where an Offer in Compromise (OIC) can come into play. It’s an agreement you make directly with the IRS to settle your tax liability for less than the full amount you owe.

This isn't a handout or a simple forgiveness program. Think of it as a last-resort option for taxpayers facing true financial hardship.

What an Offer in Compromise Really Is

An Offer in Compromise is essentially a negotiation based on financial reality. The IRS is a collection agency, but it’s also a practical one. They understand that if a taxpayer truly has no ability to pay the full amount, it's better for everyone to collect something rather than nothing at all.

To even consider an OIC, the IRS will put your finances under a microscope. They need to see everything—your income, living expenses, the value of your assets, and what you could realistically earn in the future. They are trying to answer one critical question: "What is the absolute maximum we can reasonably collect from this person?"

The final figure from that deep dive becomes the foundation of your offer. The OIC is designed for people who simply cannot get out of their tax mess through other solutions, like a standard payment plan.

Offer in Compromise Key Features at a Glance

For a quick summary, here are the core elements of the IRS Offer in Compromise program.

| Feature | Description |

|---|---|

| Purpose | To resolve a tax liability for less than the full amount owed. |

| Eligibility | Primarily for taxpayers facing genuine financial hardship. |

| Basis for Offer | Based on your ability to pay, determined by income, expenses, and asset equity. |

| Application Form | Requires submitting Form 656, Offer in Compromise . |

| Application Fee | A non-refundable $205 fee is required (waivers available for low-income applicants). |

| Legal Status | A legally binding contract between the taxpayer and the IRS upon acceptance. |

This table provides a snapshot, but the reasons why the IRS accepts an offer are just as important.

Why Would the IRS Ever Settle for Less?

It really boils down to three specific situations. If you don't fit into one of these categories, an OIC is probably not for you.

Doubt as to Collectibility: This is the most common path. It means that based on your financial situation, there's serious doubt the IRS could ever collect the full tax debt. Your income and assets just aren't enough to cover it.

Doubt as to Liability: This is a much rarer case. Here, you're arguing that the tax assessment itself was wrong. You're not just saying you can't pay; you're proving you never should have owed it in the first place.

Effective Tax Administration (ETA): This is a special circumstance. You might have the assets to pay the debt in full, but doing so would create an exceptional economic hardship. This could also apply if there are public policy or equity reasons that make collecting the full amount seem unfair.

The heart of the OIC program is the IRS’s practical understanding that sometimes, collecting a reasonable portion of a debt today is a better outcome than chasing an uncollectible full amount for years to come.

Ultimately, an OIC provides a formal pathway to a fresh start. It requires complete honesty and a lot of detailed paperwork, but for taxpayers who genuinely qualify, it can be a lifesaver.

Do You Qualify for an IRS Offer in Compromise?

Thinking you might be a candidate for an Offer in Compromise (OIC) involves much more than just wanting to settle your tax debt for less. The IRS isn't handing out deals casually; they have a very rigid evaluation process and only say yes under very specific circumstances.

Before you even dream of filling out the application, there are a few basic compliance hurdles you absolutely have to clear. First, you must have filed all your required tax returns. The IRS won't even talk to you if you're not current on your filings.

Second, you have to be up-to-date on all required estimated tax payments for the current year. And finally, if you’re a business owner, you must have made all required federal tax deposits for your employees.

Fail any of these basic checks, and your OIC application will be sent right back to you without a second glance. It's also a non-starter if you have an open bankruptcy case, as bankruptcy proceedings always take priority over an OIC.

The Three Official Grounds for an Offer

Once you're past those initial requirements, your entire argument has to hinge on one of three specific legal grounds. This is the heart of the matter—figuring out which one fits your situation is the most critical part of the entire process.

The IRS will only accept an offer based on:

Doubt as to Collectibility

Doubt as to Liability

Effective Tax Administration

Each of these is a distinct legal argument you have to build and then back up with a mountain of financial proof. If you can't build a strong case under one of these pillars, your offer has almost zero chance of succeeding.

Doubt as to Collectibility

This is, by far, the most common reason for an OIC to be accepted. It’s also the most straightforward. You're essentially proving to the IRS, "Look at my finances. I don't have the assets or the income to ever pay you back in full." The argument is based purely on your financial reality, not on whether the tax is correct.

To see if you qualify, the IRS calculates your Reasonable Collection Potential (RCP). This is their formula for figuring out what they could realistically get from you. It looks at your net monthly income (after they allow for certain living expenses) and combines it with the equity you have in your assets—your home, cars, bank accounts, and so on. If your RCP is less than your total tax debt, you might have a shot.

Think of a self-employed graphic designer who lost half their clients when the market shifted. After paying for food and rent, there's almost nothing left. They don't own much of value. If they owe $50,000, the IRS might look at their situation and agree that collecting the full amount is a long shot. That's a classic case for an offer based on Doubt as to Collectibility. To dig deeper into this, check out our guide on how to qualify for an Offer in Compromise.

Doubt as to Liability

This argument is a much tougher road and far less common. With Doubt as to Liability, you’re not saying you can’t pay—you’re saying you don’t legally owe the tax in the first place. This means you have to present concrete evidence that the IRS made a mistake when they assessed the tax.

Maybe they disallowed legitimate business expenses, or they attributed income to you that belonged to someone else. Whatever the reason, you're challenging the very foundation of the debt, not just your ability to pay it.

An important distinction: Doubt as to Liability is about correcting a mistake in the tax bill. Doubt as to Collectibility is about your inability to pay a bill you agree is correct.

Effective Tax Administration

The last option, Effective Tax Administration (ETA), is for truly exceptional situations. It's a unique argument where you admit you owe the tax and that you technically have enough assets or income to pay it. However, you're arguing that forcing you to pay would create an unfair and unjust economic hardship.

For instance, imagine a taxpayer has enough equity in their home to settle their debt. But selling that home would mean uprooting their disabled child who requires a specially modified living space. While paying is financially possible, doing so would be inequitable and cause undue harm.

The IRS will sometimes grant an ETA offer for these kinds of compelling reasons, but proving your case is incredibly difficult. You have to demonstrate that collection, while possible, would simply be unfair.

Navigating the OIC Application Process

Staring down an Offer in Compromise application can feel like preparing to climb a mountain. It’s intimidating. But the best way to approach it is one step at a time. This isn’t one giant, scary task; it’s a series of smaller, manageable actions that, when done right, build a powerful case for the IRS.

Your journey starts with telling your complete financial story. And I mean complete. This goes way beyond just handing over a few pay stubs. You need to pull back the curtain on your entire financial life so the IRS can see exactly what you can—and can't—afford to pay. That's the whole point of the OIC program.

Gathering Your Financial Life Story

Before you even think about the main application, your first job is to tackle the right financial disclosure form. This is where you lay out all the raw data the IRS will use to run the numbers on your Reasonable Collection Potential (RCP)—the make-or-break figure that decides if your offer has a chance.

There are two main forms, depending on your situation:

Form 433-A (OIC): This is the Collection Information Statement for individuals—wage earners and the self-employed. It’s a deep dive into your personal assets, debts, income, and expenses.

Form 433-B (OIC): This is the business version, the Collection Information Statement for Businesses. It covers your company's assets, cash flow, and operating costs.

Getting these forms right requires meticulous work. You’ll be digging up bank statements, pay stubs, loan agreements, property records, and proof of every single monthly living expense. This is not the place to be clever. Any attempt to hide assets or fudge your income will get your offer thrown out instantly and could land you in even more trouble.

The Application and Initial Payment

With your financial statement ready, it's time for Form 656, Offer in Compromise. This is the official proposal where you tell the IRS how much you’re offering and why you believe they should accept it (most commonly, "Doubt as to Collectibility").

Filing Form 656 isn't free. The IRS requires two things right out of the gate:

A non-refundable $205 application fee.

Your first payment toward the offer itself, which is also non-refundable.

Of course, the IRS knows that someone in serious financial trouble might not have the cash for these upfront costs. You can ask for a waiver for both the fee and the initial payment if your income falls below a certain level. The specifics are in the Low-Income Certification guidelines, which you can find in the Form 656-B booklet.

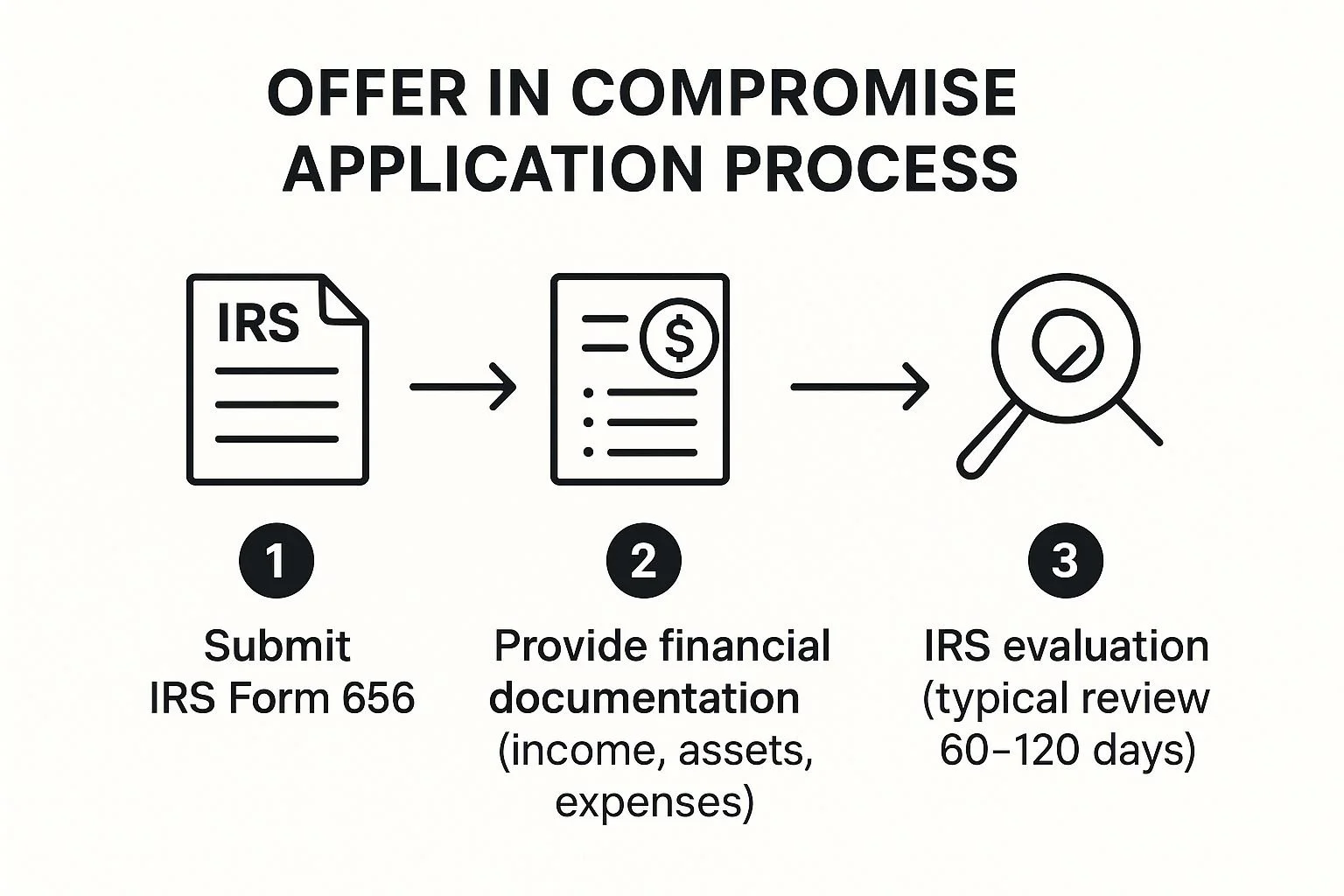

This simple chart breaks down the main stages of getting your offer submitted.

As you can see, the path moves from submitting your initial offer and fee, to backing it up with detailed financial proof, and finally, to the IRS evaluation period.

How to Calculate Your Offer

This is the part that trips up most people. What’s the magic number to offer? It’s not a guess or what you wish you could pay. Your offer has to be at least as much as your RCP. The IRS has a very specific formula for this:

RCP = Your Net Equity in Assets + Your Future Income Potential

Let's unpack that.

First, the IRS looks at your assets—home equity, cars, bank accounts, investments—and calculates their "quick sale value." After subtracting what you owe on them, you get your net equity. Next, they analyze your monthly income and subtract what they consider allowable living expenses, which are based on strict national and local standards. The leftover amount, your "disposable income," is then multiplied by either 12 or 24 months to find your future income potential.

Crucial Point: Your offer isn’t based on how much tax you owe. It’s based entirely on what the IRS determines you can afford after putting your finances under a microscope.

Let’s say you have $5,000 in net asset equity. The IRS determines you have $200 a month in disposable income. For a lump-sum offer, your future income potential would be $2,400 ($200 x 12). That means your minimum offer would have to be $7,400 ($5,000 + $2,400). It doesn’t matter if your tax debt is $50,000 or $150,000; the minimum offer is $7,400.

Getting this calculation right is everything. An offer that’s too low will be dead on arrival. A well-documented and accurately calculated offer is the only way to get the IRS to take your case seriously and turn this intimidating process into a logical, fact-based solution.

The Pros and Cons of an Offer in Compromise

An Offer in Compromise can feel like a life raft when you're drowning in tax debt. It’s a chance to settle what you owe for pennies on the dollar, but it’s not a simple get-out-of-jail-free card. This path is demanding, and you need to go in with your eyes wide open, understanding both the incredible upsides and the serious downsides.

Thinking about an OIC isn’t just about the numbers; it's about whether you’re truly ready for the commitment it requires. Let's break down what you're signing up for.

The Major Advantages of an OIC

The biggest, most obvious win? A real fresh start. A successful OIC lets you legally wipe out a mountain of tax debt for a much smaller amount—one the IRS agrees you can actually afford to pay.

For many people, this is the only realistic way to resolve a tax problem that could otherwise haunt them for a decade or more.

But the relief isn't just financial. The moment the IRS formally accepts your offer, it has to back off. All collection activity stops cold.

Key Takeaway: An approved Offer in Compromise immediately halts IRS levies on your bank accounts and garnishments of your wages. This gives you critical breathing room to get your finances back on track without the constant threat of seizures.

This peace of mind can be just as valuable as the money you save. The constant stress from IRS collection notices and threats takes a huge toll, and an OIC can finally bring that nightmare to an end.

The Serious Drawbacks and Commitments

Now for the hard part. While the benefits are huge, getting an OIC is tough, and the strings attached are non-negotiable. First off, the IRS rejects far more offers than it accepts. They turn down applications for all sorts of reasons, from missing paperwork to simply deciding the offer is too low.

And to even be considered, you have to agree to a full-blown financial colonoscopy. Be prepared to lay your entire financial life on the table for the IRS to inspect. They will dig into your income, your assets, your bank accounts, and even your monthly spending habits to calculate what they think you can pay.

It’s an invasive process. If you’re not comfortable with that level of scrutiny, an OIC is absolutely not for you. You can learn more about what’s involved in our complete guide to tax debt settlement.

Even if your offer gets approved, your obligations are far from over. You're now on probation with the IRS for the next five years.

This is called the five-year compliance period, and during this time, you must:

File every single tax return on time.

Pay every dollar of new tax you owe, on time.

Stick to every term of your OIC agreement perfectly.

Screw up on any of these, and the IRS can yank the deal right out from under you. Your original tax debt comes roaring back to life—with all the interest and penalties re-applied.

One last thing: if the IRS filed a Notice of Federal Tax Lien against you, it’s not going anywhere until your offer amount is paid in full. That lien can make it difficult to sell property or get a loan.

Pros vs. Cons of an IRS Offer in Compromise

Seeing the trade-offs laid out side-by-side can make the decision clearer. Here’s a straightforward look at what you gain versus what you give up.

| Pros (The Upside) | Cons (The Downside) |

|---|---|

| Settle Debt for Less: You can potentially resolve your entire tax liability for a fraction of the original amount. | Low Acceptance Rate: Many applications are rejected, making it a challenging path. |

| Stop Collection Actions: Ends wage garnishments, bank levies, and other aggressive IRS tactics. | Intense Financial Scrutiny: Requires a full disclosure of all your assets, income, and expenses. |

| Achieve a Fresh Start: Provides a clear path to becoming debt-free from the IRS. | 5-Year Compliance Period: You must file and pay all taxes on time for five years after acceptance. |

| Gain Peace of Mind: Alleviates the constant stress and anxiety of dealing with a large tax debt. | Federal Tax Lien Remains: A tax lien stays in place until the offer amount is paid in full. |

At the end of the day, an Offer in Compromise is an incredibly powerful solution, but only for the right person in the right situation. It’s for those who genuinely can't pay their tax debt and are ready to endure the tough process to get to the other side.

What to Expect After You Submit Your Offer

So, you’ve put in the hard work and submitted your Offer in Compromise (OIC) application. It’s a huge step, but it’s important to understand that this is just the beginning of the journey, not the finish line. Sending that package to the IRS kicks off a waiting game, and knowing what’s coming next can make all the difference.

First things first: be patient. This isn't an overnight process. Once the IRS has your application in hand, they start a deep-dive review. Even if your paperwork is flawless, it can easily take several months—and sometimes over a year in complex situations—for them to make a final decision.

The IRS Review Period

During this time, your case will land on the desk of an IRS examiner. Think of this person as a financial detective. Their job is to go through your financial disclosure forms (Form 433-A or 433-B) and all your supporting documents with a fine-tooth comb. They're essentially verifying your story and double-checking your math.

Don't be surprised if the examiner contacts you or your tax professional directly. They might have questions about your living expenses, ask for more recent bank statements, or want more proof of an asset's value. It’s absolutely critical to respond to these requests quickly and completely.

The good news? Once you submit your OIC, the IRS generally suspends most collection activities. This means that while your offer is being considered, they usually won’t start new wage garnishments or hit your bank account with a levy. Be aware, though, that they can still file a Notice of Federal Tax Lien against you during this period.

The Three Potential Outcomes

After the long wait, the IRS will come back with one of three answers: they’ll accept, reject, or return your offer. Each outcome sends you down a completely different road.

Acceptance: The best possible news. The IRS agrees to your offer.

Rejection: They’ve reviewed your finances and decided you don’t qualify or the offer is too low.

Return: A frustrating outcome where your application wasn’t even processed due to a technical error.

Let’s break down what each of these really means and what you should do next.

If Your Offer Is Accepted

Getting that acceptance letter is a moment of pure relief. You’ve successfully negotiated a deal to settle your tax debt for less than you originally owed. But your work isn’t done just yet.

An accepted OIC places you on a five-year probationary period with the IRS. Think of it as being on your best behavior.

During this five-year "compliance period," you absolutely must:

Pay the Offer Amount: Pay the settlement amount you agreed on, following the payment schedule you proposed.

File All Future Returns on Time: No exceptions. For the next five years, every tax return must be filed by its deadline.

Pay All Future Taxes on Time: Any new taxes that come up during these five years must be paid in full and on time.

If you slip up on any of these terms, the IRS can default your agreement. If that happens, your original tax debt—along with all the penalties and interest you thought were gone—comes roaring back to life. For more on building a solid plan, our smart guide to tax relief success offers a broader look at available strategies.

If Your Offer Is Rejected

A rejection means the IRS looked at the substance of your offer and said no. This is different from having your application returned. Usually, a rejection happens because the IRS calculated your Reasonable Collection Potential (RCP) to be higher than your offer, or they simply believe you have the ability to pay the full debt over time.

This isn’t necessarily the end of the road. You have the right to appeal the decision. You have 30 days from the date on the rejection letter to file an appeal with the IRS Office of Appeals. This gives you a chance to make your case to an independent division within the IRS and explain why the original examiner got it wrong.

If Your Offer Is Returned

A returned offer means your application package never even made it to an examiner for review. This is usually due to a simple mistake or a procedural hiccup, such as:

Forgetting to include the $205 application fee (if you didn't qualify for a waiver).

Missing a signature on a required form.

Having an active bankruptcy case.

Not being up-to-date on filing all your required tax returns.

It’s frustrating, but it’s fixable. The IRS will send you a letter explaining exactly why it was returned. You can then correct the issue—whether that’s paying the fee, filing a back tax return, or getting that missing signature—and resubmit the entire application.

Common Questions About the OIC Program

Even after you get the big picture, the little details of an Offer in Compromise can keep you up at night. Let's tackle some of the most practical, real-world questions that pop up for taxpayers navigating this process. Think of this as your go-to guide for those nagging uncertainties.

How Long Does an OIC Decision Take?

If you’re dealing with the IRS, you need to be prepared to play the long game. This is especially true with an Offer in Compromise. Once you’ve sent in that mountain of paperwork, the waiting begins. The IRS officially puts the timeline at six to nine months, but I always tell my clients to treat that as a best-case scenario.

The reality is, the clock moves differently for everyone. A simple case—say, for a regular wage earner with few assets—might wrap up within that timeframe. But if your finances are more tangled, maybe involving a business, multiple properties, or complex income, don't be surprised if it takes over a year. During that entire time, an IRS examiner is going line-by-line through everything you sent.

What if I Cannot Afford the Application Fee?

The IRS gets it. If you're in a financial position to need an OIC in the first place, coming up with the $205 application fee plus the initial payment can feel impossible. That's why they have a waiver specifically for low-income taxpayers.

You can see if you qualify by checking the Low-Income Certification guidelines right in the OIC Booklet (Form 656-B). Essentially, if your total household monthly income is at or below the federal poverty level for your family size, you can likely skip the fee and the first payment. You just have to make sure you fill out that specific section on Form 656 to formally request it.

Important Note: This fee waiver isn't automatic. You have to ask for it and prove you meet the low-income standards when you submit your offer package.

Will an OIC Stop Wage Garnishment Immediately?

Submitting an OIC is a powerful move that can stop collections in their tracks, but it isn't a magic wand. Once the IRS formally accepts your application for processing, the law requires them to pause most collection actions. This means any active wage garnishments or bank levies should stop while they review your offer.

But here’s the catch: the key phrase is "accepted for processing." It can take the IRS several weeks just to get your application logged into their system and officially put a hold on collections. If a garnishment is already happening or about to start, you can't just mail the forms and hope for the best. You or your tax professional must be proactive and communicate directly with the IRS to make sure that collection hold is put in place ASAP.

What if My Offer Is Rejected and an Appeal Fails?

Getting a final "no" on your OIC is tough, but it's not the end of the road. It just means you need to pivot. If both the initial offer and your appeal are rejected, it's time to look at other ways to handle the debt.

Here are the most common alternatives:

Installment Agreement: This is often the next logical step. It lets you pay off the full tax debt through manageable monthly payments over as many as 72 months.

Currently Not Collectible (CNC) Status: If you truly can't afford to pay anything right now, the IRS may place you in CNC status. This is a temporary pause on collections until your financial situation improves.

Penalty Abatement: Sometimes, a huge chunk of your debt is from penalties. If you can show a "reasonable cause" for your tax issues, you can ask the IRS to remove those penalties, which can dramatically lower your total bill.

Exploring the right tax debt solution is the most important thing you can do after a rejected OIC. The good news is that your financial picture may have changed during the long review period, potentially opening up new doors. Don't give up—just regroup and explore the other paths available to finally resolve your debt.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034