What Is Trust Fund Recovery Penalty? Essential Info You Need

Let's get one thing straight about the Trust Fund Recovery Penalty (TFRP): it's the IRS's big stick for holding individuals personally liable when a business fails to pay its payroll taxes. If a company withholds taxes from an employee's check but never sends that money to the government, the TFRP lets the IRS come after the personal assets of the people in charge.

Decoding the Trust Fund Recovery Penalty

Think of it like this: the taxes withheld from an employee’s paycheck are held in a special "trust" for the government. These specific funds, known as trust fund taxes, were never the business's money in the first place. The employer is just a middleman, a custodian.

So when a business owner dips into that trust fund to cover other expenses—like rent, vendor payments, or even their own salary—it's a major breach of trust. This is where the IRS draws a hard line, and the TFRP isn't just another fine. It's a direct collection tool.

What Are Trust Fund Taxes?

The TFRP only applies to a specific part of payroll taxes—the portion withheld directly from an employee's wages. It's a critical distinction to grasp. The taxes in question are:

Federal Income Tax: The amount taken from each employee's check to cover their personal income tax.

Employee's Share of Social Security and Medicare (FICA): The percentage deducted from an employee's gross pay to fund these federal programs.

What's not included? The employer's matching share of Social Security and Medicare taxes. While the business absolutely still owes that money, the IRS can't use the TFRP to collect it from an individual's personal accounts.

To give you a clearer picture, here's a quick breakdown of what the TFRP covers and what it means for you if you're deemed a responsible person.

Quick Guide to the Trust Fund Recovery Penalty

This table shows just how serious the TFRP is. It’s not just an additional penalty; it’s a direct transfer of the business's tax debt to an individual.

Why This Penalty Is So Severe

The IRS pursues the TFRP so aggressively because, in its eyes, failing to remit trust fund taxes isn't just a misstep—it's a form of theft. That money belongs to the employee and the U.S. Treasury, and using it for anything else is a serious offense.

This penalty completely shatters the corporate veil. The liability protection you thought you had with your LLC or corporation? It doesn't apply here. The debt jumps from the business right into your personal financial life.

You can explore our newsletter for a deeper dive into understanding the trust fund recovery penalty and its far-reaching consequences. Getting a handle on these basics is crucial before we look at exactly who the IRS can hold responsible.

Who the IRS Considers a Responsible Person

When the IRS comes looking for unpaid payroll taxes, they aren’t interested in your business card or the corporate org chart. They have one question on their mind: who had control?

The entire process of assessing the Trust Fund Recovery Penalty boils down to identifying the responsible person—the individual (or individuals) who had the power and the duty to make sure those taxes got paid.

This is a real-world test, not a formality. Your title as CEO, President, or Treasurer definitely gets the IRS’s attention, but it doesn't automatically mean you're liable. On the flip side, having no official title offers zero protection if your actions show you were the one calling the shots on company finances.

The Real-World Test for Responsibility

So, what does it mean to be a responsible person in the eyes of the IRS? It’s simply someone who had significant control over the company's money. This isn’t about managing the day-to-day grind; it’s about who ultimately held the authority to decide how money was spent. Who held the purse strings?

To figure this out, an IRS Revenue Officer will dig into who had the authority to perform key financial actions, whether they actually did them or not.

The biggest red flags for the IRS include the power to:

Sign company checks or authorize electronic fund transfers.

Decide which bills, vendors, or creditors get paid—and when.

Hire and fire employees, particularly anyone in a financial capacity.

Manage or direct payroll disbursements.

Negotiate with banks or other lenders on behalf of the company.

The IRS is incredibly direct about the stakes here: “if we charge you this penalty, we may take your assets (except exempt assets) to collect the amount owed.” This shows just how focused they are on finding people with actual financial power, not just those with fancy titles.

Beyond the Obvious Roles

Liability can stretch far beyond the business owner or the C-suite. The net the IRS casts for a "responsible person" is surprisingly wide and often catches people who had no idea they were exposed to such a massive personal risk.

Think about these common scenarios:

The Hands-On Office Manager: An office manager, not an owner, has check-signing authority and routinely decides which vendors to pay. If they knowingly paid other bills while letting the tax deposits slide, they could be held personally responsible.

The "Silent" Partner: An investor or partner who isn’t involved in daily operations but has the power to veto payments or tells the manager which bills to prioritize can easily be deemed responsible.

A Board Member: A member of the company's board of directors with the authority to approve major financial decisions could be found liable, even if they're completely detached from the day-to-day business.

This broad definition is often a huge shock, especially when multiple people get tagged.

The Sobering Reality of Shared Liability

One of the most brutal aspects of the Trust Fund Recovery Penalty is that the IRS can, and will, assess it against multiple people for the exact same tax debt. This is what’s known as joint and several liability.

In plain English, this means every single person the IRS deems "responsible" can be held personally on the hook for 100% of the unpaid trust fund taxes. The IRS doesn't care how they get the money; they can pursue collection from any or all of the responsible individuals until the full balance is paid.

For instance, if a business owes $150,000 in trust fund taxes and the IRS determines the owner, the controller, and one board member are all responsible, each of them can be assessed the full $150,000 penalty. The IRS will collect the money from whoever is easiest to collect from.

Understanding if your role puts you in this high-risk category is the first crucial step. The next is to understand the second piece of the puzzle: willfulness.

The Standard for Willful Failure to Pay

Once the IRS pins someone as a "responsible person," they only need to prove one more thing to bring the hammer down with the Trust Fund Recovery Penalty: willfulness. This is where things get tricky for business owners, because the IRS’s definition of “willful” is a lot broader and way less forgiving than what most people think.

It has nothing to do with evil intent or some grand scheme to defraud the government. Not at all.

In the world of the TFRP, a willful act is simply a conscious, voluntary, and intentional decision to pay other bills before paying the IRS. If you knew the payroll taxes were due but used that cash to pay anyone else—no matter how critical that expense seemed—you’ve met the legal standard for willfulness.

The Choice to Pay Other Creditors

Let’s play out a scenario I’ve seen countless times with struggling businesses. Cash is tight. You’ve got just enough in the bank to either make your payroll tax deposit or pay a key supplier who’s threatening to cut you off. You pay the supplier, thinking it's the only way to keep the lights on and maybe, just maybe, turn things around.

It's a tough business decision, but to the IRS, it’s a clear-cut case of willful failure to pay. By choosing the supplier, you knowingly put another creditor ahead of the U.S. Treasury. That one decision is all the proof they need to establish willfulness and come after you, personally, for those unpaid taxes.

Key Takeaway: Willfulness isn't about being a bad person. It's about knowing a tax debt is owed and using company funds to pay other expenses—rent, suppliers, utilities, even employee net paychecks—before settling up with the IRS.

An Analogy for Willfulness

Think of your company's bank account for a second. It's not just one big pot of money. It’s more like a holding tank with two separate pools. The big pool is the business's operating cash. But there's another, smaller pool of money that was withheld from your employees' paychecks. That's the "trust fund."

You are just the temporary guardian of that trust fund money. It never belonged to the business in the first place.

When you dip into that trust fund pool to cover expenses from the business's pool, you've acted willfully. It doesn’t matter if your goal was to save the company. You made an intentional choice to spend money that was never yours to begin with.

The TFRP is specifically designed for these “trust fund taxes” because the government takes it very seriously when you fail to hand over money held in trust for them.

Reckless Disregard Can Also Be Willful

So what happens if you can honestly say you didn't knowingly choose to pay others first? You might not be in the clear. The IRS can still prove willfulness if you acted with reckless disregard.

This is a lower bar that applies when a responsible person:

Should have known there was a serious risk the taxes weren't getting paid.

Failed to do their due diligence to check and make sure the payments were actually being made.

For instance, a CEO might hire a new, green controller to handle payroll and then never once follow up to see if the tax deposits are being made on time. That CEO could be found to have acted with reckless disregard. They had a duty to ensure taxes were paid and simply looked the other way. This "should have known" standard is a potent tool for the IRS, making "I didn't know" a very tough defense to pull off.

How the IRS Assesses and Collects the Penalty

When the IRS comes knocking about unpaid payroll taxes, the process can feel overwhelming and opaque. But it isn't random. The journey from a company's missed tax payment to the IRS trying to seize your personal assets follows a very specific, predictable path.

Knowing these steps is your first line of defense. It demystifies the process and turns a scary, unknown threat into a clear timeline you can navigate.

It all starts when a business gets behind on depositing its payroll taxes. At that point, the case gets assigned to an IRS Revenue Officer. Their first job is simple: figure out who in the company was a “responsible person” and who acted “willfully” in failing to pay the taxes over to the government.

The Investigation and Form 4180 Interview

The Revenue Officer's main tool for this job is the Form 4180 interview. Its official title is long-winded—"Report of Interview with Individual Relative to Trust Fund Recovery Penalty"—but its purpose is brutally direct. This interview is the linchpin of the IRS’s case against you personally.

Don't mistake this for a friendly chat. It's a formal interrogation designed to establish who held the purse strings and had control over the company's finances.

During the interview, the officer will grill you with pointed questions and ask for specific documents to prove who had financial authority. They're looking for hard evidence, such as:

Bank Signature Cards: Whose name is on the list of authorized signers for the business bank accounts?

Corporate Bylaws or Operating Agreements: What do the company’s own legal documents say about who is in charge of financial duties?

Canceled Checks: Who was physically signing checks to pay other bills and suppliers while the tax deposits were being ignored?

Board Meeting Minutes: Was the payroll tax issue ever discussed? Who was present?

The officer is simply connecting the dots between authority and action. They are building a factual picture of who was in a position to pay the taxes but chose to pay other creditors instead.

The Formal Proposal and Your 60-Day Window

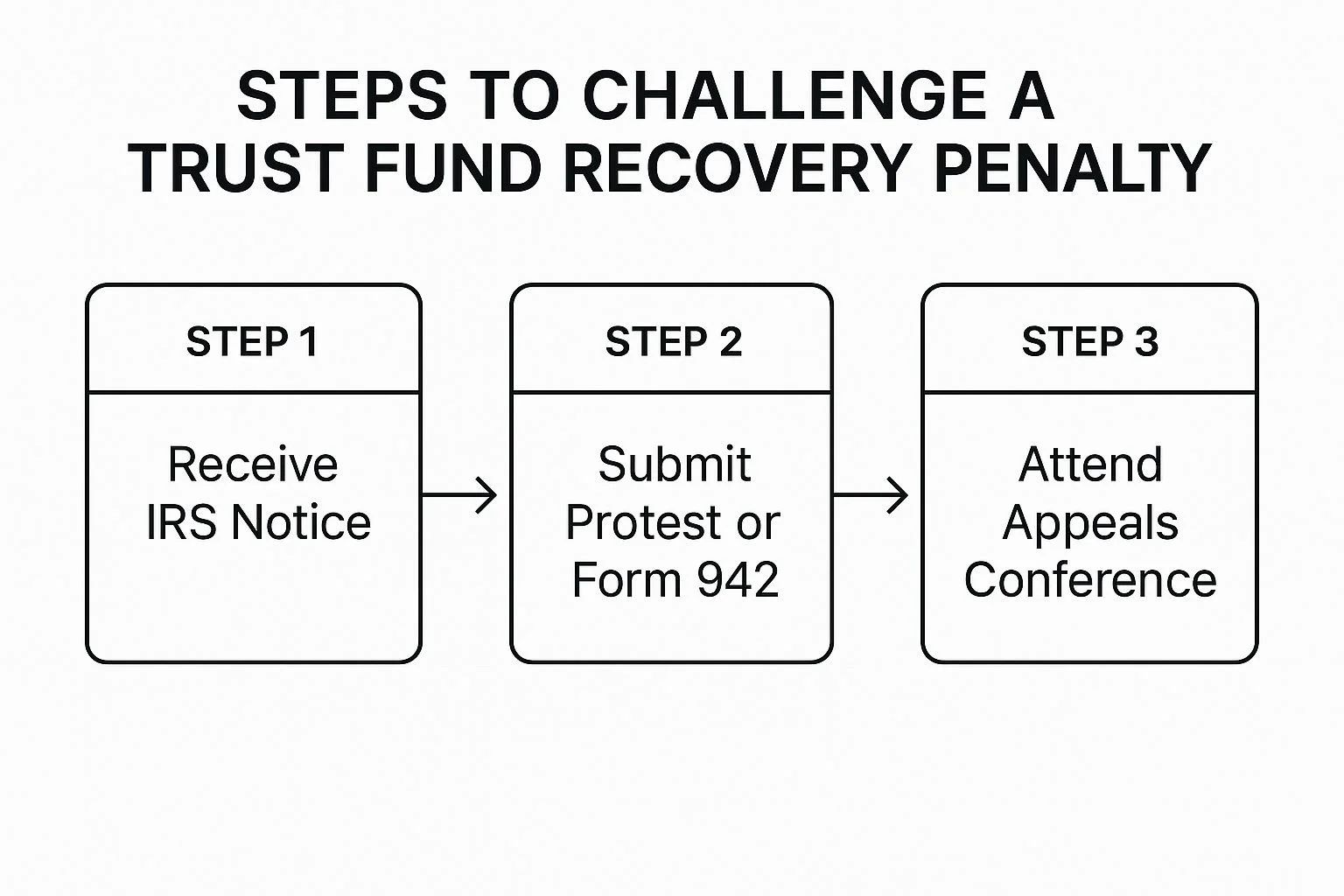

Once the Revenue Officer believes they’ve identified a responsible and willful person, the IRS makes its move. They will formally propose the penalty by mailing you Letter 1153(DO).

This letter is your official warning shot. It's not a final bill yet, but it's close. The letter lays out the proposed penalty amount and, most critically, explains your right to appeal. You have a strict 60-day window from the date on that letter to file a formal, written protest.

Ignoring this notice is one of the worst mistakes you can make. If you let the 60 days pass, you effectively give up your right to challenge the IRS’s conclusions before the penalty becomes a legally enforceable debt against you.

Filing a timely appeal is essential for anyone who feels they've been wrongly targeted.

The infographic below shows how the process flows when you challenge a proposed TFRP.

As you can see, receiving that notice isn't the end of the road. A quick response opens up the entire formal appeals process, giving you a chance to tell your side of the story.

Aggressive IRS Collection Tactics

What happens if you miss the 60-day deadline or lose your appeal? The TFRP is officially "assessed." At that moment, the IRS switches gears from investigation to collection. The problem is no longer a business liability; it's your personal debt.

And the IRS collection toolkit is powerful and aggressive. They can:

File a Federal Tax Lien: This is a public claim against all your personal property, including your home. It craters your credit score and makes it almost impossible to sell property or get a loan.

Levy Your Bank Account: The IRS can take money directly out of your personal checking and savings accounts, and they don't need a court order to do it.

Garnish Your Wages: They can force your employer to send a large chunk of every paycheck directly to them until the debt is paid in full.

Seize Your Assets: In serious cases, the IRS has the power to take physical possession of your personal property—cars, boats, collectibles—and sell them at auction to pay down the tax debt.

This entire process has gotten faster over the years, which means you have less time to react. What used to take the IRS around 18 months to complete now averages about eight months from start to finish. This sped-up timeline means you have to act fast the moment you suspect you're in the IRS's crosshairs for a potential TFRP.

So, How Do You Fight a TFRP Assessment?

When that dreaded Letter 1153(DO) lands on your desk, it’s easy to feel like the fight is already over. It’s not. Think of it as the IRS making its opening statement—now it’s your turn to build a case.

To successfully challenge a Trust Fund Recovery Penalty, you have to systematically poke holes in the two things the IRS must prove: that you were a “responsible person” and that you acted “willfully.” If they can’t prove both, their case falls apart.

Defense #1: "I Wasn't the Responsible Person"

The most straightforward defense is to show you simply didn’t have the authority the IRS claims you did. This has nothing to do with your job title and everything to do with your actual power—or lack thereof—over the company’s checkbook.

The burden of proof is on you to demonstrate you couldn't decide which creditors got paid.

Let's say you're an office manager. Your name is on the bank account, and you sign checks. Sounds bad, right? But if you can only sign checks after the business owner has approved them, you have a strong argument. You lacked the independent authority to be a truly responsible person.

Evidence is everything here. Things like company bylaws, sworn statements from partners, or emails detailing the approval process can be your best friends in proving your case.

Defense #2: "I Didn't Act Willfully"

Okay, what if you clearly fit the definition of a responsible person? Maybe you were the owner or CFO. Your next line of defense is to challenge the "willfulness" claim. This one is trickier because the IRS uses a very broad definition of the word.

A common angle is to prove you were completely unaware the taxes weren't being paid. Simply saying, "I didn't know!" won't cut it. You have to show you had no realistic way of knowing there was a problem. It’s a high bar, but not an impossible one.

Imagine you're a silent partner. You put money into a business but handed all financial duties to a managing partner who fed you doctored reports showing all taxes were current. In that case, you could argue you didn't act willfully because you reasonably relied on the information you were given. You had no reason to suspect anything was wrong.

Crucial Insight: The timing of your actions is critical when arguing against willfulness. If you discover unpaid taxes and immediately use all available company funds to pay the IRS, you can argue you weren't "willful" for payments made to other creditors before you knew about the tax issue.

Another scenario is when you knew taxes were due but were powerless to pay them. This can happen if a lender takes control of the company's bank accounts or if a senior partner explicitly orders you not to pay the IRS, threatening your job if you do.

Other Defenses You Might Have

While attacking the "responsible" and "willful" elements are your main strategies, a few other arguments can sometimes work, though they are often more challenging.

Here is a quick look at the most common defense strategies you can discuss with your tax professional.

Common TFRP Defense Strategies at a Glance

| Defense Strategy | Core Argument | Best Used When... |

|---|---|---|

| Not a Responsible Person | "I lacked the actual authority to decide which bills were paid." | Your job duties were ministerial and you followed orders from others regarding payments. |

| Not Willful | "I was unaware taxes were unpaid, or I was powerless to pay them." | You reasonably relied on false information or were explicitly blocked from making payments. |

| Reasonable Cause | "I exercised ordinary business care but was still unable to pay." | This is a very high standard and rarely successful. An example might be the destruction of records in a fire. |

| Statute of Limitations | "The IRS took too long to assess the penalty." | The IRS missed the three-year window after the Form 941 was filed to assess the TFRP. |

| Calculation Error | "The IRS calculated the penalty amount incorrectly." | You can prove the penalty includes more than just the "trust fund" portion of the taxes. |

These secondary defenses, while less common, should always be on the table. For instance, always, always double-check the IRS's math. The penalty should only be for the trust fund portion—Social Security, Medicare, and withheld income taxes. If they've made a mistake, you can at least reduce the amount you owe.

Facing down the IRS is incredibly stressful, and it's easy to feel overwhelmed. But it’s vital to remember that tax debt is scary, but you have options. Understanding your rights and the arguments at your disposal is the first, most important step toward getting this resolved.

Common Questions About the TFRP

Even after you get the basics down, the Trust Fund Recovery Penalty (TFRP) can feel like a maze. It’s the kind of thing that sends a wave of very specific, very practical questions through the minds of business owners, officers, and financial staff who suddenly find themselves in the IRS’s sights.

Let's cut through the noise and tackle some of the most common questions head-on.

Can I Discharge the TFRP in Bankruptcy?

This is often the first and most desperate question people ask, and unfortunately, the answer is rarely good news. As a general rule, you cannot get rid of a Trust Fund Recovery Penalty by filing for bankruptcy.

The tax code treats the TFRP with a special kind of severity, classifying it as a priority tax debt. This means it’s typically immune to discharge in both Chapter 7 (liquidation) and Chapter 13 (reorganization) bankruptcy filings. Even after you’ve gone through the entire bankruptcy process and other debts are wiped clean, the personal liability for that TFRP will almost certainly still be there, waiting for you. It’s a stark reminder of just how seriously the IRS takes this particular debt.

Can More Than One Person Be Held Liable?

Yes, absolutely. This is a harsh reality that catches many people by surprise. The IRS can, and frequently does, identify multiple "responsible persons" in a business and assess the full TFRP amount against each of them. The legal term for this is joint and several liability.

Here’s how it plays out: Imagine a business has racked up $200,000 in unpaid trust fund taxes. The IRS might investigate and decide the CEO, the COO, and the bookkeeper were all responsible parties. They can then assess a $200,000 penalty against all three of them.

Now, this doesn't mean the IRS can collect $600,000. They are only entitled to the original $200,000 debt. However, they can go after any one—or all three—of the individuals to get it. They'll often zero in on the person with the most accessible assets, regardless of who was "most" at fault.

What Happens if I Ignore the IRS Notices?

Ignoring any letter from the IRS is a bad move. Ignoring a notice about a potential TFRP is a catastrophic one. Pay close attention to Letter 1153(DO), the official proposal of the penalty. The moment you receive it, a clock starts ticking.

You have a strict 60-day window from the date on that letter to file a formal appeal. If you let that deadline pass without action, the penalty is automatically assessed against you personally. There’s no trial, no hearing—it just becomes a legally enforceable debt.

Once it's assessed, the IRS can unleash its powerful collection tools on your personal life. This includes:

Filing a federal tax lien against your property, including your house.

Levying your personal bank accounts (and they don't need a court order).

Garnishing a huge chunk of your wages.

Seizing and selling your personal assets, like cars or other real estate.

Can I Still Be Liable if I Already Left the Company?

Quitting doesn't give you a get-out-of-jail-free card. The IRS’s key question is who was a responsible person during the specific tax periods when the payroll taxes weren't paid.

Let’s say you were the company president with check-signing authority for the first half of the year when the non-payment occurred. If you resigned in July, you can still be held personally liable for that debt from January through June. Your departure doesn't erase what happened on your watch.

It gets even trickier. A common myth is that if you made sure payments were correct while you were there, you're in the clear. But as one Taxpayer Advocate Service case revealed, the IRS can later re-apply payments you made correctly (for withholdings) to the employer's share of taxes, creating a TFRP liability for an officer who had already left the company.

This is why it is so critical to have documentation proving all tax obligations were met at the time of your departure.

How Can I Proactively Avoid TFRP Issues?

The best defense is a great offense. The simplest way to steer clear of the TFRP is to have rock-solid financial practices in place from the start. Meticulous records are non-negotiable, and the right tools can be a lifesaver. You can explore top free bookkeeping software options to get your systems in order.

Beyond software, it comes down to smart internal controls:

Segregation of Duties: The person who authorizes payroll should never be the same person who reconciles the bank accounts. This simple separation prevents a lot of trouble.

Regular Audits: Don't just set it and forget it. Periodically review your payroll records and confirm that IRS deposits are actually being made on time and for the right amounts.

Verify, Don't Trust: Use the IRS's Electronic Federal Tax Payment System (EFTPS) to personally verify that payments have been received. Never assume a third-party payroll service is handling it without checking for yourself.

Putting these practices in place creates a system of checks and balances that can stop the kind of crisis that leads to a devastating TFRP assessment.

Facing a Trust Fund Recovery Penalty can be one of the most stressful experiences for any business professional. You do not have to navigate this complex and intimidating process alone.

Attorney Stephen A Weisberg has over a decade of experience representing individuals and businesses facing serious tax issues with the IRS. Instead of demanding a large upfront retainer, I start with a FREE Tax Debt Analysis to determine exactly how I can help you achieve the best possible outcome.

Facing payroll tax debt right now?

Download my free checklist — Behind on Payroll Taxes? What to Do in the Next 48 Hours — and understand exactly what to do before your situation gets any worse.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034