A Guide to Currently Not Collectible Status

When the IRS comes calling, the pressure can feel immense. But what happens when you genuinely can't afford to pay your tax bill? The IRS has a formal status for this exact situation: Currently Not Collectible, or CNC.

This isn't a get-out-of-jail-free card, but it is a temporary pause on collection efforts. Think of it as the IRS acknowledging that trying to collect from you right now would cause a severe financial hardship, leaving you unable to cover basic living expenses.

What Currently Not Collectible Status Really Means

Let's use an analogy. Imagine your income is a small stream of water, and that water is what you use for everything essential—rent, food, utilities, healthcare.

Your tax debt is a massive boulder the IRS wants to drop into that stream. If doing so would completely dam up the flow and leave you with nothing, the IRS can agree to hold off on dropping the boulder for a while.

That’s the essence of Currently Not Collectible status.

It's a lifeline for taxpayers who are truly struggling. Once you're approved, the most aggressive collection actions—like wage garnishments and bank levies—come to an immediate halt. This gives you some much-needed breathing room to get your financial footing back.

But it's crucial to understand what CNC is not. It doesn't make your debt disappear.

Key Takeaway: While the IRS stops actively collecting, the meter is still running. Your tax debt continues to grow as interest and penalties pile up, which can significantly inflate what you owe over time.

So, while you might not have the IRS breathing down your neck, your tax problem is quietly getting bigger in the background.

To give you a quick snapshot, here are the core components of CNC status.

Quick Overview of Currently Not Collectible (CNC) Status

| Feature | Description |

|---|---|

| Definition | A temporary status granted by the IRS when a taxpayer cannot afford basic living expenses if they pay their tax debt. |

| Primary Benefit | Immediately stops aggressive collection actions like wage garnishments and bank levies. |

| Main Drawback | The tax debt, plus interest and penalties, continues to grow while the account is in CNC status. |

| Key Requirement | Proving economic hardship through a detailed financial analysis of your income, assets, and allowable expenses. |

| Tax Lien | The IRS can still file a Notice of Federal Tax Lien, which can harm your credit and ability to sell property. |

| Duration | CNC is temporary. The IRS will periodically review your financial situation to see if you can resume payments. |

This table shows the trade-offs at a glance. You get immediate relief, but the long-term cost can be high if you don't have a plan.

The Core Concept of Financial Hardship

The entire CNC process hinges on one thing: proving economic hardship. And you can be sure the IRS won't just take your word for it. They're going to want to see the numbers.

To get approved, you'll have to submit detailed financial statements that prove your monthly income is completely eaten up by your necessary living expenses. The IRS has its own set of national and local standards for what it considers "necessary," so it's a very data-driven decision on their end.

Understanding the Trade-Offs

Pursuing CNC status means carefully weighing the pros and cons. It’s a strategic decision, not just a simple fix.

Immediate Relief: This is the biggest pro. The stress of collection calls, garnishment threats, and frozen bank accounts goes away. It's a powerful and immediate benefit.

Growing Debt: Here’s the major downside. That $20,000 debt could easily balloon to $25,000 or more while your account is in CNC status, thanks to compounding interest and penalties.

Potential for a Tax Lien: Even with collections paused, the IRS can—and often does—file a Notice of Federal Tax Lien. This public notice alerts creditors to your debt, which can wreck your credit score and make it nearly impossible to get a loan or sell property.

Is this the right path for you? It depends entirely on your current financial reality and what you expect in the future.

To get a more complete picture of how this status works and whether it’s a viable part of your tax resolution strategy, check out our detailed guide on the currently not collectible IRS program. Remember, CNC is a temporary solution, so having a long-term plan is absolutely essential.

How the IRS Decides If You Qualify for CNC

Getting the IRS to agree you can’t pay isn't as simple as just raising your hand and saying so. They don't take your word for it.

Instead, think of the IRS as a forensic accountant. They'll conduct a deep dive into your finances to see if your claim of financial hardship holds water.

This isn't a gut-feeling decision on their part. It's a cold, hard calculation based on their internal rulebook. The IRS puts your entire financial life under a microscope, comparing every dollar you earn against a rigid set of allowable living expenses.

It’s not about what you actually spend, but what the IRS says you should be spending to maintain a basic, no-frills standard of living.

This framework is designed to ensure that only people who genuinely can't pay without sacrificing food, shelter, and healthcare get this temporary break.

The Financial Formula for Hardship

The entire decision comes down to a straightforward, but unforgiving, formula: Monthly Income - Allowable Monthly Expenses = Disposable Income.

If your disposable income is zero or negative after they run the numbers, you're probably a strong candidate for CNC status.

But the devil is in the details, specifically in what the IRS considers an "allowable" expense. They use a mix of national and local standards to put a cap on what you can claim.

National Standards: These are for basic costs that don’t change much no matter where you live—things like food, clothing, and toiletries. The IRS has a set dollar amount for these based on your family size.

Local Standards: This is where things get specific to your zip code. These standards cover costs like housing and transportation, which vary wildly. The allowable mortgage payment in a major city, for example, is going to be worlds apart from what’s allowed in a rural town.

Other Necessary Expenses: This bucket covers things like health insurance premiums, court-ordered payments (like child support), and essential childcare. As long as they're reasonable, you can typically claim the actual cost.

The IRS isn’t interested in funding a lavish lifestyle. Expenses for things like vacation savings, private school tuition, or expensive hobbies will be disallowed. They are focused solely on what it takes to cover your basic needs.

This standardized method is meant to be fair, but it often means your personal budget doesn't quite line up with the IRS's numbers.

Proving Your Case with Documentation

To get the IRS to accept your financial picture, you have to back it all up with proof. You’ll need to fill out a Collection Information Statement (either Form 433-A or 433-F for individuals) and provide documentation for every single number you put down. Think of it as building a case—a strong one is built on organized, credible evidence.

Get ready to gather copies of:

Recent pay stubs or proof of self-employment income

Bank statements from the last few months

Your mortgage statement or rental agreement

Utility bills (gas, electricity, water)

Car loan or lease statements

Proof of what you pay for health insurance

Records of any other significant, necessary expenses

If you don't provide this paperwork, the IRS will simply reject your claimed expenses. That means your request for currently not collectible status will likely be dead in the water. Honesty and thoroughness are your best friends here.

How Assets Affect Your Eligibility

It’s not just about your monthly income and bills. The IRS also takes a hard look at your assets. What they really care about is your equity—the amount of cash you could pull out of an asset to pay down your tax debt.

Just owning a home or a car won't automatically disqualify you. The IRS wants to know how much equity you have. If you're sitting on a pile of cash in a non-essential asset, they'll expect you to use that to pay your taxes before they'll even consider CNC status. For most people in a tight spot, this isn't an issue, but it's a critical part of their review.

Believe it or not, CNC status is quite common. Reports show that roughly 10 million taxpayers in the U.S. have had their accounts flagged as uncollectible at some point, often due to a sudden job loss or medical crisis. You can read more about the scope of CNC status from these findings on Plunkett Cooney.

Ultimately, if the math shows that paying your tax bill would make it impossible to cover basic necessities, the IRS will likely approve your request.

For those in this tough position, it’s also smart to look at other options. For instance, understanding how to qualify for an Offer in Compromise could give you a path to settling your debt for good, often for much less than you originally owed.

How to Request Currently Not Collectible Status

Asking the IRS to place your account in Currently Not Collectible status is a formal process. You have to be organized, completely honest, and thorough.

Think of it like presenting your case to a judge—you need to lay out a clear, compelling financial picture that proves genuine hardship. There can't be any room for doubt.

The absolute cornerstone of this process is the Collection Information Statement. This is the official form where you detail your entire financial life for the IRS.

The goal is simple: show them that after you pay for basic, necessary living expenses, you have nothing left over to pay your tax debt.

Identify and Complete the Correct IRS Form

First things first, you need to grab the right form. The IRS has different versions for different taxpayers, and using the wrong one will bring everything to a screeching halt.

Form 433-F (Collection Information Statement): This is the one most people use. It's for individual wage earners and self-employed folks who owe less than $100,000. It’s a bit more streamlined for more straightforward personal financial situations.

Form 433-A (Collection Information Statement for Wage Earners and Self-Employed Individuals): This is the more detailed big brother to the 433-F. The IRS will usually ask for this one if your case is more complex or your debt is on the larger side.

Form 433-B (Collection Information Statement for Businesses): As the name implies, this one is strictly for businesses, like partnerships and corporations, that need to prove their financial state.

Once you know which form is yours, fill it out completely and accurately. Honesty is not optional here. If you misrepresent your income or assets, you’re looking at an immediate rejection and maybe even penalties.

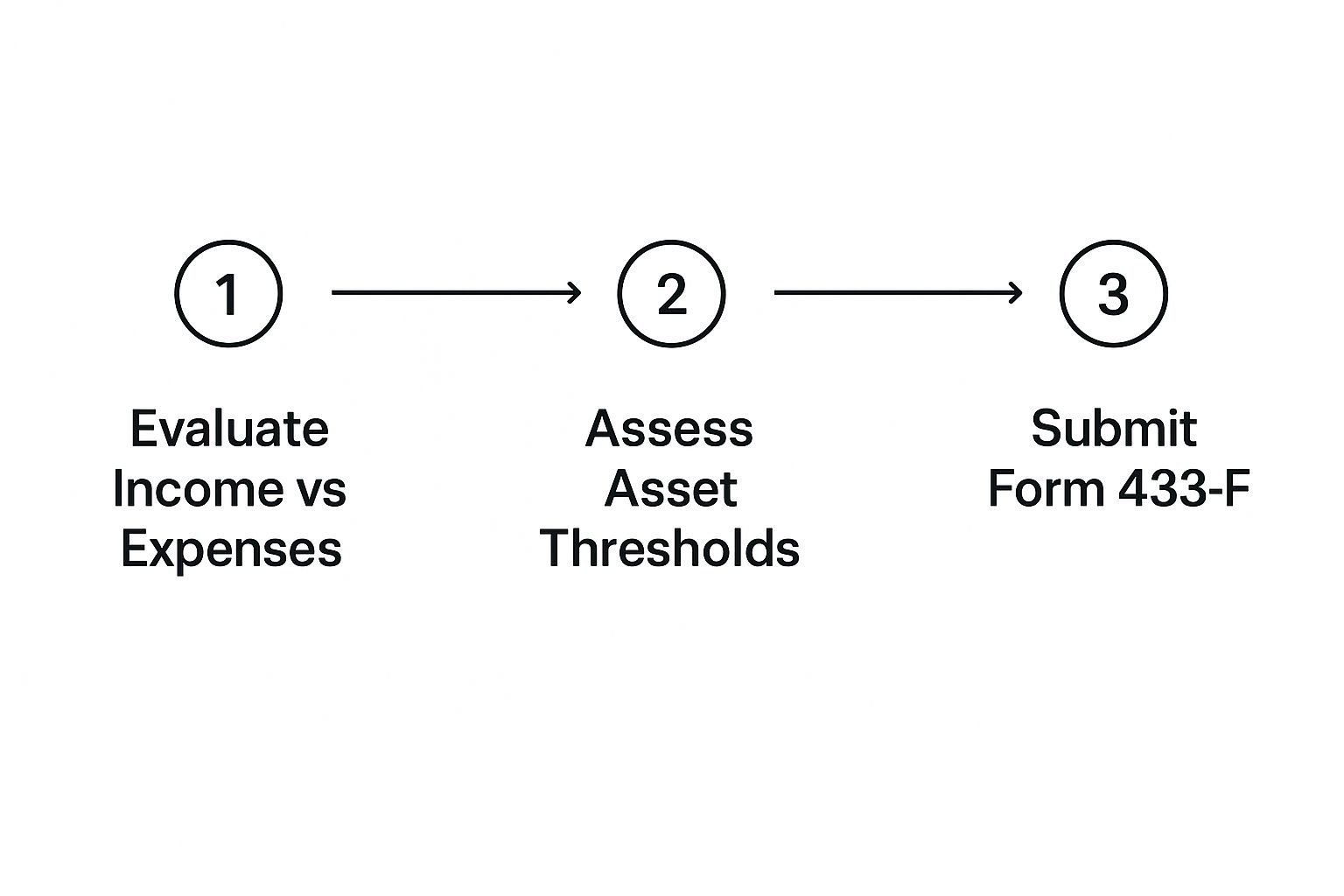

This infographic breaks down the general thought process for qualifying and submitting your request.

As you can see, it all starts with a hard look at your finances and, for most individuals, funnels into completing Form 433-F.

Gather Your Supporting Documentation

Just filling out the form isn't enough—not by a long shot. You have to provide hard evidence to back up every single number you write down. Without proof, the IRS will simply disallow your claimed expenses, which completely sinks your request for currently not collectible status.

Pro Tip: Before you even touch the form, create a dedicated folder (physical or digital) for all your financial documents. Sort everything by category—income, housing, utilities, etc. Trust me, this will make the process infinitely smoother and ensure you don’t forget something critical.

Start gathering these documents right away:

Proof of Income: Your most recent pay stubs are a must. If you're self-employed, you'll need profit and loss statements. Also include statements for any other income you receive, like Social Security or a pension.

Bank Statements: Plan on providing the last three to six months of statements for all your checking and savings accounts.

Housing Expenses: This means your latest mortgage statement or a copy of your current lease agreement.

Utility Bills: Grab recent bills for essentials like electricity, gas, water, and trash collection.

Other Mandatory Payments: You'll need proof of things like health insurance premiums, car payments, or court-ordered payments like child support.

Submit and Follow Up

With your form meticulously filled out and your stack of documents ready, it's time to submit your request to the IRS. You'll typically mail everything to the address listed on the most recent collection notice you received.

Then comes the hard part: waiting. It can easily take the IRS several months to review your case and come to a decision, so patience is key. During this time, don't be surprised if an IRS agent contacts you with some follow-up questions or to ask for more documentation. Your job is to respond quickly and cooperatively.

If your request is approved, the IRS will send you an official notice confirming your account has been placed in currently not collectible status.

Weighing the Benefits and Drawbacks of CNC

Deciding to pursue Currently Not Collectible (CNC) status with the IRS is a major financial crossroads. There are serious trade-offs to consider. It’s definitely not a magic wand that makes your tax debt vanish, but for someone truly backed into a corner, it can be an absolute lifeline.

To make the right call, you have to be brutally honest with yourself and weigh the immediate relief against the very real long-term consequences.

Think of CNC as calling a temporary truce with the IRS. It hits the pause button, giving you precious time to get your financial life back in order without the constant threat of levies and garnishments. That breathing room is its biggest, most powerful benefit.

The Clear Advantages of CNC Status

The most immediate and profound perk of getting into currently not collectible status is the complete stop to enforced collections. This isn't just a minor convenience; for someone barely scraping by, it can be life-changing.

Here’s what that relief looks like in practice:

An End to Wage Garnishments: Your employer stops taking a chunk of your paycheck for the IRS. That means more take-home pay right away, freeing up cash you desperately need for living expenses.

Release of Bank Levies: The IRS will no longer be able to seize money directly from your bank accounts. You can finally pay for rent, food, and utilities without worrying that your account will be wiped out overnight.

A Pause on Aggressive Actions: The relentless, stressful phone calls and intimidating letters stop. The mental and emotional relief from this alone is immense.

This break gives you a chance to stabilize, maybe focus on finding a better-paying job, or handle other debts without the IRS actively draining your bank account. It’s a chance to just catch your breath.

The Serious Downsides of CNC Status

But this temporary peace treaty comes at a cost. The downsides of CNC are significant and can haunt you financially for years if you aren't ready for them. Ignoring these drawbacks is a classic—and costly—mistake.

The biggest problem? Your tax debt doesn't stop growing.

Crucial Warning: While the IRS stops collecting, your tax bill keeps racking up interest and penalties. Your debt will get bigger every single day you're in CNC status, and it can grow surprisingly fast.

This means a $20,000 debt could easily balloon into $25,000 or more after just a year or two in CNC. You're essentially trading today's relief for a much larger headache down the road.

Another huge drawback is the likelihood of a Notice of Federal Tax Lien. Even if the IRS can't take your money, it can still file a public lien against your property. This lien is a flashing red light to all other creditors, and it can:

Destroy your credit score.

Make it almost impossible to get a new loan for a car or a house.

Prevent you from selling or refinancing your home.

That lien stays on the public record until the debt is paid in full, casting a long shadow over your financial life for years to come.

Comparing the Pros and Cons of CNC Status

Sometimes seeing the trade-offs side-by-side makes the decision clearer. This table lays out the good and the bad of CNC status to help you weigh your options.

| Pros of CNC Status | Cons of CNC Status |

|---|---|

| Immediately stops wage garnishments, giving you access to your full paycheck. | Interest and penalties continue to accrue, increasing your total debt over time. |

| Halts bank levies, protecting the funds you need for essential living costs. | The IRS can still file a Notice of Federal Tax Lien, damaging your credit. |

| Provides critical breathing room to address your financial hardship without collection pressure. | The status is temporary; the IRS will periodically review your finances to resume collection. |

| Offers immense psychological relief from the stress of aggressive IRS actions. | Any future tax refunds you are owed will be automatically seized by the IRS to pay down the debt. |

So, is CNC right for you? It’s a careful calculation. If your hardship is genuinely temporary and you have a realistic plan for your income to go up soon, the pause might be exactly what you need.

But if your financial situation is unlikely to get better for the foreseeable future, you could end up with an even bigger, more impossible debt.

The smartest move is to explore every single tax debt solution with a professional who can help you map out the best strategy for your specific situation.

What to Expect While in CNC Status

Getting that approval letter for Currently Not Collectible (CNC) status is a huge relief. The relentless collection notices stop, and you can finally catch your breath. But it's vital to understand this isn't the end of your tax troubles—it's just a new chapter.

Think of your tax debt as being put on a high shelf. It hasn't disappeared, but the IRS has agreed not to actively try and grab it for now. They will, however, peek up at it—and you—from time to time to see if your situation has changed. CNC is a temporary reprieve, not a permanent get-out-of-jail-free card.

At its core, CNC is a conditional pause. The IRS is essentially waiting and watching for any sign that your ability to pay has improved.

The IRS Is Always Watching

Once you're approved for CNC, the IRS doesn't just forget you exist. Their system is set up to automatically monitor your financial health, and their main tool for doing this is the tax return you file each year. This is a non-negotiable part of the deal: you must continue to file all required tax returns on time, every single year, even if you owe money you can't pay.

Certain financial changes can act as red flags, triggering an immediate review of your account and potentially kicking you out of currently not collectible status.

These triggers often include things like:

A big jump in income: Getting a significant raise, landing a much better-paying job, or even a one-time windfall will show up on your next tax return and flag your account for review.

A major drop in expenses: For instance, if you finally pay off a car loan, the IRS computer will assume you now have more disposable income to put toward your tax debt.

Filing a joint return with a higher-earning spouse: When you combine incomes, your household finances might suddenly look healthy enough to start paying again.

If your tax return shows your income has crossed a specific threshold tied to your case's "closing code," the system will automatically switch your account from paused back to active collections.

Important Note: While your account is in CNC status, don't expect a tax refund. The IRS will automatically take any future refunds you're owed and apply them directly to your outstanding tax debt, slowly chipping away at what you owe.

The CSED Clock and Your Debt

Here's where things get really interesting. One of the most powerful, yet widely misunderstood, parts of CNC status involves the Collection Statute Expiration Date (CSED). The IRS typically only has 10 years from the date a tax liability is assessed to collect on it. Once that decade is up, the debt is legally gone. Wiped out.

And here’s the crucial part: while you are in currently not collectible status, that 10-year CSED clock keeps right on ticking.

This opens up an incredible possibility. If your financial hardship lasts long enough, the entire 10-year collection window could expire while your account is on hold.

If that happens, your tax debt dies on the vine, and you owe the IRS nothing for that tax year. For people facing long-term financial struggles, this can turn a temporary pause into a permanent solution simply by running out the clock.

Exploring Your Alternatives to CNC Status

While getting into currently not collectible status offers a critical pause, it's not always the best or only tool in the IRS relief toolkit. It's so important to see it as one potential path, not the only one.

For many people, a more proactive solution that actually resolves the debt—rather than just delaying it—is a much better long-term strategy.

Thinking of CNC as your only option is like having just one play in a football game. To win, you need a full playbook.

Other IRS programs might offer a more permanent resolution, saving you from the stress of watching interest and penalties continue to grow.

Let’s look at some powerful alternatives that could be a much better fit for your financial reality.

Offer in Compromise (OIC)

An Offer in Compromise, or OIC, is often seen as the holy grail of tax relief. If the IRS accepts your offer, it allows you to settle your tax debt for less than you actually owe. This isn't a casual negotiation, though; the IRS uses a strict formula to see if you qualify. They dig deep into your ability to pay, your income, your expenses, and any equity you have in assets.

An OIC is a strong possibility for taxpayers who:

Have a tax debt so large they have no realistic chance of ever paying it off in full.

Are facing genuine, long-term financial hardship, not just a temporary slump.

Can clearly demonstrate that paying the full amount would create a severe economic burden.

Unlike CNC status, which is just a temporary hold, an accepted OIC resolves your debt for good once you've met the terms of the agreement.

Installment Agreement

An Installment Agreement is a much more straightforward solution. At its core, it’s a monthly payment plan that lets you pay your tax debt over time, usually for up to 72 months. This is a fantastic option if you can afford to make consistent monthly payments but just can't come up with the full balance at once.

An Installment Agreement immediately stops aggressive collection actions like wage garnishments and bank levies, as long as you keep up with your payments. It gives you predictability and a clear finish line for getting out of debt without the high bar of proving the severe hardship required for CNC.

This approach is best for people with a steady, reliable income that can cover their living expenses plus a reasonable monthly payment to the IRS. Getting your tax filings in order is crucial, and our guide on how to file back taxes can help you become compliant—a non-negotiable first step for any resolution.

Penalty Abatement

Sometimes, the real monster isn't the tax you originally owed, but the crushing penalties that have piled up over time. If you have a legitimate reason for not filing or paying on time, you might qualify for Penalty Abatement.

The IRS can grant this if you can show reasonable cause, which means you acted with ordinary business care and prudence but were still unable to meet your tax obligations due to circumstances outside your control. Think serious illness, a death in the family, or a natural disaster. There's also a "First-Time Abatement" for taxpayers who have a clean compliance record. While these are tough situations, you can also find real-world inspiration in reading about lessons from avoiding bankruptcy and navigating extreme financial pressure.

Common Questions About Currently Not Collectible Status

It's one thing to understand the textbook definition of currently not collectible status, but it's another thing entirely to know how it plays out in the real world. Once the IRS grants this status, what actually happens? Let's tackle some of the most pressing questions people have.

Will the IRS Take My Tax Refund?

Yes. This is a big one, and the answer is an unequivocal yes. While CNC status means the IRS will stop aggressive collection actions like wage garnishments or bank levies, they will absolutely seize any tax refund you’re owed.

Think of it as an automatic intercept. The system is set up to grab that refund and apply it to your tax bill before it ever gets to you. There's no negotiation on this point; it’s a standard part of the agreement.

How Long Does CNC Status Last?

There isn't a fixed timeline. CNC status isn't a program that lasts for a specific number of years. Instead, it lasts for as long as your financial situation justifies it.

The IRS keeps tabs on your finances, mainly by looking at your income on the tax returns you file each year. If your income stays below their hardship threshold, your account remains in CNC. But if you get a big raise or a new, higher-paying job, you can bet they’ll move to put you back into a collection status.

Key Insight: It is possible for CNC status to last all the way until your tax debt expires. The IRS generally has 10 years to collect, a period known as the Collection Statute Expiration Date (CSED). If your financial hardship continues for that entire decade, the debt can simply be wiped out.

Does CNC Status Stop Interest and Penalties?

No, and this is a crucial—and often costly—misunderstanding. While the harassing collection calls and letters stop, the debt itself keeps growing. Every single day your account is in CNC, interest and penalties are piling up.

This means that if your financial situation improves and the IRS pulls you out of CNC, the amount you owe will be significantly higher than it was when you started. It's the classic trade-off: you get breathing room now, but your total debt gets bigger over time. This is exactly why it's so important to explore all your options before settling on CNC.

If you're facing a tax problem and aren't sure which path is right for you, don't leave it to chance. Attorney Stephen A Weisberg offers a FREE, no-obligation Tax Debt Analysis to evaluate your situation and explain your options clearly.

➥ Contact Attorney Stephen A. Weisberg for a free Tax Debt Analysis.

Contact Me Here: https://www.weisberg.tax/contact-1

Email: s.weisberg@weisberg.tax

Phone/Text: (248) 971-0885

Address: 300 Galleria Officentre, Suite 402, Southfield, MI 48034